Download presentation

Presentation is loading. Please wait.

1

© Worldpanel TM division of TNS 2007 ® Chris Longbottom Director TNS Worldpanel – UK Higher Prices, Higher Volume, Higher Profits: The Business Case For Premiumisation NEC Birmingham 19 September 2007

2

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

3

© Worldpanel TM division of TNS 2007 Data Collection 25,000 Homes!

4

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

5

© Worldpanel TM division of TNS 2007 What is a Premium Brand? A collection of established consumer attributes attached to a product that enhance consumer demand and loyalty and enable the manufacturer to command a price premium Attributes can be tangible or emotional

6

© Worldpanel TM division of TNS 2007 Attributes that consumers will pay more money for Organic Environmentally Friendly Maturity or Freshness (Cheese, Bread) Decaffeination (Tea and Coffee but not Colas?) Granules (Coffee, Cup-a-Soup, Gravy) Mediterranean Lifestyle (Olive Oil, Fish, Tomatoes) Low Fat (Biscuits to Soup?) Speciality/Luxurious/Finest Ingredients Celebrity/Designer/Character endorsement Bacteria (removed - anti-bacterial or added - Yoghurt ) Ethical Trading / Provenance / Local Medicinal /Healthy properties Convenience / Time-saving

Decaffeination (Tea and Coffee but not Colas ) Granules (Coffee, Cup-a-Soup, Gravy) Mediterranean Lifestyle (Olive Oil, Fish, Tomatoes) Low Fat (Biscuits to Soup ) Speciality/Luxurious/Finest Ingredients Celebrity/Designer/Character endorsement Bacteria (removed - anti-bacterial or added - Yoghurt ) Ethical Trading / Provenance / Local Medicinal /Healthy properties Convenience / Time-saving")

7

© Worldpanel TM division of TNS 2007 Bagging and Wrapping Tablets Capsules Gel Glass Spray Concentrated Non Biological Easy Pour Twin Pot Unique Shape Formats that consumers will pay more money for

8

© Worldpanel TM division of TNS 2007

10

Cash-rich – Time-poor

11

© Worldpanel TM division of TNS 2007 What does this mean for Premium Products? If youre employed, youre getting better off! BUT……Things other than Food are absorbing this increase in Living Standards – Travel, Durables, Technology, Housing – Bigger-ticket items Food & Drinks share is diminishing all the time BUT….this is NOT bad for Premium Products Were balancing things more……… Economising on Commodity things……… …..and Indulging in The Better Things in Life When youre used to spending out on big things, whats the problem with a little bit more on Foods & Drinks that you REALLY like?!

12

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

13

© Worldpanel TM division of TNS 2007 Tea

14

© Worldpanel TM division of TNS 2007

15

Bread

16

© Worldpanel TM division of TNS 2007 Economy Premium Organic

17

© Worldpanel TM division of TNS 2007

18

Tomatoes

19

© Worldpanel TM division of TNS 2007

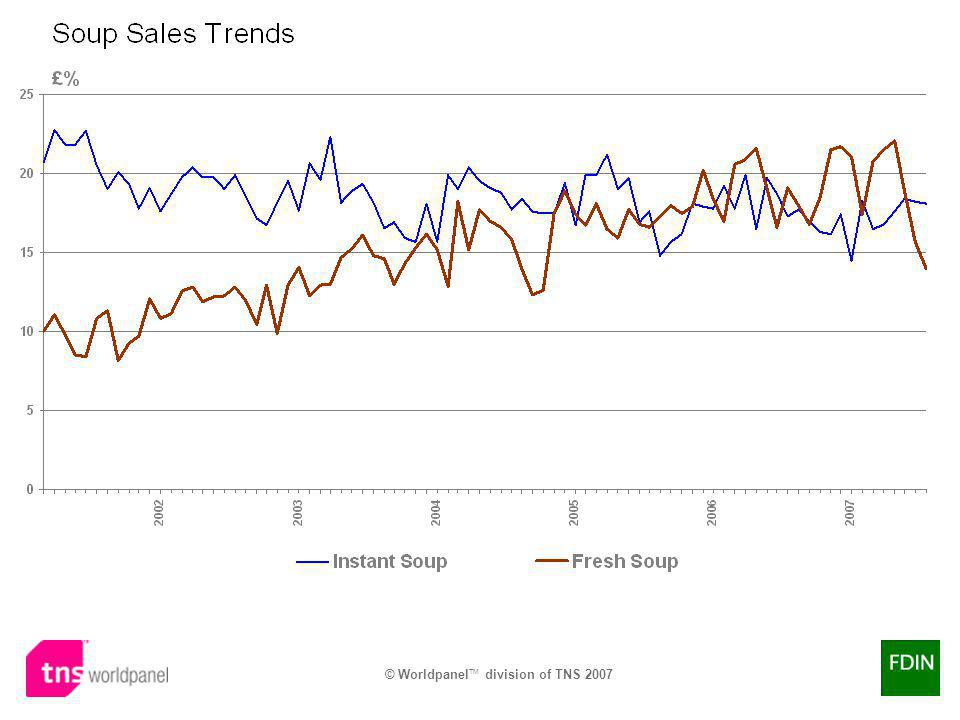

21

Fresh Soup

22

© Worldpanel TM division of TNS 2007

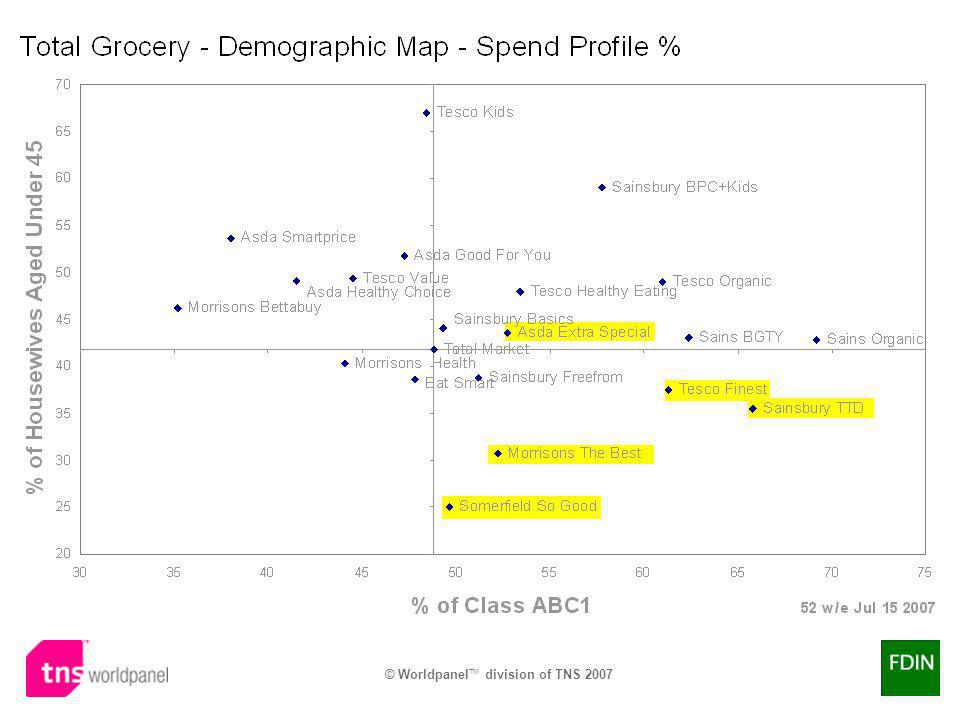

25

Premium Private Label

26

© Worldpanel TM division of TNS 2007 Categories containing Tesco Finest

27

© Worldpanel TM division of TNS 2007 Categories containing JS TTD

28

© Worldpanel TM division of TNS 2007 Categories containing JS Organic / SO Organic

29

© Worldpanel TM division of TNS 2007 Categories containing Asda Extra Special

30

© Worldpanel TM division of TNS 2007 Categories containing Morrisons The Best

31

© Worldpanel TM division of TNS 2007 Over £1.8bn a year & growing……… Christmas is crucial: driven by Festive Food & Drink Tesco Finest £800m JS TTD £625m Asda XS £200m Morr The Best £170m

32

© Worldpanel TM division of TNS 2007

36

Tesco PL Lifestyle Indices Tesco Finest Tesco Value I regard myself as a connoisseur of food and wine 15875 Price is the most important factor when buying a product 76133 Share indexed on Total Trade – 52 w/e Apr 22 2007

37

© Worldpanel TM division of TNS 2007 Sainsbury PL Lifestyle Indices Sainsbury TTD Sainsbury Low Price I regard myself as a connoisseur of food and wine 16098 Price is the most important factor when buying a product 61119 Share indexed on Total Trade – 52 w/e Apr 22 2007 Basics

38

© Worldpanel TM division of TNS 2007 TNS Lifestyles

39

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

40

© Worldpanel TM division of TNS 2007

44

Lifestyles – Innocent Smoothies Spend indexed on Households – 52 w/e Aug 12 2007

45

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

46

© Worldpanel TM division of TNS 2007

48

Chilled Fish vs Frozen Fish Average price per Kg 52 w/e Aug 12 2007 +3% +7%

49

© Worldpanel TM division of TNS 2007

51

Chilled Fish Lifestyle Indices Sector Share indexed on Chilled + Frozen Fish – 52 w/e Aug 12 2007

52

© Worldpanel TM division of TNS 2007 Frozen Fish Lifestyle Indices Sector Share indexed on Chilled + Frozen Fish – 52 w/e Aug 12 2007

53

© Worldpanel TM division of TNS 2007 Fish Lifestyle Indices ChilledFrozen I regard myself as a connoisseur of food and wine 12368 Price is the most important factor when buying a product 88115 Share indexed on Total Fish – 52 w/e Aug 12 2007

54

© Worldpanel TM division of TNS 2007 Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

55

© Worldpanel TM division of TNS 2007

57

Lifestyles – Prepacked Fruit & Vegetables Prepacked Spend indexed on Loose – 52 w/e Aug 12 2007

58

© Worldpanel TM division of TNS 2007

60

Prepared Fruit Classic Salad Luxury Fruit Salad Melon Medley Pineapple Chunks Pineapple Slices Fruit Selection Pineapple Pieces Sliced Melon Selection Fresh Fruit Salad Fruit Salad Melon+Grape Mango Chunks Tropical Fruit Salad Melon Selection Mixed Fruit Salad Sunshine Fruit Salad Seasonal Melon Medley Fruit Medley Apple Slices+Grapes Apple+Grape Exotic Fruit Salads Apple Segments Grape+Melon Mango Pieces Pineapple Cubes Melon Slice Red Grape Watermelon Pineapple Pineapple Rings

61

© Worldpanel TM division of TNS 2007 Lifestyles – Prepared Fruit Spend indexed on Households – 52 w/e Aug 12 2007

62

© Worldpanel TM division of TNS 2007

63

Leafy Salads Sweet+Crunchy Salad Iceberg Lettuce Watercress Italian Salad Crispy Salad Caesar Salad Mixed Salad Rocket Salad Herb Salad Rocket Bistro Salad Baby Leaf Salad Alfresco Salad Spinach+Watercress+Rocket Sld Crisp Mixed Salad Leaf Salad Four Leaf Salad Tender Leaf Salad Crispy Leaf Salad Mixed Leaf Salad Rocket+Spinach+Watercress Italian Leaf Salad Fine Cut Salad Watercress+Spinach+Rocket Watercress Salad Baby Leaf+Watercress Sld Seasonal Baby Leaf Salad Sweet Leaf Salad Ruby Salad Santa Plum Tomato Salad

64

© Worldpanel TM division of TNS 2007 Lifestyles – Leafy Salads Spend indexed on Households – 52 w/e Aug 12 2007

65

© Worldpanel TM division of TNS 2007

66

Prepared Vegetables Broccoli+Crrt+Cauliflower Sliced Runner Beans Mushroom Stir Fry Vegetable Stir Fry Broccoli+Cauliflower Flrt Carrot Batons Brussel Sprouts Baby Spinach Chinese Veg Stir Fry Bean Sprouts Mixed Vegetable Stir Fry Peas Young Leaf Spinach Runner Beans New Potatoes+Herbs+Butter Vegetable Medley Mini Carrots Mixed Peppers Stir Fry Broccoli Florets Diced Carrot+Swede Spinach Leaves Roast Veg W Herb Lyrd Veg Wth Seasoned Btr Swede+Carrot For Mashing Crunchy Veg Stir Fry Cabbage+Leek Vegetable Selection Cabbage Medley Broccoli+Carrot American Style Salad

67

© Worldpanel TM division of TNS 2007 Lifestyles – Prepared Vegetables Spend indexed on Households – 52 w/e Aug 12 2007

68

© Worldpanel TM division of TNS 2007

69

Agenda Definitions and Drivers Tradition / Quality / Provenance Health Chilled v Frozen Convenience The Ethical Consumer

70

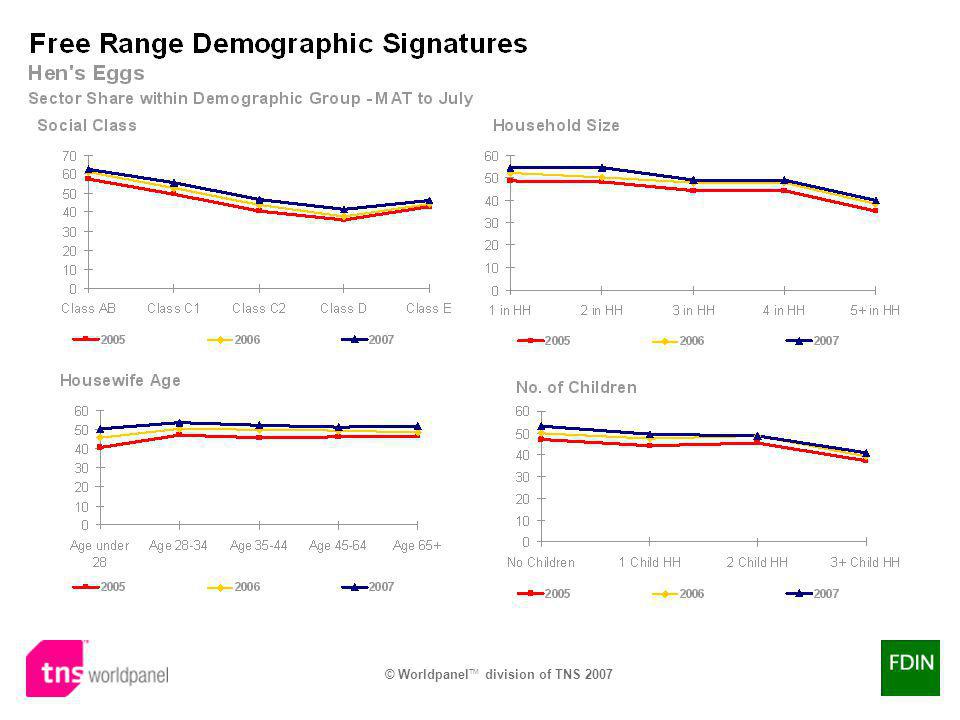

© Worldpanel TM division of TNS 2007 Free Range Eggs

71

© Worldpanel TM division of TNS 2007

74

Lifestyle Indices – Free Range Hens Eggs Share indexed on Total Market – 52 w/e Dec 31 2006

75

© Worldpanel TM division of TNS 2007 Fairtrade

76

© Worldpanel TM division of TNS 2007

77

Lifestyle Indices – Fairtrade Coffee Share indexed on Total Market – 52 w/e Dec 31 2006

78

© Worldpanel TM division of TNS 2007

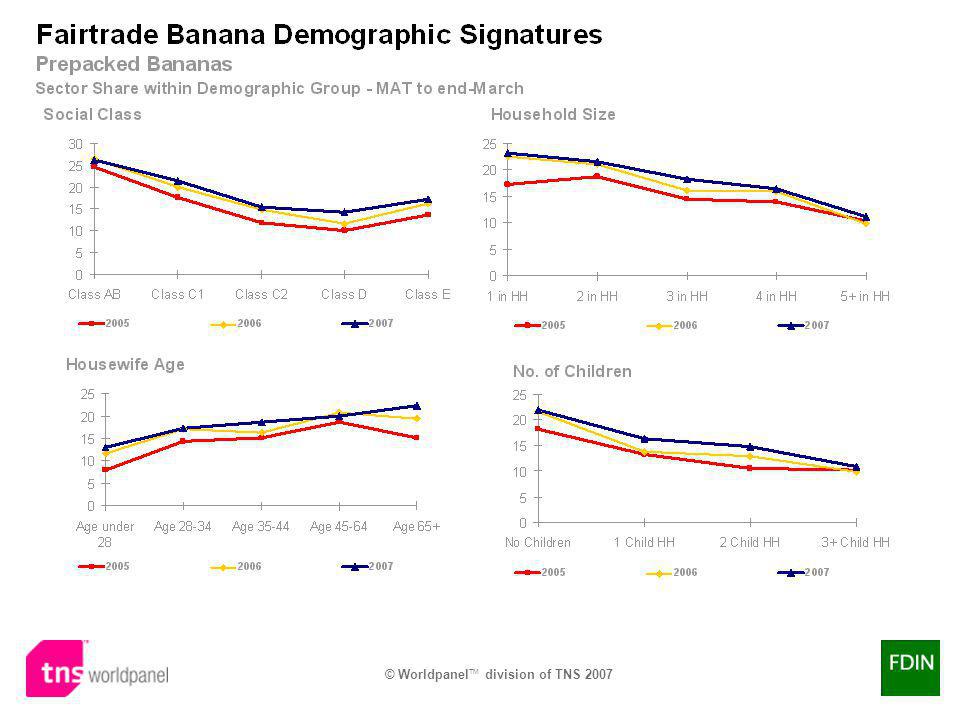

80

Lifestyle Indices – Fairtrade Bananas Share indexed on Total Market – 52 w/e Aug 13 2006

81

© Worldpanel TM division of TNS 2007 As of March 2006, we are converting all the coffee we sell to Fairtrade; we are the only major retailer to do this, with tea to follow later this year. And we are extending our commitment further through areas such as cotton, honey, chocolate, avocados, pineapples, mangoes and bananas. Sainsburys have announced that all its banana supplies will be Fairtrade certified is the biggest ever commitment to date by a single company anywhere in the world. Sainsburys sells 2000 tonnes of bananas (or about 10 million individual bananas ) each week. This move, when completed, will therefore more than double the volume of Fairtrade bananas bought by Britains shoppers.

each week. This move, when completed, will therefore more than double the volume of Fairtrade bananas bought by Britains shoppers..")

82

© Worldpanel TM division of TNS 2007 Organic

83

© Worldpanel TM division of TNS 2007 £ms Total Organic Products Annualised Value = £1.1bn

84

© Worldpanel TM division of TNS 2007 Lifestyle Indices – Total Organic Products Share indexed on All Households – 52 w/e Aug 12 2007

85

© Worldpanel TM division of TNS 2007 Lifestyle Indices – Total Organic Products Share indexed on All Households – 52 w/e Aug 12 2007

86

© Worldpanel TM division of TNS 2007

88

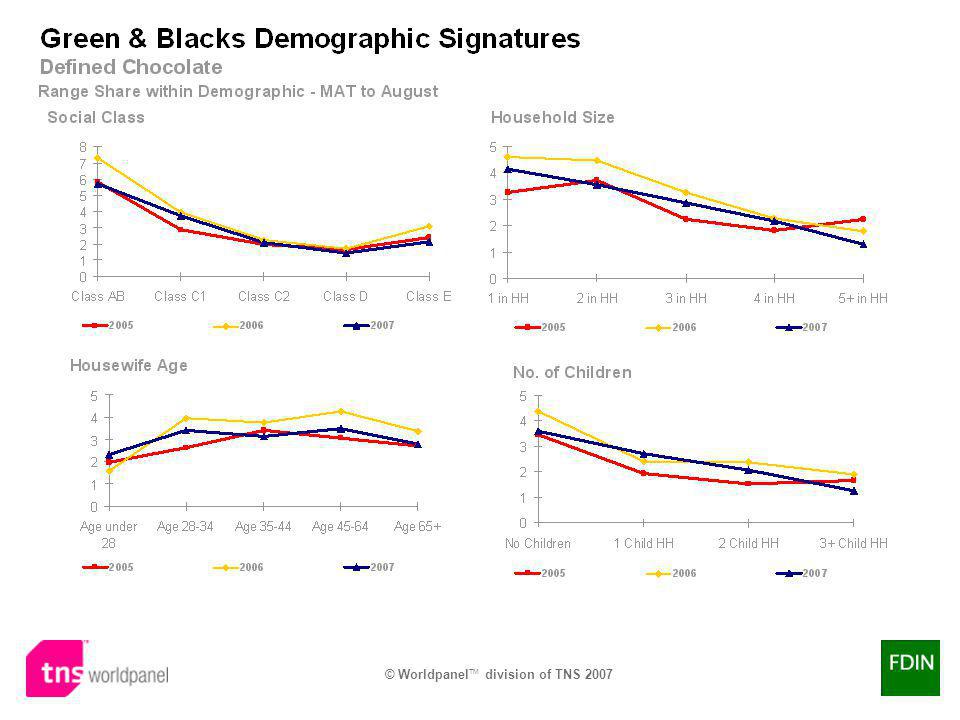

Lifestyle Indices – Green & Blacks Chocolate Share indexed on All Buyers – 52 w/e Aug 12 2007 !

89

© Worldpanel TM division of TNS 2007 BUT……… Organic Foods & Drinks STILL only account for 2% of Total Food & Drinks. More in CERTAIN Categories but negligible in others. Strongest in Fresh Fruit, Veg, & Meat. There has been a plethora of Failed Organic Products where sheer critical mass has proved to be SO difficult to achieve! Beware a simple panacea! Ditto with Fair Trade which is even smaller despite headline- grabbing initiatives where there IS a case. Again beware the dangers of failing to achieve critical mass!

90

© Worldpanel TM division of TNS 2007 Environmentally Friendly

91

© Worldpanel TM division of TNS 2007

92

Lifestyle Indices – Ecover Share indexed on Total Washing-up Liquids – 52 w/e Aug 12 2007

93

© Worldpanel TM division of TNS 2007 Remember the Key Recurring Themes……. Health Practicality = Convenience. Increasingly a Given Enjoyment = Indulgence = Premiumisation Broader Horizons The Right Thing to do, buy, consume = Ethics Nutritional Informing Getting the Balance Right = Credit/Debits in Food Values As Food & Drink become MORE peripheral to our Total Spending, SO its easier to afford just a little bit more for better A small return to Scratch & Homemade Cooking – but not like before!

94

© Worldpanel TM division of TNS 2007 …..and finally

95

© Worldpanel TM division of TNS 2007 ® Switching analysis Outlet Gains & Losses – 12-weekly

96

© Worldpanel TM division of TNS 2007 Arrow Widths Scaled for Size of Net Switch Independents Switching Summary 12 w/e July 15th 2007 vs 2006

97

© Worldpanel TM division of TNS 2007 Changes in MAJOR Switches July 2007 vs July 2005 Netted for Morrisons/Safeway Arrow Widths Scaled for Size of Net Switch Store Transfers 12 w/e 17 July 2005 vs 2004 M&S Independents Note DEcreases in magnitudes of Switches overall 12 w/e July 2007 vs 2006

98

© Worldpanel TM division of TNS 2007 Switching Headlines – July 2007 Tesco: Biggest Gains come from Somerfield, Direct Losses to Sainsburys Asda HAD Disproportionate Gains from Kwik Save, now winning from Somerfield & Morrisons, BUT Losing heavily to Sainsburys Sainsbury winning via Food from Price Players, some losses to Waitrose Morrisons gaining from Somerfield & KS, losing to Asda & Sainsburys Somerfield now losing to Asda & Tesco Iceland, Co-op & Independents losing to Tesco, Iceland & Co-op to Asda & JS too Waitrose gaining from Sainsburys & Tesco – Shoppers upgrading Now that the Kwik Save Switching Benefits are over, What will replace them? Somerfield – even more? Overall, Switching now MUCH LESS than 2 Years ago as Morrisons stabilise Underlying Trend is UPGRADING to MORE Food-Value Retailers

99

© Worldpanel TM division of TNS 2007 Reminders

100

© Worldpanel TM division of TNS 2007 Reminders Definitions and Drivers

101

© Worldpanel TM division of TNS 2007 Tradition Quality Provenance Reminders Definitions and Drivers

102

© Worldpanel TM division of TNS 2007 Definitions and Drivers Health Reminders Tradition Quality Provenance

103

© Worldpanel TM division of TNS 2007 Chilled v Frozen Definitions and Drivers Reminders Tradition Quality Provenance Health

104

© Worldpanel TM division of TNS 2007 Definitions and Drivers Reminders Convenience Tradition Quality Provenance Health Chilled v Frozen

105

© Worldpanel TM division of TNS 2007 The Ethical Consumer Definitions and Drivers Reminders Tradition Quality Provenance Health Chilled v Frozen Convenience

106

© Worldpanel TM division of TNS 2007 The Ethical Consumer Definitions and Drivers Reminders Tradition Quality Provenance Health Chilled v Frozen Convenience

107

© Worldpanel TM division of TNS 2007 Thank you chris.longbottom @tns-global.com

Similar presentations