Download presentation

Presentation is loading. Please wait.

1

Unit 2: Microeconomics: Understanding the Canadian Market Economy

Chapter 4: Demand and Supply Chapter 5: Applications of Demand and Supply Chapter 6: Business Organization and Finance Chapter 7: Production, Firms, and the Market Chapter 8: Resource Economics: The Case of Labour Economics

2

Chapter 5: Applications of Demand and Supply

Overview Elasticity of demand The total revenue approach to elasticity Factors affecting demand elasticity Elasticity of supply Factors affecting supply elasticity Utility Theory Government intervention in markets

3

Introduction This chapter deals with the practical application of the demand and supply concepts discussed in Chapter 4 The ways businesses and governments can use these concepts as a guide in making sound economic judgments

4

Elasticity of Demand Elasticity is the responsiveness of quantities demanded and supplied to changes in price In Chapter 4, we learned that consumers buy more of a product when its price falls and less of it when its prices rises What we did not learn is how much more they will buy or how much less Economists have developed a formula to measure the actual change in quantity demanded for a product whose price has changed

5

Elasticity of Demand The effect of the change is in the numerator (people buying more or less) while the cause is in the denominator (the change in price that affects people’s buying decisions)

while the cause is in the denominator (the change in price that affects people’s buying decisions)")

6

Elasticity of Demand: Gas Station Example

Suppose a large gas station sells 10 million liters of gasoline a month at a price of $0.50 per liter If the station’s owners raise their price to $0.54 per liter, the quantity demanded by the station’s customers falls to 9.5 million liters

7

Elasticity of Demand: Gas Station Example

First, let’s calculate the percent change in price Between the original price of $0.50 and the new price of $0.54, the change is $0.04 Which of these percentages should we use in our calculations? We should compromise by using the average price, which is $0.52 This figure of 7.69 percent will serve as the denominator of our equation

8

Elasticity of Demand: Gas Station Example

To determine the percent change in quantity demanded, we use the average between the original of liters sold and the quantity after the price change Since the quantity demanded fell from 10 to 9.5 million liters, the average quantity demanded is 9.75 million liters. The change in quantity is -0.5 million liters. Therefore, the percent change in quantity demanded is:

9

Elasticity of Demand: Gas Station Example

This figure of 5.13 percent will serve as the numerator of our equation The value of ∆Qd is negative because the quantity demanded falls We ignore the negative sign because we are interested in the amount of change, not the direction We can now use the general formula to determine the coefficient of demand

10

Elasticity of Demand: Gas Station Example

Any coefficient between 0 and 1 is called an inelastic coefficient This is because a given percent change in price causes a smaller percent change in quantity demanded A 7.69 percent change in price causes a 5.13 percent change in quantity demanded

11

Elasticity of Demand: Gas Station Example

Staying with our gasoline example, we find there is a different coefficient for a different set of prices and quantities demanded This is the case even if the change in price ($0.04) and the change in quantity demanded (0.5 million liters) are the same Copy Figure 5.1 into your notes

and the change in quantity demanded (0.5 million liters) are the same. Copy Figure 5.1 into your notes.")

12

Table 5.1: The changing market for gasoline

Price per Litre of Gasoline Quantity Demanded (million litres) Coefficient of Demand $0.50 10.0 0.67 $0.54 9.5 $0.58 9.0 $0.62 8.5 $0.66 8.0 1.1 $0.70 7.5 $0.74 7.0 $0.78 6.5 $0.82 6.0

Coefficient of Demand. $ $ $ $ $ $ $ $ $")

13

Elasticity of Demand: Gas Station Example

Between $0.66 and $0.70, we find the percent change in price is 5.88 per cent We calculate the percent change in quantity demanded as 6.45 percent The coefficient therefore is 1.1

14

Elasticity of Demand: Gas Station Example

Note here that any coefficient greater than 1 is called an elastic coefficient A given percent change in price causes a greater percent change in quantity demanded A 5.88 percent change in price causes a 6.45 percent change in quantity demanded A coefficient that is equal to 1 is called a unitary coefficient because a given percent change in price causes an equal change in quantity demanded

15

The Total Revenue Approach to Elasticity

It’s extremely useful for economics and business people to know whether total revenues will rise or fall when prices rise or fall Will a rise in price mean increased revenues of our gas station owner in spite of the fall in quantity demanded? If the elasticity coefficient is inelastic, then the answer is yes Let’s refer consider whether total revenues rise when owners hike the price per liter of gas from $0.50 to $0.54

16

The Total Revenue Approach to Elasticity

At the original price of $0.50 per liter, the owners sell 10 million liters of gas Total revenue is 10 million liters X $0.50 = $5 million At $0.54, revenues are 9.5 million liters X $0.54 = $5.13 million As always happens with an inelastic demand coefficient, when the price of gasoline rises, the quantity demanded falls at a lower rate (5.13 percent) than the rate at which price rises (7.69 percent) Although people buy less gasoline at the higher price, this potential loss of revenue is compensated for by the greater percent increase in price

than the rate at which price rises (7.69 percent) Although people buy less gasoline at the higher price, this potential loss of revenue is compensated for by the greater percent increase in price.")

17

The Total Revenue Approach to Elasticity

If the price falls again to $0.50, revenues will fall Though people buy more gas at the lower price, this potential revenue increase is offset by the greater percent decrease in price This changes when the coefficient is elastic When prices rise from $0.66 to $0.70 per liter, revenues fall from $5.28 million to $5.25 million The percent rise in price (5.88 percent), with its potential to raise revenues, is undercut by an even greater percent fall in quantity demanded (6.45 percent)

, with its potential to raise revenues, is undercut by an even greater percent fall in quantity demanded (6.45 percent)")

18

The Total Revenue Approach to Elasticity

When price falls with an elastic coefficient, total revenues will rise The percent decrease in price is less than the percent increase in quantity of gasoline purchased When the coefficient is unitary, total revenues are not affected by an increase or decrease in price The percent increases or decreases in price and quantity demanded are the same

19

In Summary Goods with inelastic demand coefficients:

When price rises, total revenues rise When price falls, total revenues fall Goods with elastic demand coefficients: When price rises, total revenues fall When price falls, total revenues rise Goods with unitary demand coefficients: When price rises or falls, total revenues stay the same

20

Factors Affecting Demand Elasticity

Availability of substitutes Goods that have substitutes tend to be more elastic than goods that do not

21

Factors Affecting Demand Elasticity

Nature of the item Goods that are necessities tend to be more inelastic than goods that are considered luxuries A necessity such as bread is inelastic. Price changes do not significantly change the quantities consumers purchase A luxury such as a vacation cruise will be quite elastic because if prices rise, people can do without this kind of vacation

22

Factors Affecting Demand Elasticity

Fraction of income spent on the item Goods that are expensive and take up a large part of the household budget will be elastic If prices rise for big ticket items like houses, cars, or furniture, people either do without the item entirely, postpone the purchase, or search for substitutes An item that takes up a smaller percentage of the budget (ex: shoelaces) is inelastic and may rise in price without registering a significant decline in the amount purchased

is inelastic and may rise in price without registering a significant decline in the amount purchased.")

23

Factors Affecting Demand Elasticity

Amount of time available Over time, some goods may become more elastic because consumers eventually find substitutes for them In the short term, however, demand for these goods can be quite inelastic because consumers may not know what substitutes are available immediately after the price rises

24

Elasticity of Supply As market prices rise, suppliers want to supply more so their profits will increase Can a supplier increase output as easily as consumers decrease demand, or is it more difficult to increase quantity supplied to take advantage of higher prices? Elasticity of supply measures how responsive the quantity supplied by a seller is to a rise or fall in price

25

Elasticity of Supply The formula to determine the coefficient of supply is:

26

Elasticity of Supply: Steel Manufacturer Example

Suppose the market price of steel rises from $120 per tonne to $140 Wishing to take advantage of the higher price, the manufacturer expands production immediately from 1 million tones a day to 1.2 million tones What will the coefficient of supply be?

27

Elasticity of Supply: Steel Manufacturer Example

First, we calculate the percent change in price Just with demand elasticities, we have to find the average of the two prices, which in the case of the steel manufacturer is $130 per tonne The change in price is $20, thus the percent change is:

28

Elasticity of Supply: Steel Manufacturer Example

We must also find the average of the two figures for quantity supplied, which is 1.1 million tonnes The change in quantity supplied is 0.2, thus the percent change is: Using the supply elasticity formula, we can now calculate the coefficient of supply:

29

Elasticity of Supply: Steel Manufacturer Example

The same rules apply to supply coefficients as to demand coefficients Any supply coefficient less than one is classified as inelastic, equal to one is unitary, and more than one is elastic

30

Elasticity of Supply: Steel Manufacturer Example

The steel manufacturer’s ability to increase production supply is elastic within this price range This means that when price increases by a certain percentage (15.38 percent in this case), the manufacturer is able to increase quantity supplied at an even greater rate ( percent) A seller with an elastic supply is better positioned to take advantage of an increase in demand for the product Quantity supplied can easily and quickly be increased to meet demand, resulting in an increase in revenues

, the manufacturer is able to increase quantity supplied at an even greater rate (18.18 percent) A seller with an elastic supply is better positioned to take advantage of an increase in demand for the product. Quantity supplied can easily and quickly be increased to meet demand, resulting in an increase in revenues.")

31

Elasticity of Supply: Steel Manufacturer Example

A price range that has inelastic supply has a supply coefficient of less than one The seller can’t increase the quantity supplied by a greater percentage than the percent increase in price A price range that has a unitary supply elasticity has a coefficient equal to one The seller is just able to match a price increase by the same percentage increase in quantity supplied

32

Factors Affecting Supply Elasticity

Time The longer the time period a seller has to increase production, the more elastic the supply will be In the short term supply is inelastic, and in the long term it is elastic

33

Factors Affecting Supply Elasticity

Ease of storage When the price of a product drops, sellers have 2 choices: They can sell the product at the new lower price They can put some of their inventory into storage and sell it after the price rises again

34

Factors Affecting Supply Elasticity

Cost factors Increasing supply may be costly depending on the industry Manufacturers may be able to increase production in the short term by requiring workers to put in more overtime A permanent increase in production, however, may entail building new factories, which is a far more costly move on the part of the manufacturer Supply is more elastic in industries that have lower input expenses

35

Making Consumption Choices: Utility Theory

In Chapter 4, we saw how a market demand curve is the sum of the many individual demand curves of the consumers who buy a particular product But what factors determine the demand for the products that each of us buys? Is there a rational way of explaining the decisions we make about buying and consuming? Alfred Marshall “the father of supply and demand”put forth the theory known as the marginal utility theory of consumer choice, or utility theory for short

36

Making Consumption Choices: Utility Theory

Lisa has the choice of buying either a veggie burger or frozen yoghurt What factors might influence Lisa in making her choice? First she would probably consider how many veggie burgers she’s had lately If she has had several, she would gain little extra satisfaction from consuming another The economic term for “satisfaction” or “usefulness” is utility The economic term for extra is marginal So the marginal utility Lisa would receive from yet another veggie burger is low

37

Making Consumption Choices: Utility Theory

However if she has bought little frozen yoghurt in the past week, the extra satisfaction she would gain from buying more yoghurt would be higher Since the marginal utility of buying more yoghurt is greater for Lisa than the marginal utility of eating another veggie burger, Lisa would most likely buy the yoghurt

38

Making Consumption Choices: Utility Theory

Suppose, however, that Lisa wanted both veggie burgers and frozen yoghurt We assume that, like most consumers, she wants to maximize her satisfaction, or utility, for the income she has available to spend on these items Suppose she has $10 to spend this week on these two items The burgers cost $2 and the frozen yoghurt costs $1 How should she determine how much of each she should buy?

39

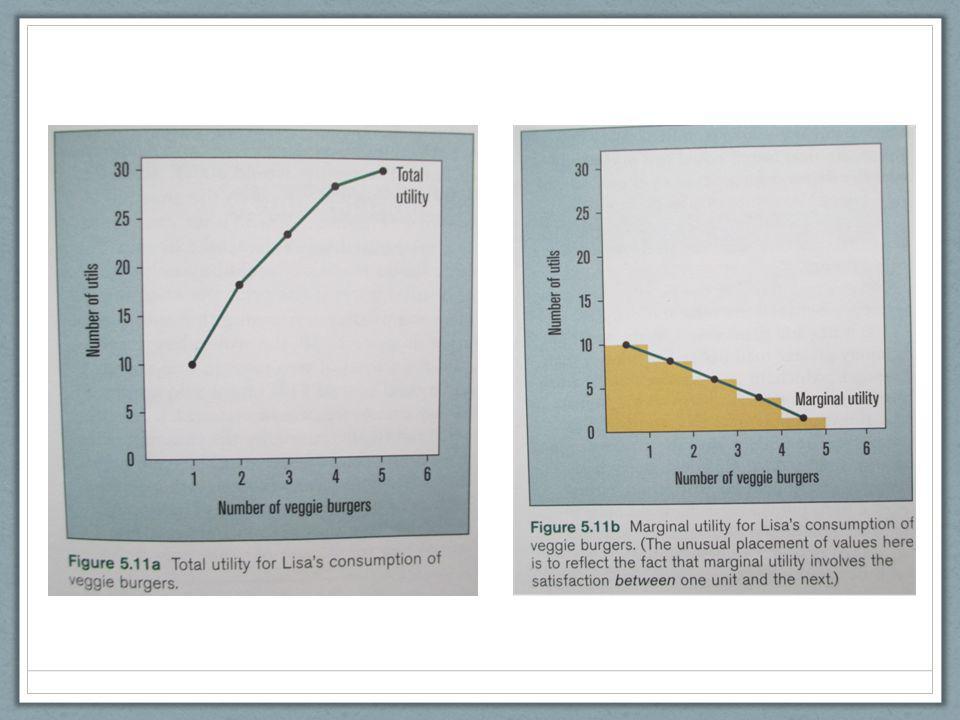

Table 5.10: Lisa’s monthly consumption of veggie burgers and frozen yoghurt

Total Utility Marginal Utility Frozen Yoghurt 1 10 11 2 18 8 7 3 24 6 22 4 28 25 5 30 26

40

Making Consumption Choices: Utility Theory

It arbitrarily assigns numerical values called utils, or units of satisfaction to the burgers and yoghurt We see that the utility Lisa receives from consuming one veggie burger or one frozen yoghurt is high Total utility is 10 utils for one burger and 11 utils for one frozen yoghurt

41

Making Consumption Choices: Utility Theory

For the first unit of the item in question, the marginal utility is always the same as total utility Lisa is gaining 10 utils of extra satisfaction by consuming one veggie burger instead of none and similarly, 11 utils of extra satisfaction by consuming one frozen yoghurt instead of none If Lisa buys a second veggie burger or a second frozen yoghurt, the extra satisfaction she experiences drops slightly to 8 utils for the second burger and 7 for the second frozen yoghurt Her total satisfaction is now 18 utils for two veggie burgers and also 18 utils for the two frozen yoghurts – a total of 36 utils We see the same pattern for the third and fourth veggie burger or frozen yoghurt: marginal utility steadily falls as Lisa consumes one more of either product Total utility continues to rise as more is consumed, but not as quickly

43

Making Consumption Choices: Utility Theory

If Lisa’s budget were unlimited, she could maximize her utility by consuming 5 veggie burgers and 5 frozen yoghurts This would cost her (5 X $2) + (5 X $1) = $15 This combination produces = 56 utils, which is the highest total utility achievable (as shown in Table 5.10)

+ (5 X $1) = $15. This combination produces = 56 utils, which is the highest total utility achievable (as shown in Table 5.10)")

44

Making Consumption Choices: Utility Theory

Since she has limited herself to $10, Lisa must find another combination that will yield her the highest satisfaction, or total utility possible Which combination of veggie burgers and frozen yoghurt will give her the most satisfaction? The formula that yields the answer is the utility maximization formula: MU = marginal utility MU/price signifies the amount of satisfaction received per dollar

45

Table 5.12: Lisa’s marginal utility/price of veggie burgers and frozen yoghurt

MU Price Frozen Yoghurt 1 10 5 11 2 8 4 18 7 3 6 22 25 26

46

Making Consumption Choices: Utility Theory

We can now determine Lisa’s best combination for maximizing her satisfaction She can do so by purchasing 3 veggie burgers and 4 frozen yoghurts because, at these positions, the MU/price is equal for both items Since Lisa is receiving the same amount of satisfaction per dollar for each item, she has no reason to buy more of one and less of the other An economist would say she is in a condition of consumer equilibrium She has spent 3 X $2 = $6 on veggie burgers and 4 X $1 on frozen yoghurt for a total of $10 More importantly, she has maximized her total utility by amassing 49 utils No other combination will give her more total utils within her $10 budget

47

Applications of Utility Theory

The Demand Curve Recall from Chapter 4 that the demand curve slopes downward from top left to bottom right Consumers will buy more only if price falls The theory of marginal utility supports this People consume more, the extra satisfaction they receive declines If people receive less satisfaction as they consume more of a product, they will want to pay less for that product the more they buy it

48

Application of Utility Theory

Adam Smith’s paradox Smith wrestled with an economic problem he was never able to solve, one he called the paradox of value Why, he wondered, are diamonds more costly than water, when water is essential to human life and diamonds are not? Smith could not understand why the demand for a necessity should not be high enough to assure the price is as high as the price for luxury items This paradox remained unsolved until the development of utility theory

49

Application of Utility Theory

The key to unlocking the paradox lies in the difference between the total and marginal utility for water and diamonds Water has greater total utility than diamonds Diamonds are scarce compare to water Satisfaction received from a diamond is extremely high The marginal utility buyers receive from purchasing a diamond means they are willing to pay a high price for something that has little total utility In comparison, the very abundance of water means that most people can consume so much of it that its marginal utility is pushed very low

50

Application of Utility Theory

Consumer Surplus If we examine the concept of marginal utility closely enough, we come to a surprising conclusion: we get a bargain on everything we buy! Economists call this result a consumer surplus Let’s suppose we asked Lisa how many cases of bottled water she would buy at different prices

51

Table 5.13: Lisa’s consumer surplus for bottled water

Price Number of Cases of Water Consumer Surplus $9 1 $9 - $6 = $3 $8 2 $8 - $6 = $2 $7 3 $7 - $6 = $1 $6 4 $6 - $6 = $0

52

Application of Utility Theory

Lisa would buy only 1 case if the price per case was $9 However, if after consuming this 1 case the price dropped to $8, she would buy another A total of 2 cases in one month and a total cost of $17 Lisa would continue to buy 1 more case of water each time the price fell further until, when the price reached $6, she would have bought 4 cases This is a perfect illustration of marginal utility because it demonstrates that Lisa would buy more cases of water only if the price fell

53

Application of Utility Theory

The sellers of bottled water do not drop their prices throughout the month to encourage Lisa to buy more of their product They charge a constant price, say $6 a case Lisa actually receives a surplus for the first 3 cases of bottled water she buys This surplus is calculated by subtracting the amount she would have paid for each case of water from the amount she actually paid

55

Government Intervention in Markets

The market engines of demand and supply automatically produce the vast range of goods and services that consumers want and then distribute these goods and services with a minimum of waste or shortages All this is done without the benefit of any individual or group providing direction for the economy Governments do intervene extensively in the market Why do they do this? Are they threatening the “magic of the market” by intervening?

56

Government Intervention in Markets

Three examples of controversial government actions: If the government believes the people are paying too much for an item, it will introduce a ceiling price If the government believes sellers are receiving too little for a product, it will introduce a floor price If the government believes it must intervene in a market for social or environmental reasons, it will introduce a subsidy or a quota as a solution

57

Ceiling Prices A ceiling price is a restriction placed by a government in order to prevent the price of a product from rising above a certain level If the ceiling price is set below the equilibrium price, a shortage will result

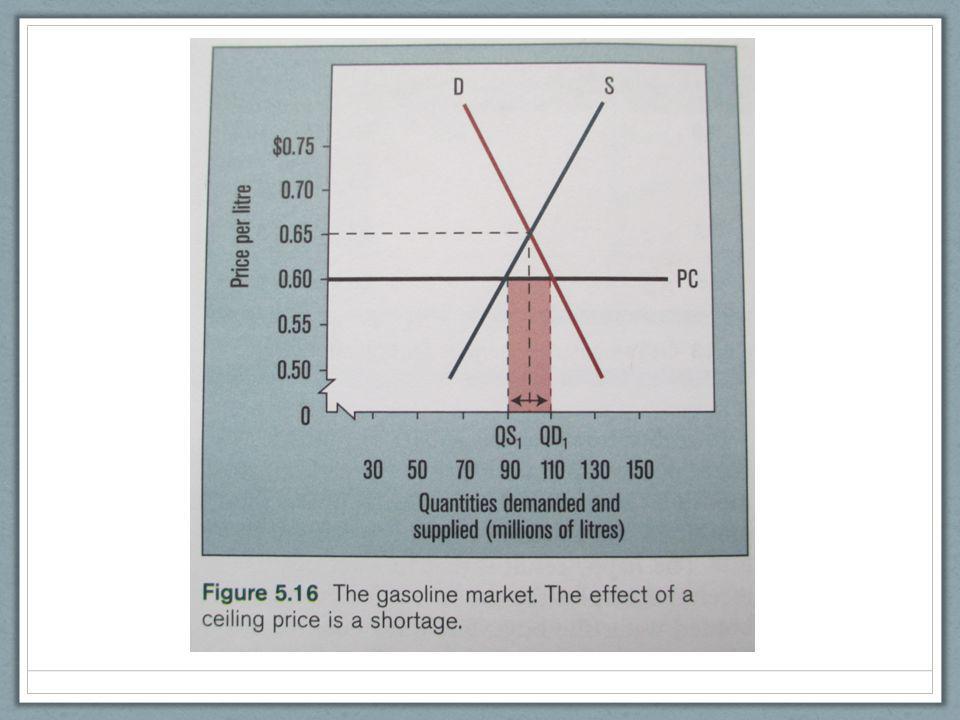

59

Ceiling Prices Suppose an international crisis has interfered with oil supplies and prices start to climb The government, concerned by the hardship these price increases have caused for motorists, places a price ceiling (PC) on gasoline The equilibrium price was $0.65 per litre, with 100 million litres per month demanded and supplied The price ceiling prohibits prices from rising above $0.60 per litre At this price, 110 million litres (QD1) are demanded, and 90 million litres (QS1) are supplied This creates a shortage of QD1 – QS1 = 20 million litres

on gasoline. The equilibrium price was $0.65 per litre, with 100 million litres per month demanded and supplied. The price ceiling prohibits prices from rising above $0.60 per litre. At this price, 110 million litres (QD1) are demanded, and 90 million litres (QS1) are supplied. This creates a shortage of QD1 – QS1 = 20 million litres.")

60

Ceiling Prices There are three possible outcomes of price ceilings:

First, the shortages can cause long lineups for the product Second, price ceilings may create a black market for certain goods A shortage of a product encourages some people to buy up as much of it as they can at the ceiling price, stockpile it, and then sell it at a higher price to people who can’t get enough for their own use Third, price ceilings may cause the quality of a product to suffer if sellers try to reduce their costs in order to make more money This is less likely to occur with natural resource products, but it occurs more frequently for products like rental accommodations

61

Floor Prices A floor price is a restriction that prevents a price from falling below a certain level If the floor price is set above equilibrium price, it will cause a surplus

63

Floor Prices Suppose the government believes that milk producers are making too little profit on milk, priced at $0.50 a litre The government may set a floor price of $0.60 per litre, below which prices are not allowed to fall The line PF is the floor price of $0.60 per litre At that price, 10 million litres will be supplied The higher floor price cuts the quantity demanded to 8 million litres The result, QS1 – QD1, is a surplus of 2 million litres of milk

64

Floor Prices Maintaining the floor price causes two problems:

First, there is the problem of what to do with the surplus In order to keep the floor price at $0.60 per litre, the government must buy the surplus of milk (using taxpayers’ money) Little chance that the surplus will generate a return Cannot be sold within the country at prices below the floor price without undercutting the floor price Surpluses can be sold on the world market or donated to less developed countries Since milk is perishable, it is turned into products that can be stored, such as powdered milk, butter, and cheese

Little chance that the surplus will generate a return. Cannot be sold within the country at prices below the floor price without undercutting the floor price. Surpluses can be sold on the world market or donated to less developed countries. Since milk is perishable, it is turned into products that can be stored, such as powdered milk, butter, and cheese.")

65

Floor Prices Second, consumers pay a higher price for the product and receive less Consumers in an unregulated market would probably have paid the equilibrium price of $0.50 per litre and would have received 9 million litres of milk With the floor price set by the government, they pay $0.60 per litre ($0.10 more) and receive 8 million litres (1 million litres less)

and receive 8 million litres (1 million litres less)")

66

Subsidies and Quotas Subsidies

Both price ceilings and price floors share a common problem: Less of the product is actually transacted between sellers and buyers when these policies force the price away from its equilibrium price In order to avoid this problem, governments sometime enact subsidies A subsidy is a grant of money to a particular industry by the government

68

Subsidies Figure 5.18 shows how the milk market will be affected by a subsidy of $ 0.10 per litre The supply line increases by the amount of the subsidy since producers turn out more milk because they are receiving an extra $0.10 per litre The new equilibrium price of $0.45 is lower than the old equilibrium price of $0.50, and the quantity sold is increased by 3 million litres (from Q1 to Q2)

")

69

Subsidies A subsidy has the advantage of benefiting buyers with lower prices and sellers with extra revenue More of the product is exchanged between buyers and sellers with extra revenue A subsidy has a couple of drawbacks: The taxpayer pays for the program Some critics charge that subsidies keep inefficient producers in business In the global economy, subsidies are often seen as a barrier to fair trade

70

Subsidies and Quotas Quotas

A quota is a restriction placed on the amount of a product that individual producers are allowed to produce Administered by organizations called marketing boards composed of representatives from the government and from the producers

72

Quotas Figure 5.19 illustrates what happens when a provincial marketing board enforces a reduced quota on all milk producers in the province S2 shows the shift in supply to the left P2 is the new, higher price, and Q2 is the new, smaller amount of milk that is actually sold

73

Quotas Quotas set by marketing boards raise farmers’ incomes mainly because food is an inelastic commodity When prices rise on an inelastic product, sales revenue also rises because quantity demanded does not fall by much Farmers were given the authority to establish marketing boards years ago because governments believed that their incomes were, on average, very low Farmers are producing an essential commodity, and if too many of them go out of business, Canadians will wind up paying more for their food

74

Quotas Critics claim that marketing boards raise prices above equilibrium, with the result that less of the product is actually produced and exchanged The fact remains that most of the Canadian meat, vegetables, and dairy products we buy in supermarkets are sold to the stores by marketing boards

75

Rent Controls A rent-control program is a good example of a price ceiling Most Canadian provinces and many American states have enacted such programs, and the controversy that surrounds them never seems to end Rent is the price people pay for accommodation Like any other market price, it is determined by demand and supply

77

Rent Controls Figure 5.20a shows the rent the market sets for the quantity of apartments demanded and supplied in a particular building At $500 for a one-bedroom apartment, the owner will supply 50 apartments The supply line is vertical because the owner can’t increase supply immediately That would involve building more units The supply of apartments is fixed, or perfectly inelastic, in the short term

78

Rent Controls Suppose an increase in renters occurs, shifting demand upwards This encourages the owner to raise rents to $600 a month This increase has 2 effects: Those who can afford the higher rent will stay and pay Those who can’t will have to find less expensive accommodation elsewhere Higher rents mean more profits for the owner, who is therefore encouraged to build more units

80

Rent Controls Figure 5.20b illustrates the effect of this long-term decision to construct another apartment building The supply curve shifts to the right This long-run supply curve, with greater elasticity, also has beneficial effects for renters The supply of apartments is increased, and the rental price, at least in theory, falls to $550 This is how a free rental market works, and both renters and apartment owners appear to win in the long run

81

Rent Controls Suppose that in response to the increase in demand that caused rents to rise to $600 in the short term, the government comes under pressure to alleviate the economic hardship renters are experiencing The government introduces a rent-control program: a law that freezes, reduces, or controls the amount of rent that owners can charge We’ll assume that a freeze on rent for one-bedroom apartments will be fixed at $500

83

Rent Controls Figure 5.21 shows that if demand continues to rise to D2, there will be a shortage of supply of 10 units If this kind of shortage is occurs in buildings everywhere, people will have difficulty finding essential accommodation People looking for an apartment will be tempted to offer building owners more money “under the table” in hopes of beating others to a vacancy Owners, with no incentive to keep buildings in good repair to attract new tenants, may stop making essential repairs and renovations With rental prices fixed, they will also be disinclined to build more units

84

Rent Controls While many people wonder whether rent controls are worth these costs However, without rent control owners are able to raise rent prices to whatever they can get and hold bidding wars between interested tenants

85

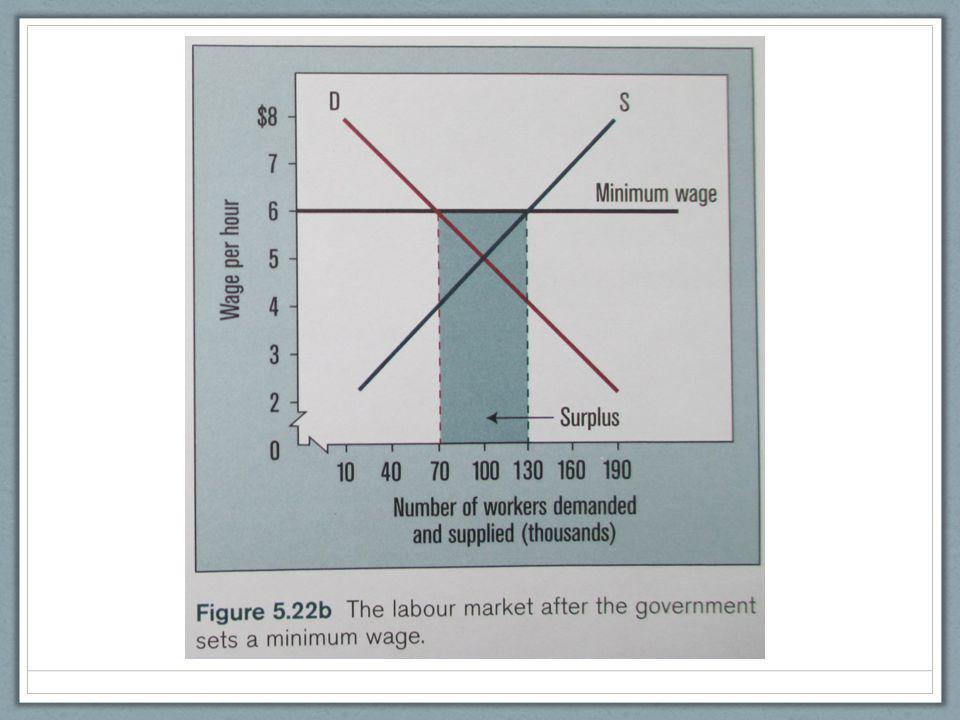

Minimum Wages Governments also intervene to establish floor prices when they believe the price sellers are receiving is too low A wage is the price a worker receives for supplying labour to a business with a demand for it Figure 5.22a shows that 100,000 workers are receiving wages of $5 an hour

87

Minimum Wages Suppose the government responds to public pressure to raise the low wages of these workers by setting a minimum wage A wage that is higher than the one set by the forces of demand and supply Figure 5.22b shows the results of the government’s efforts The minimum wage is set at $6 an hour Businesses adjust to this by employing only 70,000 workers The higher wage rate attracts an additional 30,000 workers into the labour market This is a total of 130,000 workers who are willing to work This means the minimum wage has created an unemployment problem 60,000 workers who can’t find jobs

89

Minimum Wages Floor prices tend to create surpluses

Minimum wages create surpluses of potential workers who cannot find jobs The minimum wage also increases the wages of thousands of people at the low end of the wage scale These people receive a more substantial paycheque than they would have if wages had been set solely by supply and demand

Similar presentations