Download presentation

Presentation is loading. Please wait.

1

Master Template1 Global forecasting service Economic forecast summary – June 2013 www.gfs.eiu.com

2

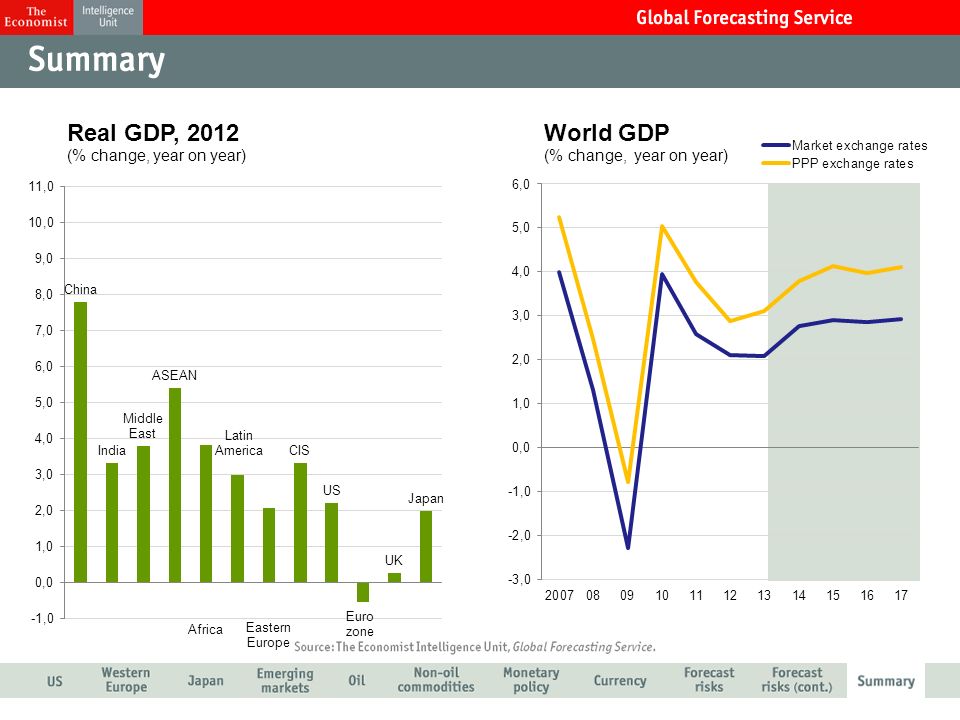

US employers created an average of 208,000 jobs a month between November and April, 50% more than in the previous six months. Fiscal tightening may yet dull the recovery, but US growth is still set to accelerate in the second half of the year. As it stands, public spending cuts are going ahead as planned, since neither party was able to convince the other to compromise. We maintain our GDP growth forecast for 2013 at 2.1%, down slightly from an estimated 2.2% in 2012. We haved raised our 2014 growth forecast to 2.5%.

3

Aggregate unemployment in the currency area is above 12%, and GDP will contract for a second year in 2013. The European Central Bank cut its main interest rate by a quarter percentage point in early May as economies sputtered across the euro zone. The interest-rate cut will have only a minimal effect on growth in the hardest hit countries, where funding costs for companies and households are not expected to fall much. After a period of post-election uncertainty in Italy a broad coalition government was formed in April.

4

We have edged our 2013 growth forecast to 1.2%. Demand will be boosted by the expansionary monetary and fiscal policies of Shinzo Abe. The yen has continued to slide. A weaker yen will provide some relief to Japan’s exporters. It will also contribute to raising the annual inflation rate to around 1.3% between 2014 and 2017. Over the long term the ageing of the population, combined with disorderly public finances, will make it difficult for policymakers to engineer a self- sustaining recovery in domestic demand. The consumption tax rate is scheduled to rise from 5% at present to 8% in April 2014 and then to 10% in October 2015.

5

Following a weak first quarter, we have further reduced our 2013 GDP forecast for China to 7.9% from 8%, after a larger cut from 8.4% last month. The outlook should improve in the coming months, but China has now embarked on a permanently slower growth path as the economy matures and investment declines. We expect India’s growth to pick up in 2013 to 6.5%, after growth of just 3.3% in 2012. Following a slow start to 2013, we have cut our 2013 growth forecast for Russia to 2.8%.

6

Oil consumption growth in 2013 is expected to be a subdued 1.2% reflecting the slowdown in China’s growth and the weak euro zone economies. Overall, consumption growth will average around 1.6% a year in 2013-17, led by the developing world. Geopolitical risks continue to weigh on the supply picture, particularly the tensions between the West and Iran. Still weak demand growth and ample supply will constrain prices in 2013, assuming no unforeseen disruptions to supply or heightened political risk.

7

Demand will remain relatively subdued in 2013, constrained by weak OECD growth and only a modest pick up in China’s consumption Despite somewhat slower growth in non-OECD economies, rising incomes and ongoing urbanisation will underpin medium-term demand growth in industrial raw materials Grains and soybeans prices are expected to weaken in 2013 on improved supply prospects. Nominal commodity prices will remain historically high in 2013-17, but prices will ease in real terms

8

The new governor of the Bank of Japan has announced a massive expansion of QE, with plans to double the monetary base by 2015. The Fed’s current monetary stimulus, a third round of QE, worth US$85bn in monthly bond purchases, is open- ended and will last until at least 2014. The ECB cut its refinancing rate by 25 basis points to 0.5% in May. South Korea, Australia, Poland, India and Denmark have all cut rates in recent weeks. Brazil has embarked on a monetary tightening cycle.

9

A protracted recession and concerns about a resurgence of the debt crisis will remain potential sources of pressure on the euro. The relative outperformance of the US is supporting the dollar, despite headwinds from loose monetary policy, fiscal tightening and a large external funding requirement. Japanese macroeconomic policy will keep the Yen weak. EM currencies should be supported over the medium term by positive growth and interest rate differentials with OECD economies.

10

- One or more countries leave the euro zone - Tensions over currency manipulation lead to protectionism - The global economy falls into recession + A sustained decline in oil prices provides a global economic fillip - Tensions over disputed islands rupture Sino-Japanese ties 16 20 15 12

11

- Social and political disorder undermine stability in China - US economy stumbles in the wake of a wave of fiscal tightening - Economic upheaval leads to widespread social and political unrest - An attack on Iran results in an oil price shock + Co-ordinated monetary stimulus kick-starts a global recovery 10 9 8 8

13

Master Template13 Access analysis on over 200 countries worldwide with the Economist Intelligence Unit T he analysis and content in our reports is derived from our extensive economic, financial, political and business risk analysis of over 203 countries worldwide. You may gain access to this information by signing up, free of charge, at www.eiu.comwww.eiu.com Click on the country name to go straight to the latest analysis of that country: Further reports are available from Economist Intelligence Unit and can be downloaded at www.eiu.comwww.eiu.com G8 Countries * Canada Canada * FranceFrance * GermanyGermany * ItalyItaly * JapanJapan * RussiaRussia * United KingdomUnited Kingdom * United States of AmericaUnited States of America BRIC Countries * BrazilBrazil * RussiaRussia * IndiaIndia * ChinaChina CIVETS Countries * ColombiaColombia * IndonesiaIndonesia * VietnamVietnam * EgyptEgypt * TurkeyTurkey * South AfricaSouth Africa Or view the list of all the countries.view the list of all the countries Should you wish to speak to a sales representative please telephone us: Americas: +1 212 698 9717 Asia: +852 2585 3888 Europe, Middle East & Africa: +44 (0)20 7576 8181 www.gfs.eiu.com

")

14

Master Template14 Access analysis and forecasting of major industries with the Economist Intelligence Unit I n addition to the extensive country coverage the Economist Intelligence Unit provides each month industry and commodities information is also available. The key industry sectors we cover are listed below with links to more information on each of them. www.gfs.eiu.com Automotive Analysis and five-year forecast for the automotive industry throughout the world providing detail on a country by country basis Commodities This service offers analysis for 25 leading commodities. It delivers price forecasts for the next two years with forecasts of factors influencing prices such as production, consumption and stock levels. Analysis and forecasts are split by the two main commodity types: “Industrial raw materials” and “Food, feedstuffs and beverages”. Consumer goods Analysis and five-year forecast for the consumer goods and retail industry throughout the world providing detail on a country by country basis Energy Analysis and five-year forecast for the energy industries throughout the world providing detail on a country by country basis Financial services Analysis and five-year forecast for the financial services industry throughout the world providing detail on a country by country basis Healthcare Analysis and five-year forecast for the healthcare industry throughout the world providing detail on a country by country basis Technology Analysis and five-year forecast for the technology industry throughout the world providing detail on a country by country basis

15

Master Template15 Media Enquiries for the Economist Intelligence Unit www.gfs.eiu.com Europe, Middle East & Africa Grayling PR Jennifer Cole Tel: + 44 (0)20 7592 7933 Sophie Kriefman Tel: +44 (0)20 7592 7924 Ravi Sunnak Tel : +44 (0)207 592 7927 Mobile: + 44 (0)7515 974 786 Email: allgraylingukeiu@grayling.comallgraylingukeiu@grayling.com Asia The Consultancy Tom Engel +852 3114 6337 / +852 9577 7106 tengel@consultancy-pr.com.hk Ian Fok +852 3114 6335 / +852 9348 4484 ifok@consultancy-pr.com.hk Rhonda Taylor +852 3114 6335 rtaylor@consultancy-pr.com.hk Americas Grayling New York Ivette Almeida Tel: +(1) 917-302-9946 Ivette.almeida@grayling.com Katarina Wenk-Bodenmiller Tel: +(1) 646-284-9417 Katarina.Wenk-Bodenmiller@grayling.com Australia and New Zealand Cape Public Relations Telephone: (02) 8218 2190 Sara Crowe M: 0437 161916 sara@capepublicrelations.com Luke Roberts M: 0422 855 930 luke@capepublicrelations.com

Sophie Kriefman Tel: +44 (0) Ravi Sunnak Tel : +44 (0) Mobile: + 44 (0) Asia The Consultancy Tom Engel / Ian Fok / Rhonda Taylor Americas Grayling New York Ivette Almeida Tel: +(1) Katarina Wenk-Bodenmiller Tel: +(1) Australia and New Zealand Cape Public Relations Telephone: (02) Sara Crowe M: Luke Roberts M:")

Similar presentations

: Average sustained growth, with risks Ken Goldstein WWW.CONFERENCE-BOARD.ORG.>")

HSBC Bank Australia Limited +61 (2) 435 966>")