Download presentation

Presentation is loading. Please wait.

1

US Economy Forecast 2011, 2012 Till Schreiber College of William & Mary August 4 th 2011 Nafa Annual Convention, Williamsburg, VA

2

Forecast for 2011, 2012 What would we like to happen? – Deficit deal – Entitlement reform – Fewer but smarter regulations – Less uncertainty – …. What’s actually going to happen? – Not all of that.

3

Realistic forecast must make assumptions about some of these factors No ideological agenda Based on current and historical data, facts (and some theory) Where is the economy now? What do some leading indicators suggest about the near future?

4

Snapshot of the economy Unemployment rate 9.2% – Little job creation – Government sector shedding jobs GDP growth disappointing – Less than 2% in first quarter, likely not better than that for the second quarter Economy slowed down by multiple “headwinds” – Oil (and other commodities) prices – Supply chain disruptions because of Japan – Depressed housing market Inflation expected to be about 2% each year going forward

prices – Supply chain disruptions because of Japan – Depressed housing market Inflation expected to be about 2% each year going forward")

5

Government spending cuts Absolutely necessary over the long term – Unless you are ok with living in a country like France; most Americans don’t seem to be Big cuts right NOW will slow the economy down for the rest of the year – Higher unemployment – Reduction in growth – All bets are off, if debt ceiling is not increased. This would lead to a massive reduction of spending right NOW Assume Assume: Some further cuts this year, no “stimulus” from government sector

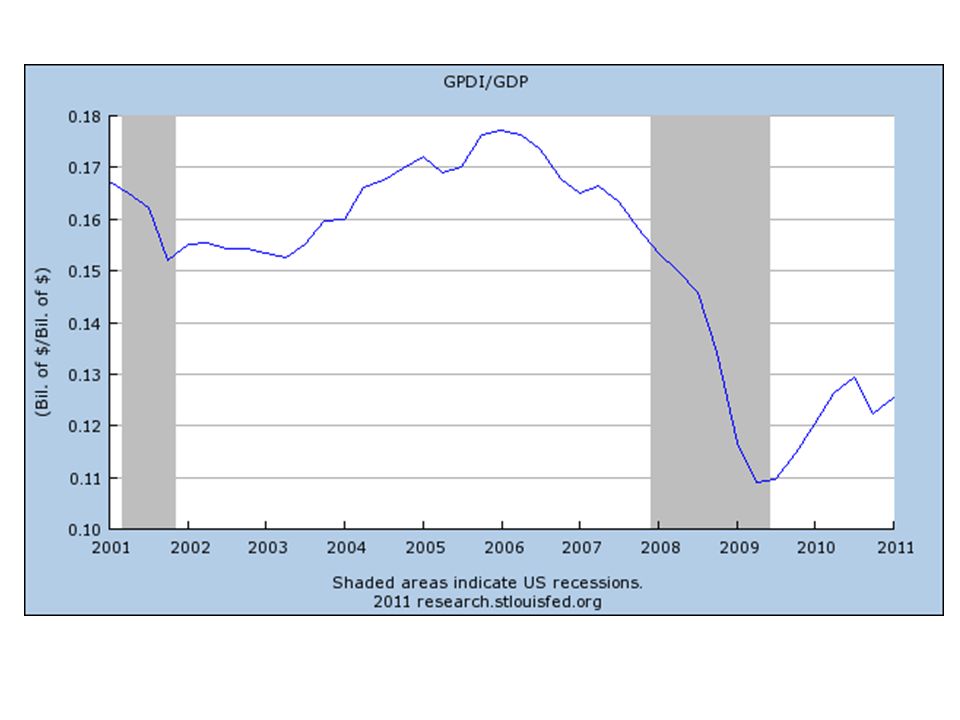

6

Investment, Investment, Investment Main issue of disappointing “recovery” – Private sector investment fell of a cliff in late 2008, early 2009 – Has not recovered since to anywhere near normal levels

8

Housing Market Residential fixed investment (People building houses, or major remodel/improvements) – According to latest numbers still only 42% of 2005 level. For every $100 spend on housing construction in 2005, now only $42 are spent. – Building permits, housing starts, existing home sales, foreclosures all do not suggest major boom ahead anytime soon. Assume Assume: Housing market continues to be depressed, at least no major improvement in sight

9

Business Sector You guys! High levels of uncertainty – Regulations and Taxes – Consumer and Industry demand going forward Consumer Confidence Measures still very low – Down compared to last year Purchasing Managers’ Index (ISM) – Lower compared to April, how temporary are the “headwinds”?

– Lower compared to April, how temporary are the headwinds .")

10

Hiring

11

What does this picture mean? Even where there are job openings many businesses take it relatively slow to fill them Assume Assume: No jobs miracle likely to be coming soon from the private sector under current conditions

12

Financial Markets Reports on Banking and Finance activity nationwide (Beige Book) show loan demand as “mixed” or “slightly improved” Senior Loan Officer Opinion Survey shows some (minor) improvements in availability of credit to businesses nationwide – Banks state they are mostly held back by an increased uncertainty of the economic outlook and a reduced tolerance for risk

show loan demand as mixed or slightly improved Senior Loan Officer Opinion Survey shows some (minor) improvements in availability of credit to businesses nationwide – Banks state they are mostly held back by an increased uncertainty of the economic outlook and a reduced tolerance for risk")

13

Exports Still strong growth in China, India, Brazil – Even larger growth for products pitched at new middle class – Chinese apartments with two air conditioners – Currency manipulation will continue Eurozone faces internal issues, so does Japan No export boom likely overall

14

What to make of all this? Growthin the second half of 2011 Growth in the second half of 2011 will likely be at most around 3%, maybe lower. – Not enough to make major progress in terms of reducing unemployment; no surprise if rate remains around 9% over the rest of the year – Combined with growth of less than 2% in the first half, overall growth for the year of 2011 will be below 3%

15

Forecast for 2012 Growth should pick up once the recovery really takes hold – Has been predicted since late 2009 Crucial market: Housing! No government policies in sight to address housing market boldly – Muddling through Economist: Housing market now potentially undervalued in US (based on rent to price ratios), does not mean has reached bottom

, does not mean has reached bottom.")

16

Forecast for 2012 Households and many businesses are still paying down debt from the bubble years – Will continue in 2012 – Debt levels have come down but not nearly to pre-bubble levels “Disappointing” recovery may continue Growth of 3-3.5% Growth of 3-3.5% unlikely to be topped next year Unemployment comes down very, very slowly

17

Forecast for 2012 Assumes no major new “headwinds” Also no miracles Assumes no major policy changes – Safe assumption for Congress – Also unlikely that the Federal Reserve will be willing to do something dramatic Forecast consistent with forecast from Federal Reserve, economists at Goldman Sachs etc. – Sorry, I am not more cheerful but I have good company…

Similar presentations

Is the Banking Sector Stable? 2) Are State and Local Governments Solvent? 3) How Serious.>")