Download presentation

Presentation is loading. Please wait.

1

Principles of Economics Overview of Macroeconomics

2

20.Overview of Macroeconomics MACROEOCONOMICS is the study of the behaviour of the economy as a whole. Short term fluctuations in Y, u, and P: Business cycle Long term trends in Y and living standards: Economic growth Started in 1930s by John Maynard Keynes whose theory helped fighting Great depression 1936: The General Theory of Employment, Interest and Money: high and production below PPF can persist, hence government has to use fiscal and monetary policy to shorten downturns.

3

Macroeconomic objectives and instruments OBJECTIVES: 1.Low unemployment 2.Inflation control 3.High growth rate of the economy These goals are often confronted, for example too low unemployment increases inflation, or too low inflation causes GDP to stagnate INSTRUMENTS: 1.Monetary policy: control M to affect i 2.Fiscal policy: G, T

4

1. High and growing level of output (Y) Gross domestic product (GDP) is the most comprehensive measure of the total output in an economy (Y) NOMINAL GDP is measured in actual market prices. REAL GDP is measured in constant prices (taking certain year’s price level as a base) GDP GROWTH RATE, g Y, is a percentage increase in GDP in a time period (mostly year) POTENTIAL OUTPUT is the maximum sustainable output that the economy can produce When Y is above potential Y inflation appears, when it is below u rises.

Gross domestic product (GDP) is the most comprehensive measure of the total output in an economy (Y) NOMINAL GDP is measured in actual market prices. REAL GDP is measured in constant prices (taking certain year’s price level as a base) GDP GROWTH RATE, g Y, is a percentage increase in GDP in a time period (mostly year) POTENTIAL OUTPUT is the maximum sustainable output that the economy can produce When Y is above potential Y inflation appears, when it is below u rises..")

5

2. Low unemployment Unemployment rate (u) is the share of people who do not work but seek job in the labour force (employed + unemployed): unemployed seeking job u = labour force Employment rate the share of people who work in the labour force (employed + unemployed)

is the share of people who do not work but seek job in the labour force (employed + unemployed): unemployed seeking job u = labour force Employment rate the share of people who work in the labour force (employed + unemployed).")

6

3. Stable price level Price stability is the situation in which the overall level of prices either remains unchanged or rises very slowly. Inflation (π) is the percentage change in the overall level of prices in a year. Price level is measured using price indices, mostly CPI (consumer price index): Price index is a measure of the average level of prices Where P stands for the level of prices, t for the current year and t – 1 for the previous year.

is the percentage change in the overall level of prices in a year. Price level is measured using price indices, mostly CPI (consumer price index): Price index is a measure of the average level of prices Where P stands for the level of prices, t for the current year and t – 1 for the previous year..")

7

Undesired price levels DEFLATION is the fall in price level HYPERINFLATION is is the inflation of 1000% or more (e.g. Croatia in the war year 1992) High inflation erodes pensions, taxes become variable, the currency sis no longer a value of worth. Deflation causes stagnation

High inflation erodes pensions, taxes become variable, the currency sis no longer a value of worth. Deflation causes stagnation.")

8

Fiscal policy POLICY INSTRUMENT is a government controled variable which affect at least one macroeconomic goal. FISCAL POLICY denotes use of taxes (T) and government spending (G) and is conducted by Ministry of finance G consists of: 1.Public goods (infrastructure, defence, salaries for public services) 2.Transfer payments (aid for unemployed and elderly) G is part of Y (income) and therefore affects GDP. T affect i) incomes and ii) prices of goods and factors

and government spending (G) and is conducted by Ministry of finance G consists of: 1.Public goods (infrastructure, defence, salaries for public services) 2.Transfer payments (aid for unemployed and elderly) G is part of Y (income) and therefore affects GDP. T affect i) incomes and ii) prices of goods and factors.")

9

IS curve IS curve shows the relation between output and interest rate when goods markets are at its equilbria. Expansive f.p. shifts IS rightwards, and restrictive leftwards. i IS Y

10

Monetary policy MONETARY POLICY is an activity of affecting money supply (M) It is conducted by the central bank (HNB in Croatia) Money consists of the means of exhange (cash, deposit money) Money supply affects interest rates, stock prices, investments, etc., which affects output.

It is conducted by the central bank (HNB in Croatia) Money consists of the means of exhange (cash, deposit money) Money supply affects interest rates, stock prices, investments, etc., which affects output.")

11

LM curve LM curve shows relationship between output and interest rate when financial markets are at their equilibria. Expansive M.P. shifts LM rightwards, restrictive M.P. shifts it leftwards. i LM Y

12

IS-LM model IS-LM shows relation between i and Y when goods and services markets and financial markets are at its equilbrium. i IS Y LM Y* i*

13

Restrictive fiscal policy Fall in interest rate Fall in the output

14

Expansive fiscal policy i rises Y rises

15

Restrictive monetary policy i rises Y falls

16

Expansive monetary policy i falls Y rises

17

Aggregate supply and aggregate demand Aggregate supply (AS) is total amount of goods and services that a country produces and sells in certain period at all possible price levels. AS depends on the productive capacity and level of costs Aggregate demand (AD) is total amount of goods and services that consumers, government and companies spend in a certain period of time at all possible price levels. It is deducted from IS-LM model (equilibrium on the goods and financial markets)

is total amount of goods and services that consumers, government and companies spend in a certain period of time at all possible price levels. It is deducted from IS-LM model (equilibrium on the goods and financial markets).")

18

Deduction of aggregate demand from IS-LM model

19

Macroeconomic equilibrium 0 AD AS Y* Output Y Price level P P* AD& AS: fiscal policy, money supply and capital stock is constant D&S: other goods’ prices, tastes, income, technology and costs held constant Macroeconomic equilibrium is a combination of the overall price level and output level at which all sellers and buyers are satisfied with their purchases, sales and prices.

20

International economy International economy is the system of trading and finance connections among countries. International trade: borderless microeconomics Trade policies affect international trade (tariffs, quotas, subsidies) International finance: borderless macroeconomics International financial management deals with exchange rates in different exhange rate systems

International finance: borderless macroeconomics International financial management deals with exchange rates in different exhange rate systems.")

21

Macroeconomic history Great depression (1930’s) Wartime boom (1960’s) Tight money (1979 – 1982) Expansion decade (1990’s)

Wartime boom (1960’s) Tight money (1979 – 1982) Expansion decade (1990’s)")

22

21. Measuring economic activity GDP is the most common measure of national output GNP contains total output of the companies produced by the observed country domestically or abroad, without domestic output of the foreign companies GDP includes all production in a country without output of domestic companies abroad and includes output of foreign companies in the observed country Up to 1992 GNP was more common, later it was GDP

23

Two ways to measure national product: 1.CONSUMPTION APPROACH: Sum of all expenditures on goods and services: Y = C + I + G + NX 2. INCOME APPROACH: Sum of all incomes in an economy: Y = w + i + r + Π + Dp + T They both have to give the same GDP In order to exclude double counting intermediate products are excluded

24

Gross domestic product (GDP), National income (NI) and Disposable personal income (DI) C I G X GDP NDP = NI Dp Taxes NI Net business saving Transfer payments DI

, National income (NI) and Disposable personal income (DI) C I G X GDP NDP = NI Dp Taxes NI Net business saving Transfer payments DI")

25

Nominal and real GDP NOMINAL GDP is expressed in current prices REAL GDP excludes the effect of price changes Real GDP can be obtained from the nominal GDP by DEFLATIONING (dividing with the price index) GDPreal = GDPnom/P Price indices: CPI (consumer price index) and PPI (producer price index) CPI: measure of the average change over time of the urban consumers’ basket of goods (364 classes of goods) PPI: measure of the price level of goods at th wholesale or producer level, where weights are share of the commoditie’s net sales in total sales.

GDPreal = GDPnom/P Price indices: CPI (consumer price index) and PPI (producer price index) CPI: measure of the average change over time of the urban consumers’ basket of goods (364 classes of goods) PPI: measure of the price level of goods at th wholesale or producer level, where weights are share of the commoditie’s net sales in total sales.")

26

Investment and saving Y = C + S (income can be either saved or consumed) Investment is made from savings: I = S Accumulation of investment creates capital: K = ΣI In detail: I T = I + NX = S P + S G = S T I T (national investment), S P (private saving), S G (government saving), S T (total saving)

Investment is made from savings: I = S Accumulation of investment creates capital: K = ΣI In detail: I T = I + NX = S P + S G = S T I T (national investment), S P (private saving), S G (government saving), S T (total saving)")

27

Example 1 GDP = 1000, where expats produce 200. Residents of the country produce abroad 100. Find GNP GNP = 1000 – 200 + 100 = 900

28

Exercise 2 Let rent be 100, profit 500, investments 600, depreciation 400, wages 5500, interests 500, consumption 6700and taxes 300. Find GDP and NDP using both approaches.

29

Consumption approach – GDP = C + I + G + NX – GDP = 6700 + 600 = 7300 Income approach – GDP = w + i + R + Pf + Dp + T – GDP = 5500 + 500 + 100 + 500 + 400 + 300 = 7300 NDP = BDP – Dp = 7300 – 400 = 6900

30

Exercise 3 Find nominal and real GNP

31

GNP deflator = nominal GNP / real GNP * 100

32

Exercise 4 If GDP is 3000, depreciation 600, taxes 300, net business savings 100 and trasfer payments 50, find national income and disposable personal income. Find GNP if country has no international relations.

33

NI = GDP – Dp NI = 3000 – 600 = 2400 DI = NI – T – Net business savings + TR NI = 2400 – 300 – 100 + 50 If a country has no international relations then GDP = GNP = 3000

34

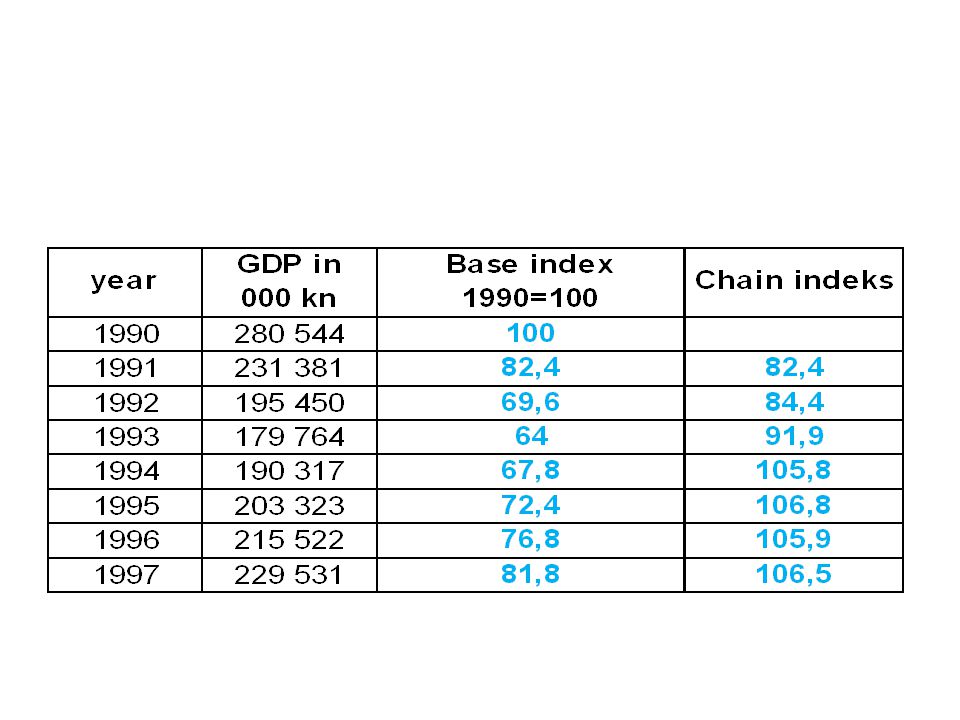

Zadatak 1: Table below shows GDP of Croatia in prices from 1990 for 1990 – 1997. Find chain and base indices (1990 = 100)

.")

35

Base index (1990=100) = BDP t / BDP 90. * 100 – 231 381 / 280 544 * 100 = 82,48 – 195 450 / 280 544 * 100 = 69,67 Chain index = BDP t / BDP t-1 * 100 – 231 381 / 280 544 * 100 = 82,48 – 195 450 / 231 381 * 100 = 84,47

Similar presentations

>")