Download presentation

Presentation is loading. Please wait.

1

Redrawing the World’s Energy Map: The Gas Revolution and Energy Self- Reliance in North America The Natural Gas Industry Future Directions Kevin McCrackin Vice President Utility Marketing

2

Corporate Overview Largest Natural Gas Utility Company 7 Local Distribution Utilities in 7 states 4.5 million customers Tropical Shipping

3

North American Gas Markets: Abundant Low Cost Resource of over 100 years per EIA and Potential Gas Committee © Wood Mackenzie Shale gas and tight oil plays Sources: Wood Mackenzie (North America Gas Service, Unconventional Gas Service) $2 $3 $4 $5 $6 $7 $8 2000200520102015202020252030 Year production >250 mmcfde $/mmbtu US shales Canadian shales Tight oil Liquid-rich shales 10 tcfe 100 tcfe 50 tcfe 201020112012 Marcellus becomes the leading US gas play

$2 $3 $4 $5 $6 $7 $ Year production >250 mmcfde $/mmbtu US shales Canadian shales Tight oil Liquid-rich shales 10 tcfe 100 tcfe 50 tcfe Marcellus becomes the leading US gas play")

4

Changing Economics: Natural Gas Prices Exceptionally Low Source: U.S. Department of Energy, Energy Information Administration Between June 2008 and December 2012, Henry Hub natural gas prices have decreased 78% Hurricanes Katrina and Rita 2008 Oil Shock

5

© Wood Mackenzie Price outlook Source: Wood Mackenzie (North America Gas Service, Coal Market Service, Macro Oils Service) Where are fuel prices headed in North America markets? Oil/gas ratio Source: Wood Mackenzie (North America Gas Service)

.")

6

Who Is Using Natural Gas in the United States? Residential Commercial Industrial Power Generation Source: U.S. Department of Energy, Energy Information Administration % of natural gas throughput Natural gas use for power generation has increased 87% in the past 25 years Industrial customer usage has decreased by 21% in that same period

7

© Wood Mackenzie …But, an Industrial Renaissance is underway due to abundant supplies and low natural gas prices Source: Wood Mackenzie North America Gas Service Annual gas demand growth (US & Canada) Demand growth (vs. 2010)

.")

8

Looming Natural Gas Demand: Coal retirements will accelerate in mid-decade with Mercury & Air Toxics Standards (MATS) © Wood Mackenzie Source: Wood Mackenzie North America Power Service US coal retirements

© Wood Mackenzie Source: Wood Mackenzie North America Power Service US coal retirements")

9

New Markets for Natural Gas Power Generation Combined Heat & Power Compressed Natural Gas Liquefied Natural Gas

10

Source: U.S. Department of Energy, Energy Information Administration Power Generation Mix Million megawatts Coal Natural Gas Other Nuclear Petroleum Products

11

Projected Natural Gas Consumption 11 Source: ICF International The Largest Natural Gas Market Growth Opportunity is Power Generation – Are Central Bulk Power Plants the most efficient way to grow?

12

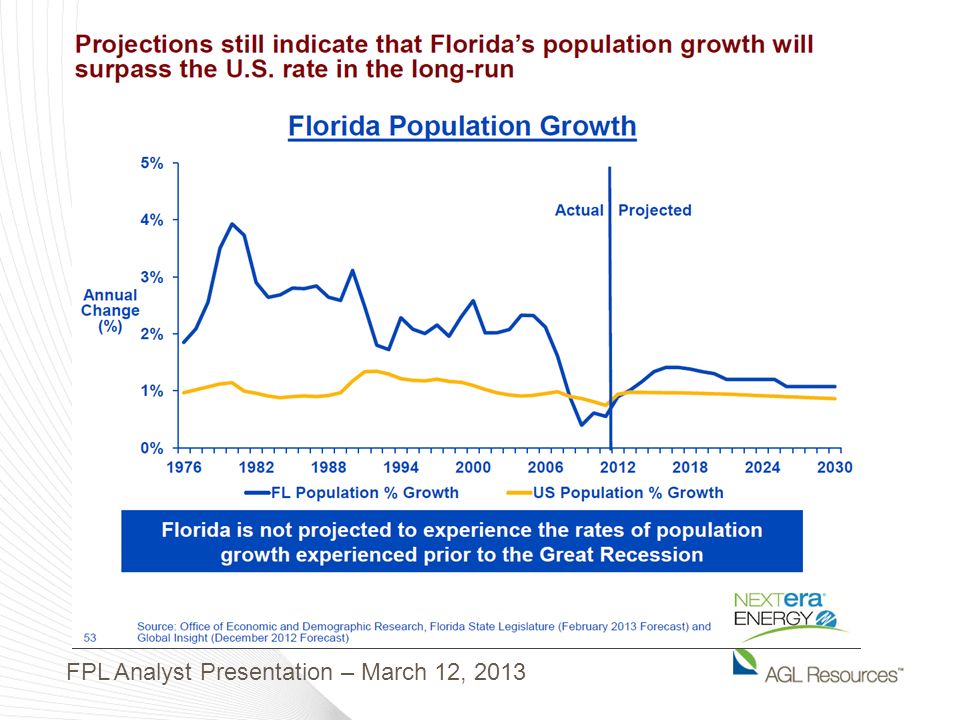

Implications to the Florida Generation Market FP&L Generation Plans: New combined cycle power plants planned or under construction at Rivera Beach, Martin and Port of Everglades Old peaking units requiring upgrades due to heat rates above 17,000 Btu/kWh Achieving the improved environmental standards could require replacement of existing natural gas turbine peakers Evaluation is looking at new natural gas combustion turbines Other Possible Gas-Fired Plants: Closure of Crystal River Polk Power Station Expansion FPL Analyst Presentation – March 12, 2013

14

Between now and 2035, North America requires construction of over 1,400 miles/year of natural gas pipelines, with 17% of the new pipeline being constructed in the Southeast. $205 Billion invested in North America through 2035 Southeast U.S. natural gas demand doubles; 10 Bcf/d to 20 Bcf/d Southeast U.S. infrastructure investment of over $35 Billion 568 pipeline laterals to attach new gas-fired power generation. 33% of these laterals projected to be constructed in the Southeast. Natural Gas Infrastructure Requirements Source: ICF International study for INGAA Foundation, “ North American Midstream Infrastructure through 2035” $Billions

15

FPL Analyst Presentation – March 12, 2013

16

NATURAL GAS vs. ELECTRIC The Big Picture – Direct Use is Most Efficient… ….so, distributed generation at the home makes sense.

17

Combined Heat and Power (CHP) is more Efficient 17 http://www.aga.org/our-issues/playbook/Documents/AGA_Playbook2012_HI_RES.pdf

is more Efficient 17")

18

18 Executive Order – August 30 “Coordinate and strongly encourage efforts to achieve a national goal of deploying 40 gigawatts of new, cost effective industrial CHP in the United States by the end of 2020.” ”Convene stakeholders, through a series of public workshops, to develop and encourage the use of best practice State policies and investment models that address the multiple barriers to investment in industrial energy efficiency and CHP.” ”Utilize their respective relevant authorities and resources to encourage investment in industrial energy efficiency and CHP.”

19

Federal Support for CHP 19 Incentives 10% Investment Tax Credit (ITC) for CHP through December, 2016; 50 MW or less 10% ITC for micro turbines capped at $200/kW of capacity; 2 MW or less 30% ITC for fuel cells or $3,000/kW ($1,000/ kW residential), whichever is smaller Modified Accelerated Cost-Recovery System – for 2013 bonus depreciation is 50% of the eligible basis Renewable Energy Production Tax Credit (ARRA portion expires end of 2013) – renewable fuels only Support EPA recognizes CHP as an efficiency measure under developing greenhouse gas emissions standards EPA includes output-based options that recognize CHP benefits in ICI Boiler MACT and Utility MACT (MATS) DOE increases technology deployment support for CHP and announces goal of 40 GW of new CHP capacity by 2020 Clean Energy Standard Act of 2012 – Includes nuclear, clean coal, and natural gas – Recognizes the additional energy efficiency and greenhouse gas benefits of CHP Proposals to encourage rate-basing of utility investments in behind the meter energy efficiency and CHP Florida - Renewable energy tax credit of 1¢/kWh annually (CHP is eligible), Solar and CHP sales tax exemption. Net metering excess generation credited at the utility retail rate.

20

U.S. CHP Generation Capacity Vision 20 Source: Combined Heat and Power: Effective Energy Solutions for a Sustainable Future Sponsored by the U.S. Department of Energy

21

The U.S. is the world’s largest natural gas producer, but lags behind other nations in natural gas transportation There are more than 12.7 million natural gas vehicles on the road worldwide – but less than 125,000 are in the United States. Source: NGV Global

22

Fuel price is the driver, and it is expected to stay this time….

23

PRICING CHARACTERISTICS 20% 13% 27% 40% Natural Gas Distribution & Compression Marketing & Profit Taxes CNG (July 2012) Retail Price: $1.85/gge The natural gas commodity cost component is about one quarter the crude oil cost component in the make-up of the overall price of the delivered fuel, giving CNG a price dampener against price volatility.

Retail Price: $1.85/gge The natural gas commodity cost component is about one quarter the crude oil cost component in the make-up of the overall price of the delivered fuel, giving CNG a price dampener against price volatility.")

24

PRICE STABILITY OF CNG Natural Gas at $2.88/Mcf Natural Gas (divide by 7.2) $0.40 Transport Costs & Fees $0.20 Electricity Costs per GGE $0.10 Maintenance per GGE $0.20 Federal and State Taxes $0.25 Fuel Card Fees per GGE $0.05 Retailer Profit Margin $0.70 CNG at the Pump $1.90 Natural Gas at $5.76/Mcf Natural Gas (divide by 7.2) $0.80 Transport Costs & Fees $0.20 Electricity Costs per GGE $0.10 Maintenance per GGE $0.20 Federal and State Taxes $0.25 Fuel Card Fees per GGE $0.05 Retailer Profit Margin $0.70 CNG at the Pump $2.30 The natural gas fuel commodity makes up a smaller portion of the overall price of the delivered fuel when compared to gasoline or diesel.

$0.40 Transport Costs & Fees $0.20 Electricity Costs per GGE $0.10 Maintenance per GGE $0.20 Federal and State Taxes $0.25 Fuel Card Fees per GGE $0.05 Retailer Profit Margin $0.70 CNG at the Pump $1.90 Natural Gas at $5.76/Mcf Natural Gas (divide by 7.2) $0.80 Transport Costs & Fees $0.20 Electricity Costs per GGE $0.10 Maintenance per GGE $0.20 Federal and State Taxes $0.25 Fuel Card Fees per GGE $0.05 Retailer Profit Margin $0.70 CNG at the Pump $2.30 The natural gas fuel commodity makes up a smaller portion of the overall price of the delivered fuel when compared to gasoline or diesel.")

25

THE ECONOMICS OF VEHICLE CLASSES Type of Vehicle Incremental Cost * Annual Use (Gals.) Annual Savings ** Simple Payback Honda Civic (consumer)$7,500500$75010 yrs. Sedan (fleet application)$10,0001,200$1,8006 yrs. Pickup Truck (fleet app.)$11,0002,000$3,0004 yrs. Cargo Van$14,0002,500$3,7504 yrs. Step Van/Box Truck$24,0004,000$6,0004 yrs. School Bus$28,0002,600$3,7507 yrs. Garbage Truck$35,0008,000$12,0003 yrs. Class 8 Truck$65,00015,000$22,5003 yrs. * Cost assumes no grant money, rebates, tax credits, etc. available * * Savings calculated based on savings of $1.50/GGE at retail CNG station

$10,0001,200$1,8006 yrs. Pickup Truck (fleet app.)$11,0002,000$3,0004 yrs. Cargo Van$14,0002,500$3,7504 yrs. Step Van/Box Truck$24,0004,000$6,0004 yrs. School Bus$28,0002,600$3,7507 yrs. Garbage Truck$35,0008,000$12,0003 yrs. Class 8 Truck$65,00015,000$22,5003 yrs. * Cost assumes no grant money, rebates, tax credits, etc. available * * Savings calculated based on savings of $1.50/GGE at retail CNG station.")

26

THE LIGHT DUTY MARKET CHALLENGE $500,000+ for Centralized Fueling Stations 500 down, 160,000 to go - $50+ billion? in investment to match gasoline stations The economics work for fleets, so there will continue to be growth $100,000?+ to make a private station public accessible $8,000+ Vehicle Conversion/Replacement Premium Takes 7 years+ to recover the premium Limited vehicle selection from OEM’s, especially vehicles desired by target customers Efforts around conversion, and specifically tank technologies, is ongoing $5,000 Home Refueling Appliance (HRA) product and Installation Cost An additional 4+ years to recover the HRA cost Limited fill capability, maintenance unknown (historically not good) Result: $8,000 + $5,000 = $13,000 per vehicle premium, or 11+ years payback MUST REDUCE VEHICLE CONVERSION COSTS & DEVELOP A LESS EXPENSIVE HRA

product and Installation Cost An additional 4+ years to recover the HRA cost Limited fill capability, maintenance unknown (historically not good) Result: $8,000 + $5,000 = $13,000 per vehicle premium, or 11+ years payback MUST REDUCE VEHICLE CONVERSION COSTS & DEVELOP A LESS EXPENSIVE HRA.")

27

Expect 12% of New vehicle sales to be NGV’s by 2020 NGV Engine Costs are expected to be competitive by 2020

28

THE HOME REFUELING APPLIANCE (HRA) BRC Fuelmaker Phill is the only commercially available HRA Expensive price with installation, approximately $6,000 Limited fill capability, less than a half gallon per hour Historically has had compressor performance and maintenance issues AGL is a distributor, and installs and maintains Phill units AGL Resources is actively engaged with a team of industry leaders in the development of a less costly HRA U.S. Department of Energy - Advanced Research Projects Agency-ENERGY (ARPA-E) – Methane Opportunities for Vehicular Energy (MOVE) 13 projects awarded with $30 million in funding – including 4 HRA designs Engineer Light-Weight Affordable Natural Gas Tanks Develop Natural Gas Compressors that can efficiently fuel a NGV at home GTI and GE have projects within this program, and AGL is actively involved

– Methane Opportunities for Vehicular Energy (MOVE) 13 projects awarded with $30 million in funding – including 4 HRA designs Engineer Light-Weight Affordable Natural Gas Tanks Develop Natural Gas Compressors that can efficiently fuel a NGV at home GTI and GE have projects within this program, and AGL is actively involved.")

29

Florida Legislation is headed in the right direction Repeals the “Decal” program for Alternative Fuels effective January 1, 2014 Exempts natural gas fuel from taxes for 5 years Survey of Florida residents shows 72% support for legislation encouraging NGV adoption 96% of the residents think Energy Independence is important Florida Natural Gas Vehicle Coalition In an August 2012 study, the transistioning of Florida Commercial Fleets to Natural Gas results in following benefits over 20 years: 10,000 new jobs $330 million in new wages $1 billion in economic output An update based upon February 2013 SB560 and HB579 legislation improves these results as follows over 5 years: 20,000 new jobs $715 million in new wages $2.5 billion in economic output

30

LNG in HHP Applications Total High Horsepower 15.2 billion gallons

31

Key Takeaways Natural gas is more relevant than ever to our energy future. New market opportunities for natural gas will potentially reshape entire industries. Florida’s growth is aligned with the growth in natural gas as a fuel and will make Florida a significant market participant. AGL Resources is uniquely positioned to deliver on the promise of natural gas.

Similar presentations

April 2009 1.>")