Download presentation

Presentation is loading. Please wait.

1

Chapter 2: An Overview of the Financial System Classifying Financial Markets Financial Market Instruments Financial Intermediaries Regulation Classifying Financial Markets Financial Market Instruments Financial Intermediaries Regulation

2

I. Classification Debt vs. Equity Markets debt security cash flows are fixed bonds, loans equity security cash flow variable, residual common stock debt security cash flows are fixed bonds, loans equity security cash flow variable, residual common stock

3

Primary vs. Secondary Markets primary market newly issued securities -- investment banking secondary market brokers match buyers and sellers dealers act as buyers and sellers -- “market-makers” primary market newly issued securities -- investment banking secondary market brokers match buyers and sellers dealers act as buyers and sellers -- “market-makers”

4

Exchanges vs. OTC Markets exchange buying & selling of securities in physical location NYSE OTC (over-the-counter) dealers in many locations buy & sell securities exchange buying & selling of securities in physical location NYSE OTC (over-the-counter) dealers in many locations buy & sell securities

dealers in many locations buy & sell securities exchange buying & selling of securities in physical location NYSE OTC (over-the-counter) dealers in many locations buy & sell securities.")

5

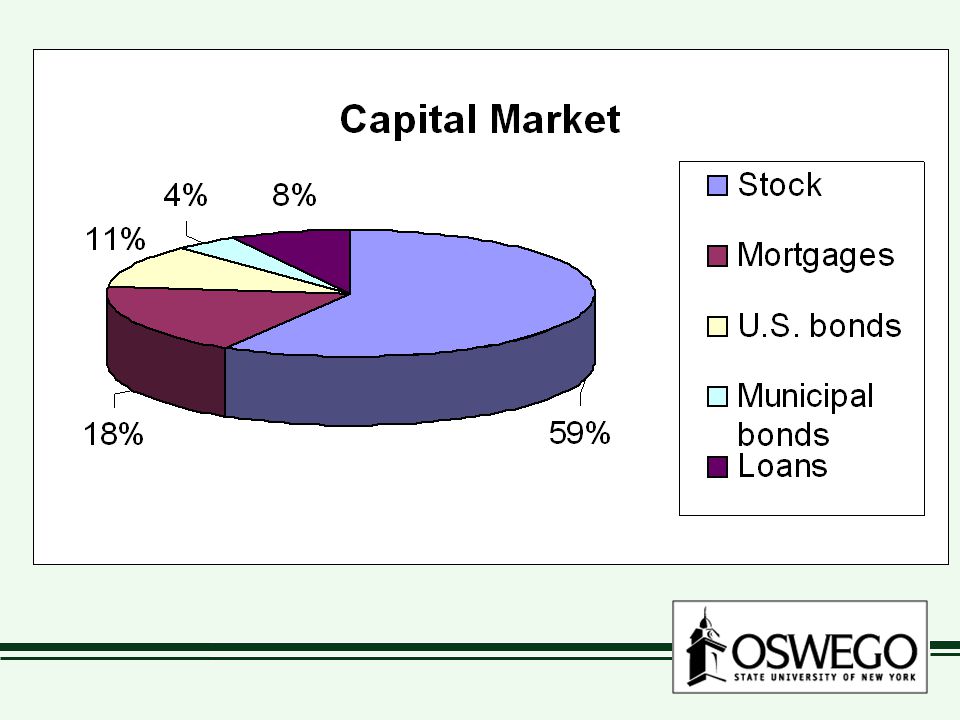

Money vs. Capital Markets money market short-term debt securities (up to 1 yr.) highly liquid, low risk capital market longer-term debt equity money market short-term debt securities (up to 1 yr.) highly liquid, low risk capital market longer-term debt equity

highly liquid, low risk capital market longer-term debt equity money market short-term debt securities (up to 1 yr.) highly liquid, low risk capital market longer-term debt equity.")

6

II. Financial Market Instruments a security or financial instrument = claim on future income or assets of issuer a security is an asset for the buyer, but a liability for the issuer a security or financial instrument = claim on future income or assets of issuer a security is an asset for the buyer, but a liability for the issuer

7

exampleexample shares of stock in Time Warner, Inc. shares of ownership in TW a claim on the earnings/assets of TW a liability for Time Warner an asset for me shares of stock in Time Warner, Inc. shares of ownership in TW a claim on the earnings/assets of TW a liability for Time Warner an asset for me

8

my mortgage I am the issuer (liability) the bank is the buyer/holder (asset) the bank has a claim on my house my mortgage I am the issuer (liability) the bank is the buyer/holder (asset) the bank has a claim on my house

the bank is the buyer/holder (asset) the bank has a claim on my house my mortgage I am the issuer (liability) the bank is the buyer/holder (asset) the bank has a claim on my house")

11

III. Financial Intermediaries Why have them? Transactions costs search costs to find borrower & lender contract costs economies of scale Why have them? Transactions costs search costs to find borrower & lender contract costs economies of scale

12

Risk sharing intermediaries are experts at bearing risk asset transformation Risk sharing intermediaries are experts at bearing risk asset transformation

13

Asymmetric Information one party has more info than the other creates problems BEFORE loan is made creates problems AFTER loan is made financial intermediaries minimize these problems Asymmetric Information one party has more info than the other creates problems BEFORE loan is made creates problems AFTER loan is made financial intermediaries minimize these problems

14

adverse selection BEFORE the loan people with worst credit are more likely to seek a loan lending not attractive solution? banks expert at assessing credit risks BEFORE the loan people with worst credit are more likely to seek a loan lending not attractive solution? banks expert at assessing credit risks

15

moral hazard AFTER the loan once money is lent, borrower may blow the money solution banks monitor borrowers and enforce lending contracts AFTER the loan once money is lent, borrower may blow the money solution banks monitor borrowers and enforce lending contracts

16

Types of intermediaries Depository institutions “banks” accept deposits, make loans Depository institutions “banks” accept deposits, make loans

17

Commercial banks largest in total assets Savings & Loans originally restricting to savings deposits and mortgages less restricted today Credit Unions consumer loans nonprofit organized around a group Commercial banks largest in total assets Savings & Loans originally restricting to savings deposits and mortgages less restricted today Credit Unions consumer loans nonprofit organized around a group

18

Contractual savings institutions acquire funds through payments in return for obligations life insurance property and casualty insurance pension funds Contractual savings institutions acquire funds through payments in return for obligations life insurance property and casualty insurance pension funds

19

Investment intermediaries indirect investment finance companies issue commercial paper consumer & commercial loans mutual funds sell shares to stock/bond portfolios taken away bank business in past 30 years Investment intermediaries indirect investment finance companies issue commercial paper consumer & commercial loans mutual funds sell shares to stock/bond portfolios taken away bank business in past 30 years

20

money market mutual funds money market portfolio shares = $1, pay dividends check writing privileges money market mutual funds money market portfolio shares = $1, pay dividends check writing privileges

21

IV. Regulation Reducing asymmetry of info disclosure of financial information -- by companies selling securities -- by financial institutions restrict insider trading Reducing asymmetry of info disclosure of financial information -- by companies selling securities -- by financial institutions restrict insider trading

22

promoting stability prevent financial panic -- markets cease to function financial institutions -- restrict ownership -- restrict activities -- insurance on deposits promoting stability prevent financial panic -- markets cease to function financial institutions -- restrict ownership -- restrict activities -- insurance on deposits

23

controlling the money supply Federal Reserve System controlling the money supply Federal Reserve System

Similar presentations

Households Firms Government Foreigners Financial Markets.>")