Download presentation

Presentation is loading. Please wait.

1

An Overview of the Financial System chapter 2

2

Function of Financial Markets Lenders-Savers (+) Households Firms Government Foreigners Financial Markets Borrowers-Spenders (-) Business-Firms Government Households Foreigners Direct Finance Indirect Finance Financial Intermediaries

Households Firms Government Foreigners Financial Markets Borrowers-Spenders (-) Business-Firms Government Households Foreigners Direct Finance Indirect Finance Financial Intermediaries")

3

Function of Financial Markets Financial markets perform the function of channeling funds from people with a surplus of funds (savers-lenders) to people with a shortage of funds (borrowers-spenders). In other words, lenders finance spending by borrowers. The finance process can be either direct or indirect: Direct finance: borrowers borrow from lenders through financial markets by selling securities (financial instruments), which are defined as claims on the borrower's future income or assets. Example: Indirect finance: borrowers borrow through financial intermediaries (e.g. banks) who receive funds from savers and lend them to borrowers. Example:

, which are defined as claims on the borrower s future income or assets. Example: Indirect finance: borrowers borrow through financial intermediaries (e.g. banks) who receive funds from savers and lend them to borrowers. Example:.")

4

Why the channeling of funds is important to the economy? Savers not necessarily have investment projects. In the absence of financial markets, it is difficult for savers and borrowers to meet. With financial markets both benefit, the saver and the borrower. As a result, the whole economy is better off as more income is generated and more output is produced. Thus financial markets promote economic efficiency.

5

Structure of Financial Markets 1. Debt and Equity Markets Firms and individuals can obtain funds in a financial market in two ways: A. Issue a debt instrument (e.g. bond) by which the borrower pays the holder of the instrument specified amounts in the future. Debt instruments are defined by their maturity as follows: Short term Instruments: instruments that mature in 3 to 12 months. Long term Instruments: Instruments that mature in more than one year.

by which the borrower pays the holder of the instrument specified amounts in the future. Debt instruments are defined by their maturity as follows: Short term Instruments: instruments that mature in 3 to 12 months. Long term Instruments: Instruments that mature in more than one year..")

6

B. Issue equities (e.g. common stocks), which are claims to share in the net income and assets of a business. The owner of the equity receives dividends (fraction of profits) at specified periods plus receiving part of the business assets if it goes bankrupt. Disadvantage: equity holder is a residual claimant (i.e. is paid whatever lefts paying debt holders)

, which are claims to share in the net income and assets of a business. The owner of the equity receives dividends (fraction of profits) at specified periods plus receiving part of the business assets if it goes bankrupt. Disadvantage: equity holder is a residual claimant (i.e. is paid whatever lefts paying debt holders).")

7

2. Primary and Secondary Markets A primary market is a financial market in which new issues of a security (e.g. bond, stock) are sold to initial buyers. A secondary market is a financial market in which securities that have been previously issued are resold. Secondary markets serve two functions: A. They make financial instruments more liquid. B. They determine the price of the security (through supply and demand).

are sold to initial buyers. A secondary market is a financial market in which securities that have been previously issued are resold. Secondary markets serve two functions: A. They make financial instruments more liquid. B. They determine the price of the security (through supply and demand)..")

8

3. Exchanges and Over the Counter Markets Secondary markets can be organized in two ways: Exchanges: Trades are conducted in central locations where sellers and buyers (or their agents or brokers) meet. Over-the-Counter Markets: Dealers at different locations, connected by computers, buy and sell securities.

meet. Over-the-Counter Markets: Dealers at different locations, connected by computers, buy and sell securities..")

9

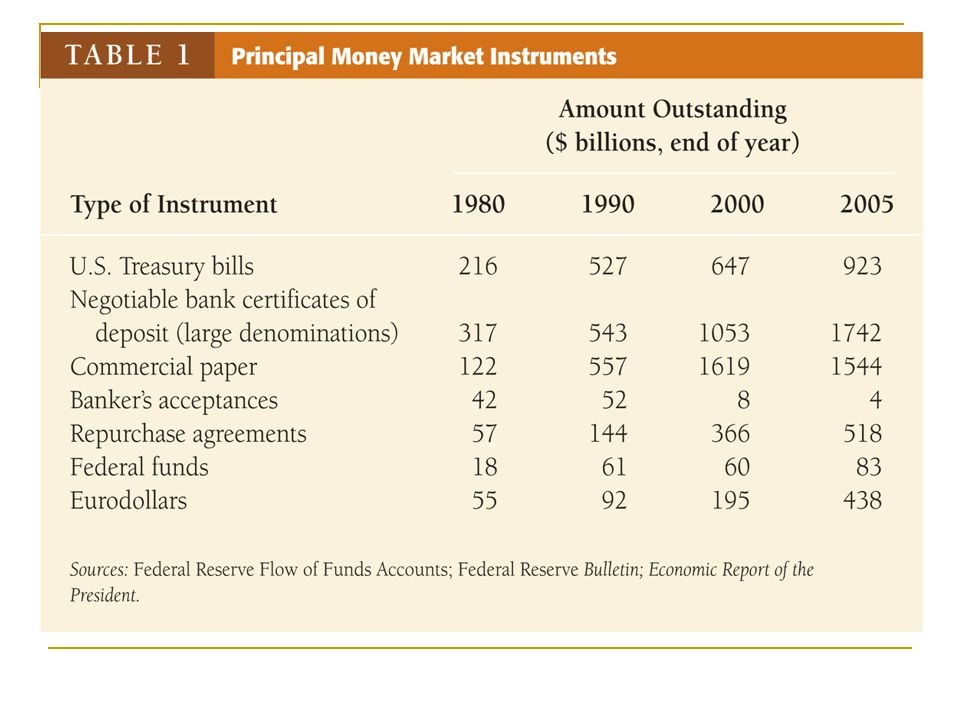

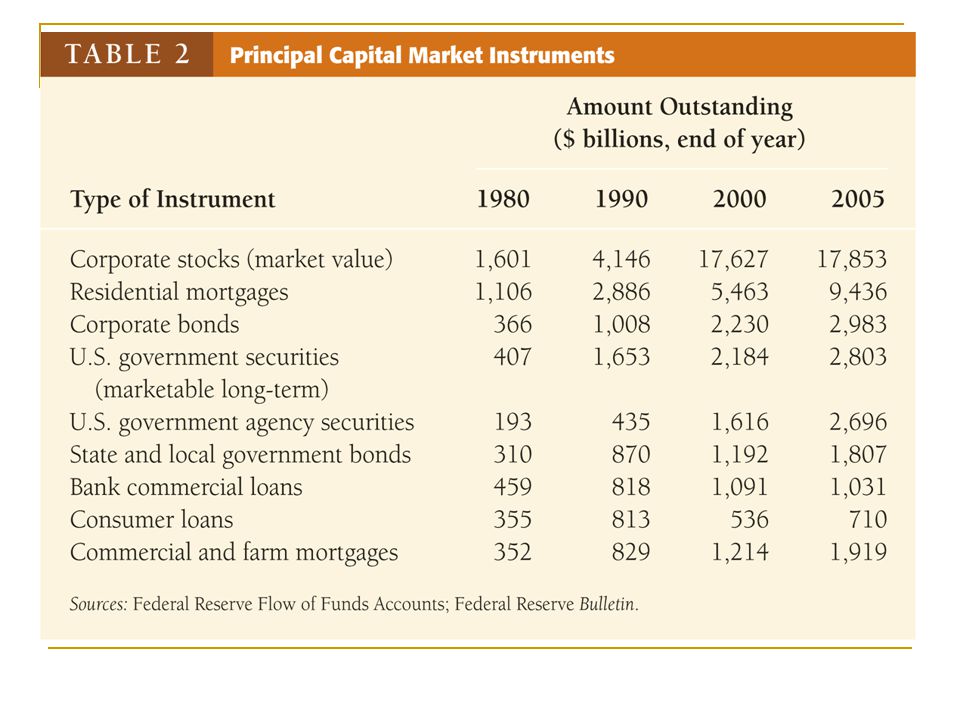

4. Money and Capital Markets Another way of distinguishing between markets is on the basis of the maturity of the securities traded in each market. Money Market: Financial market in which only short- term debt instruments are traded. Example: Treasury Bills, Commercial Papers. Capital Market: Financial market in which longer-term debt and equity instruments are traded. Example: Government Bonds, Corporate Bonds, Stocks.

10

Money and Capital market Instruments Capital market Instruments Money market Instruments Government Companies

13

Function of Financial Intermediaries Funds move through financial intermediaries (FIs) as they acquire funds from Savers and use them to make loans to Borrowers. They do so for three reasons: A. Transaction Costs: Definition: time and money spent on financial transactions. It can be reduced by (FIs) through experience and their large size which allows them to take advantage of economies of scale.

through experience and their large size which allows them to take advantage of economies of scale..")

14

B. Risk Sharing Financial intermediaries reduce exposure of investors to risk (uncertainty about the returns on assets) through risk sharing (selling assets with low risk, then use the funds to purchase other assets with higher risk). Low transaction costs enable (FIs) to do risk sharing at low cost, allowing them to earn profit on the spread between the returns of the low and high risk assets (also called asset transformation). FIs also help individuals in diversifying their assets and therefore lowering their exposure to risk by creating portfolios.

through risk sharing (selling assets with low risk, then use the funds to purchase other assets with higher risk). Low transaction costs enable (FIs) to do risk sharing at low cost, allowing them to earn profit on the spread between the returns of the low and high risk assets (also called asset transformation). FIs also help individuals in diversifying their assets and therefore lowering their exposure to risk by creating portfolios..")

15

C. Asymmetric Information (or inequality): Definition: One party to a financial transaction (e.g. borrower) knows more about the risk and return of the transaction than the other party (e.g. lender). This leads to two problems: 1. Adverse Selection: a problem created by asymmetric information occurs before the transaction takes place. It leads to undesirable outcome (e.g. bad borrowers selected). 2. Moral Hazard: a problem created by asymmetric information occurs after the transaction takes place (e.g. borrowers take actions undesirable by lenders).

knows more about the risk and return of the transaction than the other party (e.g. lender). This leads to two problems: 1. Adverse Selection: a problem created by asymmetric information occurs before the transaction takes place. It leads to undesirable outcome (e.g. bad borrowers selected). 2. Moral Hazard: a problem created by asymmetric information occurs after the transaction takes place (e.g. borrowers take actions undesirable by lenders)..")

16

Financial Intermediaries A. Depository Institutions: Take deposits and make loans. They include: 1. Commercial Banks: take deposits to use them in making loans and buying bonds. 2. Saving and Loan Associations: take deposits and make mortgage loans. 3. Mutual Saving Banks: similar to (S&Ls) but differ by being owned by their depositors. 4. Credit Unions: very small cooperatives organized by a group (union members, etc). Take deposits (called shares) to make consumer and mortgage loans.

but differ by being owned by their depositors. 4. Credit Unions: very small cooperatives organized by a group (union members, etc). Take deposits (called shares) to make consumer and mortgage loans..")

17

B. Contractual Savings Institutions: Acquire funds at periodic intervals on contractual basis. 1. Life Insurance Companies: Insure against financial hazards. They acquire funds from premiums and use them to buy corporate bonds and stocks. 2. Fire and Casualty Insurance Companies: Insure against loss and damage of property. They acquire funds from premiums and use them to buy liquid assets. 3. Pension Funds And Government Retirement Funds: Acquire funds from employees and employers and use them to pay retirement incomes.

18

C. Investment Intermediaries: 1. Finance Companies: Acquire funds by selling commercial papers and issuing stocks and bonds then lend them to consumers and small businesses. 2. Mutual Funds: Acquire funds by selling shares and use them to buy diversified portfolios of stocks and bonds. 3. Money Market Mutual Funds: Similar to mutual funds and depository institutions because they offer deposit-type accounts. Acquire funds by selling shares to use them in buying money market instruments. Then, pay shareholders interest on assets.

19

Size of Financial Intermediaries

20

Regulation of the Financial System For two main reasons: 1.Increasing information available to investors to lower the problem of asymmetric information in financial markets to increase their efficiency. 2.Ensuring the soundness of (FIs) to prevent financial panics caused by asymmetric information problem through: A. Restrictions on entry B. Disclosure C. Restrictions on assets and activities D. Deposit insurance E. Limits on competition F. Restrictions on interest rates

to prevent financial panics caused by asymmetric information problem through: A. Restrictions on entry B. Disclosure C. Restrictions on assets and activities D. Deposit insurance E. Limits on competition F. Restrictions on interest rates.")

21

Regulatory Agencies

Similar presentations

and borrowers.>")