Download presentation

Presentation is loading. Please wait.

1

Chapter 3: Financial Instruments, Markets and Institutions

Financial Markets Financial Institutions

2

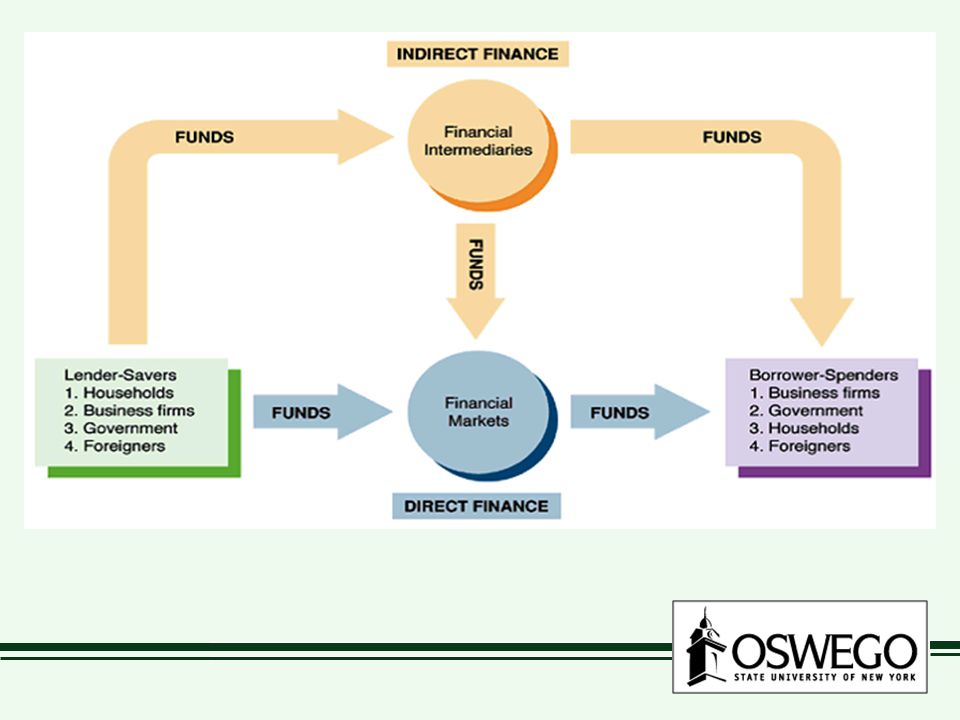

People who need funds borrowers/issuer/seller People who have funds to give lenders/savers/buyers

3

Indirect vs. Direct Finance

Indirect finance Borrowers and lenders meet through a financial intermediary (e.g. bank) Loan is a liability for borrower, and asset for a bank

Loan is a liability for borrower, and asset for a bank.")

4

Direct finance Borrowers sell securities directly to lenders e.g. corporate and Treasury bonds

6

I. Financial Instruments

aka. securities, financial assets definition (p. 36 (1st) or 41 (2nd)) = written legal obligation of one party to transfer something of value, usually money, to antoher party at some future date, under certain conditions a security is an asset for the buyer/lender, but a liability for the issuer/borrower/seller

or 41 (2nd)) = written legal obligation of one party to transfer something of value, usually money, to antoher party at some future date, under certain conditions. a security is an asset for the buyer/lender, but a liability for the issuer/borrower/seller.")

7

example shares of stock in Time Warner, Inc. shares of ownership in TW

a claim on the earnings/assets of TW a liability for Time Warner an asset for me

8

my mortgage I am the borrower (liability) the bank is the buyer/holder (asset) the bank has a claim on my house

the bank is the buyer/holder (asset) the bank has a claim on my house.")

9

uses of financial instruments

means of payment but much less liquid than money store of value better than money over time, but also greater risk transfer of risk buyer transfers risk to seller e.g. insurance policies, futures contract

10

Valuing financial instruments

sizing, timing & certainty of promised cash flows Size: how much is promised? the larger the cash flows, the greater the value Timing: when is it promised? the sooner the cash flows are received, the greater the value

11

Certainty: how likely its it that payments will be made?

the likelier the payments the greater the value Under what conditions? e.g. insurance, derivatives payments when we need them the most are more valuable

12

examples (p. 43/44 or 46/47) bank loans stocks bonds home mortgages

asset-backed securities option and futures contracts insurance policies

13

II. Financial Markets where financial instruments are bought and sold

these markets provide liquidity for buying/selling information through prices risk-sharing among buyers/sellers classified in various ways…

14

Primary vs. Secondary Markets

primary market newly issued securities -- investment banking secondary market brokers match buyers and sellers dealers act as buyers and sellers -- “market-makers”

15

Debt vs. Equity Markets debt security cash flows are fixed

bonds, loans equity security cash flow variable, residual common stock

16

Exchanges vs. OTC Markets

buying & selling of securities in physical location NYSE OTC (over-the-counter) dealers in many locations buy & sell securities

dealers in many locations buy & sell securities.")

17

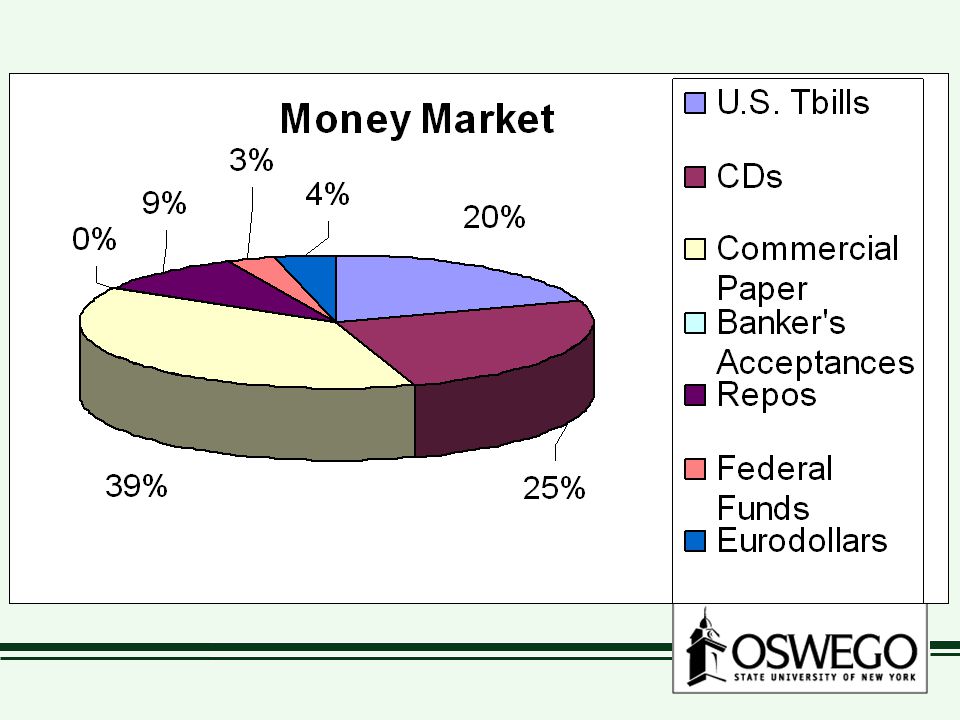

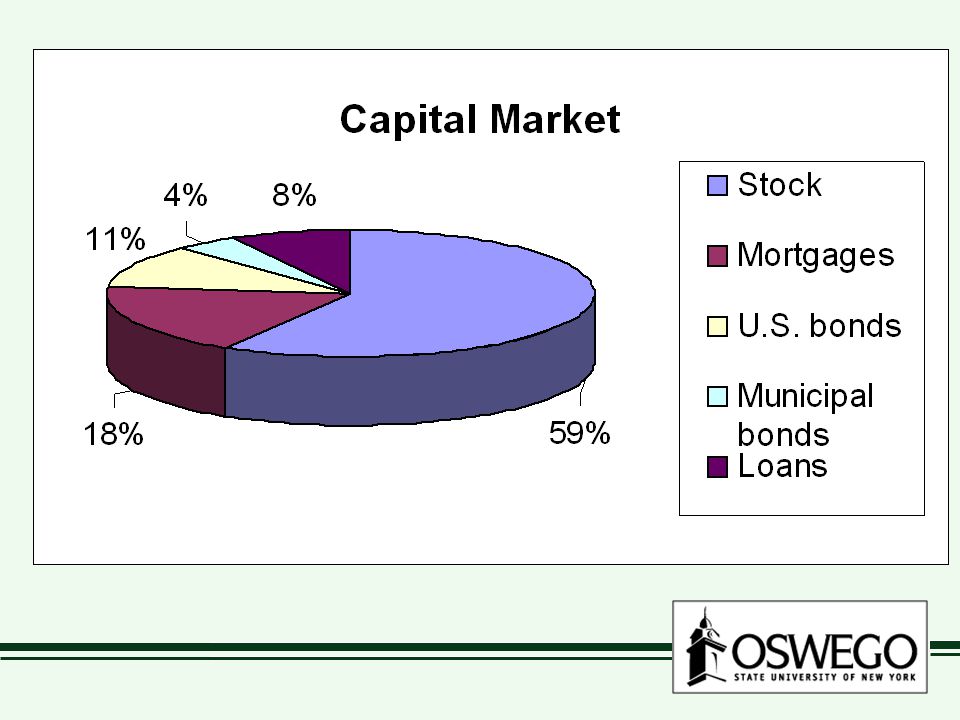

Money vs. Capital Markets

money market short-term debt securities (up to 1 yr.) highly liquid, low risk capital market longer-term debt equity

highly liquid, low risk. capital market. longer-term debt. equity.")

20

III. Financial Institutions

aka. financial intermediaries Why have them? Transactions costs search costs to find borrower & lender contract costs economies of scale

21

Risk sharing intermediaries are experts at bearing risk Asset transformation short-term to long-term illiquid to liquid

22

Types of intermediaries

Depository institutions “banks” accept deposits, make loans

23

Commercial banks largest in total assets least restricted Savings & Loans originally restricted to savings deposits and mortgages less restricted today Credit Unions consumer loans nonprofit, organized around a group

24

Nondepository institutions insurance companies pension funds

finance companies Mortgage, auto, office equipment Securities firms gov’t-sponsored enterprises (GSEs)

")

25

Subprime mortgage meltdown

Hit several types of financial institutions: finance companies Countrywide securities firms Citigroup, Merrill Lynch GSEs Fannie Mae, Freddie Mac

Similar presentations

Households Firms Government Foreigners Financial Markets.>")

and borrowers.>")