Download presentation

Presentation is loading. Please wait.

1

Satisfaction with the local grocery store mix: A consumer perspective

Harmen Oppewal (Monash University) Ian Clarke (University of Edinburgh) Malcolm Kirkup (University of Exeter) Supermarket Power in Australia Symposium, Melbourne, 1 August 2013 Department of Marketing

Ian Clarke (University of Edinburgh) Malcolm Kirkup (University of Exeter) Supermarket Power in Australia Symposium, Melbourne, 1 August Department of Marketing.")

2

UK grocery sector issues similar but further developed and more debated than in Australia

Concerns over increasing concentration Supply chain issues & accusations of abuse of power Town centre v out of town locations Role of the small store & supermarkets moving into the convenience sector Homogenisation of high street Food deserts debate Overseas entrants incl ALDI and Walmart Private labels Loyalty cards Unit pricing Organic and local products Online channel Consumer concern and activism Comp Commission investigations 2000, 2008 Incl 2011 Portas review of high street

5

Aim and approach of this research

Explore what it means to have variety in the retail setting, what influences it, and how it affects consumer perceptions of choice Assess how concentration, format diversity and proximity to stores influence satisfaction with the local store mix Approach Consumer satisfaction survey among consumers from different neigbourhoods, across different cities Respondents rated their current neighbourhood’s provision and then completed a set of ‘stated preference’ tasks.

6

Some relevant literature

Consumer perceptions of local choice Quality of consumers’ lives affected by neighbourhoods in which they live, including retail provision Clarke et al., 2006; Jackson et al., 2006 Perception of assortments within stores Effects of assortment reductions and extensions Botti & Iyengar, 2006; Broniarczyk et al, 1998; Iyengar & Lepper, 1999; Oppewal & Koelemeijer, 2005 Access and disadvantage Benefits of co-location Arentze et al., 2005; Dellaert et al., 1998, Oppewal et al, 1997 Role of location and distance Dawson et al 2008; Talukdar 2008; Wrigley et al 2003 Handy & Niemeier 1997;

7

Stated preference study (Clarke et al 2012)

Personal interviews across the population in one ‘average’ town in Mid England (Worcester) (n=288) Respondents evaluate hypothetical store mixes for their local area Local parade of shops within 5 minutes Location at 15 minutes but near the town centre Location at 15 minutes towards the edge of town Presence/absence of 8 individual stores varied across the three locations Tesco (3x); Sainsbury; ASDA; Morrison; Somerfield Tesco Express; Independent small retailer Satisfaction with store mix 1=very unsatisfied, .., 5 = very satisfied

(n=288) Respondents evaluate hypothetical store mixes for their local area. Local parade of shops within 5 minutes. Location at 15 minutes but near the town centre. Location at 15 minutes towards the edge of town. Presence/absence of 8 individual stores varied across the three locations. Tesco (3x); Sainsbury; ASDA; Morrison; Somerfield. Tesco Express; Independent small retailer. Satisfaction with store mix. 1=very unsatisfied, .., 5 = very satisfied.")

8

Stated preference task

“Imagine your neighbourhood has a completely different range of food store available…” “How satisfied or dissatisfied would you be with this mix of stores” (1= very dissatisfied, 5 = very satisfied)

")

9

Store presence effects (regression parameters)

Including one interaction (5TescoSup x 5Sainsup) – reverse coded so shown here as positive but has to be DEDUCTED.

– reverse coded so shown here as positive but has to be DEDUCTED.")

10

Findings Supermarkets at 5 minutes have largest contribution

Tesco more than Sainsbury If both present then joint effect is reduced Only minimal contribution of small stores Small effect for independent, does not depend on presence of other retailers; mainly reduces dissatisfaction No effect for Tesco Express at 15 minutes Effects at 15 minutes vary by brand and location ASDA and Morrison larger effects than (second) Tesco If Tesco at 5 minutes then smaller effects of ASDA/Morrison

Tesco. If Tesco at 5 minutes then smaller effects of ASDA/Morrison.")

11

Main findings Consumers are more satisfied if they have more grocery stores available Consumers are more satisfied if they have a greater variety of brands and formats available Published as: Clarke I., M. Kirkup and H. Oppewal (2012), “Consumer satisfaction with local retail diversity in the UK: effects of supermarket access, brand variety, and social deprivation” Environment and Planning A, 44:

, Consumer satisfaction with local retail diversity in the UK: effects of supermarket access, brand variety, and social deprivation Environment and Planning A, 44:")

12

Extension (similar approach, separate sample)

Role of online shopping Extra condition varied presence of online channel No significant effect: online is no substitute for brick and mortar store access Role of discounters ALDI adds significant benefit, but only if a main supermarket is also present Role of premium stores Waitrose adds only modest amount

13

Store presence effects (study 2)

Including two interactions

14

Next steps in the research

Real neighbourhood evaluations Effect of actual store mix and access levels Comparison across two towns With different levels of concentration

15

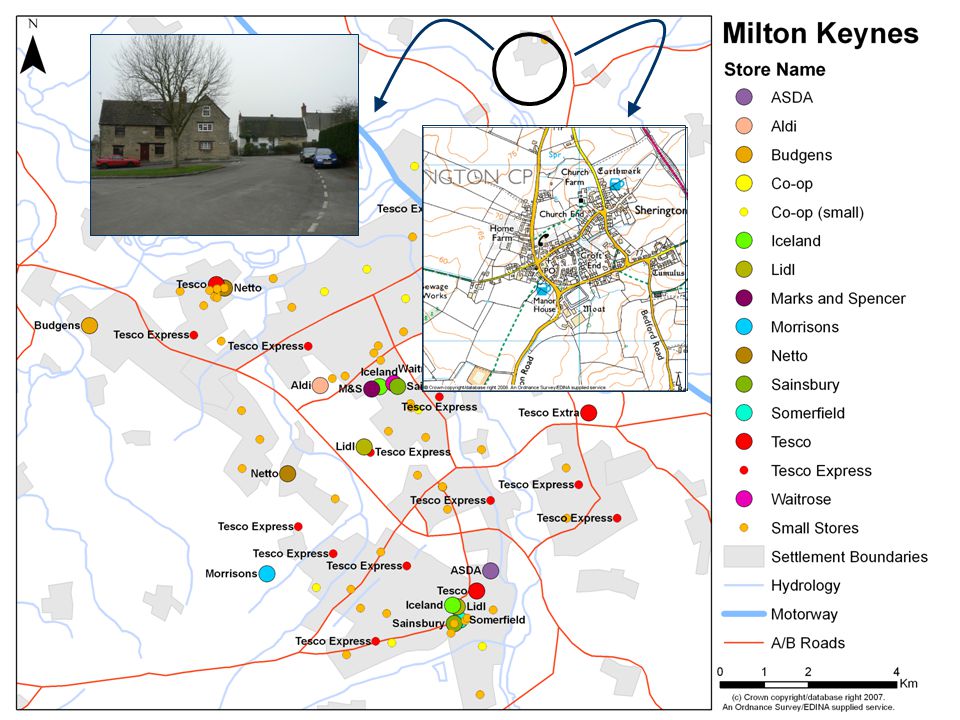

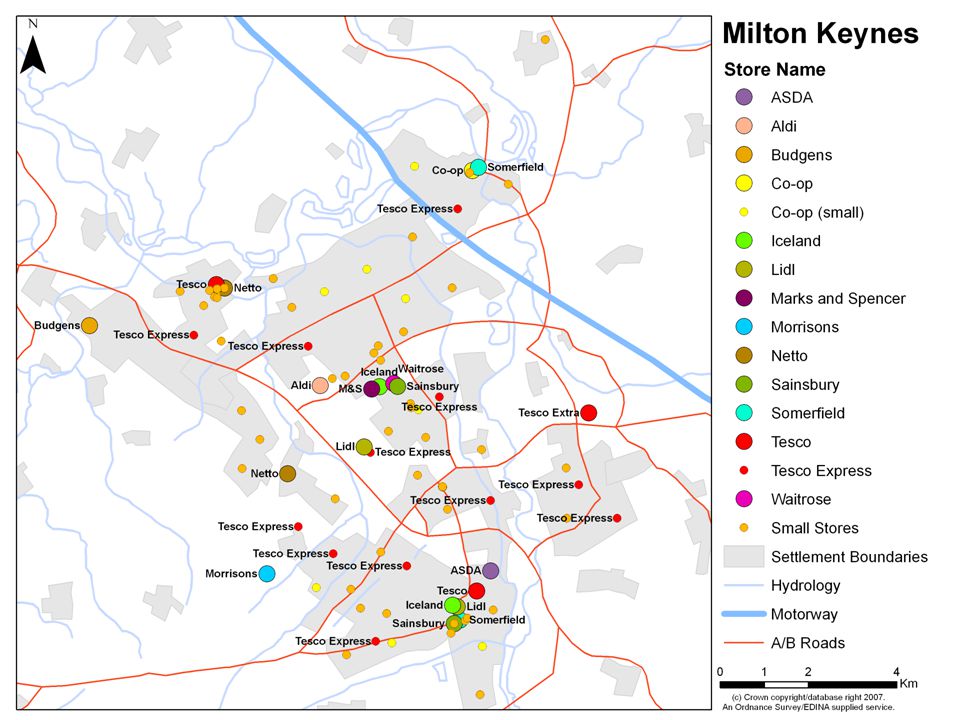

Study Areas Telford Milton Keynes

Other research focused on most extreme cases - e.g deprived estates We’ve looked at ‘Middle England’ - more average scenarios Guided by the CC rankings from 2000 on concentration Not a study of these towns in essence, but they provide a framework for accessing our neighbourhoods as Unit of Analysis Milton Keynes

16

Retail supply in the two towns

Town A = Telford: Low level of concentration of main supermarket brands (HHI<1500) and a Tesco market share of only 17%, Town B = Milton Keynes: High level of concentration (Herfindahl-Hirschman Index >3000) and a high Tesco market share of 52% (at time of surveying) Approximately 20 supermarkets and 50 small local supermarkets and convenience stores in each town All main competitors present Similar presence of discounters and of high end luxury supermarkets

and a Tesco market share of only 17%, Town B = Milton Keynes: High level of concentration (Herfindahl-Hirschman Index >3000) and a high Tesco market share of 52% (at time of surveying) Approximately 20 supermarkets and 50 small local supermarkets and convenience stores in each town. All main competitors present. Similar presence of discounters and of high end luxury supermarkets.")

17

Illustrates what local dominance can mean - for those of you not familiar with the MK situation

Had opportunity to look at area where Tesco is highly represented Interested in how consumer sees dominance - effect of local competition on choice

19

Methodology Careful selection of nine local areas in each town

60 face to face interviews in each area to collect consumer evaluations of the retail supply Location data for all supermarkets combined with travel time data for all area postcodes. Resulted in each respondent’s available set of stores, including their brands and travel times. Selected nearest six supermarkets for each respondent

23

Independent variables: Store mix across six nearest supermarkets

X1= travel time to nearest supermarket; X2= extra travel time to the next (third) nearest supermarket; X3= proportion (presence) of discount stores among the respondent’s six nearest stores; X4= proportion of ‘high end’ stores among the respondent’s six nearest stores; X5= proportion of main party supermarkets among the respondent’s six nearest stores; X6= proportion of Tesco stores within the selection of main party supermarkets. X7= dummy variable for whether the householder has a car available more than 3 days a week for shopping; X8= Town dummy

nearest supermarket; X3= proportion (presence) of discount stores among the respondent’s six nearest stores; X4= proportion of ‘high end’ stores among the respondent’s six nearest stores; X5= proportion of main party supermarkets among the respondent’s six nearest stores; X6= proportion of Tesco stores within the selection of main party supermarkets. X7= dummy variable for whether the householder has a car available more than 3 days a week for shopping; X8= Town dummy.")

24

Descriptive statistics

25

Analysis: mixed linear regression

18 neighbourhoods as groups, each has random intercept Null model (only random intercepts) has intragroup correlation coefficient of .25. The model is significant (Chi-2(7) = 42.59, p<.001) and explains 27% of the between group variance and 2% of the within group variance. No improvement when including distance and store mix variables as random slopes (after within-group mean centering) .25 intra class correlation 25% of the variance in sat scores is attributable to between group (neigbhourhood) differences 27% between group var vs only 2% within group variance So huge multilevel effect! – but not surprising.

has intragroup correlation coefficient of .25. The model is significant (Chi-2(7) = 42.59, p<.001) and explains 27% of the between group variance and 2% of the within group variance. No improvement when including distance and store mix variables as random slopes (after within-group mean centering) .25 intra class correlation 25% of the variance in sat scores is attributable to between group (neigbhourhood) differences. 27% between group var vs only 2% within group variance. So huge multilevel effect! – but not surprising.")

26

Analysis: mixed linear regression (18 groups; 1129 respondents)

")

27

Results (1) Distance to nearest supermarket: no effect

But negative effect of distance to next nearest So it is the access to multiple supermarkets in the vicinity that is important Variety: Presence of a discount store increases satisfaction No effect of the presence of a high end store So the effect is due to discounter availability, not mere variety

28

Results (2) Proportion of Tesco’s negatively affects satisfaction

Consumers are more satisfied when there is more brand variety among the main supermarkets Respondents in Low Concentration town more satisfied than those in HC town The High Concentration town also included more Tesco branded convenience stores Higher satisfaction if car available No interaction with distance variables

29

Conclusions Consumers in the town less dominated by Tesco significantly more satisfied with their local mix Satisfaction does not depend on distance to the nearest supermarket; instead it depends on the combined distances to the set of nearest stores Consumers value brand variety and discounter Policy makers should focus on variety, not just on providing ‘minimal’ access levels But there may be vulnerable subgroups who need access No indication that online can provide a substitute

30

Do these findings transfer to the Australian context?

Yes, in principle, – But differences to note Number of competitors Regulatory environment … Still an open research question Research pending Partnering (Monash): Higher levels of concentration Higher dependence on car

: Higher levels of concentration. Higher dependence on car.")

31

Questions & discussion

Thank you! Questions & discussion

32

Satisfaction with the local grocery store mix: A consumer perspective

Harmen Oppewal (Monash University) Ian Clarke (University of Edinburgh) Malcolm Kirkup (University of Exeter) Supermarket Power in Australia Symposium, Melbourne, 1 August 2013 Department of Marketing

Ian Clarke (University of Edinburgh) Malcolm Kirkup (University of Exeter) Supermarket Power in Australia Symposium, Melbourne, 1 August Department of Marketing.")

Similar presentations