Download presentation

Presentation is loading. Please wait.

1

GOLD as an asset class www.fpgindia.org1

2

Gold and India In 2009, total Indian gold demand touched USD 19bn = 15% of global market Over last decade, value of gold demand in India has increased @13% per year Currently India and China together account for 25% of annual gold demand Foundation asset in Indian household – jewellery and investment www.fpgindia.org2

3

Gold and India Savings rate estimated @ 30% Around 10% in invested in gold Traditional division between jewellery and investment overlap During H1CY10 Indian net retail investment in gold has increased by 264% to 93 tonnes (25% of Indias gold demand) Individuals purchases of coins and bars www.fpgindia.org3

Individuals purchases of coins and bars")

4

4

5

GOLD IMPORTS www.fpgindia.org5

6

Currently produces 0.5% of its annual consumption Between 1992 and 2009: Value of annual gold imports has risen by 1,015% Gold imports rose from ` 88 bn to ` 881 bn www.fpgindia.org6

7

Reasons for investing Diversification Hedge against inflation Volatililty (over the last 5 years) Sensex – 27% BSE 500 – 30% BSE Metal – 46% Gold – 23% www.fpgindia.org7

Sensex – 27% BSE 500 – 30% BSE Metal – 46% Gold – 23%")

8

Reasons for investing Better returns in shorter periods (over last 5 yrs ending Sept 30, 2010) Gold – 37% Sensex – 1% Safe haven US Dollar hedge www.fpgindia.org8

Gold – 37% Sensex – 1% Safe haven US Dollar hedge")

9

In risk management and portfolio theory it is not only individual volatilities that matter it is also how assets interact with each other, i.e., their correlation structure Gold tends to have little correlation with many asset classes strong viable choice for portfolio diversification Some are peculiar to the gold market, underpinning its lack of correlation to other assets. These include: fashion trends, marketing campaigns, the Indian wedding season, religious festivals, gold mine exploration spending, new discoveries of gold, the cost of finding and mining gold, and central banks strategic reserve decisions. www.fpgindia.org9

10

Gold avenues Physical gold Gold ETF Gold mutual funds (FoFs) E-Gold through NSEL India Post gold retail program Gold-linked microfinance scheme Gold through commodities exchange www.fpgindia.org10

E-Gold through NSEL India Post gold retail program Gold-linked microfinance scheme Gold through commodities exchange")

11

Gold ETF vs E-Gold Gold ETF an exchange traded mutual fund scheme it does not necessarily hold physical gold stock at its fullest cannot be redeemed for physical gold No exchange possible E-Gold physical gold held in dematerialized form which can be traded electronically at NSEL a digital gold currency that allows you to trade redeem physical gold from your demat account retail investors can soon exchange their e-Gold units issued by NSEL with selected jewellery outlets, in the form of jewellery www.fpgindia.org11

12

Gold ETF vs E-Gold Gold ETF Tradable only during market hours intends to mirror gold prices. Charges - around 1%-1.5% per annum Only Gold ETFs at present E-Gold E-Gold is tradable for longer hours (1000 hrs to 2330 hrs) spot rates of gold no custody charges Gold, silver, zinc and copper www.fpgindia.org12

spot rates of gold no custody charges Gold, silver, zinc and copper")

13

Categories3 yr CAGR5 yr CAGR10 yr CAGR Gold24.3421.9017.84 Equity funds-0.2316.3322.78 Gilt funds7.336.799.23 Debt funds7.046.917.80 www.fpgindia.org13 Figures as on Dec. 31, 2010 Source: CRISIL

14

www.fpgindia.org14 Price of gold over the years (in ` )

")

15

www.fpgindia.org15 Source: RBI

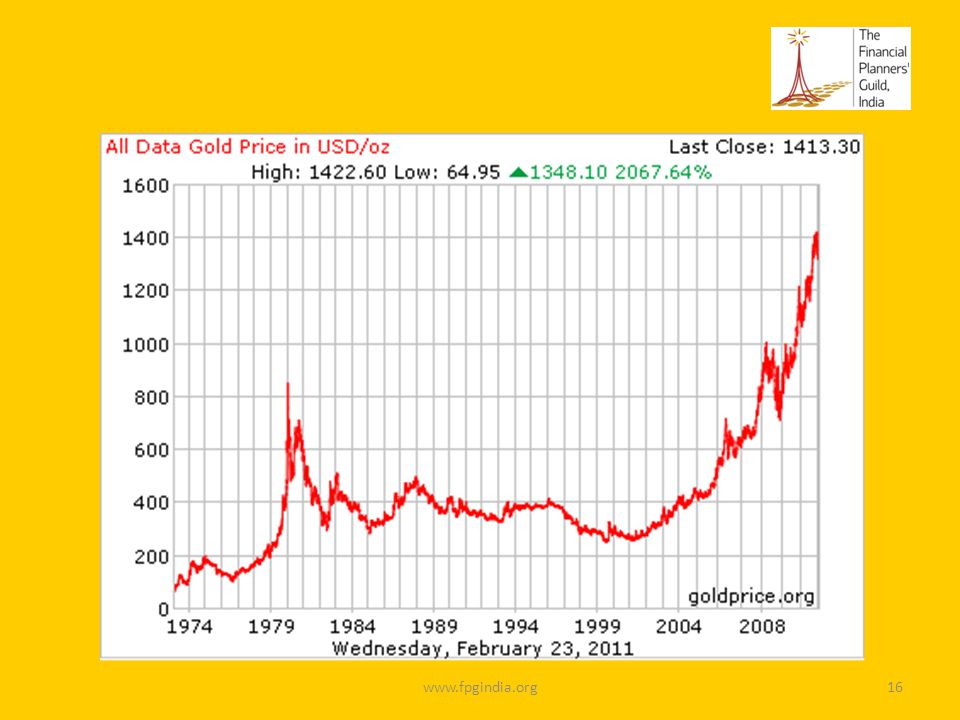

16

www.fpgindia.org16

17

INTERESTING FACTS Indian context www.fpgindia.org17

18

Returns over the last 36 years 5% plus in the last 24 years 7% in the last 20 years 16% plus in the last 11 years 33 years of positive returns y-o-y www.fpgindia.org18

19

Returns over the last 36 years 3 years of negative return 1992 India Economic Crisis Sensex went down from a high of 4546 to close the year at 2615 Gold gave a return of -2% 1997-98 Asian Financial Crisis Sensex went down in the same period after touching a high of 4605 to close 1998 at 3055 levels Gold gave a negative return of -14% in 1997 and -1.8% in 1998 www.fpgindia.org19

20

Largest producer of gold –China (almost a tenth of worlds supply) By 2014, China will overtake India as the largest user of gold www.fpgindia.org20

By 2014, China will overtake India as the largest user of gold")

21

The gold supply is limited: all the gold ever mined would fit into a storage room about 55 feet long, 55 feet tall and 55 feet wide www.fpgindia.org21

22

VIEWS ON GOLD For 2011 www.fpgindia.org22

23

10 years of consecutive rise 25% rise in 2010 Expect trend to continue in 2011 www.fpgindia.org23

24

Combination of factors which encourages a high price for gold: safe haven in the face of a very delicate global economic situation uncertainty generated in the European financial system weakness of the dollar growth in inflation in Asian countries and emerging markets excess of liquidity in the USA www.fpgindia.org24

25

Jim Rogers, the commodities investment guru: gold will continue to rise over the next decade, although it may fall off before it reaches historical values adjusted for inflation Swiss private bank, Sarasin: the price of gold over recent months has been mainly driven by investment demand. This is principally reflected by the growing quantities of gold held in exchange-traded funds (ETF) www.fpgindia.org25

")

26

German newspaper Handelsblat: central banks have moved from being sellers to buyers of this metal and this is an unequivocal signal about the safest place for investors www.fpgindia.org26

27

GOLD ETF www.fpgindia.org27

28

Gold ETF Pros Investments can be made in small amounts Safety and security Easy to transact Cheaper than investing in physical gold Transparency of prices Lower cost of holding Cons Need to be computer savvy No possibility of doing a SIP Liquidity could be an issue in case of emergencies www.fpgindia.org28

29

www.fpgindia.org29

30

PHYSICAL GOLD www.fpgindia.org30

31

Physical gold Pros Can be purchased from any bank or jeweller Feel the product Can be sold back to jeweller Can be purchased in cash Used for storage of unaccounted money Cons Cannot be sold back to a bank Security Guarantee of quality High cost at time of purchase and sale High cost of storage www.fpgindia.org31

32

GOLD FUND OF FUNDS www.fpgindia.org32

33

Gold FoFs Pros SIP/STP/SWP is possible Good for small investors - start with amounts of as low as ` 100 or ` 500 No demat account is required Cons Higher costs than ETFs Minimum annual cost of 1.5% p.a. Gold mining fund FoFs track the prices of the mining companies and not the price of gold Exit load of 2% in year 1 www.fpgindia.org33

34

E-GOLD www.fpgindia.org34

35

E-gold Pros Seamless entry and exit Safety and security Zero holding cost Convertibility into physical gold (takes 3-4 days) Working on conversion of e- gold in demat directly into jewellery items Cons Capital Gains – 3 yrs Still very new in India. Downsides are still not known www.fpgindia.org35

36

TAXATION www.fpgindia.org36

37

Varies according to investment route Treated as a capital asset Liable for capital gains tax Tax treatment similar to a debt fund www.fpgindia.org37

38

www.fpgindia.org38 TypeHolding periodTaxation Physical gold STCGLess than 3 yrsGains added to income and taxed as per individuals slab LTCGMore than 3 yrs20% with indexation + 3% education cess Post DTCGains added to income and taxed as per individuals slab; for LTCG indexation benefit applicable Gold ETFs STCGLess than 1 yrGains added to income and taxed as per individuals slab LTCGMore than 1 yr10% without indexation or 20% with indexation (whichever is less) + 3% education cess Post DTCGains added to income and taxed as per individuals slab Source: Outlook Money

+ 3% education cess Post DTCGains added to income and taxed as per individuals slab Source: Outlook Money")

39

www.fpgindia.org39 TypeHolding periodTaxation Gold FoFs STCGLess than 1 yrGains added to income and taxed as per individuals slab LTCGMore than 1 yr20% with indexation + 3% education cess Post DTC Gains added to income and taxed as per individuals slab; for LTCG indexation benefit applicable Source: Outlook Money

40

GOLD IN FINANCIAL PLANNING www.fpgindia.org40

41

Important part of asset allocation just after the 9/11 terror attacks in the US, while both stock markets and bond markets crashed across the world, gold held steady and, in fact, rose on that day by 6% during the financial crisis in 2008, gold prices increased by 28% while the S&P CNX Nifty (Nifty) declined by 51% during the year www.fpgindia.org41

declined by 51% during the year")

42

Idea is to use it as a defensive asset class Good for managing risk in a portfolio Gold market is highly liquid and many gold bullion investments have neither credit nor counterparty risk Should ideally be in the region of 5%. 10% tops www.fpgindia.org42

43

Strong case for gold to be allocated as an asset class on its own merits part commodity part luxury consumption good part financial asset its price does not always behave like other asset classes and especially not other commodities www.fpgindia.org43

44

STUDY David Ranson of Wainwright Economics (in Oregon) (Source: The Economist – Aug 4, 2010) www.fpgindia.org44

(Source: The Economist – Aug 4, 2010)")

45

Gold along with corporate bond spreads, as the key Gold is the best indicator of future inflation Corporate bond spreads are a predictor of economic growth when spreads are falling, the economy is improving, and when spreads are widening, the economy is deteriorating www.fpgindia.org45

46

Gold down, spreads down This indicates a period of disinflationary growth, so buy equities. Gold down, spreads up This indicates a weakening economy with disinflation, so buy government bonds. Gold up, spreads down This indicates inflationary growth, so buy commodities (an equally-weighted basket of the five components in the Goldman Sachs Commodities Index: energy, industrial metals, precious metals, agriculture and livestock) Gold up, spreads up Growth is decelerating and inflation is accelerating, so buy gold. www.fpgindia.org46

Gold up, spreads up Growth is decelerating and inflation is accelerating, so buy gold.")

47

Thank you for your time www.fpgindia.org47

Similar presentations