Download presentation

Presentation is loading. Please wait.

1

Grain Outlook ISU Extension Swine In-Service Ames, Iowa Nov. 1, 2012

Chad Hart Associate Professor/Grain Markets Specialist 1 1

2

U.S. Corn Supply and Use 2008 2009 2010 2011 2012 Area Planted

(mil. acres) 86.0 86.4 88.2 91.9 96.9 Yield (bu./acre) 153.9 164.7 152.8 147.2 122.0 Production (mil. bu.) 12,092 13,092 12,447 12,358 10,706 Beg. Stocks 1,624 1,673 1,708 1,128 988 Imports 14 8 28 75 Total Supply 13,729 14,774 14,182 13,514 11,769 Feed & Residual 5,182 5,125 4,793 4,562 4,150 Ethanol 3,709 4,591 5,021 5,000 4,500 Food, Seed, & Other 1,316 1,370 1,407 1,421 1,350 Exports 1,849 1,980 1,835 1,543 1,150 Total Use 12,056 13,066 13,055 12,526 11,150 Ending Stocks 619 Season-Average Price ($/bu.) 4.06 3.55 5.18 6.22 7.80 These are the latest numbers from USDA. Record production and demand is gone and was replaced by record prices. All sectors of demand took major cuts. Ending stocks are projected to be at pipeline levels. Source: USDA-WAOB 2 2

Yield. (bu./acre) Production. (mil. bu.) 12, , , , ,706. Beg. Stocks. 1,624. 1,673. 1,708. 1, Imports Total Supply. 13, , , , ,769. Feed & Residual. 5,182. 5,125. 4,793. 4,562. 4,150. Ethanol. 3,709. 4,591. 5,021. 5,000. 4,500. Food, Seed, & Other. 1,316. 1,370. 1,407. 1,421. 1,350. Exports. 1,849. 1,980. 1,835. 1,543. 1,150. Total Use. 12, , , , ,150. Ending Stocks Season-Average Price. ($/bu.) These are the latest numbers from USDA. Record production and demand is gone and was replaced by record prices. All sectors of demand took major cuts. Ending stocks are projected to be at pipeline levels. Source: USDA-WAOB")

3

U.S. Soybean Supply and Use

2008 2009 2010 2011 2012 Area Planted (mil. acres) 75.7 77.5 77.4 75.0 77.2 Yield (bu./acre) 39.7 44.0 43.5 41.9 37.8 Production (mil. bu.) 2,967 3,359 3,329 3,094 2,860 Beg. Stocks 205 138 151 215 169 Imports 13 15 14 16 20 Total Supply 3,185 3,512 3,495 3,325 3,050 Crush 1,662 1,752 1,648 1,703 1,540 Seed & Residual 106 110 130 92 115 Exports 1,279 1,499 1,501 1,360 1,265 Total Use 3,047 3,361 3,280 3,155 2,920 Ending Stocks Season-Average Price ($/bu.) 9.97 9.59 11.30 12.50 15.25 For soybeans, a tight market continues to get tighter. USDA ratcheted down demand for the new crop to hold 2012/13 ending stocks at 115 million bushels. As with corn, all sectors of demand took a big cut. Source: USDA-WAOB 3 3

Yield. (bu./acre) Production. (mil. bu.) 2,967. 3,359. 3,329. 3,094. 2,860. Beg. Stocks Imports Total Supply. 3,185. 3,512. 3,495. 3,325. 3,050. Crush. 1,662. 1,752. 1,648. 1,703. 1,540. Seed & Residual Exports. 1,279. 1,499. 1,501. 1,360. 1,265. Total Use. 3,047. 3,361. 3,280. 3,155. 2,920. Ending Stocks. Season-Average Price. ($/bu.) For soybeans, a tight market continues to get tighter. USDA ratcheted down demand for the new crop to hold 2012/13 ending stocks at 115 million bushels. As with corn, all sectors of demand took a big cut. Source: USDA-WAOB")

4

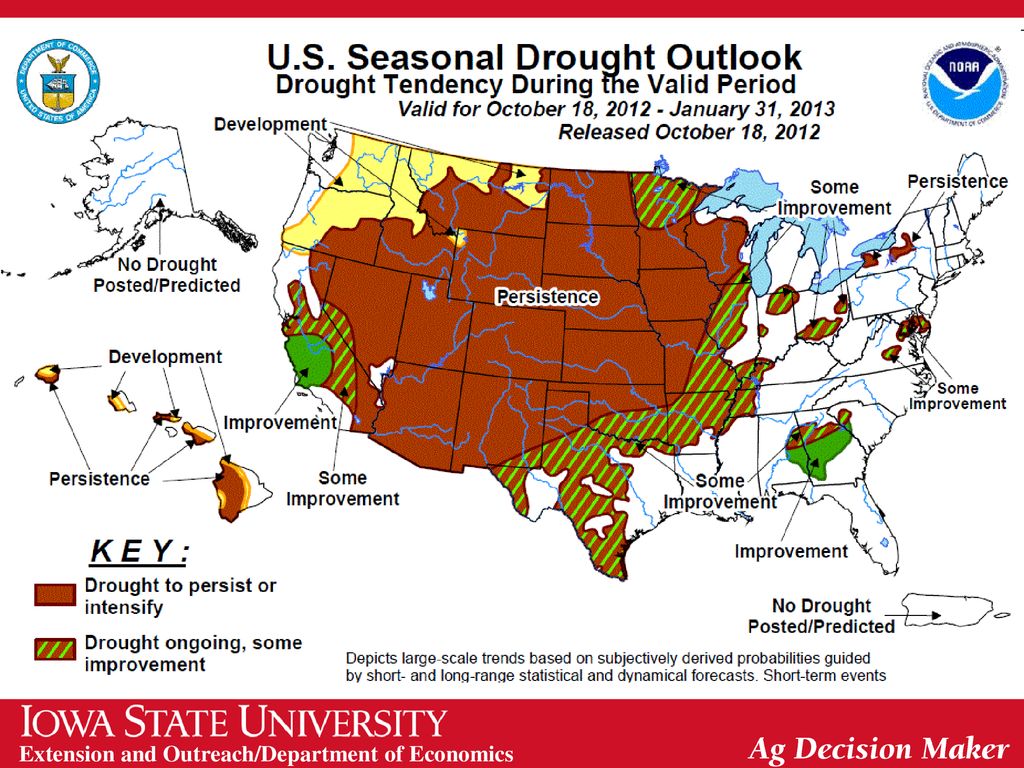

Crop Conditions Source: USDA-NASS

But dry conditions have weakened the crops, as the crop conditions show. The USDA update reflects the scale of yield loss as they have taken over 40 bushels from corn and nearly 8 bushels from soybeans. Source: USDA-NASS

5

Prices Prices have risen and fallen with the temperatures.

6

Objective Corn Yield Data

USDA crop adjusters found grain weights well below those for the last 8 years. Source: USDA-NASS

7

Objective Soybean Yield Data

USDA crop adjusters found pod numbers well below those for the last 8 years. Source: USDA-NASS

8

Projected Corn Yields Yields (bu/acre) 2011 2012 % Change

United States 147.2 122 -17% Iowa 172 140 -19% Illinois 157 98 -38% Nebraska 160 142 -11% Minnesota 156 168 8% Indiana 146 100 -32% South Dakota 132 94 -29% Wisconsin 127 Ohio 158 123 -22% Kansas 107 91 -15% Missouri 114 75 -34%

9

Projected Soybean Yields

Yields (bu/acre) 2011 2012 % Change United States 41.9 37.8 -10% Iowa 51.5 43 -17% Illinois 47.5 39 -18% Minnesota 10% Nebraska 54 41 -24% Indiana 45.5 Ohio 48 Missouri 36.5 30 South Dakota 37 28 Arkansas 38.5 1% North Dakota 29 34 17%

% Change. United States % Iowa % Illinois % Minnesota. 10% Nebraska % Indiana Ohio. 48. Missouri South Dakota Arkansas % North Dakota %")

10

World Corn Production Source: USDA-WAOB

Global corn production took a hit last month, with Canada and Europe seeing reductions in potential corn production. Source: USDA-WAOB 10 10

11

World Soybean Production

Soybean prices have spurred on increased soybean plantings worldwide. South America will lead the charge. Source: USDA-WAOB 11 11

12

Corn Export Shifts Source: USDA-FAS

13

Soy Export Shifts Source: USDA-FAS

14

Corn Grind for Ethanol Negative margins at some ethanol plants have dragged down production.

15

U.S. Blended Gasoline Consumption

7.6 bil. gal. But the industry still faces blend wall issues as fuel consumption has dropped with the economy and the E-10 market is basically full. 7.4 bil. gal. Source: DOE-EIA, via USDA-ERS

16

Current Corn Futures 6.95 6.00 5.65 Source: CME Group, 10/30/2012

17

Current Soybean Futures

14.48 12.68 12.27 Source: CME Group, 10/30/2012

18

Early Prices for 2013 Crops 2013 crop prices are still strong to entice acreage to remain in production.

19

Total Acreage Shift Source: USDA-NASS

We brought back a lot of acres in Can we hold them in 2013? Source: USDA-NASS

20

Acreage Shift by State Top: Planted in 2012 Bottom: Change from 2011

Weather was great for planting in 2012 (just not for producing). To hold acreage we will need great planting weather again. Top: Planted in 2012 Bottom: Change from 2011 Units: 1,000 acres Source: USDA-NASS

. To hold acreage we will need great planting weather again. Top: Planted in Bottom: Change from Units: 1,000 acres. Source: USDA-NASS.")

22

Acreage Shift by Crop Acreage change from 2011 Units: 1,000 acres

Cotton will likely give up acreage again. But with crop prices strong across the board, the acreage battle could be interesting in 2013. Source: USDA-NASS

23

Thoughts for 2012 and Beyond

Supply/demand concerns Soil moisture issues Biofuel and export strength Worldwide response to drought-induced pricing 2012/13 USDA Futures (10/30/12) 2013/14 Corn $7.80 $6.95 $6.00 Soybeans $15.25 $14.48 $12.68

2013/14. Corn. $7.80. $6.95. $6.00. Soybeans. $ $ $")

24

Thank you for your time. Any questions. My web site: http://www. econ

Thank you for your time! Any questions? My web site: Iowa Farm Outlook: Ag Decision Maker:

Similar presentations