Download presentation

Presentation is loading. Please wait.

1

Markets, Policy, and Outlook

Iowa Corn Growers Coralville, Iowa Sept. 7, 2012 Chad Hart Associate Professor/Grain Markets Specialist 1 1

2

U.S. Corn Supply and Use 2008 2009 2010 2011 2012 Area Planted

(mil. acres) 86.0 86.4 88.2 91.9 96.4 Yield (bu./acre) 153.9 164.7 152.8 147.2 123.4 Production (mil. bu.) 12,092 13,092 12,447 12,358 10,779 Beg. Stocks 1,624 1,673 1,708 1,128 1,021 Imports 14 8 28 25 75 Total Supply 13,729 14,774 14,182 13,511 11,875 Feed & Residual 5,182 5,125 4,793 4,550 4,075 Ethanol 3,709 4,591 5,021 5,000 4,500 Food, Seed, & Other 1,316 1,370 1,407 1,390 1,350 Exports 1,849 1,980 1,835 1,550 1,300 Total Use 12,056 13,066 13,055 12,490 11,225 Ending Stocks 650 Season-Average Price ($/bu.) 4.06 3.55 5.18 6.25 8.20 These are the latest numbers from USDA. Record production and demand is gone and was replaced by record prices. All sectors of demand took major cuts. Ending stocks are projected to be at pipeline levels. Source: USDA-WAOB 2 2

Yield. (bu./acre) Production. (mil. bu.) 12, , , , ,779. Beg. Stocks. 1,624. 1,673. 1,708. 1,128. 1,021. Imports Total Supply. 13, , , , ,875. Feed & Residual. 5,182. 5,125. 4,793. 4,550. 4,075. Ethanol. 3,709. 4,591. 5,021. 5,000. 4,500. Food, Seed, & Other. 1,316. 1,370. 1,407. 1,390. 1,350. Exports. 1,849. 1,980. 1,835. 1,550. 1,300. Total Use. 12, , , , ,225. Ending Stocks Season-Average Price. ($/bu.) These are the latest numbers from USDA. Record production and demand is gone and was replaced by record prices. All sectors of demand took major cuts. Ending stocks are projected to be at pipeline levels. Source: USDA-WAOB")

3

U.S. Soybean Supply and Use

2008 2009 2010 2011 2012 Area Planted (mil. acres) 75.7 77.5 77.4 75.0 76.1 Yield (bu./acre) 39.7 44.0 43.5 41.5 36.1 Production (mil. bu.) 2,967 3,359 3,329 3,056 2,692 Beg. Stocks 205 138 151 215 145 Imports 13 15 14 20 Total Supply 3,185 3,512 3,495 3,286 2,857 Crush 1,662 1,752 1,648 1,690 1,515 Seed & Residual 106 110 130 101 116 Exports 1,279 1,499 1,501 1,350 1,110 Total Use 3,047 3,361 3,280 3,141 2,742 Ending Stocks 115 Season-Average Price ($/bu.) 9.97 9.59 11.30 12.45 16.00 For soybeans, a tight market continues to get tighter. USDA ratcheted down demand for the new crop to hold 2012/13 ending stocks at 115 million bushels. As with corn, all sectors of demand took a big cut. Source: USDA-WAOB 3 3

Yield. (bu./acre) Production. (mil. bu.) 2,967. 3,359. 3,329. 3,056. 2,692. Beg. Stocks Imports Total Supply. 3,185. 3,512. 3,495. 3,286. 2,857. Crush. 1,662. 1,752. 1,648. 1,690. 1,515. Seed & Residual Exports. 1,279. 1,499. 1,501. 1,350. 1,110. Total Use. 3,047. 3,361. 3,280. 3,141. 2,742. Ending Stocks Season-Average Price. ($/bu.) For soybeans, a tight market continues to get tighter. USDA ratcheted down demand for the new crop to hold 2012/13 ending stocks at 115 million bushels. As with corn, all sectors of demand took a big cut. Source: USDA-WAOB")

4

Prices Prices have risen with the temperatures.

5

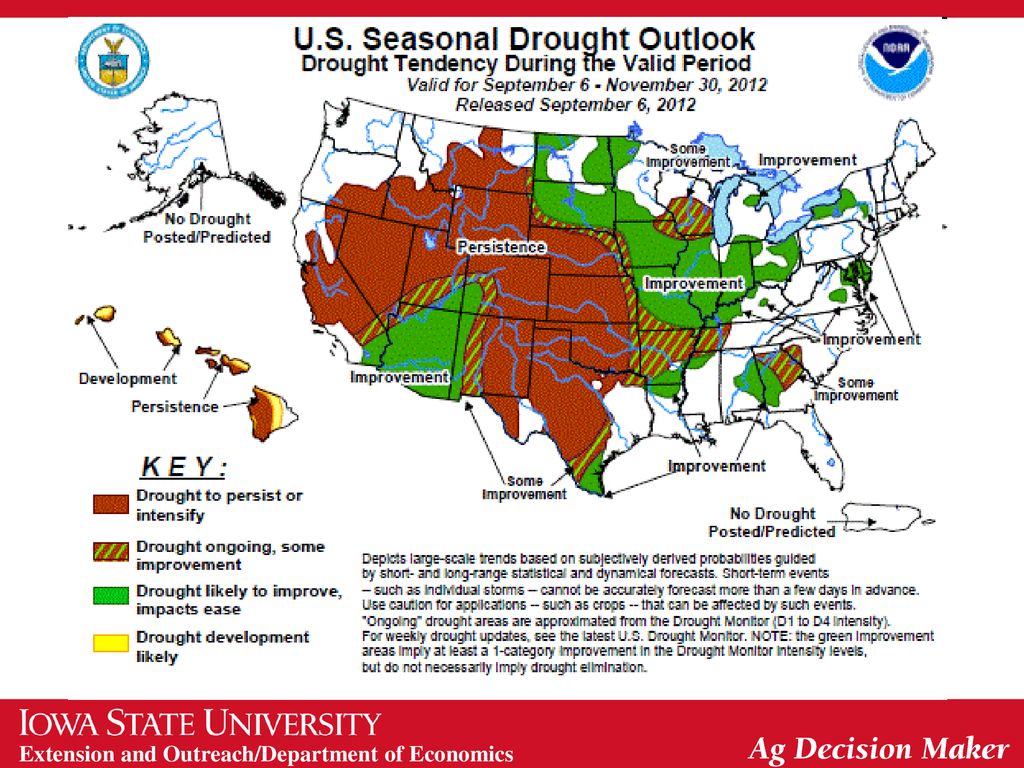

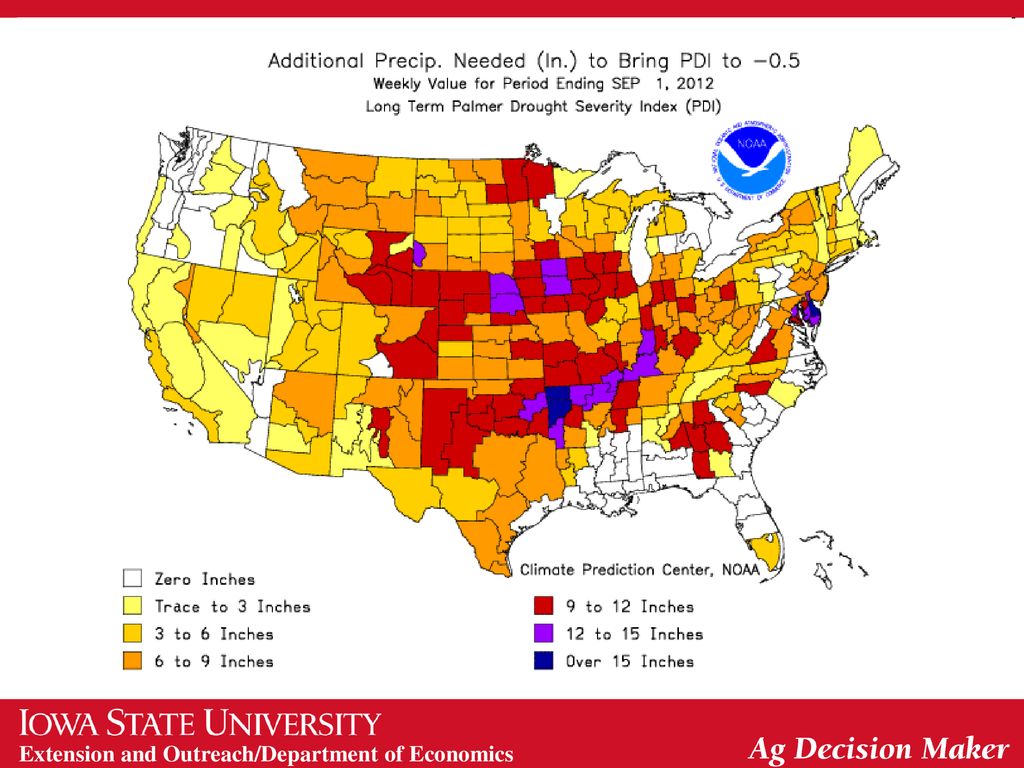

Crop Conditions Source: USDA-NASS

But dry conditions have weakened the crops, as the crop conditions show. The USDA update reflects the scale of yield loss as they have taken over 40 bushels from corn and nearly 8 bushels from soybeans. Source: USDA-NASS

6

Corn Harvested Acre Adjustments

USDA has accounted for some loss in corn harvested due to silage chopping and abandonment. Next month’s update will likely show more acres being lost.

7

Projected Corn Yields These are based on conditions around Aug. 1.

8

Objective Corn Yield Data

USDA crop adjusters found grain weights well below those for the last 8 years. Source: USDA-NASS

9

World Corn Production Source: USDA-WAOB

Global corn production took a hit last month, with Canada, Europe, and the former Soviet Union all seeing reductions in potential corn production. Source: USDA-WAOB 9 9

10

World Soybean Production

Soybean prices have spurred on increased soybean plantings worldwide. South America will lead the charge. Source: USDA-WAOB 10 10

11

Hog Crush Margin The Crush Margin is the return after the pig, corn and soybean meal costs. Carcass weight: 200 pounds Pig price: 50% of 5 mth out lean hog futures Corn: 10 bushels per pig Soybean meal: 150 pounds per pig Projected hog margins are well south of breakeven. Source: ISU Extension

12

Cattle Crush Margin The Crush Margin is the return after the feeder steer and corn costs. Live weight: pounds Feeder weight: 750 pounds Corn: 50 bushels per head Cattle returns look better next year, but feed costs remain a major concern. Source: ISU Extension

13

U.S. Meat Production & Prices

Higher feed costs have led to lower meat production projections. Source: USDA-WAOB 13 13

14

Corn Exports Source: USDA-FAS

Corn exports for the 2011 crop have been slow, with only Mexico and China buying more. Source: USDA-FAS

15

Soy Exports Source: USDA-FAS

2011 soybean exports are also lower, but have been improving for the last few months. The key market here is China and they have purchased a lot of soybeans recently. Source: USDA-FAS

16

Corn Advance Export Sales

Advance sales have backed off as prices have risen. Mexico and China continue to be our better markets. Source: USDA-FAS

17

Soy Advance Export Sales

Soybean advance sales have held up better. China is still the key to the soybean market. Source: USDA-FAS

18

Corn Grind for Ethanol Negative margins at some ethanol plants have dragged down production.

19

Ethanol Stocks Source: DOE-EIA

But stocks have begun to decline as we are in the heart of the summer driving season. Source: DOE-EIA

20

U.S. Blended Gasoline Consumption

7.6 bil. gal. But the industry still faces blend wall issues as fuel consumption has dropped with the economy and the E-10 market is basically full. 7.4 bil. gal. Source: DOE-EIA, via USDA-ERS

21

Projected 2012 Season-Average Corn Price

The drought has brought in some very strong and profitable prices.

22

Projected 2012 Season-Average Soy Price

The same is true for soybeans.

23

Prices Prices have risen with the temperatures.

24

Current Corn Futures 7.44 6.24 5.64 Source: CME Group, 9/6/2012

Based on current futures prices, national season-average cash price estimates for corn are $7.44 for the 2012 crop, $6.24 for 2013, and $5.64 for 2014. 5.64 Source: CME Group, 9/6/2012

25

Current Soybean Futures

16.23 For soybeans, the estimates are $16.23 for the 2012 crop, $13.17 for 2013, and $12.44 for 2014. 13.17 12.44 Source: CME Group, 9/6/2012

26

Early Prices for 2013 Crops 2013 crop prices are on the rise to entice acreage to remain in production.

27

Total Acreage Shift Source: USDA-NASS

We brought back a lot of acres in Can we hold them in 2013? Source: USDA-NASS

28

Acreage Shift by State Top: Planted in 2012 Bottom: Change from 2011

Weather was great for planting in 2012 (just not for producing). To hold acreage we will need great planting weather again. Top: Planted in 2012 Bottom: Change from 2011 Units: 1,000 acres Source: USDA-NASS

. To hold acreage we will need great planting weather again. Top: Planted in Bottom: Change from Units: 1,000 acres. Source: USDA-NASS.")

29

Acreage Shift by Crop Acreage change from 2011 Units: 1,000 acres

Cotton will likely give up acreage again. But with crop prices strong across the board, the acreage battle could be interesting in 2013. Source: USDA-NASS

30

Thoughts for 2013 and Beyond

Supply/demand concerns Soil moisture South America gets 1st chance to respond to drought pricing Will supply be able to keep pace with demand? Drought is pulling supply down But high prices are diminishing demand General economic conditions Continued worldwide economic recovery is a key for crop prices US job recovery, European financial concerns, China? 2012/13: USDA: Corn $8.20; Soy $16.00 Futures (as of 9/6/12): Corn $7.44; Soy $16.23 2013/14: Futures Corn $6.24; Soy $13.17 2014/15: Futures Corn $5.64; Soy $12.44

: Corn $7.44; Soy $ /14: Futures Corn $6.24; Soy $ /15: Futures Corn $5.64; Soy $")

33

2013 Crop Cost Estimates Source: ISU Extension Economics, July 2012

Open your book to page 84. On the screen you see our 2013 estimates. We’ll publish new estimates in January Note the historical costs of production on pages 97 and 98. Then on 99 you have a recent survey of current input costs. This changes over time. As crop values have gone up, the different input suppliers have responded. The level of fundamental driven change in input prices is worth discussing as well as the market driven changes. SEED UP 7% HERBICIDES UP 5% FOR NOW N PRICE IS NOW 60% NH3 AND 20% UAN AND UREA N DOWN; P DOWN P is for MAP and includes N value; K UNCHANGED CROP INSURANCE UP 4% LABOR UP $.55 AN HOUR INTEREST DOWN .36% RENTS UP 7% ENERGY UNCHAGED FROM 2012 Total Cost Expected Yield bu/A Cost Per Bushel Corn After Corn Corn After Beans Beans After Corn $832 165 $5.04 $778 180 $4.32 $567 50 $11.34 Source: ISU Extension Economics, July 2012 33

34

Corn Projections 2013 2014 2015 2016 2017 Area Planted (mil. acres)

96.1 93.1 93.2 92.7 92.8 Yield (bu./acre) 163.2 165.7 167.9 170.2 172.4 Production (mil. bu.) 14,386 14,159 14,354 14,468 14,676 Beg. Stocks 645 1,510 1,675 1,766 1,789 Imports 25 Total Supply 15,056 15,695 16,054 16,259 16,490 Feed & Residual 4,852 4,855 4,964 5,022 5,082 Ethanol 5,386 5,649 5,665 5,643 5,657 Food, Seed, & Other 1,435 1,460 1,473 1,472 1,490 Exports 1,890 2,055 2,186 2,322 2,445 Total Use 13,546 14,020 14,288 14,470 14,675 Ending Stocks 1,815 Season-Average Price ($/bu.) 5.20 4.86 4.74 4.75 Source: FAPRI-MO

Production. (mil. bu.) 14, , , , ,676. Beg. Stocks ,510. 1,675. 1,766. 1,789. Imports. 25. Total Supply. 15, , , , ,490. Feed & Residual. 4,852. 4,855. 4,964. 5,022. 5,082. Ethanol. 5,386. 5,649. 5,665. 5,643. 5,657. Food, Seed, & Other. 1,435. 1,460. 1,473. 1,472. 1,490. Exports. 1,890. 2,055. 2,186. 2,322. 2,445. Total Use. 13, , , , ,675. Ending Stocks. 1,815. Season-Average Price. ($/bu.) Source: FAPRI-MO.")

35

Soybean Projections 2013 2014 2015 2016 2017 Area Planted (mil. acres)

77.0 76.0 76.4 77.1 77.4 Yield (bu./acre) 43.8 44.5 44.9 45.5 46.0 Production (mil. bu.) 3,326 3,333 3,385 3,459 3,510 Beg. Stocks 110 182 186 180 177 Imports 15 Total Supply 3,452 3,530 3,586 3,653 3,702 Crush 1,683 1,719 1,740 1,762 1,780 Seed & Residual 128 131 133 136 138 Exports 1,460 1,494 1,533 1,578 1,609 Total Use 3,270 3,344 3,406 3,476 3,526 Ending Stocks 176 Season-Average Price ($/bu.) 11.28 11.05 11.26 11.41 11.57 Source: FAPRI-MO

Production. (mil. bu.) 3,326. 3,333. 3,385. 3,459. 3,510. Beg. Stocks Imports. 15. Total Supply. 3,452. 3,530. 3,586. 3,653. 3,702. Crush. 1,683. 1,719. 1,740. 1,762. 1,780. Seed & Residual Exports. 1,460. 1,494. 1,533. 1,578. 1,609. Total Use. 3,270. 3,344. 3,406. 3,476. 3,526. Ending Stocks Season-Average Price. ($/bu.) Source: FAPRI-MO.")

36

Land Allocation Source: FAPRI-MO

37

U.S. Per-Capita Meat Consumption

Source: FAPRI-MO

38

U.S. Pork Projections Source: FAPRI-MO

39

U.S. Beef Projections Source: FAPRI-MO

40

Food Price Projections

Source: FAPRI-MO

41

Senate Proposal, $ per acre Source: FAPRI-MO

42

House Proposal, $ per acre Source: FAPRI-MO

43

Planted Acres, Million acres Source: FAPRI-MO

44

Prices, Source: FAPRI-MO

45

Gov. Expenditures, $ million Source: FAPRI-MO

46

Change in Expenditures, 2013-2017

Source: FAPRI-MO

47

Payments as a Share of Receipts

Source: FAPRI-MO

48

Source: Babcock, ISU

49

Iowa Corn Yields Source: USDA-NASS

50

Land Value & Cash Rental Rate Trends

Source: ISU Extension Economics 50

51

Positive Factors for Land Values

51

52

Negative Factors for Land Values

52

53

53

54

Grain Transportation Source: USDA-AMS

Open your book to page 84. On the screen you see our 2013 estimates. We’ll publish new estimates in January Note the historical costs of production on pages 97 and 98. Then on 99 you have a recent survey of current input costs. This changes over time. As crop values have gone up, the different input suppliers have responded. The level of fundamental driven change in input prices is worth discussing as well as the market driven changes. SEED UP 7% HERBICIDES UP 5% FOR NOW N PRICE IS NOW 60% NH3 AND 20% UAN AND UREA N DOWN; P DOWN P is for MAP and includes N value; K UNCHANGED CROP INSURANCE UP 4% LABOR UP $.55 AN HOUR INTEREST DOWN .36% RENTS UP 7% ENERGY UNCHAGED FROM 2012 Source: USDA-AMS 54

55

Grain Transportation Source: USDA-AMS

Open your book to page 84. On the screen you see our 2013 estimates. We’ll publish new estimates in January Note the historical costs of production on pages 97 and 98. Then on 99 you have a recent survey of current input costs. This changes over time. As crop values have gone up, the different input suppliers have responded. The level of fundamental driven change in input prices is worth discussing as well as the market driven changes. SEED UP 7% HERBICIDES UP 5% FOR NOW N PRICE IS NOW 60% NH3 AND 20% UAN AND UREA N DOWN; P DOWN P is for MAP and includes N value; K UNCHANGED CROP INSURANCE UP 4% LABOR UP $.55 AN HOUR INTEREST DOWN .36% RENTS UP 7% ENERGY UNCHAGED FROM 2012 Source: USDA-AMS 55

56

Lock Breakdowns Source: Steven Stockton

Open your book to page 84. On the screen you see our 2013 estimates. We’ll publish new estimates in January Note the historical costs of production on pages 97 and 98. Then on 99 you have a recent survey of current input costs. This changes over time. As crop values have gone up, the different input suppliers have responded. The level of fundamental driven change in input prices is worth discussing as well as the market driven changes. SEED UP 7% HERBICIDES UP 5% FOR NOW N PRICE IS NOW 60% NH3 AND 20% UAN AND UREA N DOWN; P DOWN P is for MAP and includes N value; K UNCHANGED CROP INSURANCE UP 4% LABOR UP $.55 AN HOUR INTEREST DOWN .36% RENTS UP 7% ENERGY UNCHAGED FROM 2012 Source: Steven Stockton 56

57

Thank you for your time. Any questions. My web site: http://www. econ

Thank you for your time! Any questions? My web site: Iowa Farm Outlook: Ag Decision Maker:

Similar presentations