Download presentation

Presentation is loading. Please wait.

1

Money and Banking Chapter 24

2

What is Money? Section 1

3

Functions of Money 1.Serves as a Medium, or form of exchange. -We can trade money for other goods and services.

4

Functions of Money 3.Serves as a measure of value -Used to assign value to a good or service.

5

Function of Money 2.Serves as a store of value -We can hold our wealth in the form of money until we are ready to use it.

6

Types of Money Coins= metallic forms of money such as pennies and nickels. Currency= Both coins and paper money.

7

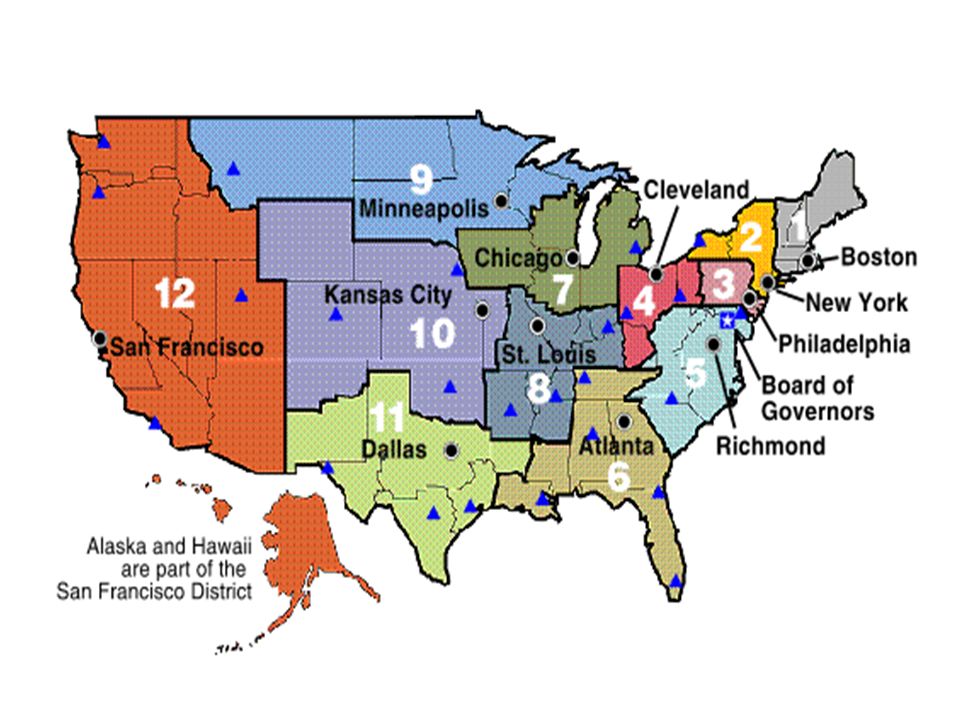

What Gives Money Value? Why do we value and accept money? –Because we are absolutely sure that someone else will accept its value as well. –A $10 only costs a few cents to make.

8

Financial Institutions Commercial Banks= are financial institutions that offer full banking services to individuals and businesses. –Most people have their checking and savings accounts in commercial banks.

9

Financial Institutions Saving and Loan Associations (S&L)= are financial institutions that traditionally loaned money to people buying homes. –Perform many of the activities that commercial banks do,

10

Financial Institutions Credit Unions= work on a non-for-profit basis. Open only to member of the group that sponsors them. Offer better rates on savings and loans

11

Safeguarding Our Financial System FDIC –This is a national corporation that insures individual accounts in financial institutions for up to $200,000. –Came after the Great Depression.

12

Consumer Confidence Consumers continue to deposit their money in banks and those deposits give the financial institutions the funds they need to make loans that help fuel economic growth.

13

The Federal Reserve System Section 2

14

Structure and Organization The Central Bank of the United States is the Federal Reserve System, known as the Fed. When banks need money, they borrow from the Fed.

15

Structure and Organization The U.S. is divided into 12 Federal Reserve districts. Each District has one main Federal Reserve Bank, along with branch banks. Thousands of banks are members of the Federal Reserve sysem.

17

Board of Governors The President appoints and the senate ratifies the seven members who make up the board of Governors. The President selects the chair of the Board.

18

Board of Governors Controls and coordinates the Fed’s activities The board acts independent from the President and Congress. So they are free from political pressure.

19

Advisory Councils 1.Reports on the general condition of the economy in each district. 2.Reports on financial institutions. 3.Reports on issues related to consumer loans.

20

Advisory Councils FOMC (Federal Open Market Committee)= Makes the decisions that affect the economy as a hole by manipulating the money supply. –FOMC has 12 members.

21

Functions of the Fed 1.Deals with banking regulation 2.Deals with Consumer Credit

22

The Fed as Regulator The Fed oversees and regulates large commercial banks. Regulates connections between American and foreign banking and oversees the international business of banks that operate in this country. Enforce laws that deal with consumer borrowing.

23

Acting as the Government’s Bank 1.It holds government money -Government revenues are deposited in the Fed. 2. The Fed sells U.S. government bonds and Treasury bills, which the government utilizes to borrow money.

24

Acting as the Government’s Bank 3. The Fed manages the nation’s currency, including paper money and coins. –When coins and currency become damaged, banks send them to the Fed for replacement.

25

How monetary Policy Works Monetary Policy= controlling of the supply of money and the cost of borrowing money. –The Fed can increase or decrease the supply of money.

26

Changing the Supply of Money The point where supply of money and demand for money meet sets the interest rate--the rate that people and businesses must pay to borrow money. The Fed can change the interest rate by changing the money supply.

27

Changing the Supply of Money If the Fed wants a lower interest rate, it must expand the money supply by moving the supply curve to the right. If the Fed wants to raise the interest rate, it has to reduce the money supply by shifting the supply curve to the left.

29

Monetary Policy Tools 1.Lower or raise the discount rate= the rate the Fed charges member banks for loans. -If the Fed wants to stimulate the economy, it lowers the discount rate. -Low discount rates encourage banks to borrow money from the Fed to make loans to their customers.

30

Monetary Policy Tools 2. The Fed may raise or lower the reserve requirement for member banks. Member banks must keep a certain % of their money in the Federal Reserve Bank as a reserve against their deposits. –If the Fed raises the reserve requirements, banks must leave more money with the Fed, and they have less to lend.

31

Monetary Policy Tools 3.The Fed can change the money supply through open market operations= purchase or sale of U.S. government bonds and Treasury bills. -Buying bonds from investors puts more cash in investors’ hands, increasing the money supply. -This shifts the supply curve or money to the right, which lowers interest rates. -Consumers and businesses then borrow more money, which increases consumer demand and business production.

32

Why is Monetary Policy Effective? It can be implemented quickly and Fed officials can easily fin tune its policy. If the Fed wants to encourage business investment, it can lower interest rates. –Raising rates will have the opposite effect.

33

How Banks Operate Section 3

34

Banking Services Banks are started by investors. Banks need to attract depositors to survive. To earn money, banks accept deposits to create different types of accounts and then use deposited funds to make loans.

35

Accepting Deposits Checking Accounts= allow customers to write checks or use check or debit cards. Use the funds deposited in the account to pay for expenses.

36

Accepting Deposits Savings Accounts –Banks pay interest to customers based on how much money they have deposited. Certificate of Deposit (CDs)

.")

37

Making Loans The main functions of banks is to lend money to businesses and customers. Loans can increase the supply of money –Suppose you deposit $1000 in a bank. The bank can use that money to lend to other customers. Those customers then deposit their loans in the bank.

38

The National Banking Act In 1863, Congress passed the National Banking Act Federally chartered private banknotes, or national currency, which were uniform in appearance and backed by the U.S. government bonds.

39

The Federal Reserve The Panic of 1907 resulted in the passage of the Federal Reserve Act of 1913.

40

The Great Depression When FDR became president he closed all banks. Banks could only reopen after in proved it was financially sound. Congress established the FDIC.

41

The Savings and Loan Crisis S&Ls were allowed to make higher-risk loans and investments. When these investments went bad, several S&Ls failed. As a result the FDIC intervened and took over regulation of the S&L industry.

42

The Gramm-Leach Bliley Act Passed in 1999 permits bank holding companies greater freedom to engage in a full range of financial services, including banking, insurance, and securities. Banks must also protect their customers’ personal financial information.

Similar presentations