Download presentation

Presentation is loading. Please wait.

1

Monetary Policy Summary of 2007 and Looking Ahead to 2008 January 2008

2

Inflation in Israel and around the world

3

Inflation in the last 12 months and the inflation targets, 1997−2007

4

Percent The Bank of Israel interest rate, actual inflation,* and inflation expectations,** 2004-08 ** For next 12 months. SOURCE: Bank of Israel Monetary Department. * In previous 12 months.

5

Inflation in previous 12 months (to November 2007) in Israel and selected emerging markets and advanced economies Emerging marketsAdvanced economies Percent

in Israel and selected emerging markets and advanced economies Emerging marketsAdvanced economies Percent")

6

The CPI, the Energy Price Index, and the Basic Foods Price Index * (rate of change in previous 12 months, to November 2007) Percent Energy Price Index Index of Basic Food Prices CPI * Basic foods—Bread, cereals and baked goods, fats and margarine.

Percent Energy Price Index Index of Basic Food Prices CPI * Basic foods—Bread, cereals and baked goods, fats and margarine.")

7

The CPI, and the index excluding energy and basic food prices (rate of change over previous 12 months, to November 2007) Percent CPI excluding energy and basic food prices CPI * Basic foods—Bread, cereals and baked goods (?), fats and margarine..

Percent CPI excluding energy and basic food prices CPI * Basic foods—Bread, cereals and baked goods ( ), fats and margarine..")

8

Inflation expectations based on the market and forecasters predictions

9

Inflation in 12 previous months, inflation targets, and one-year inflation expectations based on the market, 1997─2007 Inflation expectations CPI Limit of inflation target

10

Long-term inflation expectations (average of ten to twelve years forward, January 2003 to December 2007)

")

11

Inflation expectations for the next 12 months based on the capital market and forecasters’ predictions SOURCE: Bank of Israel Monetary Department. Percent

12

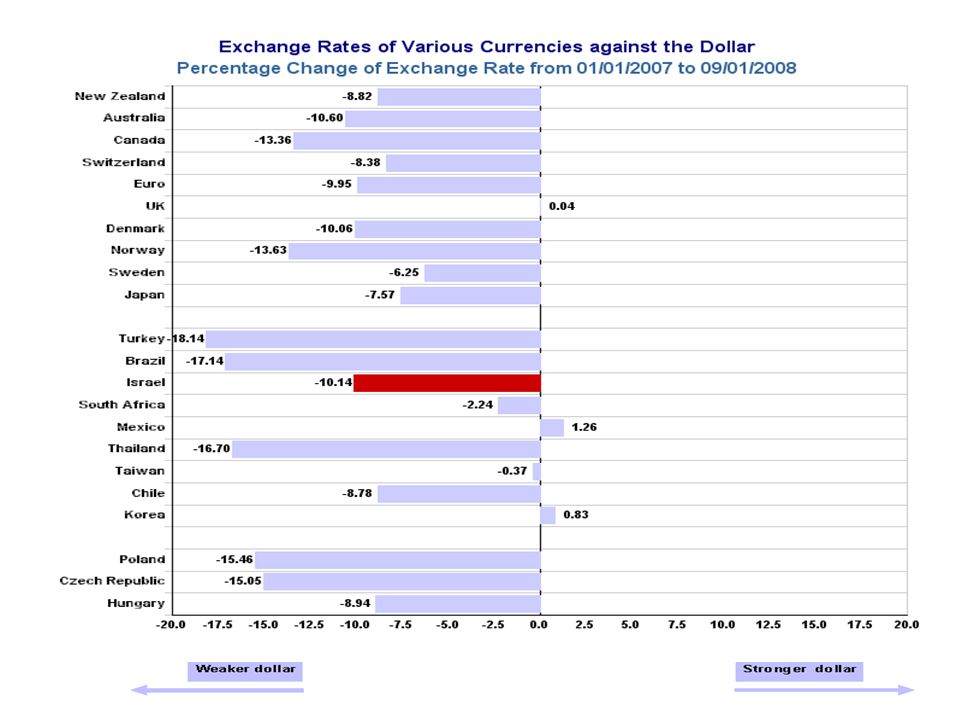

The Exchange Rate

13

The exchange rate 1 January 2001 to 8 January 2008

15

The real exchange rate vis-à-vis Israel’s trading partners (January 1997─December 2007*) SOURCE: IFS data. August−December 2007 figures calculated by Bank of Israel. Percent 124.8 A rise in the index indicates depreciation. The figure for December 2007 is calculated from spot exchange rates known for the half-month, our forecast CPI from the monthly model, and an extrapolation of inflation in the countries whose currencies are in the currency basket.

16

The current account of the balance of payments (percent of GDP in annual terms, 1995─2007*) SOURCE: Balance of payments, Central Bureau of Statistics. Percent of GDP * Estimate

17

Percent of GDP 8,092 14,302 4,792 4,1386,871 2,0413,822 1,812 1,767 723 3,626 75 5,062 5,058 8,956 14,399 8,244 2,9304,544 2,381 2,065 3,154 2,708 982 1,623 688 2,149 3,336 9,700 450 6,100 5,900 * Forecast by the Bank of Israel Foreign Exchange Activity Department. Nonresidents’ investments in Israel (percent of GDP, 2000─07*) Israelis’ investments abroad (percent of GDP, 2000─07*) SOURCE: Balance of payments, Central Bureau and Statistics.

Israelis’ investments abroad (percent of GDP, 2000─07*) SOURCE: Balance of payments, Central Bureau and Statistics..")

18

The CPI, the housing index, and the NIS/$ exchange rate (rate of change in previous 12 months)

")

19

Looking ahead

20

Inflation forecasts for 2008 (at end of 2007) Forecasters—2.7 percent (2.0─3.7 percent) Capital market—1.6 percent BoI Companies Survey—2.7 percent (74 percent of respondents believe that we will meet the inflation target) The Bank of Israel models According to both models, at the current level of the exchange rate the current interest rate environment is consistent with inflation of 2 percent at the end of 2008

Forecasters—2.7 percent (2.0─3.7 percent) Capital market—1.6 percent BoI Companies Survey—2.7 percent (74 percent of respondents believe that we will meet the inflation target) The Bank of Israel models According to both models, at the current level of the exchange rate the current interest rate environment is consistent with inflation of 2 percent at the end of 2008")

21

Percent *The fan covers 66 percent of the distribution of expected inflation. SOURCE: Bank of Israel Monetary Department. Actual inflation and fan chart of expected inflation, 2006─2009 (Rate of cumulative price increases in previous 4 quarters) 38% 32% 30%

38% 32% 30%.")

22

Thank you

Similar presentations

(a) Data are non seasonally adjusted.>")

LOP Conditions for LOP to hold 2. Purchasing Power Parity (PPP)>")

(a) Contributions to annual CPI inflation. Data are non.>")

Sources: ONS and.>")

Sources: Bank of England, Bloomberg.>")