Download presentation

Presentation is loading. Please wait.

1

Monetary Policy and Financial Stability Policies in Israel Presented at Economic Dialogue Meeting by Dr. Edward Offenbacher by Dr. Edward Offenbacher Director, Monetary/Finance Division, Research Dept. Bank Of Israel January 2012

2

Outline of Presentation Key Macroeconomic Developments Issues for Monetary Policy Issues for Financial Stability

3

Key Macroeconomic Developments Slowdown of real growth after seven “ good years ” of export-led growth Slowdown of real growth after seven “ good years ” of export-led growth Slowdown of real growth after seven “ good years ” of export-led growth Low unemployment but moderate wage increase. Low unemployment but moderate wage increase Low unemployment but moderate wage increase BoP – CA deficit due mainly to ToT “ hit ”. BoP – CA deficit due mainly to ToT “ hit ”. BoP – CA deficit due mainly to ToT “ hit ”. Inflation moderating after target misses. Inflation moderating after target misses Inflation moderating after target misses House price inflation. House price inflation House price inflation Fiscal policy: Expenditures within target path despite pressures from defense, social justice; tax receipts slowing due to growth slowdown so deficit missing target. Fiscal policy: Expenditures within target path despite pressures from defense, social justice; tax receipts slowing due to growth slowdown so deficit missing target Fiscal policy: Expenditures within target path despite pressures from defense, social justice; tax receipts slowing due to growth slowdown so deficit missing target Monetary policy: Tension between domestic vs. foreign pressures. Monetary policy: Tension between domestic vs. foreign pressures. Monetary policy: Tension between domestic vs. foreign pressures.

4

Issues for Monetary Policy Growth slowdown w/ economy near full employment: weak demand side or supply constraints? Where is relevant potential output? Slowing inflation: one-time effects or indicator of recession ahead? Why is wage growth subdued? Interest rate differentials: Potential for capital inflow, local currency appreciation (on hold recently). Complaints of “ credit crunch ” – how legitimate?

. Complaints of credit crunch – how legitimate .")

5

Financial Stability Policy Issues (1) Financial stability policy (aka Macroprudential Policy): Do we know what it is? Do we have relevant information and analysis – in the profession, in Israel? Contagion/network effects; credibility/confidence. Key measues taken in Israel: (a) Capital surcharge on high LTV mortgages; (b) Limits on variable rate mortgages; (c) Reporting/reserve requirements on foreign activity in Makam and derivatives; (d) Elimination of tax exemption for foreigners on Makam interest. Key new measure: adoption of Basel III Tier 1 capital adequacy requirements for banks.

Capital surcharge on high LTV mortgages; (b) Limits on variable rate mortgages; (c) Reporting/reserve requirements on foreign activity in Makam and derivatives; (d) Elimination of tax exemption for foreigners on Makam interest. Key new measure: adoption of Basel III Tier 1 capital adequacy requirements for banks..")

6

Financial Stability Issues (2) “ Imported ” issues European crisis – direct (financial) and indirect (trade) exposures Geopolitical: Arab spring, Iran U.S.: Looking better for now, but … “ Home-made ” issues Highly leveraged conglomerates House price inflation Construction industry loans

Imported issues European crisis – direct (financial) and indirect (trade) exposures Geopolitical: Arab spring, Iran U.S.: Looking better for now, but … Home-made issues Highly leveraged conglomerates House price inflation Construction industry loans")

7

Thanks

8

8 GDP Growth Rates in Israel and in the Advanced Economies (2000-2011) % -The Quarterly data show the seasonally adjusted rate of change from the previous quarter at an annualized rate. -The growth rate for the advanced OECD economies (excluding Luxembourg and Iceland) is a simple average of their individual growth rates. SOURCE: OECD Data and the Bank of Israel

is a simple average of their individual growth rates. SOURCE: OECD Data and the Bank of Israel.")

9

9 % Israel’s Annual GDP Growth Rates (2000 – 2012F) Bank of Israel forecasts for 2012

Bank of Israel forecasts for 2012")

10

10 Goods imports and exports* (2000–2011) * Monthly figures, $ million, at current prices. Imports and exports excluding airplanes, ships and diamonds. SOURCE: Bank of Israel. Goods Exports Goods Imports $ millions

11

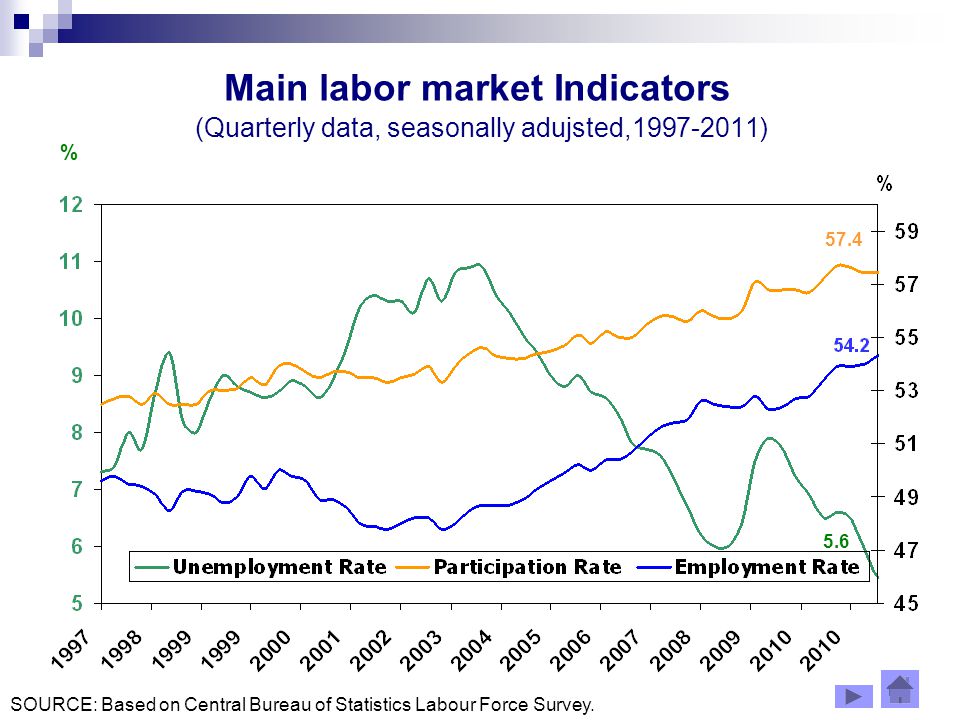

11 Main labor market Indicators (Quarterly data, seasonally adujsted,1997-2011) % SOURCE: Based on Central Bureau of Statistics Labour Force Survey. 57.4 5.6

12

12 Real Wage per Employee Post* (1999-2011) *Seasonally adjusted, 3 months moving average. 2004 prices. SOURCE: Based on Central Bureau of Statistics Data.

13

13 Current Account of Balance of Payments (Percentage of GDP, 1995-2011) SOURCE: Balance of Payments, Central Bureau of Statistics. %

14

14 % * Budget Deficit* (Percent of GDP, 2000-2012**) *Percent of GDP; excluding credit extended. The data refers to the deficit excluding the Bank of Israel’s profits. **2011 and 2012 Budget deficit is based on the current budget and BOI forecast.

16

16 % Gross Public Debt ( 2000-2012F) Gross Public Debt (Percent of GDP, 2000-2012F) *Bank of Israel forecast

Gross Public Debt (Percent of GDP, F) *Bank of Israel forecast")

17

17 The Tax Burden in Israel and in the OECD Countries (Percent of GDP, 2010) Including income tax, social security tax, fees, levies and fines, Including consumption taxes, levies on specific goods & services and valued added taxes. SOURCE: OECD data %

18

18 % Inflation expectations The Bank of Israel Interest Rate, Actual Inflation,* and Inflation Expectations** (2004–12) * In the previous twelve months. ** Twelve months forward, calculated form the capital market. SOURCE: Bank of Israel.

19

19 Inflation Over Past 12 Months, Inflation Targets and Inflation Expectations from the Capital Market and Inflation Expectations from the Capital Market(1997-2011) Inflation expectations Consumer price index SOURCE: Research Department, Bank of Israel %

Inflation expectations Consumer price index SOURCE: Research Department, Bank of Israel %")

20

20 10 Year Break-Even Inflation Expectations* (2001-2012) 10 years average Inflation Expectation. SOURCE: Research Department, Bank of Israel

21

21 The Nominal and the Real Exchange Rates (1997-2012) Shekel / Dollar Exchange Rate The Real Exchange Rate by Trading Partners (100=01/1997) 111.8 NIS Ø The NIS/$ chart is on a daily basis, while the real exchange rate chart is on a monthly basis. A rise in the index indicates depreciation. The figure for the last month is calculated from spot exchange rates known for the half-month, our forecast CPI from the monthly model, and an extrapolation of inflation in the countries whose currencies are in the currency basket. SOURCE: IFS and Bank of Israel Index 3.8

22

22 The EMBI+ tracks total return for traded external debt instruments in the emerging markets. The EMBI + expands upon the original EMBI index which covered only Brady Bonds. SOURCE: Bank of Israel 10 Year Israel-US Gov. Bond Spread and EMBI+ Index (Basis points 2006-2012,) EMBI + Israel-USA Government Bonds 10 Years Spread

EMBI + Israel-USA Government Bonds 10 Years Spread.")

23

23 The Stock Markets: Israel, NASDAQ and the Emerging Markets (1/6/2006=100) Emerging Markets Israel (Tel Aviv 100) NASDAQ SOURCE: Bloomberg Index

Emerging Markets Israel (Tel Aviv 100) NASDAQ SOURCE: Bloomberg Index")

24

Credit Balances Outstanding (2006-2011, NIS Billion)

")

25

Credit from the Banking Sector (2006-2011, NIS Billion)

")

26

Credit to the Business Sector (2006-2011, NIS Billion)

")

Similar presentations

sector, collective farm market and cooperative trade Consumer goods market Black market.>")