Download presentation

Presentation is loading. Please wait.

1

Liquefied Natural Gas: Global Overview

Alan Townsend World Bank Myanmar, October 2015

2

Source: GIIGNL

3

This infographic shows new LNG export and import capacity due online in 2015 and The size of the circle reflects the total volume from each country. Export capacity is colored green, import capacity is red, in million tons per annum. Source: ICIS

4

LNG Trade East of Suez dominates

Major changes are coming this year, with the first Lower 48 US gas exports Two other major, new sources of LNG may emerge by 2025: Canada and Mozambique Source of Map: GIIGNL

5

Flat global demand, but dynamic shifts within it

Asian buyers becoming more price sensitive Demand growth in China and India has been lower than generally expected New buyers continue to appear (2014: Lithuania, Singapore) Source: GIIGNL

Source: GIIGNL.")

6

“Flexible” LNG has become a major part of the market

Overall market is bigger, with growing liquidity Export projects has generally had good technical performance and have been debottlenecked, so can produce more than their contractual obligations Investors and financiers have become comfortable with projects that are not fully sold out on a long term basis In recent years, demand has evolved with price sensitivity becoming a factor in influencing demand at the margin With more offtake commitments coming from marketers, the true size of the flexible market may already be larger than shown Source: GIIGNL

7

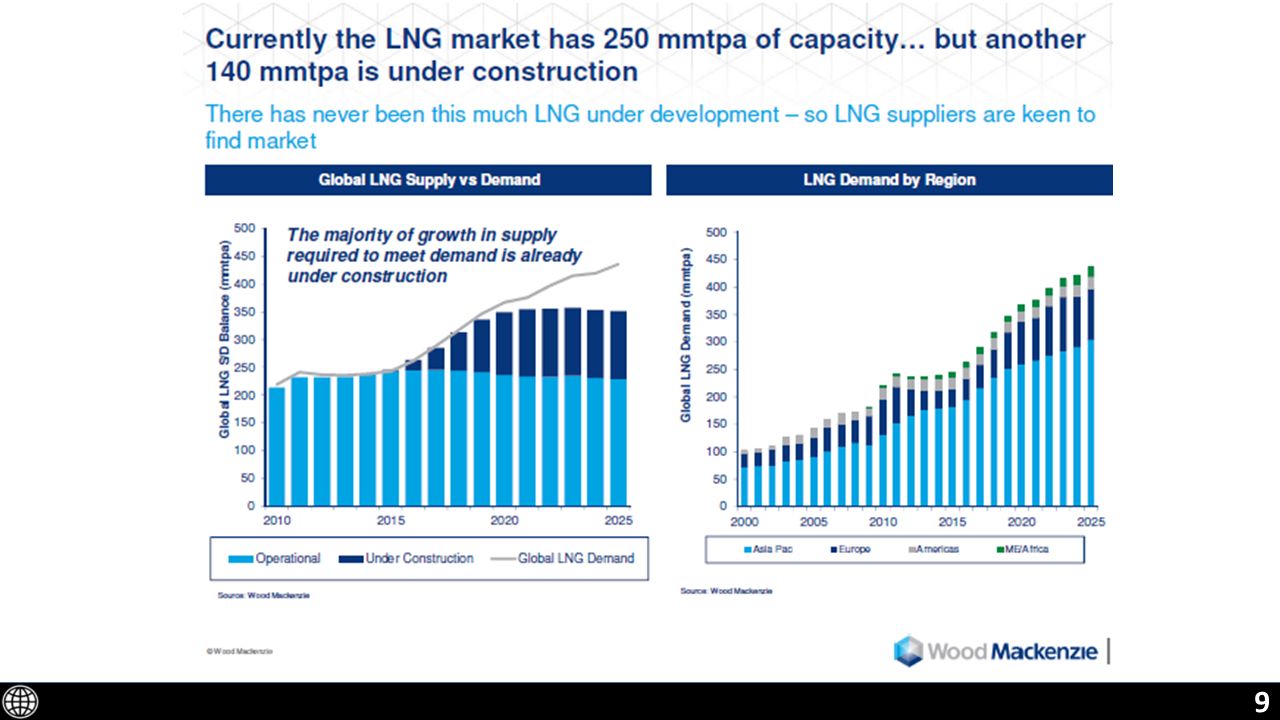

LNG production capacity growth will outpace demand growth for the next few years

8

New supply coming on strong . . .

10

Supply at risk Ambitious proposals from large resource basins are at risk in a low oil price environment because of high costs © 2015 IHS Source: IHS Energy Note: Units are MMtons.

12

Gas prices 1997-2014 ($/mmBtu) [BP Statistical Review of World Energy 2015]

![Gas prices ($/mmBtu) [BP Statistical Review of World Energy 2015]](http://slideplayer.com/slide/8960722/27/images/12/Gas+prices+%28%24%2FmmBtu%29+%5BBP+Statistical+Review+of+World+Energy+2015%5D.jpg "Gas prices ($/mmBtu) [BP Statistical Review of World Energy 2015]")

13

2014-2015 prices: seismic shifts

Up to 50% declines in NE Asia Europe – prices down by at least a third Transportation differentials are too low to easily justify trade from the Atlantic basin to the Pacific (including re-exports) In 2015, Egypt, Pakistan, and Jordan have emerged to take some of these volumes

In 2015, Egypt, Pakistan, and Jordan have emerged to take some of these volumes.")

14

The downtrend continues . . .

15

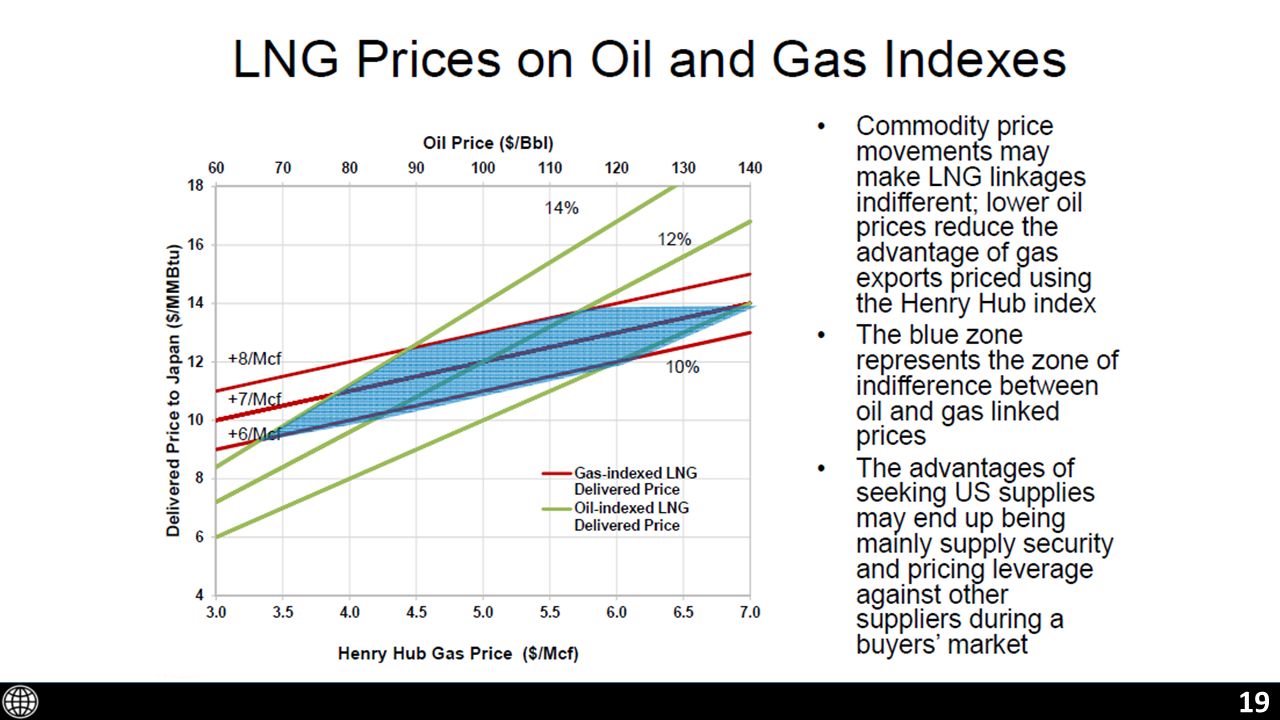

But where will prices go?

The FGE view (at left) is not untypical and reflects an industry consensus about: Cost of production of crude oil (from $50-$60 per barrel to $80- $90) Cost of production of US natural gas, which is assumed to be the marginal supply to world markets Source: FACTS Global Energy

is not untypical and reflects an industry consensus about: Cost of production of crude oil (from $50-$60 per barrel to $80- $90) Cost of production of US natural gas, which is assumed to be the marginal supply to world markets. Source: FACTS Global Energy.")

16

US Natural Gas Exports – permanent feature of global trade?

Charts show results from the Rice World Gas Trade Model (RWGTM) from model runs in 2014 – before the collapse in prices Analysis suggests that, even with some periods of short-term imbalances, there is enough supply and demand response such that in the long run the differential between the US and East Asia is just enough to allow for exports The implication is more globally integrated natural gas markets

from model runs in 2014 – before the collapse in prices. Analysis suggests that, even with some periods of short-term imbalances, there is enough supply and demand response such that in the long run the differential between the US and East Asia is just enough to allow for exports. The implication is more globally integrated natural gas markets.")

18

How is LNG priced? Traditional DES* pricing in Asia: P = A(x) + B

Price = JCC times a percentage + a constant Example: ($60/barrel x 15%) + $1 = $10/mmBtu Some common formulas are shown at right (indicative values shown) Spot cargos might be purchased on a fixed price basis, with no formula US export tolling contracts focus only on the liquefaction fee – the purchase of natural gas, its delivery to the LNG plant, and the transport of LNG are the assumed by the buyer of the tolling service NBP is also often used as an index especially for deals in the Atlantic basin Singapore has launched an LNG spot price index; Tokyo and Shanghai next? Cheniere model for pricing US exports, FOB Price = Henry Hub times 115% plus a liquefaction fee Example: ($3/mmBtu x 115%) + $3 = $6.45/mmBtu FOB, so add $3 for transport to Asia = $9.45/mmBtu Kansai purchase from BP, DES Price = Henry Hub times 115% plus a constant Example: ($3/mmBtu x 115%) + $7 = $10.45/mmBtu Seller provides liquefaction and transport *delivered ex-ship

+ $1 = $10/mmBtu. Some common formulas are shown at right (indicative values shown) Spot cargos might be purchased on a fixed price basis, with no formula. US export tolling contracts focus only on the liquefaction fee – the purchase of natural gas, its delivery to the LNG plant, and the transport of LNG are the assumed by the buyer of the tolling service. NBP is also often used as an index especially for deals in the Atlantic basin. Singapore has launched an LNG spot price index; Tokyo and Shanghai next Cheniere model for pricing US exports, FOB. Price = Henry Hub times 115% plus a liquefaction fee. Example: ($3/mmBtu x 115%) + $3 = $6.45/mmBtu. FOB, so add $3 for transport to Asia = $9.45/mmBtu. Kansai purchase from BP, DES. Price = Henry Hub times 115% plus a constant. Example: ($3/mmBtu x 115%) + $7 = $10.45/mmBtu. Seller provides liquefaction and transport. *delivered ex-ship.")

21

LNG Shipping: big increases in vessel numbers, shipping capacity

22

LNG shipping glut Short-term charter rates have fallen far below vessel replacement costs From Fearnleys, October 22, 2015: Spot $32,000 per day 1 yr T/C $35,000 per day

23

Shipping is tighter in the medium term than one might think

Shipping is tighter in the medium term than one might think Unless trades are optimized Is Kansai-Engie deal a model for future optimization of supply portfolios and shipping?

24

Who trades LNG (selected examples)

Portfolio Marketers Who trades LNG (selected examples) Traders Production Companies

Traders. Production Companies.")

25

Key Trends Who buys LNG 80 million tons in 2014 (1/3) The rest (2/3)

Smaller share of LNG on LTC For large buyers, new LTC’s will favor new projects Desire for more gas-on-gas pricing but oil-linked pricing will not disappear; new gas hubs support Portfolio approach not limited to sources but to contract tenors, indexation terms Long Term Contracts 80 million tons in 2014 (1/3) (Tepco/Chubu jv JERA formed in 2015) New Supply Desirable Gas- On-gas Pricing Other power and gas utilities, national oil companies, traders, power generators, and portfolio marketers Real portfolios for big buyers The rest (2/3)

(Tepco/Chubu jv JERA formed in 2015) New. Supply. Desirable. Gas- On-gas. Pricing. Other power and gas utilities, national oil companies, traders, power generators, and portfolio marketers. Real. portfolios. for big. buyers. The rest (2/3)")

27

Small and mid-scale LNG shipping Vibrancy but challenging economics

Multi-carriers have emerged – when will they start trading LNG? A boom in the Baltic New ships for coastal China trade New designs for bunkering, small-scale trade New, lower cost containment approaches

28

LNG Shipping Economics

Strong economies of scale Moving small cargos long distances will be expensive Hub-and-spoke models will work when there is a logical hub Panama could be a logical hub Bunkering market gives Panama a key comparative advantage versus other players in Central America

Similar presentations