Download presentation

Presentation is loading. Please wait.

1

MONEY What is Money? Distinguishing Functions of Money: (Static Functions) Medium of exchange Unit of account A standard of deferred payments A store of Value To influence the economy by the dynamic function of money

Medium of exchange Unit of account A standard of deferred payments A store of Value To influence the economy by the dynamic function of money.")

2

What is Money? Money is one of the greatest inventions of mankind. According to Walker, "Money is what Money does.” In a wider sense, Money includes all mediums of exchanges like Gold, Silver, Copper, Paper, Cheques, and Bills of exchange, etc. Money is a good that acts as a medium of exchange in transactions. Classically it is said that money acts as a unit of account, a store of value, and a medium of exchange.

3

According to Crowther, "Anything that is generally acceptable as a means of exchange and which at the same time acts as a measure and store of value."

4

Medium of Exchange Facilitates efficient economic transactions Advantage over Barter Economy: –Double Coincidence of Wants Not Necessary –Promotes Specialization & Division of Labor

5

Unit of Account –Measure of Value in the Economy –Common Yardstick to Value Different Goods and Services

6

Store of Value –Enables agents to shift consumption across time, i.e., save now, consume later. –Other financial & Non-financial assets may also have this property. Money is distinguished by its Liquidity. –Money is unattractive as a store of value in an inflationary environment.

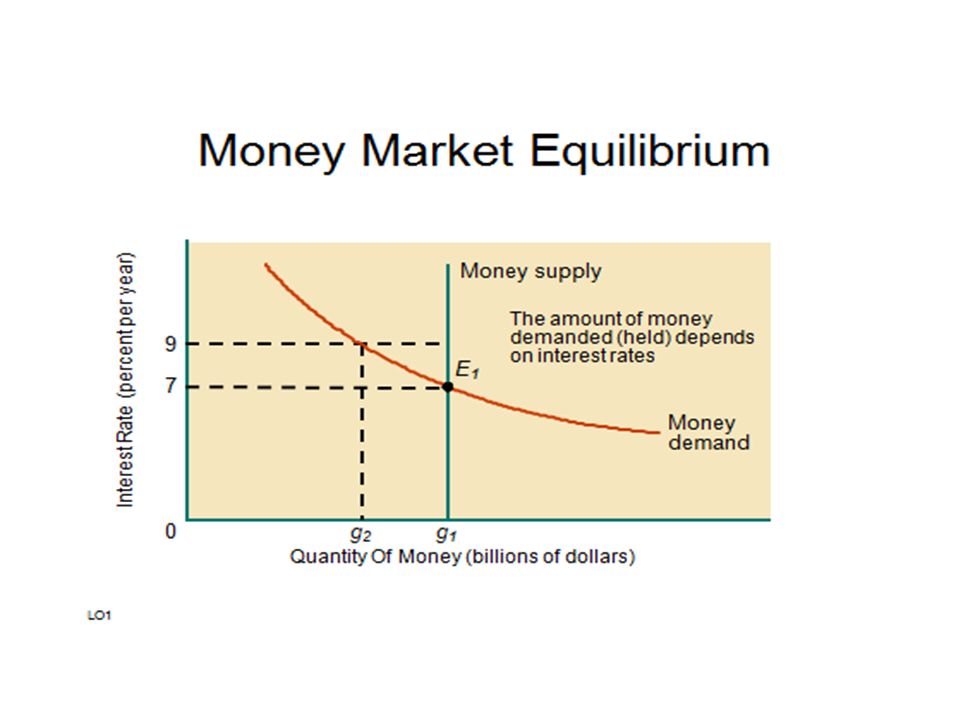

7

Money Market Equilibrium Where: The demand for money = the supply of money

8

The Demand for Money Quantity Theory of Money or Equation of Exchange Cambridge Approach Liquidity Preference Theory

9

Quantity Theory of Money classical economists –Irving Fisher relates quantity of money to nominal income

10

Equation of Exchange MV = PY where –M = quantity of money –P = price level –Y = real output = real income –V = velocity = # times money used to purchase output

11

Assumptions V is constant in short-run –depends on institutions, technology that change slowly Y is at full employment level –also constant in short-run

12

MV = PY if V, Y constant then A change in M must cause an equal % change in P –Quantity Theory of Money

13

Cambridge Approach MV = PY M = (1/V)PY M = kPY let (1/V) = k Md = M in equilibrium –Md = kPY –Md is depends on income NOT interest rates

PY M = kPY let (1/V) = k Md = M in equilibrium –Md = kPY –Md is depends on income NOT interest rates")

14

Liquidity Preference Theory Keynes 1936 Although holding money provides little or no interest, there are reasons for doing so: 3 motives to holding money –transactions motive, Transactions demand. –precautionary motive, Precautionary demand –speculative motive, Speculative demand

15

The Demand for Money Transactions demand for money – Money held for the purpose of making everyday market purchases. Precautionary demand for money – Money held for unexpected market transactions or for emergencies.

16

The Demand for Money Speculative demand for money – Money held for speculative purposes, for later financial opportunities.

17

Why Hold Money John Maynard Keynes noted that people had three reasons for holding money –People hold money to make transactions –People hold money for precautionary reasons –People hold money to speculate

18

Why Hold money Economists have since identified major factors that influence the three Keynesian motives for holding money: –T–The price level –I–Income –T–The interest rate –C–Credit availability –W–Wealth of the country –E–Expectations as to future income receipts –T–The nature and variety of substitute assets –T–The system of payments in the community.

19

The Keynesian Motives for Holding Money The transaction motive –Individuals have day-to-day purchases for which they pay in cash or by check –Individuals take care of their rent or mortgage payment, car payment, monthly bills and major purchases by check –Businesses need substantial checking accounts to pay their bills and meet their payrolls.

20

The Keynesian Motives for Holding Money The precautionary motive –People will keep money on hand just in case some unforeseen emergency arises They do not actually expect to spend this money, but they want to be ready if the need arises

21

The Keynesian Motives for Holding Money The speculative motive –When interest rates are very low you don’t stand to lose much holding your assets in the form of money –Alternatively, by tying up your assets in the form of bonds, you actually stand to lose money should interest rates rise You would be locked into very low rates –This motive is based on the belief that better opportunities for investment will come along and that, in particular, interest rates will rise

22

The Demand Schedule for Money The Three Demands for Money

23

Total Demand for Money This is the sum of the transaction demand, precautionary demand, and speculative demand for money shown in the previous slide

24

Money Supply In economics, the money supply or money stock, is the total amount of money available in an economy at a particular point in time. While talking about equilibrium of money market supply of money is exogenous.

26

Nominal and Real Rate of Interest Definition of 'Real Interest Rate' An interest rate that has been adjusted to remove the effects of inflation to reflect the real cost of funds to the borrower, and the real yield to the lender. The real interest rate of an investment is calculated as the amount by which the nominal interest rate is higher than the inflation rate. Real Interest Rate = Nominal Interest Rate - Inflation (Expected or Actual)

.")

27

EXAMPLE For example, if you are earning 4% interest per year on the savings in your bank account, and inflation is currently 3% per year, then the real interest rate you are receiving is 1% (4% - 3% = 1%). The real value of your savings will only increase by 1% per year, when purchasing power is taken into consideration.

28

Nominal versus Real Interest Rate The real interest rate is the nominal rate of interest minus inflation. In the case of a loan, it is this real interest that the lender receives as income. If the lender is receiving 8 percent from a loan and inflation is 8 percent, then the real rate of interest is zero because nominal interest and inflation are equal. A lender would have no net benefit from such a loan because inflation fully diminishes the value of the loan's profit. The relationship between real and nominal interest rates can be described as:

29

Nominal versus Real Interest Rate real interest rate = nominal interest rate - expected inflation In this analysis, the nominal rate is the stated rate, and the real interest rate is the interest after the expected losses due to inflation. Since the future inflation rate can only be estimated, the ex ante and ex post (before and after the fact) real interest rates may be different; the premium paid to actual inflation may be higher or lower. In contrast, the nominal interest rate is known in advance.

real interest rates may be different; the premium paid to actual inflation may be higher or lower. In contrast, the nominal interest rate is known in advance..")

30

Calculation of Real Interest Rate The real interest rate solved from the Fisher Equation is: 1+Interest /1+Inflation -1= Real If there is a negative real interest rate, it means that the inflation rate is greater than the nominal interest rate. If the rate of interest is 2% and the inflation rate is 10%, then the borrower would gain 7.27% of every dollar borrowed per year.

31

Liquidity Trap The liquidity trap is the portion of the money-demand curve that is horizontal. People are willing to hold unlimited amounts of money at some (low) interest rate.

interest rate..")

32

Constraints on Monetary Stimulus A liquidity trap can stop interest rates from falling The liquidity trap Interest Rate E1E1 E2E2 g1g1 g2g2 Quantity Of Money Demand for money

33

Factors Influencing Demand for Money The price level –As the price level rises, people need to hold higher money balances to carry out day-to-day transactions –As the price level rises, the purchasing power of the dollar declines, so the longer you hold money, the less that money is worth –Even though people tend to cut down on their money balances during periods of inflation, as the price level rises people will hold larger money balances

34

Factors Influencing Demand for Money Income –The more you make, the more you spend –The more you spend, the more money you need to hold as cash or in your checking account –Therefore as income rises, so does the demand for money balances.

35

Factors Influencing Demand for Money Interest rates –The quantity of money demanded (held) goes down as interest rates rise The alternative to holding your assets in the form of money is to hold them in some type of interest bearing paper As interest rates rise, these assets become more attractive than money balances.

goes down as interest rates rise The alternative to holding your assets in the form of money is to hold them in some type of interest bearing paper As interest rates rise, these assets become more attractive than money balances.")

36

Factors Influencing Demand for Money Credit availability –If you can get credit, you don’t need to hold so much money The last three decades have seen a veritable explosion in consumer credit in the form of credit cards and bank loans Over this period, increasing credit availability has been exerting a downward pressure on the demand for money

37

Other Factors Influencing Demand for Money Nature and variety of substitute assets: the demand for money is likely to be high if the only other assets available for holding are highly illiquid and risky. However, demand for money is reduced as more liquid and safer substitutes become available. The payment system of the community: if the production processes are combined within vertically integrated firms with no money payments among the departments of each firms, the demand for money is likely to be smaller.

38

Four generalizations –As interest rates rise, people tend to hold less money –As the rate of inflation rises, people tend to hold more money –As the level of income rises, people tend to hold more money –As credit availability increases, people tend to hold less money

Similar presentations