Download presentation

Presentation is loading. Please wait.

1

Term 2: Lecture 1 Topic 1: Global Impact of the 2008 Financial Crisis: Comparing Canada and the Third World Countries

2

Onaran (2010) argues: Neoliberalism is an initial attempt to deal with the 1970s stagflation crisis After leaving the policies based on the “Keynesian consensus” and turning away from the capitalism’s “golden age” (higher spending on social welfare, strengthening the unions, cooperation between labour and management) neoliberalist policies were introduced. Profits increased but a greater risk of crisis arose as a result : investment and wages declined To control the crisis, US boosted the economy with quick financialization- this stimulated debt-credit and other yields of wealth

3

Capitalism is facing a major realization crisis: An inability to sell the output produced, i.e., to realize, in the form of profits, the surplus value extracted from workers’ labor. Why did unemployment grew and labour’s purchasing power decline? Economic growth rates have been low and well below the mark leading to unemployment Labour’s purchasing power declined as a result of unemployment and lower wages – decline in consumers for goods produced – capitalists as profit-makers do not spend as much as workers who earn wages (“a dollar transferred from a worker to a capitalist reduces total consumption spending”).

..")

4

The result was Capitalists played the financial markets for high- profits through financial speculation This led to unmanageable debt leading to capitalist crisis: The Financial crisis of 2008

5

Immanuel Wallerstein (2011) argues: Capitalist system requires endless accumulation of capital Appropriation of surplus value Monopoly of global production with global linkages Support of various states

argues: Capitalist system requires endless accumulation of capital Appropriation of surplus value Monopoly of global production with global linkages Support of various states")

6

1.AICs rules that shaped global neoliberalism (slides 6-15 for self-review)

")

7

WTO: AICs commercial interests are embodied in the rules global trade, aid and loan imposed on the LDCs : WTO works on power-based bargaining Neoliberal policies Washington consensus SAP Conditionality MFN

8

How does Structural Adjustment Program (SAP) affect the Developing countries? Impact: Balancing the government budget Weakening the Labour Deregulating the economy Reducing the State BLeeDS In the past, IMF’s imposition of SAP on South Asian countries (e.g., S.Korea, Indonesia, Thailand) created a financial crisis of economic contraction and depression.

created a financial crisis of economic contraction and depression..")

9

Continued from Lec 4: WTO: AICs commercial interests are embodied in the rules global trade, aid and loan imposed on the LDCs: WTO works on power-based bargaining Neoliberal policies Washington consensus SAP Conditionality MFN

10

What are the Neoliberal policies? DOPE LD Liberalize trade Deregulate finance/currency Open up for foreign investment, Privatize economy Deregulate commercial activity Ensure property protection

11

http://www.youtube.com/watch?v=XIUWZnnHz2g&feature=related neolib as a water balloon 12 min

12

WTO: AICs commercial interests are embodied in the rules global trade, aid and loan imposed on the LDCs : WTO works on power-based bargaining Neoliberal policies Washington consensus SAP Conditionality MFN

13

WASHINGTON CONSENSUS (1989) LiberalizationLiberalization AusterityAusterity PrivatizationPrivatization De-regulationDe-regulation og LAPDog

LiberalizationLiberalization AusterityAusterity PrivatizationPrivatization De-regulationDe-regulation og LAPDog")

14

WTO: AICs commercial interests are embodied in the rules global trade, aid and loan imposed on the LDCs : WTO works on power-based bargaining Neoliberal policies Washington consensus SAP Conditionality MFN

15

Conditionality: Conditions placed on loans to LDCs Conditions imposed to make aid effective in a recipient country – in reality could hurt the country’s economy or the country’s political stability

16

Global Capitalism, Financial Crisis & Developing Countries 1.Origins of the Crisis: USA 2.Impact of the Crisis: Global Source: Valpy FitzGerald http://hdr.undp.org/en/media/FitzGerald_Global_Financial_Crisis_edit.ppt

17

1.What caused the US/EU financial system to fail in 2007-9 that led to a shock to global production and trade? 2.What has been the impact of the crisis on the US vs. Canada ? 3.Why has the impact on the Developing countries been less than that on the AICs? 4.Why has the recovery been quicker in the Developing countries?

18

What caused the crisis? Market failure? Policy failure?

19

Causes of Market failures Lack Information: Markets do not know how to price systemic risk (hidden by derivatives) and investors “herd” (risk aversion) The Principle-agent: Incentives to traders to take risks; securitization of loans by banks removes monitoring Deregulations led to Moral hazard/market distortion: banks “too big to fail” and government underwriting Assumed Systemic risk: http://www.youtube.com/watch?v=UM0z6K6NDT0 2 min (watch at home)http://www.youtube.com/watch?v=UM0z6K6NDT0 Franklin Allen - What is Systemic Risk?

and investors herd (risk aversion) The Principle-agent: Incentives to traders to take risks; securitization of loans by banks removes monitoring Deregulations led to Moral hazard/market distortion: banks too big to fail and government underwriting Assumed Systemic risk: v=UM0z6K6NDT0 2 min (watch at home) v=UM0z6K6NDT0 Franklin Allen - What is Systemic Risk")

20

Risk: It’s a risky transaction between parties if one party has not entered into the contract in good faith – if it has given misleading information on important elements required for that contract to be sound: e.g., on assets, liabilities, capacity for credit, or the nature of its risk. Is the party misleading the buyer to earn a quick profit? Deregulation: the reduction or elimination of government power to regulate how an industry operates – usually to create more competition within the industry, e.g., financial market (e.g., banking sector) deregulation led to reckless lending and the housing crisis 2008 Moral hazard can be present any time two parties come into agreement with one another. Each party in a contract may have the opportunity to gain from acting contrary to the principles laid out by the agreement.

deregulation led to reckless lending and the housing crisis 2008 Moral hazard can be present any time two parties come into agreement with one another. Each party in a contract may have the opportunity to gain from acting contrary to the principles laid out by the agreement..")

22

Security An instrument representing ownership (stocks), a debt agreement (bonds) or the rights to ownership (derivatives). A security is a negotiable instrument representing financial value. The company or other entity issuing the security is called the issuer A country's regulatory structure determines what qualifies as a security. For example, private investment pools may have some features of securities, but they may not be registered or regulated as such, if they meet various restrictions.

23

Derivatives http://www.youtube.com/watch?v=X3nS5kSce_M Derek Banas 8min http://www.youtube.com/watch?v=X3nS5kSce_M A derivative is an agreement between two parties that is contingent on a future outcome. It is a financial contract with a value linked to the expected future price movements of the asset it is linked to - such as a share, currency, commodity or even the weather. Derivatives allow risk related to the price of the underlying asset to be transferred from one party to another. Options, futures and swaps, including credit default swaps, are types of derivatives. A common misconception is to refer to derivatives as assets. This is erroneous, since a derivative is incapable of having value of its own as its value is derived from another asset.

25

https://www.youtube.com/watch?v=NPfwUTm1isU understanding the fin crisis 11 min Mostafa Mourad 2009Mostafa Mourad CDO CDS, SUBPRIME, INTEREST RATE, EQUITY etc

26

SayItVisually--US Financial Crisis 4 min 2008 http://www.youtube.com/watch?v=h4Ns4ltUvfw http://www.youtube.com/watch?v=bYZdKNjTIzYhttp://www.youtube.com/watch?v=bYZdKNjTIzY sovereign bonds/debt 101- 16 min ( you can watch later) 2010 Derek BanasDerek Banas fin instruments – derivative- CDO –CDSwap – regulated market- deregulation-credit rating agencies 9 min 2011 http://www.youtube.com/watch?v=S3AXHQcXYMk

2010 Derek BanasDerek Banas fin instruments – derivative- CDO –CDSwap – regulated market- deregulation-credit rating agencies 9 min v=S3AXHQcXYMk")

27

Equity http://www.youtube.com/watch?v=tcpW0mM4OD4 equity 7.5min (watch at home) http://www.youtube.com/watch?v=tcpW0mM4OD4 A stock or any other security representing an ownership interest. In finance, equity is ownership in any asset after all debts associated with that asset are paid off, e.g., a car or house with no outstanding debt is the owner's equity because he or she can readily sell the item for cash. Stocks are equity because they represent ownership in a company. Interest Rate Swap financing involves two parties (MNCs) who agree to exchange loan payments (cash flows), results in benefits for both parties. Floating vs. fixed rate exchange Currency Swap - One party swaps the interest payments of debt (bonds) denominated in one currency (USD) for the interest payment of debt (bonds) denominated in another currency (BP), Currency swap is used for cost savings on debt, or for hedging long term currency risk.

who agree to exchange loan payments (cash flows), results in benefits for both parties. Floating vs. fixed rate exchange Currency Swap - One party swaps the interest payments of debt (bonds) denominated in one currency (USD) for the interest payment of debt (bonds) denominated in another currency (BP), Currency swap is used for cost savings on debt, or for hedging long term currency risk..")

28

CDS: The buyer of a Credit Default Swap receives credit protection, whereas the seller of the swap guarantees the credit worthiness of the product. By doing this, the risk of default is transferred from the holder of the fixed income security to the seller of the swap. For example, the buyer of a credit swap will be entitled to the par value of the bond by the seller of the swap, should the bond default in its coupon payments.

29

Subprime Subprime is a classification of borrowers with a tarnished or limited credit history. Lenders will use a credit scoring system to determine which loans a borrower may qualify for. Subprime loans are usually classified as those where the borrower has a credit score below 640. Subprime loans carry more credit risk, and as such, will carry higher interest rates as well. Approximately 25% of mortgage originations in US are classified as subprime. Subprime lending encompasses a variety of credit types, including mortgages, auto loans, and credit cards.

30

Collateralized Debt Obligation (CDO) CDOs are a type of structured asset-backed security whose value and payments are derived from a portfolio of fixed-income underlying assets. CDOs are split into different risk classes, or tranches, whereby "senior" tranches are considered the safest securities. Interest and principal payments are made in order of seniority, so that junior tranches offer higher coupon payments (and interest rates) or lower prices to compensate for additional default risk. Note: Each CDO is made up of hundreds of individual residential mortgages. CDOs that contained subprime mortgages or mortgages underwritten because of predatory lending, were at greatest risk of default. They are blamed for precipitating the global crisis and have been called WMD “weapons of mass destruction.”

or lower prices to compensate for additional default risk. Note: Each CDO is made up of hundreds of individual residential mortgages. CDOs that contained subprime mortgages or mortgages underwritten because of predatory lending, were at greatest risk of default. They are blamed for precipitating the global crisis and have been called WMD weapons of mass destruction. .")

31

Credit Default Swap (CDS) A CDS is an insurance contract in which the buyer of the CDS makes a series of payments to the protection seller and, in exchange, receives a payoff if a security (typically a bond or loan or a collection of loans such as a CDO) goes into default. NOTE: CDOs are widely thought to have exacerbated the financial crisis, by allowing investors who did not own a security to purchase insurance in case of its (CDOs they did not own) default. AIG (American International Group of insurers) almost collapsed because of these bets, as it was left on the hook for tens of billions of dollars in collateral payouts to some of the biggest U.S. and European financial institutions. AIG paid Goldman Sachs $13 billion in taxpayer money as a result of the CDSs it sold to Goldman Sachs.

default. AIG (American International Group of insurers) almost collapsed because of these bets, as it was left on the hook for tens of billions of dollars in collateral payouts to some of the biggest U.S. and European financial institutions. AIG paid Goldman Sachs $13 billion in taxpayer money as a result of the CDSs it sold to Goldman Sachs..")

32

What caused the crisis? Market failure? Policy failure?

33

Policy failure US and EU government “populism” over-indebts lower-income groups US and EU fiscal low-interest policies fuelled asset bubble (including commodities) Global imbalances generated growing and unsustainable debts of US, EU, and Japan (G3)

Global imbalances generated growing and unsustainable debts of US, EU, and Japan (G3)")

34

Origins of current financial crisis Since 1990s deregulation of financial markets: risk pricing replaces prudential supervision. Rise of derivative “assets” with opaque markets and few players. Bank loans replaced by bonds, etc. Huge US fiscal deficit, monetary expansion (“Greenspan put”), low savings led to a US mortgage boom/bust (non traded sector) and a huge current account deficit (traded sector). Mortgage bubbles (e.g. 1992 in UK) are familiar with obvious political costs; join recurrent bubbles in past decade (dotcoms, LTCM, Tequila etc); But this is by far the most serious systemically because it threatens the global banking system itself as creditor, and whole US electorate as debtor.

, low savings led to a US mortgage boom/bust (non traded sector) and a huge current account deficit (traded sector). Mortgage bubbles (e.g in UK) are familiar with obvious political costs; join recurrent bubbles in past decade (dotcoms, LTCM, Tequila etc); But this is by far the most serious systemically because it threatens the global banking system itself as creditor, and whole US electorate as debtor..")

35

Sub-prime lending By 2005, one in five mortgages were sub-prime, and they were particularly popular among recent immigrants trying to buy a home for the first time, and the poor.

37

Subprime Repossessions of houses in America as many of these mortgages reset to higher rates. By late 2007, one in ten homes in Cleveland had been repossessed Two million families will be evicted from their homes as their cases make their way through the courts.

39

Scale and Spread Collapse of the government backed mortgage system in the USA (Fannie and Freddie) followed by meltdown of major investment banks (Lehman, Bear, Merrill) exposed to mortgage market Mark-to-market asset pricing effects on balance sheets and cumulative liquidity retraction due to rising risk aversion Affecting insurance, e.g., American International Group, Inc. (AIG) ; and pensions funds

; and pensions funds.")

40

Global mortgage boom and bust

41

The end of the stock market boom in U.S., 2007-08

42

Financial Times, 20 Sept 2008 “… bank boards and bank executives have failed to understand complex mortgage-backed banking products, as have central bankers, regulators and credit rating agencies.” “…a reward system that has granted huge bonuses to those who peddled toxic mortgage-related products….” “Almost as absurd has been the degree of leverage racked up by investment banks.”

43

Policy reactions Fannie Mae and Freddie Mac (re)nationalised; Merrill sold to BankAmerica; Lehman to Barclays; Goldman and Morgan become banks again; US govt $700bn purchase of bad debt; G3 central banks support world banking. Expansionary monetary policy (to avoid recession like 1930s) and scale of US Govt (and G3) bailouts will have large repercussions, yet to be evaluated [lessons of Mexico etc?]

and scale of US Govt (and G3) bailouts will have large repercussions, yet to be evaluated [lessons of Mexico etc ].")

44

Scale of the potential bailout in Billions (2008) http://hdr.undp.org/en/media/FitzGerald_Global_Financial_Crisis_edit.ppt

")

45

Despite massive trade shock from G3 economies (US, Euro area & Japan) decline, developing economies declined less and recovered better

decline, developing economies declined less and recovered better")

46

Developing Countries pursued autonomous policies not dependent on those of IMF strictures: Reserve accumulation to insure themselves after learning form 1990s crises Counter-cyclical macro-policies (fiscal, monetary and exch-rate) to stabilize their output More extensive safety nets (universal rather than targeted) to sustain demand

to stabilize their output More extensive safety nets (universal rather than targeted) to sustain demand")

47

World International Reserves (USD million) http://www.nber.org/public_html/confer/2011/GFC11/Dominguez_Hashimoto_Ito.pdf

")

48

Pre-crisis accumulation of Financial Reserves in Billions acts as buffer

49

Real devaluations of own currencies to accommodate the shock rebalanced their finances

50

India in 2009 http://www.youtube.com/watch?v=W5xMujBRvmU However, income distribution has worsened and poverty risen in the DW Managed exchange rates maintain output/employment rather than wages/incomes in the formal sector. The burden falls on the informal sector – lower wages and spending by the poor. Remittances from abroad declined. World Bank estimates poverty rising due to deceleration in growth Decline in job creation while labour force continues to grow

51

In AICs employment growth is negative (i.e. unemployment rises), but not in Emerging economies

, but not in Emerging economies")

52

Debt Crisis in AICs: Sudden end to a decade-long US and EU household and corporate credit boom http://www.economist.com/blogs/buttonwood/2010/06/indebtedness_after_fina ncial_crisis

53

Increasing trend in G7 sovereign debt has accelerated http://www.investopedia.com/video/play/sovereign-debt-overview/http://www.investopedia.com/video/play/sovereign-debt-overview/ 3 min on sov debt

54

What Does Sovereign Debt Mean? A national government issues Bonds in a foreign currency, in order to finance the issuing country's growth. Sovereign debt is generally a riskier investment when it comes from a developing country, and a safer investment when it comes from a developed country. The stability of the issuing government is an important factor to consider, when assessing the risk of investing in sovereign debt, and sovereign credit ratings help investors weigh this risk. Ref: http://www.investopedia.com/terms/s/sovereign-debt.asp#ixzz1d0utu3rA

55

Lenders were scared when loan defaults began to rise from 2007 on: Securitized mortgages the most “toxic”

56

lending to banks in turn became Risky- Total bank losses exceed $2 trillion: 25% of US & EU securitized mortgages written off

57

Rapid (and massive) US & EU government response Monetary expansion Fiscal expansion Bank bailouts

US & EU government response Monetary expansion Fiscal expansion Bank bailouts")

58

Interest rates in G3 cut to zero (negative in real terms)

")

59

Advanced economies’ debt/GDP ratio risen by 35% 2007-14 Though fiscal stimulus is not the main cause – rather automatic stabilisers, bailouts and lost tax base from the crisis itself

60

Inflation: In the BRICs only India is alarming

61

Asia the leading example of large reserves actively managed

62

Income distribution and poverty Stabilization and income distribution: Output shocks reduce employment; real devaluations reduce real wages Decrease of modern sector wage bill cuts informal incomes through lack of demand for the informal sector Poor urban households (casual labour and petty services) particularly hard hit

particularly hard hit")

63

Developing country employment has suffered much less than in developed

64

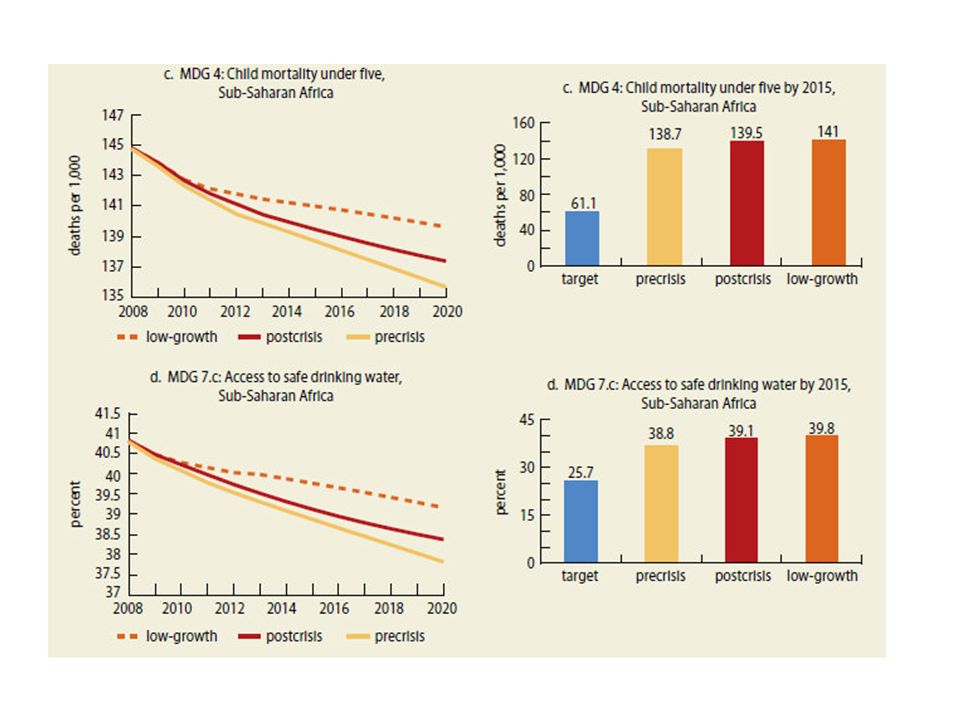

TheWorld Bank Global Monitoring Report 2010: The Millennium Development Goals (MDGs) after the Crisis (April 2010) WB projects the poverty impact of the crisis through the effect on growth; also for MDG targets “The crisis left an estimated 50 million more people in extreme poverty in 2009, and some 64 million more will fall into that category by the end of 2010 relative to a pre-crisis trend” (p. 102) That is 2% of the world population... http://www.imf.org/external/pubs/ft/gmr/2010/eng/gmr.pdf

That is 2% of the world population...")

66

Full poverty impact of the crisis will depend upon whether high growth is achieved (Asia 8%, LAC 4%, SSA 5%) or not

or not")

71

Is there an equitable stabilization possible? the heterodox stabilization policies of EMs have not protected wages and jobs or contained the impact on countries’ poverty

72

Consequences for longer-term inequality and poverty: Mainly depends on (a) growth/employment effects; and (b) fiscal redistribution Accelerated industrial shift for some countries (esp. Asia) creating employment and skills; commodity export model for others (esp LAC and SSA), requiring fiscal redistribution But greater reliance on domestic investment and saving would possibly favour Small & medium Enterprises and thus asset redistribution worldwide?

creating employment and skills; commodity export model for others (esp LAC and SSA), requiring fiscal redistribution But greater reliance on domestic investment and saving would possibly favour Small & medium Enterprises and thus asset redistribution worldwide .")

Similar presentations

Households Firms Government Foreigners Financial Markets.>")

and borrowers.>")