Download presentation

Presentation is loading. Please wait.

1

Working Capital Management

CHAPTER 21 Working Capital Management

2

Topics in Chapter Working capital policies

Cash, inventory, and A/R management Accounts payable management Short-term financing policies Bank debt and commercial paper 1

3

Basic Definitions Gross working capital: Total current assets

Net working capital (NWC): Current assets - Current liabilities Net operating working capital (NOWC): Operating CA – Operating CL = (Cash + Inv. + A/R) – (Accruals + A/P) 2

: Current assets - Current liabilities. Net operating working capital (NOWC): Operating CA – Operating CL = (Cash + Inv. + A/R) – (Accruals + A/P) 2.")

4

Working Capital Management

Day-to-day control Cash Inventories Accounts receivable Accruals Accounts payable Working capital policy The level of each current asset How current assets are financed 2

5

Cash Conversion Cycle The time between payments made for materials and labor and payments received from sales: Cash Conversion = Cycle Inventory Conversion + Period Receivables Collection − Payables Deferral (21-4)

")

6

Inventory Conversion Period

Average time required to convert materials into finished goods and to sell those goods:

7

Receivables Collection Period

Average length of time required to convert the firm’s receivables into cash: Receivables Collection Period = DSO = Days Sales Outstanding

8

Payables Deferral Period

Average length of time between the purchase of materials and labor and the payment of cash for them:

9

Real Time Computer Cash Conversion Data

10

Inventory Conversion Period

11

Receivables Collection Period

12

Payables Deferral Period

13

Cash Conversion Cycle CCC = 73 days + 24 days – 30 days CCC = 67 days

Inventory Conversion + Period Receivables Collection − Payables Deferral (21-4) CCC = days days – 30 days CCC = days

CCC = 73 days + 24 days – 30 days. CCC = 67 days.")

14

Cash Conversion Cycle Figure 21-1

15

Cash Conversion Objective

Shorten the cash conversion cycle as much as possible without hurting operations: Reduce Inventory Conversion period Process & sell goods quicker Reduce Receivables Collection period Speed up collections Lengthen Payables Deferral Period Slow firm’s payments

16

Real Time Computer TABLE 21.1

17

Real Time Computer

18

Alternative NOWC Policies

19

Cash Management: Cash = “Non-earning Asset”

Transactions: Must have some cash to pay current bills. Precautionary balances = “Safety stock” Compensating balances: For loans and/or services provided. Speculation: Take advantage of bargains Take discounts 6

20

Cash Budget: The Primary Cash Management Tool

Projected cash inflows, outflows, and ending cash balances forecast loan needs and funds available for temporary investment Daily, weekly, or monthly, depending upon budget’s purpose Monthly for annual planning Daily for actual cash management 11

21

Data Required for Cash Budget

Sales forecast Information on collections delay Forecast of purchases and payment terms Forecast of cash expenses: wages, taxes, utilities, and so on Initial cash on hand Target cash balance 12

22

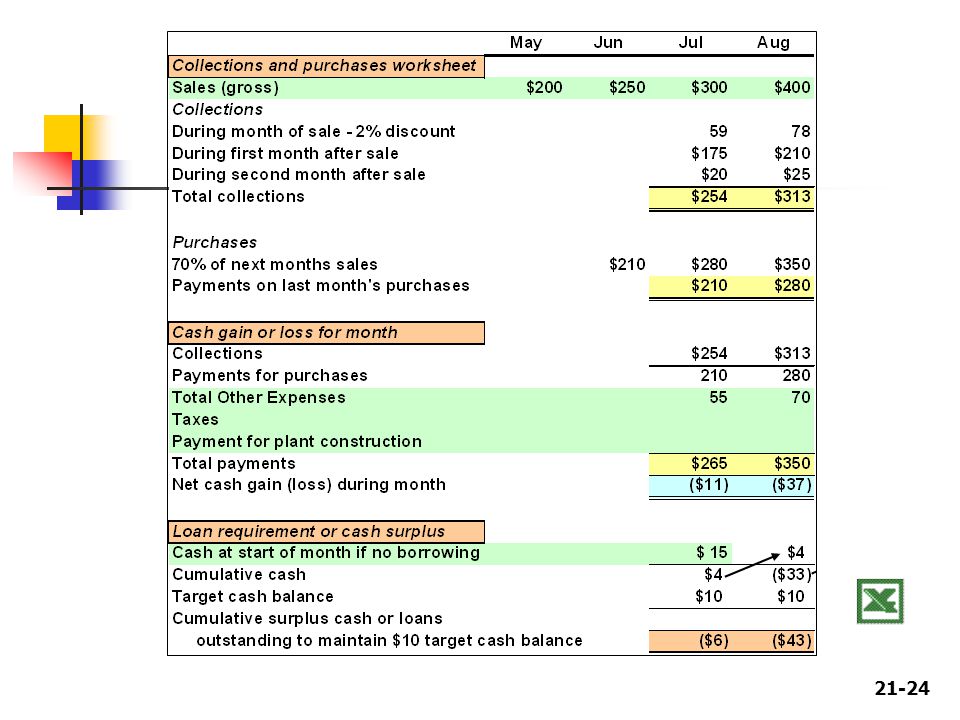

MicroDrive Cash Budget

23

Table 21-2

25

$300*20%*98% = $250*70% = $200*10% = $300*70% =

26

MicroDrive Cash Budget

27

Table 21-2

28

Other Cash Budget Line Items

Interest earned or paid = Interest rate x surplus/loan line of cash budget for preceding month Interest on any other outstanding loans Bad debt expense Collections reduced by bad debt losses. For example, if 3% bad debt losses, collections would = 97% of sales 17

29

Cash Budget with Adjustments

30

Cash Management Techniques

Synchronize inflows and outflows Billing cycle = Payment cycle Use Float Remote disbursement accounts (+) Net Collections float (-) Float Lockbox Plan Payment by wire transfer or automatic debit Reduce the need for a cash “safety stock”: Increase forecast accuracy Hold marketable securities instead of a cash Negotiate a line of credit 8

Net. Collections float (-) Float. Lockbox Plan. Payment by wire transfer or automatic debit. Reduce the need for a cash safety stock : Increase forecast accuracy. Hold marketable securities instead of a cash. Negotiate a line of credit. 8.")

31

Inventory Management Goals

Ensure that the inventory needed to sustain operations is available Minimize the costs of ordering and carrying inventory Trade-off to balance goals

32

Inventory Management: Categories of Inventory Costs

Carrying Costs Storage and handling Insurance Property taxes Depreciation Obsolescence 21

33

Inventory Management: Categories of Inventory Costs

Ordering Costs Cost of placing orders Shipping Handling costs 21

34

Inventory Management: Categories of Inventory Costs

Costs of Running Short Loss of sales Loss of customer goodwill Disruption of production schedules 21

35

Receivables Management

A/R = Credit sales/day X Collection Period Depends on volume of credit sales Average time from credit sale to collection of cash Credit policy Receivables monitoring

36

Elements of Credit Policy

Credit Period = How long to pay? Shorter period reduces DSO Reduces average A/R May discourage sales Cash Discounts Lowers price Attracts new customers Reduces DSO 25

37

Elements of Credit Policy

Credit Standards Tighter standards reduce bad debt losses, May reduce sales Fewer bad debts reduces DSO Collection Policy Tougher policy will reduce DSO May damage customer relationships

38

Receivables Monitoring

Credit sale events: Inventories reduced by COGS A/R increased by sales price Price – COGS = Profit Profit Retained Earnings DSO = Days Sales Outstanding DSO = Average Collection Period

39

Days Sales Outstanding

40

Receivables Aging Schedule

Breaks down firm’s receivables by age TABLE 21.3

41

Accruals Accrued wages and accrued taxes Increase spontaneously

Accruals are free in that no explicit interest is charged Firms have little control over the level of accruals Levels influenced by industry custom, economic factors, and tax laws

42

Trade Credit Credit furnished by a firm’s suppliers Accounts Payable

Often largest source of short-term credit, especially for small firms Spontaneously increases Easy to get, but cost can be high Example: 2/10, net 30 2% discount if paid within 10 days Due in 30 days

43

The Cost of Trade Credit

Microchip sells on terms of 2/10, net 30 True price = 98% of selling price PCC buys $100 of memory chips from Microchip If paid within 10 days Cost = $98 If PCC wants 20 extra days to pay Cost = $100 List price = $98 true cost + $2 finance charge

44

PCC’s Trade Credit Cost

PCC buys an average of $11,923,333 from Microchip $32, per day If PCC pays on day 10 PCC A/P average = 10(32,667) = $326,667 PCC is receiving $326,667 credit from Microchip

= $326,667. PCC is receiving $326,667 credit from Microchip.")

45

PCC’s Trade Credit Cost

If PCC takes the extra 20 days to pay PCC A/P average = 30(32,667) = $980,000 PCC is receiving $980, ,667 = $653,333 credit from Microchip PCC is foregoing a 2% discount PCC’s total cost = $11,923,333/0.98 = $12,166,666 Annual finance cost = $12,166,666 – 11,923,333 = $243,333 = 37.2%

= $980,000. PCC is receiving $980, ,667 = $653,333 credit from Microchip. PCC is foregoing a 2% discount. PCC’s total cost = $11,923,333/0.98. = $12,166,666. Annual finance cost = $12,166,666 – 11,923,333 = $243,333 = 37.2%")

46

Nominal Cost Formula 2/10, net 30

rNOM = Discount % 1 - Discount % × 365 days Days Taken Discount Period - = 2 98 365 20 = × 18.25 = = 37.2% PCC Pays 2.04% times per year

47

Effective Annual Rate (EAR) 2/10, net 30

Periodic rate = 0.02/0.98 = 2.04% Periods/year = 365/(30 – 10) = 18.25 EAR = (1 + Periodic rate)n – 1.0 = (1.0204)18.25 – 1.0 = 44.6%

= EAR = (1 + Periodic rate)n – 1.0. = (1.0204)18.25 – 1.0. = 44.6%")

48

The Cost of Trade Credit

49

Trade Credit Two components:

Free trade credit = discount period credit Costly trade credit = cost implied by foregone discount Firms should always use the free credit Use the costly credit only after careful analysis and comparison with other sources

50

Working Capital Financing Policies

Moderate = Match the maturity of the assets with the maturity of the financing “Maturity matching” “Self-liquidating” Aggressive = Use short-term financing to finance permanent assets Conservative = Use permanent capital for permanent assets and temporary assets

51

FIGURE 21.2 Page 751

52

Moderate Financing Policy

Years $ Perm NOWC Fixed Assets Temp. NOWC Lower dashed line, more aggressive. } S-T Loans L-T Fin: Stock & Bonds,

53

Conservative Financing Policy

Fixed Assets Years $ Perm NOWC L-T Fin: Stock & Bonds Marketable Securities Zero S-T debt

54

Short-term Investments

Marketable securities Lower yields than operating assets Held for same reasons as cash Benefits: Reduces risk and transactions costs Won’t need to issue securities or borrow as frequently Ready cash for opportunities = “speculative balances” Disadvantages Low after-tax return

55

Short-term Financing Advantages Funds available relatively quickly

Lower cost Yield curve usually upward sloping Lower flotation costs Can repay early without penalty Less restrictive loan covenants

56

Short-term Financing Disadvantages Higher risk

Interest expense fluctuates Required repayment comes quicker Firm may have trouble rolling over loans

57

Short-term Bank Loans = Notes payable Maturity Promissory Note

2/3 are for less than 1 year Frequently 90 days Promissory Note Signed when bank loan approved Specifies: Amount Interest rate Repayment schedule Collateral

58

Short-term Bank Loans Compensating Balances Informal Line of Credit

Raises the effective loan rate Illegal in many states Informal Line of Credit Maximum amount bank will extend Revolving Credit Agreement Formal line of credit Periodic commitment fee Bank legally obligated to honor agreement

59

Commercial Paper (CP) Short term, unsecured promissory notes issued by large, strong companies Maturity = 1-9 months; average 5 months Interest rates fluctuate daily just above the T-bill rate Less personal than bank relationships

60

Security in Short-term Financing

Commercial paper is never secured Better to borrow on an unsecured basis Lower bookkeeping costs Collateral options: Marketable securities Land or buildings Equipment Inventory Receivables

Similar presentations

>")

.>")

(Chapter 6 – pages 143 – 145)>")