Download presentation

Presentation is loading. Please wait.

1

Mergers and Acquisitions in British Banking: Forty Years of Evidence from 1885 until 1925 Fabio BraggionNarly DwarkasingLyndon Moore CentER, EBC &CentER,University of MelbourneTilburg University

2

M&As in U.K. Banking 1885-1925 A Study of M&As in Banking in a unregulated environment

3

M&As in U.K. Banking 1885-1925 What happens if banks are allowed to merge during a 40 year period, without the regulator (almost) ever saying no?

ever saying no .")

4

M&As in U.K. Banking 1885-1925 What happens if banks are allowed to merge during a 40 year period, without the regulator (almost) ever saying no? Who gained from mergers – acquiring shareholders, target shareholders, consumers? Why did they gain? What were the effects on banks’ risk taking?

ever saying no. Who gained from mergers – acquiring shareholders, target shareholders, consumers. Why did they gain. What were the effects on banks’ risk taking .")

5

Preview of the Results Both Bidder and Target banks experienced gains in the month of the M&A announcement Wealth creation appears to be related to both: efficiency gains increased oligopoly power. As the degree of competition decreased, banks became safer

6

Motivation Laissez-faire environment (no restrictions on mergers, no capital requirements, no deposit insurance) Only after 1917 the Treasury started to look into the phenomenon Bank managers faced few constraints from shareholders Timing of information release is unambiguous

Only after 1917 the Treasury started to look into the phenomenon Bank managers faced few constraints from shareholders Timing of information release is unambiguous")

7

Motivation We provide a useful benchmark to compare the results of studies on contemporary M&As

8

Issues and Puzzles in (contemporary) Banking M&As M&As in banking do not appear to be associated with performance improvements: At the M&A announcement bidders’ returns are negative or zero (between 0 and -2.5% ; Houston and Ryngaert, 1994, 2001) Not clear if: Methodological issue: difficult to time the event Methodological issue: not clear if the deal will succeed Or M&As really are destroying value

Banking M&As M&As in banking do not appear to be associated with performance improvements: At the M&A announcement bidders’ returns are negative or zero (between 0 and -2.5% ; Houston and Ryngaert, 1994, 2001) Not clear if: Methodological issue: difficult to time the event Methodological issue: not clear if the deal will succeed Or M&As really are destroying value")

9

Merger Process Release of information was full and spontaneous Boards met in private, settled the terms, and then communicated the terms to the shareholders No tender offers, just private negotiations The process was very quick: no more than 2-3 months from announcement to completion Although shareholders had to vote to ratify the merger this was a formality (only 1 out of almost 200 M&A agreements was disallowed by shareholders of the target bank)

")

10

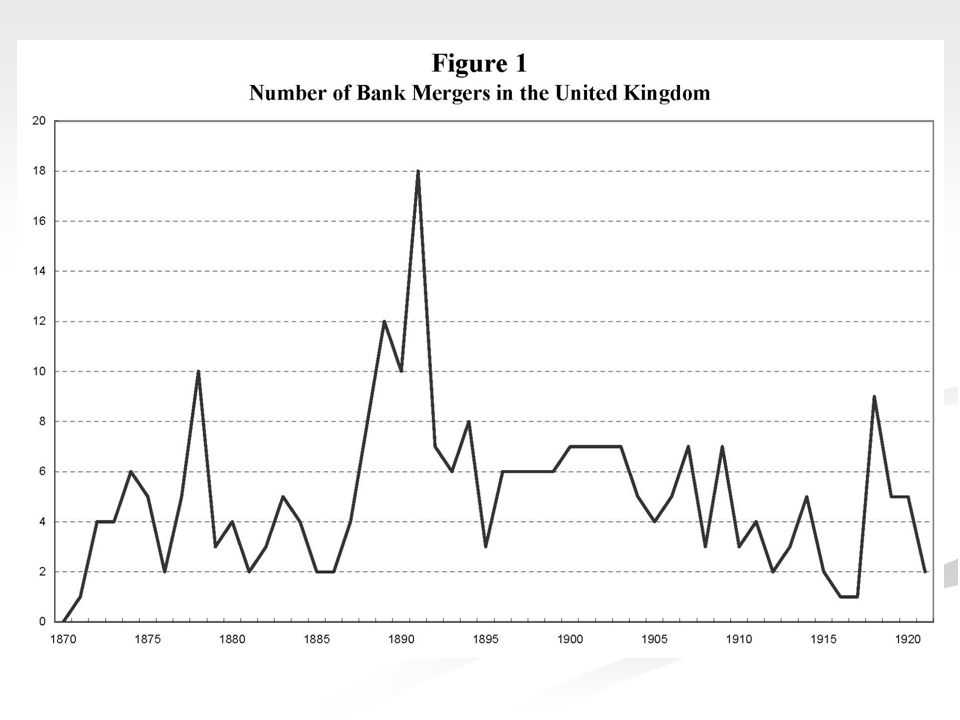

The Merger Wave 1870: 387 banks operating in the U.K. 1885 – 1900: Many takeovers of private banks by public banks 1900-1925: Mostly mergers between joint-stock banks 1920: Only 20 public banks operating in England and Wales Large rise in banking sector concentration

13

What do we do? We collect data on British banks Accounting data (profits, balance sheet info) Asset prices (of joint-stock banks) Public announcements of mergers Original merger agreements Number of Shareholders

Asset prices (of joint-stock banks) Public announcements of mergers Original merger agreements Number of Shareholders.")

14

What do we do? 1. 1. We estimate wealth effects related to the announcement of Banks’ M&As 2. 2. We identify the sources of wealth effects a) a) Cross-sectional analysis of bidders and targets wealth effects b) b) What happens to the returns of uninvolved banks? 3. 3. We estimate the impact of the mergers activities and reduction of competition on banks’ risk taking

a) Cross-sectional analysis of bidders and targets wealth effects b) b) What happens to the returns of uninvolved banks We estimate the impact of the mergers activities and reduction of competition on banks’ risk taking.")

15

Data Accounting data: The Economist Banking Supplement Asset Prices: The Investors’ Monthly Manual Announcement Dates: Times of London, Manchester Guardian and bank archives Merger Agreements: Original documents retrieved from bank archives (Barclays, HSBC, Lloyds, RBS) and the Times of London Number of Shareholders and Branch Data: London Banks and Kindred Companies and The Bankers’ magazine

and the Times of London Number of Shareholders and Branch Data: London Banks and Kindred Companies and The Bankers’ magazine")

16

Summary Statistics Mean (s.d.) Private Target Public Target Obs. Assets, £ '000 (Bidder) 50,764 (75,520) 57,455 (91,492) 45,152 (58,847) 171 Assets, £ '000 (Target) 5,282 (12,526) 1,626 (2,580) 7,352 (15,202) 141 Target in Distress 0.09 (0.84) 0.097 (0.298) 0.085 (0.281) 166 Return on Equity (Bidder) 0.108 (0.033) 0.105 (0.027) 0.109 (0.038) 166 Return on Equity (Target) 0.098 (0.161) 0.09 (0.031) 0.082 (0.023) 103 Number of Shareholders Bidder 8,322 (9,534) 7,496 (7,835) 8,979 (10,692) 167 Number of Shareholders Target 995 (2,472) 3.93 (2.12) 1,795 (3,106) 167 Branch Overlap 0.020 (0.051) 0.07 (0.020) 0.03 (0.063) 168 Payment in shares 0.76 (0.43) 0.56 (0.50) 0.88 (0.324) 152

50,764 (75,520) 57,455 (91,492) 45,152 (58,847) 171 Assets, £ 000 (Target) 5,282 (12,526) 1,626 (2,580) 7,352 (15,202) 141 Target in Distress 0.09 (0.84) (0.298) (0.281) 166 Return on Equity (Bidder) (0.033) (0.027) (0.038) 166 Return on Equity (Target) (0.161) 0.09 (0.031) (0.023) 103 Number of Shareholders Bidder 8,322 (9,534) 7,496 (7,835) 8,979 (10,692) 167 Number of Shareholders Target 995 (2,472) 3.93 (2.12) 1,795 (3,106) 167 Branch Overlap (0.051) 0.07 (0.020) 0.03 (0.063) 168 Payment in shares 0.76 (0.43) 0.56 (0.50) 0.88 (0.324) 152.")

17

Bidders’ Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 0.74*** (0.19) 0.90*** (0.24) 0.92*** (0.26) 173 1885-1905 1.03*** (0.03) 0.95*** (0.26) 1.06*** (0.31) 114 1906-19250.17 (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders

0.90*** (0.24) 0.92*** (0.26) *** (0.03) 0.95*** (0.26) 1.06*** (0.31) (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders.")

18

Bidders’ Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 0.74*** (0.19) 0.90*** (0.24) 0.92*** (0.26) 173 1885-1905 1.03*** (0.03) 0.95*** (0.26) 1.06*** (0.31) 114 1906-19250.17 (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders

0.90*** (0.24) 0.92*** (0.26) *** (0.03) 0.95*** (0.26) 1.06*** (0.31) (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders.")

19

Bidders’ Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 0.74*** (0.19) 0.90*** (0.24) 0.92*** (0.26) 173 1885-1905 1.03*** (0.03) 0.95*** (0.26) 1.06*** (0.31) 114 1906-19250.17 (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders

0.90*** (0.24) 0.92*** (0.26) *** (0.03) 0.95*** (0.26) 1.06*** (0.31) (0.27) 0.80* (0.45) 0.63 (0.52) 59 Wealth Effects – Bidders.")

20

Bidders’ Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Public Targets 0.95*** (0.27) 1.2*** (0.34) 1.13*** (0.32) 95 Private Targets 0.47** (0.23) 0.50* (0.25) 0.64** (0.30) 78 Wealth Effects – Bidders

1.2*** (0.34) 1.13*** (0.32) 95 Private Targets 0.47** (0.23) 0.50* (0.25) 0.64** (0.30) 78 Wealth Effects – Bidders.")

21

Bidders’ Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Public Targets 0.95*** (0.27) 1.2*** (0.34) 1.13*** (0.32) 95 Private Targets 0.47** (0.23) 0.50* (0.25) 0.64** (0.30) 78 Wealth Effects – Bidders

1.2*** (0.34) 1.13*** (0.32) 95 Private Targets 0.47** (0.23) 0.50* (0.25) 0.64** (0.30) 78 Wealth Effects – Bidders.")

22

Wealth Effects - Targets Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) 82 1885-1905 3.3*** (0.7) 4.5*** (1.1) 5.15*** (1.31) 47 1906-1925 10.9*** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35

Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) *** (0.7) 4.5*** (1.1) 5.15*** (1.31) *** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35.")

23

Wealth Effects - Targets Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) 82 1885-1905 3.3*** (0.7) 4.5*** (1.1) 5.15*** (1.31) 47 1906-1925 10.9*** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35

Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) *** (0.7) 4.5*** (1.1) 5.15*** (1.31) *** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35.")

24

Wealth Effects - Targets Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) 82 1885-1905 3.3*** (0.7) 4.5*** (1.1) 5.15*** (1.31) 47 1906-1925 10.9*** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35

Obs. Event Window 0-1 → 0-1 → +1 Full Sample 6.6*** (1.19) 7.9*** (1.4) 8.2*** (1.48) *** (0.7) 4.5*** (1.1) 5.15*** (1.31) *** (2.4) 12.5*** (2.7) 12.4*** (2.83) 35.")

25

Wealth Effects – Combined Average Wealth Effect (st. errors) Obs. Event Window 0-1 → 0-1 → +1 Full Sample 2.1*** (0.38) 2.5*** (0.43) 2.4*** (0.41) 82 1885-1905 1.7*** (0.29) 2.0*** (0.41) 2.1*** (0.48) 47 1906-1925 2.6*** (0.84) 3.1*** (1.03) 2.7*** (1.05) 35

Obs. Event Window 0-1 → 0-1 → +1 Full Sample 2.1*** (0.38) 2.5*** (0.43) 2.4*** (0.41) *** (0.29) 2.0*** (0.41) 2.1*** (0.48) *** (0.84) 3.1*** (1.03) 2.7*** (1.05) 35.")

26

Wealth Effects Both bidders and targets gain from mergers Combined Wealth effects increase in the time period Distribution of wealth gains shifts from bidders to targets

27

Did merger announcements leak? Pre-announcement month Bidder CAR Bidder St. error Target CAR Target St. error -50%0.1%-0.4%0.3% -4-0.2%0.2%0.4%0.3% -3-0.2%0.2%0.1%0.3% -20.2% 0.1%0.4% 0.2% 1.2%0.8%

28

What determines these gains? We tackle this issue in two ways: We relate the cross-section of bidder and target wealth effects on bidder, target and deal characteristics We check what happen to the returns of rivals/uninvolved banks at the announcement of M&As

29

Determinants of Bidder’s Wealth Effects

30

Cross Sectional Results: Bidder Bidder’s Returns were higher if the ROE of the target is lower “Restructuring” hypothesis If the target was London-based, bidder’s returns were lower London target→ “ more sophisticated” Membership of the Clearing House Gave them more bargaining power

31

Determinants of Target’s Wealth Effects

32

If the target was London-based, returns were higher compared to non-London based targets Large economic effect: A London experienced on average 10 percentage points higher abnormal returns than an identical provincial target Targets with a larger branch network had lower returns, ceteris paribus Looking at Combined wealth effects there is also an indication of a restructuring hypothesis Determinants of Target’s Wealth Effects

33

Analysis of Uninvolved Banks Mergers may have 3 effects on non-involved banks: 1. 1. Increase their returns due to increased opportunities for collusion 2. 2. Increase their returns due to learning opportunity for uninvolved banks 3. 3. Decrease their returns due to the merged entity being a stronger competitor for other banks This usually indicates gains in a efficiency of the merged entity

34

Effect on Uninvolved Banks We calculate the abnormal returns of uninvolved banks over the month in which some other banks announced that they were merging. Average AR All TargetsPublic Targets Full0.14%***0.21%*** 1885-1895-0.04%-0.01% 1896-19050.26%***0.27%*** 1906-19150.08%0.11% 1916-19251.41%***1.61%***

35

Effects on uninvolved banks? I Bank HHI : Measures a bank’s local market competition. Calculate county-level HHI, and then Bank HHI weighting by % of bank’s branches in each county: Bank HHI=1 (no local market competition)

.")

36

Effects on uninvolved banks? II Bank HHI i,j, pre : The Bank HHI of rival i before merger j took place Bank HHI i,j, post : The bank HHI of rival i after merger j has been completed ∆ Bank HHI : Bank HHI i,j, post - Bank HHI i,j, pre

37

Effects on uninvolved banks? Example In 1918 the London City and Midland bank merged with the London Joint Stock bank Both had branches in Yorkshire Affected the HHI highly of banks that mainly operated in Yorkshire: NameBHHI PreBHHI Post∆BHHI∆BHHI % Bradford District0.1370.2010.06447%

38

Regress AR of uninvolved banks on characteristics

39

Interpretation A positive relation between ∆ Bank HHI and the abnormal return for an uninvolved bank Uninvolved bank shares jump in value most when the market will experience a big increase in concentration. Greater ability to facilitate and maintain collusive agreements. Some evidence for a lender of last resort effect, as uninvolved banks with more loans to assets benefit the most from an announced merger

40

Impact of Mergers on Balance Sheets Trend decrease in bank capital ratios over the period 1885-1925. capital(mkt.) / assets declines from 20% to 10% capital(book) / assets declines from 28% to 14% Decrease in loans/assets declined 10% Increase in investments/assets from 15% to 20%

/ assets declines from 20% to 10% capital(book) / assets declines from 28% to 14% Decrease in loans/assets declined 10% Increase in investments/assets from 15% to 20%.")

42

We regress balance sheet ratios on various banks’ characteristics First: banks fixed effects regressions Second: 2SLS with Average Overlap (1885) used as an instrument for Bank HHI Banks with certain balance sheet ratios may be more/less likely to undertake acquisitions Same results Impact of Mergers on Balance Sheets

used as an instrument for Bank HHI Banks with certain balance sheet ratios may be more/less likely to undertake acquisitions Same results Impact of Mergers on Balance Sheets")

43

Fixed Effects Results

44

Effect of Competition on Ratios Less local competition (higher Bank HHI) leads to holdings of more safe marketable securities (govt. securities) and less loans to firms. Results consistent with the charter value of hypothesis Bank system (probably) become more stable, since risky loans replaced with less risky government debt.

and less loans to firms. Results consistent with the charter value of hypothesis Bank system (probably) become more stable, since risky loans replaced with less risky government debt..")

45

What did we learn? We studies 40 years of mergers in a virtually unregulated environment: Mergers were beneficial for acquirer and target shareholders Wealth creation appears to be related to both: efficiency gains and increased oligopoly power. As the degree of competition decreased, banks became safer Lending support for the so-called “Charter Value Hypothesis”

46

Some Robustness It is unlikely that the results are due to uninvolved banks learning about the benefits of consoldiation. Did it take them 30 years to learn? It is unlikely that the results are due to uninvolved banks learning about the benefits of consoldiation. Did it take them 30 years to learn? It is unlikely that the results are due to a “too big too fail type of argument”. Counterparty risk appears to be low It is unlikely that the results are due to a “too big too fail type of argument”. Counterparty risk appears to be low It is unlikely that univolved banks gained because targets’ employees abandoned the new bank It is unlikely that univolved banks gained because targets’ employees abandoned the new bank

Similar presentations

concepts 2.>")

Target shareholder wealth could increase due to value creation wealth transfer (from employees, customers, etc.). In either case,>")

Optimal Dividend Policy Conflicting Theories Other Dividend Policy Issues Residual Dividend Theory Stable.>")

>")

refers to the aspect of corporate strategy, corporate finance and management dealing.>")