Download presentation

Presentation is loading. Please wait.

1

Interest Rates and Rates of Return

Chapter 4 Interest Rates and Rates of Return

2

Discount Future Income

Debt in its most basic form is a promise to pay some amount of money $D at a period T units of money. Question: How much money, $P, would you exchange today for such a promise. In other terms, what is the discount you would apply, ,to money not available for T periods.

3

Time Deposit You bring $D to a bank and buy a time deposit for 1 year. The bank offers you an interest rate, i quoted in % terms. This means that after 1 year you can collect (1+i)$D For example, if you are offered a 10% interest rate on a $100K Time Deposit, you can collect (1+i) ×$100K where (i = .1) the payoff being $110K.

$D. For example, if you are offered a 10% interest rate on a $100K Time Deposit, you can collect (1+i) ×$100K where (i = .1) the payoff being $110K.")

4

Annualized Interest Most time deposits are made for less than a year. However, the interest rates quoted are always annualized. If you deposit funds for a time t, you will collect after t periods. For example, if you buy a 1 month time deposit, you will receive ×Y after 1 month. If you buy a 5 year time deposit, offering interest rate (1+i) , then after 5 years you will receive ×Y

, then after 5 years you will receive ×Y.")

5

Savings Deposits and Present Value

Consider if you could put $100K in a bank account that pays 10% interest for 5 years. At the end of 5 years, you will have ×$100K = $161.05K How much is a promise to pay $ K, 5 years from now worth to you today. A fair answer is $100K. If you have $100K today, then you could get $ K in 5 years by putting the $100K in the bank today. We, thus, say that $100K is the present value of a promise to pay $ K in 5 years.

6

Present Value In general $Y, put into some comparative alternative investment which pays return i could pay-off ×$Y . The present value of a payment of ×$Y in t years will have a present value of $Y. Similarly, the present value of a pay-off of $D in t years is

7

Definitions Present Value – The current value of a stream of future payments. The present value of a payment is less than its nominal value because a dollar today is worth more than a dollar in the future. This is so, because a dollar today can be used to earn interest. Discount Factor: The interest rate used to discount the value of future payments. Should be equivalent to the interest that could be earned over the time until the future payment is made.

8

Present Value of a Lottery

Last year, in the US, a lottery (called Powerball) paid prizes to 4 people. These prizes were advertised as the equivalent of HK$500 Million each. But were they really? The prizes were actually paid in even installments over 20 years. This means that the payments were $25 million each. The final payment would be received in 19 years. Using the formula we can calculate the present value of these payments. If the bank interest rate is 10%, what is the present value of $25 million in 19 years PV =

paid prizes to 4 people. These prizes were advertised as the equivalent of HK$500 Million each. But were they really The prizes were actually paid in even installments over 20 years. This means that the payments were $25 million each. The final payment would be received in 19 years. Using the formula we can calculate the present value of these payments. If the bank interest rate is 10%, what is the present value of $25 million in 19 years PV =")

9

PV of Each Payment & Total

10

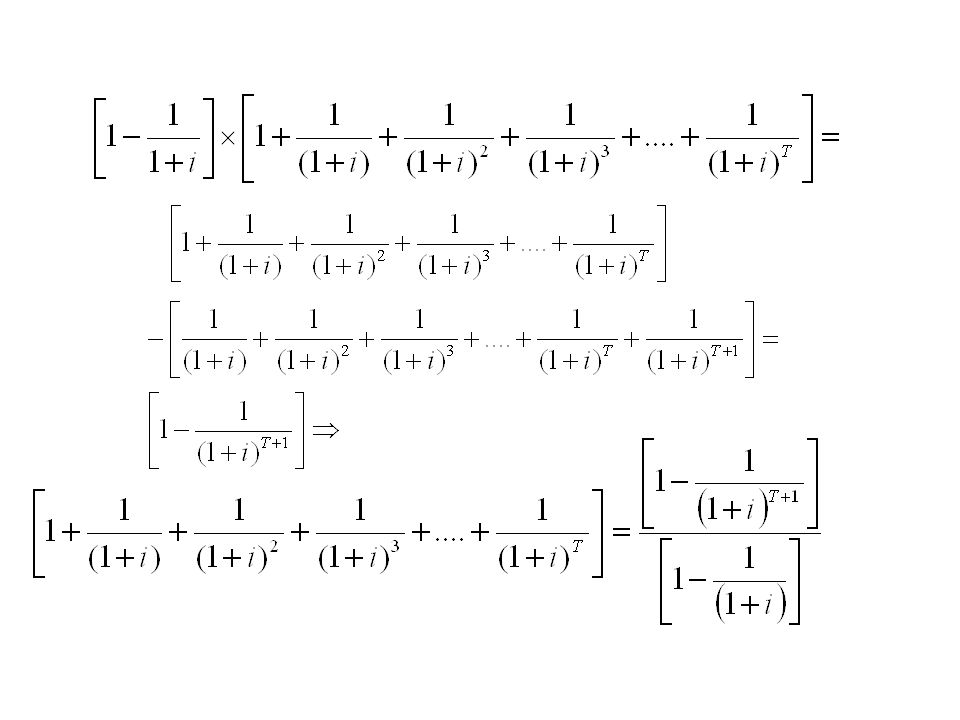

PV of Stream of Constant Payments

What is the present value of a constant stream of payments? You receive $C dollars today, next year, and every following year until year T. The present value of your payments would be given by: Take the second part of this product and multiply by

12

Example: C = 25 i=.1, T =19

13

Types of Loans and Bonds

Single Payment Debt Simple Loan Discount Bond Present Value of the Loan or Bond is the Present Value of the Final Payment. Multiple Payment Debt Fixed Payment Loan Coupon Bond Present Value of the Loan or Bond is the Sum of the Present Values of Each Payment.

14

Simple Loan A bank has lent a certain amount of money. In return, they are promised a simple pay-off T years in the future. The present value of that payment is

15

Discount Bond The issuer of a discount bond pays its Face Value at some designated time T periods from now. What is the present value of a discount bond? Note: The present value Of the discount bond is Smaller than the face value. Thus, the bond should be sold at a discount of its face value. Thus, the name.

16

Fixed Payment Loan You borrow a certain amount from the bank. Beginning next year, you will pay $C every year until year T. The present value is the sum of the present values of each payment.

17

Coupon Bond In T years, receive a payoff called the face value of the bond. In one year and every year, thereafter, the owner of the bond will receive a fixed coupon payment until the date of maturity (T) when they will receive the final coupon payment in addition to a lump sum payment called the face value of the bond. The coupon rate of the bond is the ratio of the coupon payment to the face value. The present value will be equal to

when they will receive the final coupon payment in addition to a lump sum payment called the face value of the bond. The coupon rate of the bond is the ratio of the coupon payment to the face value. The present value will be equal to.")

18

Which Discount Factor What discount rate should be used to calculate the present value of a discount or coupon bond? Should the same interest rate be used to calculate the present value for all bonds? These are two difficult questions. Basically, the discount rate that should be used to calculate present value of a future payment is the interest rate that could be obtained on some alternative asset with approximately the same level of risk. This implies that a different discount factor should be used for risky assets than for safe assets. In general, people do not like risk and risky assets should have higher discount factors. Calculating the exact risk of debt and thus the appropriate discount factor is part art and part science.

19

Yield to Maturity In the secondary market, discount and coupon bonds have a price at which they are sold. One thing that can be determined is the discount factor that sets the price of the bond equal to the present value. This rate is the yield to maturity . In the primary market, a simple loan, a fixed payment loan, and a coupon bond have an associated interest rate. For loans, the sale price in the primary market is the original payment to the borrower from the originating bank. Thus, the primary market interest rate is the yield to maturity of the loan at the time the loan was made.

20

Interpretations of Yield to Maturity

Sellers of a bond would not sell if they believed the price was less than the present value. Buyers of a bond would not sell if they believed the price more than the present value. In a competitive active market, buyers and sellers would be very close in their assessment of present value. Thus, the price will be equal to the market’s assessment of the present value. Since YTM is the discount factor that sets price equal to the present value, we can interpret YTM as the discount factor that the market uses to discount the value of the future payments offered by the bond.

21

Interpreting YTM YTM is an interest rate that allows bonds to be compared with simple assets like a bank account. YTM can be calculated across all debt. YTM is the average return that you would collect if you held the debt for the life of the instrument.

22

Loan Interest Rate: Simple Loan

The interest rate associated with a simple loan is calculated implicitly as the rate that sets the present value of the pay-off equal to the amount originally borrowed. This is easy to calculate:

23

Loan Interest Rate: Fixed Payment Loan

The interest rate associated with a fixed payment loan sets the present value of the payments equal to the amount of the original loan. It is difficult to solve for the interest rate on a fixed payment loan if you know the original loan and each payment. This is usually done by computer or special calculator.

24

Example: Car Loan If you know the original loan, it is relatively easy to calculate the payment level needed to generate any given interest rate. Example: You are a loan officer at a bank. A potential borrower wants to borrow $100K to buy a car and will pay back the loan over 10 years. You decide to charge a 10% interest rate. What will the payment be?

25

Yield to Maturity In secondary markets, coupon and discount bonds are sold. The yield to maturity is the interest rate that sets the price equal to the present value of the bond. The maturity date of a bond is the date of its final pay-off. The yield to maturity of a discount bond that matures in T periods is easy to calculate. Note: The price of the bond is inversely related to the yield to maturity. If you can buy a bond for a very low price relative to the face value, you can earn a very high return.

26

Examples HKMA issues a 3 year discount Exchange Fund note that with a face value of $1 Million. They sell the note for $700K. The yield to maturity of the note is 12.62% Note: We automatically expect the price of a discount note to rise as we get closer to the maturity date. If the yield to maturity stays constant, we would expect that in one year (when the maturity of the note is T = 2)

")

27

Then someone offers the owner of the discount note 800K in the secondary market. What is the yield to maturity that the new purchaser can expect. Note: A rise in the price is associated with a fall in the yield to maturity. Since the new owner has paid a high price for a future payment, he is discounting the future payment by less.

28

Yield to Maturity of Coupon Bond

The YTM of a Coupon Bond sets the price equal to the present value Its easy to calculate the coupon rate (the ratio of the coupon payment to the face value). Its also easy to calculate the current yield. The current yield is the ratio of the coupon payment to the price. Example: A coupon bond with a face value of $1 Million, a price of $900K and a coupon of $100K has a coupon rate of 10% and a current yield of 11.11%.

. Its also easy to calculate the current yield. The current yield is the ratio of the coupon payment to the price. Example: A coupon bond with a face value of $1 Million, a price of $900K and a coupon of $100K has a coupon rate of 10% and a current yield of 11.11%.")

29

YTM vs. Coupon Rate vs. Current Yield

If the price of the bond is equal to the face value, then the yield to maturity is equal to the coupon rate and the current yield.

30

If the price of the bond is lower than the face value, the yield to maturity is greater the current yield which is greater than the coupon rate face value.

31

Intuitively, if the price is less than the face value, the return of the coupon will be higher relative to the initial investment of the purchaser (the price) than the coupon rate. Further, if the purchaser holds the bond until the maturity date, they will get an extra return as money returned at maturity will exceed the initial purchase price Conversely, if the price of the bond is higher than the face value, the yield to maturity is less than the current yield which is less than the coupon rate.

32

Price and Discount Factors

Typically, bond underwriters negotiate an interest rate and price with initial buyers of bonds so that the price is very close to the face value. Thus, initially, the coupon rate will be very close to the yield to maturity. However, in secondary markets, the price may fluctuate in later periods. Why? Remember, the yield to maturity is the discount factor used by the market. If the markets discount factor changes, so will the price of a bond.

33

Examples A bank issues a bond and a note,each with a face value of $1000. The note is issued with a 2 year maturity and the bond is issued with a 10 year maturity. The market has a discount factor such that a yield to maturity of 10% would set the price equal to present value. The bond issuer offers a coupon rate of 10% and sells both instruments for the face value. After 1 year, the first coupon payment is made. If new bonds issued at that date also have an interest rate of 10%, the price of both instruments would remain at 1000. Note: If the coupon rate equals the yield to maturity, then the face value will equal the price no matter how long the maturity is.

34

Bond Price Changes What if the discount factor next year is a 20% interest rate. This might constitute a reasonable alternative discount factor. What is the price of the note at this time? What is the price of the bond at this time?

35

The rise in the interest rate leads to a decline in prices.

A given rise in the YTM has a much larger impact on the price of the long bond (the bond with the later maturity). This is because higher interest rates persist over the longer life of the bond and result on much larger discount of the final pay-off. Fluctuations in the price of bonds due to changes in interest rates are known as interest rate risk. If you have to sell the bond before the maturity date, you can lose money if interest rates rise.

. This is because higher interest rates persist over the longer life of the bond and result on much larger discount of the final pay-off. Fluctuations in the price of bonds due to changes in interest rates are known as interest rate risk. If you have to sell the bond before the maturity date, you can lose money if interest rates rise.")

36

Return Consider the pay-off of the bond to a person who had bought 1 of each kind of bond at the initial date for 1000, but sold each after the first coupon payment was made. The gross return on holding an asset for 1 period is the payoff at the end of 1 period divided by the price of the asset at the beginning of the period:

37

The net return on an asset is the gross return –1

The net return on an asset is the gross return –1 . We see that the note holder received a return of less than 2%, much less than the anticipated yield to maturity. The bond holder actually lost money and received a large negative return. Net Return is -.30

38

Returns vs. YTM YTM is an ex ante calculation of average returns of the bond. Returns are ex post calculation of payoff vs. price of holding bonds for some given period. If market discount factor/YTM rises, bond prices will fall. This means that ex post returns will be lower than original YTM, but future returns will be higher than original YTM

39

Floating Rate Notes and Interest Rate Risk

Since the 1980’s, issuers of long-term debt instruments have insulated their creditors from interest rate risk through floating rate notes. Floating rate notes allow the coupon payment to change with the market interest rate. When the coupon payment is made in any given period, the payment is made as a percentage of the face value called the coupon rate. Under a floating rate bond, the coupon rate changes when the pre-determined interest rate changes. The coupon rate is expressed as a pre-determined markup over the benchmark interest rate.

40

Flexible rate international bond coupon rates are often represented as markups over LIBOR (London InterBank Offered Rate). If LIBOR is 5%, and a flexible rate bond has a LIBOR +5% rate, than the coupon payment will be 10% of the face value. When interest rates go up, and the markets discount factor goes up, so do the coupon payments, which reduces the fall in the price level.

41

Inflation and Interest Rates

The Fischer hypothesis suggests that savers and borrowers base their decisions on the so called real interest rate. Nominal return represents how much money you will receive after 1 year for giving up 1 dollar of money today Real return represents how many goods you can buy if you give up the opportunity to buy 1 good today.

42

Nominal Return Inflation Real Return Fischer Equation

43

Types of Risk Default Risk – The risk that a borrower will fail to make a promised payment of interest or principal. Interest Rate Risk - The risk that the value of financial assets and liabilities will fluctuate in response to changes in market interest rates. To Be Continued ….

Similar presentations