Download presentation

Presentation is loading. Please wait.

1

EU-India Trade and Transport Integration Prabir De RIS, New Delhi TRANSBALTIC CONFERENCE 2010 17-18 March 2010, Malmö, Sweden

2

Presentation Outline Introduction EU – Asia trade EU- India trade EU- India trade EU-Asia transport linkages Trade barriers India infrastructure projects Opportunities for Baltic Sea region for EU– India trade

3

Rise of regionalism Regional trade agreements (RTAs) have increased by nearly five-fold over 1990-2008, from 86 in 1990 to 421 in 2008 (WTO, 2009) Among the Asian countries, India leads with the largest number of FTAs (30), followed by Singapore (26), China and Korea (22 each) and Japan (19). EU is India’s largest trading partner while India ranks as the EU’s 10th most important trading partner and that trade in goods more than doubled over 2000-2008 (EUROSTAT 2009). In 2008, nearly 22% of total India’s exports went to the EU and 18% of India’s total imports came from the EU. Top export destinations within the EU were Germany (26%) followed by the United Kingdom (16%) and Belgium (13%). Goods exports have grown at an average of 14% per year, particularly commodities and manufacturing goods. A large portion of India – EU trade is remained unrealized. India – EU FTA negotiation has been slow.

. In 2008, nearly 22% of total India’s exports went to the EU and 18% of India’s total imports came from the EU. Top export destinations within the EU were Germany (26%) followed by the United Kingdom (16%) and Belgium (13%). Goods exports have grown at an average of 14% per year, particularly commodities and manufacturing goods. A large portion of India – EU trade is remained unrealized. India – EU FTA negotiation has been slow..")

4

India has high trade potential, but largely unrealized International trade in India is moving below potential Global trade in 2006: US$ 350 billion Global trade in 2006: US$ 350 billion Global trade potential: US$ 680 billion Global trade potential: US$ 680 billion About 48% of trade potential is remained to be realized About 48% of trade potential is remained to be realized Causes of high underutilization of trade are mostly economic in nature High trade barriers – both visible and invisible High trade barriers – both visible and invisible Poor transportation links Poor transportation links Inadequate trade facilitation measures Inadequate trade facilitation measures Lack of supply capabilities Lack of supply capabilities

5

Poor infrastructure holding back India’s growth Infrastructure in South Asian countries is largely inadequate and generally of poor quality. Infrastructure gap in South Asia in terms of the index widened than narrowed. South Asia’s growth potential will be realized only if we can narrow the infrastructure gap, not only between them but also with the global best practice. Laggard areas (pocket of deficits) in South Asia need utmost importance so that they can enjoy the opportunities created by regional trade liberalization and integration. Countries 199120002006 IndexRankIndexRankIndexRank India3.48503.95494.4951 Sri Lanka 2.57623.18564.3553 Pakistan2.39642.26682.8966 Bangladesh1.83732.12712.574 Nepal1.29811.37811.3886 South Asia in Global Infrastructure Rankings: RIS Index Source: Kumar, N. and P. De (2008), and RIS (2008)

in South Asia need utmost importance so that they can enjoy the opportunities created by regional trade liberalization and integration. Countries IndexRankIndexRankIndexRank India Sri Lanka Pakistan Bangladesh Nepal South Asia in Global Infrastructure Rankings: RIS Index Source: Kumar, N. and P. De (2008), and RIS (2008).")

6

India’s soft infrastructure grew much faster than hard infrastructure Particulars 199120002006 AAGR (%) 1991-2006 Railways length (1000 km) 62.4662.7663.470.13 Road length (million km) 2.353.323.855.32 Fixed line and mobile phone subscribers (per 1,000 people) 736128150.35 Air freight (million tons per km) 493.10547.65773.224.73 Air passengers carried (million) 10.7217.3027.5313.07 Air transport, registered carrier departures worldwide (million) 0.120.200.3314.89 Container port traffic (million TEUs) 0.152.454.94266.01 Electric power consumption (kWh per capita) 295.02402.02457.324.58 Electric power consumption (kWh) 255.65408.42493.787.76 Note: AAGR – Annual Average Growth Rate (%) Source: World Development Indicators CD ROM 2009, World Bank

Railways length (1000 km) Road length (million km) Fixed line and mobile phone subscribers (per 1,000 people) Air freight (million tons per km) Air passengers carried (million) Air transport, registered carrier departures worldwide (million) Container port traffic (million TEUs) Electric power consumption (kWh per capita) Electric power consumption (kWh) Note: AAGR – Annual Average Growth Rate (%) Source: World Development Indicators CD ROM 2009, World Bank")

7

India needs huge investment in physical infrastructure development Supply side bottleneck – Country’s investment in physical infrastructure is very low - 4.86% of GDP in 2004-05. ‘Deficit Everywhere’ (contrary to ‘India Everywhere’ in Davos) Shortfall in capacity in port and poor performance (avg. 24 box / hour handling rate; avg. 3 days to clear a container vessel, 6 days to clear a export consignment at port) Shortfall in capacity in port and poor performance (avg. 24 box / hour handling rate; avg. 3 days to clear a container vessel, 6 days to clear a export consignment at port) Same repeat at airports (Delhi, Mumbai……) Same repeat at airports (Delhi, Mumbai……) Planning Commission desired to raise the investments from 4.86% of GDP to 7.5% in the 11th Five Year Plan (FYP) period. Requirement is US$ 320 billion, estimated by Planning Commission, during the 11th FYP (2007-2011) Infrastructure is the critical element to India’s growth. YearPublicPrivateTotal (%)(%)(%) 1991-924.001.405.40 1995-963.201.104.30 2001-023.101.704.80 2004-053.101.764.86 Investment in Infrastructure as Percent of GDP

Shortfall in capacity in port and poor performance (avg. 24 box / hour handling rate; avg. 3 days to clear a container vessel, 6 days to clear a export consignment at port) Shortfall in capacity in port and poor performance (avg. 24 box / hour handling rate; avg. 3 days to clear a container vessel, 6 days to clear a export consignment at port) Same repeat at airports (Delhi, Mumbai……) Same repeat at airports (Delhi, Mumbai……) Planning Commission desired to raise the investments from 4.86% of GDP to 7.5% in the 11th Five Year Plan (FYP) period. Requirement is US$ 320 billion, estimated by Planning Commission, during the 11th FYP ( ) Infrastructure is the critical element to India’s growth. YearPublicPrivateTotal (%)(%)(%) Investment in Infrastructure as Percent of GDP.")

8

EU’s Trade with Asia Growing Fast

9

EU (25) trade with China (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 113.511.98384.7186.477 0 Food and live animals 1.350.385.4571.427 1 Beverages and tobacco 0.610.820.1270.237 2 Crude materials, inedible, except 7.435.264.1762.054 3 Mineral fuels, lubricants and relat 0.270.081.5390.178 4 Animal and vegetable oils, fats and 0.070.330.0590.207 5 Chemicals and related products, n.e 12.221.4313.7561.856 6 Manufactured goods classified chief 13.251.5055.5826.670 7 Machinery and transport equipment 67.463.14172.0809.199 8 Miscellaneous manufactured articles 7.641.29130.13820.059 9 Commodities and transactions not cl 3.100.991.2580.404 *SITC revision 4** Share in total trade Source: UNCOMTRADE

trade with China (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl *SITC revision 4** Share in total trade Source: UNCOMTRADE")

10

EU (25) trade with Indonesia (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 8.630.1521.5740.363 0 Food and live animals 0.360.101.5330.401 1 Beverages and tobacco 0.030.040.1290.240 2 Crude materials, inedible, except f 0.470.332.2281.096 3 Mineral fuels, lubricants and relat 0.020.002.0600.238 4 Animal and vegetable oils, fats and 0.010.052.84810.016 5 Chemicals and related products, n.e 1.540.180.8500.115 6 Manufactured goods classified chief 1.080.122.6190.314 7 Machinery and transport equipment 4.370.203.3550.179 8 Miscellaneous manufactured articles 0.390.075.8080.895 9 Commodities and transactions not cl 0.350.110.0480.015 ** Share in total trade *SITC revision 4 Source: UNCOMTRADE

trade with Indonesia (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl ** Share in total trade *SITC revision 4 Source: UNCOMTRADE")

11

EU (25) trade with India (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 45.620.8044.7560.753 0 Food and live animals 0.160.042.7550.721 1 Beverages and tobacco 0.100.140.1320.247 2 Crude materials, inedible, except f 1.911.361.1720.577 3 Mineral fuels, lubricants and relat 0.290.083.3510.386 4 Animal and vegetable oils, fats and 0.020.090.3171.115 5 Chemicals and related products, n.e 4.360.514.8540.655 6 Manufactured goods classified chief 14.151.6112.6591.519 7 Machinery and transport equipment 20.100.947.1610.383 8 Miscellaneous manufactured articles 2.980.5012.0561.858 9 Commodities and transactions not cl 1.480.480.2690.086 Source: UNCOMTRADE ** Share in total trade*SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4

trade with India (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl Source: UNCOMTRADE ** Share in total trade*SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4")

12

EU (25) trade with Japan (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 61.161.07129.7582.184 0 Food and live animals 3.661.030.1740.045 1 Beverages and tobacco 2.052.770.0200.037 2 Crude materials, inedible, except f 1.641.160.9760.480 3 Mineral fuels, lubricants and relat 0.740.210.9420.109 4 Animal and vegetable oils, fats and 0.231.070.0270.096 5 Chemicals and related products, n.e 13.081.5310.0911.361 6 Manufactured goods classified chief 5.710.657.9810.958 7 Machinery and transport equipment 21.481.0094.0745.029 8 Miscellaneous manufactured articles 10.411.7614.7002.266 9 Commodities and transactions not cl 1.490.480.5060.162 Source: UNCOMTRADE ** Share in total trade*SITC revision 4 Source: UNCOMTRADE *SITC revision 4** Share in total trade Source: UNCOMTRADE *SITC revision 4

trade with Japan (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl Source: UNCOMTRADE ** Share in total trade*SITC revision 4 Source: UNCOMTRADE *SITC revision 4** Share in total trade Source: UNCOMTRADE *SITC revision 4")

13

EU (25) trade with Korea (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 37.290.6561.8671.042 0 Food and live animals 0.910.260.1640.043 1 Beverages and tobacco 0.470.630.0230.043 2 Crude materials, inedible, except f 0.770.540.6130.302 3 Mineral fuels, lubricants and relat 0.720.212.1950.253 4 Animal and vegetable oils, fats and 0.090.430.0010.005 5 Chemicals and related products, n.e 6.070.712.4540.331 6 Manufactured goods classified chief 4.500.516.1750.741 7 Machinery and transport equipment 17.970.8446.0002.459 8 Miscellaneous manufactured articles 3.980.674.0610.626 9 Commodities and transactions not cl 1.680.540.1600.051 ** Share in total trade Source: UNCOMTRADE *SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4

trade with Korea (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl ** Share in total trade Source: UNCOMTRADE *SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4")

14

EU (25) trade with Malaysia (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 16.780.2928.1400.474 0 Food and live animals 0.380.110.6190.162 1 Beverages and tobacco 0.110.140.0040.008 2 Crude materials, inedible, except f 0.430.311.5190.747 3 Mineral fuels, lubricants and relat 0.080.020.4020.046 4 Animal and vegetable oils, fats and 0.010.041.9536.869 5 Chemicals and related products, n.e 1.500.180.9950.134 6 Manufactured goods classified chief 1.660.191.5150.182 7 Machinery and transport equipment 10.970.5117.5900.940 8 Miscellaneous manufactured articles 1.200.203.3670.519 9 Commodities and transactions not cl 0.400.130.1400.045 Source: UNCOMTRADE ** Share in total trade*SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4

trade with Malaysia (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl Source: UNCOMTRADE ** Share in total trade*SITC revision 4** Share in total trade*SITC revision 4 Source: UNCOMTRADE ** Share in total trade*SITC revision 4")

15

EU (25) trade with Thailand (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities 12.220.2128.6290.482 0 Food and live animals 0.520.153.6860.964 1 Beverages and tobacco 0.120.170.0520.096 2 Crude materials, inedible, except f 0.460.330.9620.473 3 Mineral fuels, lubricants and relat 0.050.010.2510.029 4 Animal and vegetable oils, fats and 0.020.080.1470.516 5 Chemicals and related products, n.e 2.260.261.1170.151 6 Manufactured goods classified chief 2.050.232.5190.302 7 Machinery and transport equipment 5.410.2513.8590.741 8 Miscellaneous manufactured articles 0.900.155.8880.908 9 Commodities and transactions not cl 0.380.120.1220.039 Source: UNCOMTRADE ** Share in total trade*SITC revision 4

trade with Thailand (2008) Product* Product Name ExportShare**ImportShare** (US$ bln.) (%) (%) Total Total All Commodities Food and live animals Beverages and tobacco Crude materials, inedible, except f Mineral fuels, lubricants and relat Animal and vegetable oils, fats and Chemicals and related products, n.e Manufactured goods classified chief Machinery and transport equipment Miscellaneous manufactured articles Commodities and transactions not cl Source: UNCOMTRADE ** Share in total trade*SITC revision 4")

16

Transport costs outweigh tariff in EU-Asia trade

17

Exporter1981-199019911991-200020012001-20082007# Transport cost (%)* Tariff (%)** Transport cost (%)* Tariff (%)** Transport cost (%)* Tariff (%)** China22.68613.58044.1317.07027.8986.360 India22.71513.50019.3547.07012.2376.720 Indonesia17.61312.56017.2577.76025.0237.170 Japan8.19212.63010.5415.6707.8025.030 Malaysia9.41314.60011.4835.58018.9945.280 Thailand8.86414.3405.5597.60010.5356.980 Importer: European Union (27) *Ad-valorem (as % of import value), simple average, calculated based on DOTS, IMF ** Simple average tariff, sourced from WITS, World Bank Source: Author #Averaged over 2003-2007

* Tariff (%)** Transport cost (%)* Tariff (%)** Transport cost (%)* Tariff (%)** China India Indonesia Japan Malaysia Thailand Importer: European Union (27) *Ad-valorem (as % of import value), simple average, calculated based on DOTS, IMF ** Simple average tariff, sourced from WITS, World Bank Source: Author #Averaged over")

18

India has high trade potential with EU

19

India’s trade potential with EU (contd.) Partner 2008*2008200920102011201220132014 AAGR # (US$ billion) (%) AUSTRIA1.081.401.281.481.671.932.262.6414.73 BELGIUM- LUXEMBOURG 9.5725.7423.7527.5031.4936.4142.5549.6415.47 BULGARIA0.150.410.370.410.470.570.720.8919.71 CYPRUS0.350.000.000.000.000.000.000.0020.44 DENMARK1.032.212.032.402.783.303.944.6418.30 ESTONIA0.070.100.070.080.090.100.130.159.34 FINLAND1.401.991.782.072.402.813.333.9416.33 FRANCE8.0313.0512.1614.1116.1718.8022.0725.7816.27 GERMANY17.2826.1923.1226.3629.5133.5538.5144.0011.34 GREECE0.881.541.491.721.952.252.633.0516.46 HUNGARY0.550.650.500.600.710.871.051.2715.84 IRELAND0.651.391.171.281.421.641.912.209.81 (Gravity model)

Partner 2008* AAGR # (US$ billion) (%) AUSTRIA BELGIUM- LUXEMBOURG BULGARIA CYPRUS DENMARK ESTONIA FINLAND FRANCE GERMANY GREECE HUNGARY IRELAND (Gravity model)")

20

India’s trade potential with EU Partner2008*2008200920102011201220132014AAGR# ITALY8.0214.2512.9815.0216.9219.4122.5326.1813.96 LATVIA0.150.260.180.170.190.230.270.334.32 LITHUANIA0.490.180.130.140.160.190.230.278.41 MALTA0.090.200.190.220.250.300.360.4319.33 NETHERLANDS7.9010.689.6911.2612.7114.6217.0419.8814.37 POLAND0.741.691.321.491.752.092.543.0913.84 PORTUGAL0.500.950.861.001.121.291.501.7313.61 ROMANIA0.781.761.381.591.982.683.614.7328.09 SLOVAK REPUBLIC 0.080.000.000.000.000.000.010.0124.58 SLOVENIA0.220.000.000.000.000.000.010.0119.55 SPAIN3.427.166.487.368.229.3610.8112.5112.46 SWEDEN2.543.703.033.764.545.476.587.8818.86 UNITED KINGDOM 12.2027.2922.0026.4131.1137.3645.2354.6916.73 EU (25) 78.16142.78125.96146.44167.64195.27229.81269.9414.84 Notes: *Actual trade. #Average annual growth rate Source: De, Prabir, (2010), South Asia: Trade Integration after the Global Financial Crisis, Mimeo, World Bank, Washington, D.C

, South Asia: Trade Integration after the Global Financial Crisis, Mimeo, World Bank, Washington, D.C.")

21

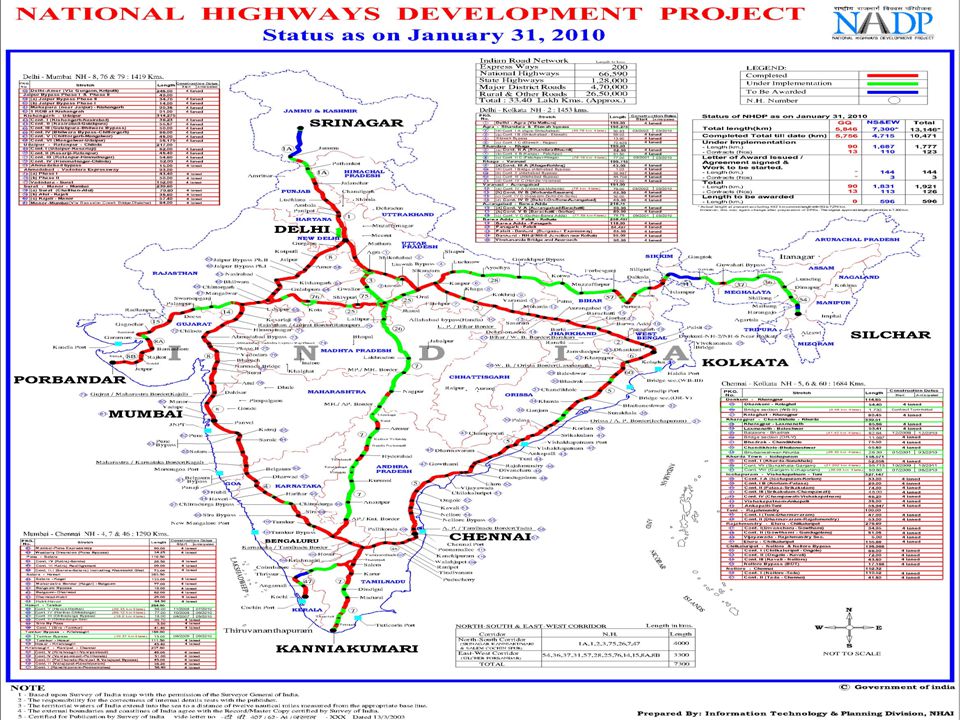

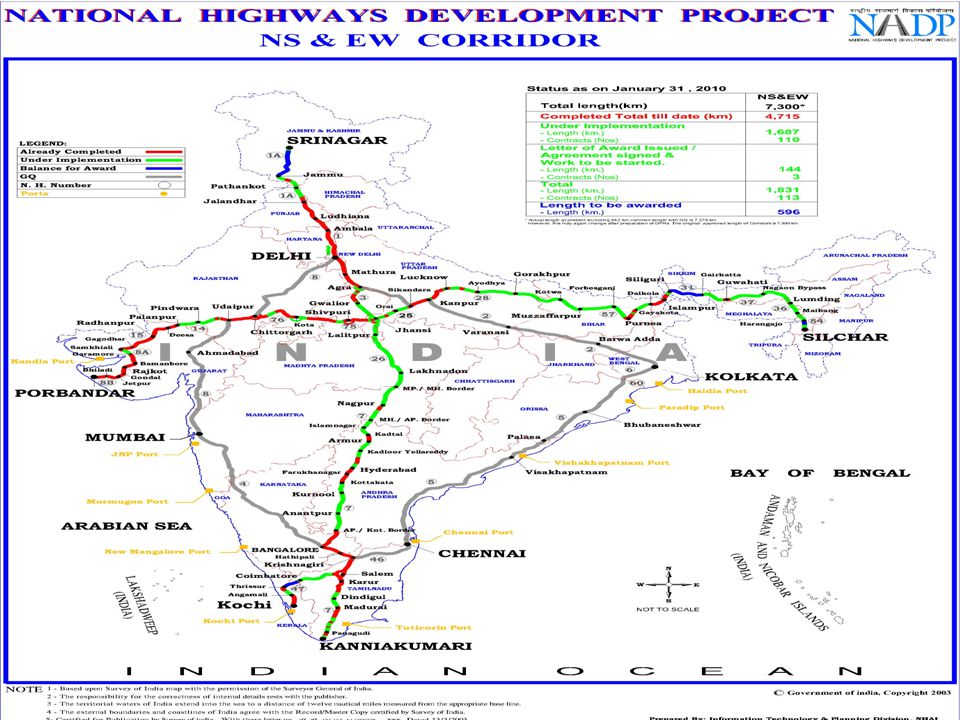

India offers high investment opportunities in infrastructure Telecom, Tourism, SEZs & Townships, Supporting Urban Infrastructure, Water & Sanitation, State & Rural Roads, Logistics etc. Source: Planning Commission, Government of India Sectors Anticipated Investment in 10 th FYP (2002-2007) Projected Investment in 11 th FYP (2007- 2011) Percentage Change US$ billion % Electricity70.5150.4111.3 Roads and bridges 31.776.1140.1 Telecom22.565.1189.3 Railways20.362.2206.4 Irrigation32.153.165.4 Water and sanitation 15.648.6211.5 Ports1.318.01284.6 Airports2.18.5304.8 Storage2.35.5139.1 Gas2.15.0138.1 Total200.5492.5145.6

Projected Investment in 11 th FYP ( ) Percentage Change US$ billion % Electricity Roads and bridges Telecom Railways Irrigation Water and sanitation Ports Airports Storage Gas Total")

25

Delhi – Mumbai Industrial Corridor (DMIC)

")

26

Dedicated Freight Corridors

27

SPV - India Infrastructure Finance Company Limited Lack of long term debt in capital markets SPV to provide long term debt to viable infrastructure projects Direct lending to PPP and public sector projects Direct lending to PPP and public sector projects Refinance for private projects Refinance for private projects Funds to be raised from domestic and external markets on strength of government guarantees Reliance on lead bank for appraisal and lending operations Guarantee limit of Rs.100 billion for first year of operation

28

India’s Overland Connectivity with East Asia India – Myanmar- Thailand Trilateral Highway India – Myanmar – Thailand – Vietnam Railway Cooperation: Delhi – Hanoi Railway Link Afghanistan – Pakistan – India – Bangladesh – Myanmar (APIBM) Transport Corridor Potential Transport Hubs in South Asia Afghanista n PakistanIndia Banglades h Sri Lanka Maritime Hub Nepal Bhutan Towards West Asia / Europe Towards Southeast / East Asia & Pacific Myanma r Maldives Towards Middle East Towards Central Asia Overland Maritime China

Transport Corridor Potential Transport Hubs in South Asia Afghanista n PakistanIndia Banglades h Sri Lanka Maritime Hub Nepal Bhutan Towards West Asia / Europe Towards Southeast / East Asia & Pacific Myanma r Maldives Towards Middle East Towards Central Asia Overland Maritime China")

29

Opportunities for Baltic Sea region for EU– India trade EU- India investment towards production / services networks holds the key Baltic sea region has to increase its FDI in India Baltic sea region has to increase its FDI in India India – Germany partnership a successful case India – Germany partnership a successful case Removal of trade barriers Higher trade costs impede trade flows between India and EU Higher trade costs impede trade flows between India and EU Opening of Asia – Europe overland connectivity Extending Asian Highway / Trans-Asian Railway Extending Asian Highway / Trans-Asian Railway

30

Thank you For further information, please contact Prabir De, PhD Fellow Research and Information System for Developing Countries (RIS) India Habitat Centre Lodhi Road New Delhi, India Tel. (+91-11) 2468 2177 Fax. (+91-11) 2468 2174 Email: prabirde@ris.org.in prabirde@hotmail.com Web: www.ris.org.in prabirde@ris.org.in prabirde@hotmail.comwww.ris.org.inprabirde@ris.org.in prabirde@hotmail.comwww.ris.org.in

Fax. (+91-11) Web:")

Similar presentations