Download presentation

Presentation is loading. Please wait.

1

Adding the Knowledge and Subtracting the Confusion

2

Contents / Agenda Accountant Rap ! & Welcome Finance Team Structure/Roles Finance Team Introductions Dental Partners Overview Business Planning DP Finance Quiz Prizes! Wrap up / questions

3

The Finance Team Welcomes you!

4

The NEW Finance Area (in the making)

")

5

Finance Team Structure General Manager Finance Manager Practice AccountantsAccounts Payable

6

Malcolm - General Manager General management / commercial Oversee the finance function Involved in acquisitions

7

Aden - Finance Manager Maintaining the daily finance function Reviewing internal controls Daily management of the team Producing monthly accounts and the annual report Analysing the financial results Consolidating the company’s budget & forecasts Annual Audit prep

8

Accountants – Tania, Jodie, Jerri Debtors reconciliation Bank Account reconciliations Commission & Administration Services calculations Management reporting including analytical review and commentary Budgeting & Forecasting Fixed assets reporting

9

Accounts Payable – Annette, Jenny, Joanne 200 invoices per day Enter invoices into Accounting Software (Navision) Reconcile invoices to supplier statements Supplier and practice queries Process supplier payments File invoices appropriately

Reconcile invoices to supplier statements Supplier and practice queries Process supplier payments File invoices appropriately")

10

DP Overview O – 61 locations in 5 years An additional 100+ practices in another 5 years $100m revenue now $250m revenue in 5 years Approaching 200 clinicians in DP Approx 500 support staff in DP 4000+ purchase invoices per month

11

DP Overview continued What does all that mean....? Rapid growth and rapid change. All of us are new within 5 years Control of a large company.....cant be hands on Light & flexible 61 locations making up one business You & the Lead Dentist run the practice Partnership

12

Business Planning Business Plan (Vision and Core Strategies) Budgeting.....numbers represent the Business Plan Numbers tell a story.....they are not the story Base line – relativity

Budgeting.....numbers represent the Business Plan Numbers tell a story.....they are not the story Base line – relativity")

13

Budgeting Things to think about: Clinical days Average daily rates Lab Fee rates and consumable rates Admin staff costs (new positions?) Marketing Premises Other Costs Fixed Assets Bottom up v Top down Positive approach v negative approach

Marketing Premises Other Costs Fixed Assets Bottom up v Top down Positive approach v negative approach")

14

Business Cycle Business Plan Budget Delivery Operational / Clinical KPIs Results P&L Exceptional Patient Care – Successful Practice

15

Summary Know The Business (the story) behind the numbers Examine the past, understand the present, plan for the future. Numbers are just numbers – it’s the story that is important.

16

DP Finance QUIZ 12 Multiple Choice Questions – 1 mark each 1 Invoice Coding Question – 4 marks 3 great mystery prizes…. ???

17

Question 1 Where should cash and cheques received during the day, be kept if banking cannot be completed prior to practice closure: a) Leave the money in a drawer until it is ready to be banked the next day; b) Put the money in a locked safe place; c) Complete deposit slip, place this with money in a quick deposit bag/sealed envelope and put it in a locked safe place; d) Put the money in an envelope, and write the amount on the front.

Leave the money in a drawer until it is ready to be banked the next day; b) Put the money in a locked safe place; c) Complete deposit slip, place this with money in a quick deposit bag/sealed envelope and put it in a locked safe place; d) Put the money in an envelope, and write the amount on the front.")

18

Question 2 On the 16th of November you discover that an EFTPOS amount of $200.00 you receipted on the 15th of November actually declined, what do you do: a) Delete the payment; and call the patient to bring another card in to process the payment; b) Process negative invoice/refund through your banking bag or banking slip for the transaction on the 16 th November; c) Ring Malcolm Lean at head office; d) Back date the correction to the 15 th November.

Delete the payment; and call the patient to bring another card in to process the payment; b) Process negative invoice/refund through your banking bag or banking slip for the transaction on the 16 th November; c) Ring Malcolm Lean at head office; d) Back date the correction to the 15 th November.")

19

Question 3 What components make up an official Tax Invoice: a) Supplier name, ABN, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; b) Supplier name, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; c) Supplier name, ACN, date, amount of FBT (if any), detailed description of sale and indication that the document is intended to be a statement; d) Hand written note on a scrap of paper.

Supplier name, ABN, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; b) Supplier name, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; c) Supplier name, ACN, date, amount of FBT (if any), detailed description of sale and indication that the document is intended to be a statement; d) Hand written note on a scrap of paper.")

20

Question 4 What should you do when you receive a credit note: a) Stamp, code, approve then fax, email and post the original invoice to DPRC; b) Stamp, code, approve then post the original invoice to DPRC; c) Post to DPRC. d) Put it in the bottom draw and forget about it; e) Set it on fire.

Put it in the bottom draw and forget about it; e) Set it on fire..")

21

Question 5 What should you do when you receive a supplier statement: a) Stamp, code, approve then fax, email and post the original supplier statement to DPRC; b) Stamp, code, approve then post the original supplier statement to DPRC; c) Post the original supplier statement to DPRC; d) Put it in the rubbish bin; e) Keep them at the practice to reconcile the invoices you receive.

Stamp, code, approve then fax, and post the original supplier statement to DPRC; b) Stamp, code, approve then post the original supplier statement to DPRC; c) Post the original supplier statement to DPRC; d) Put it in the rubbish bin; e) Keep them at the practice to reconcile the invoices you receive.")

22

Question 6 On 20 th November a patient was invoiced $150.00 twice for the same procedure, but only paid once. You discover this error on 23 rd November, what do you do: a) Change the date to 23 rd November and process an invoice correction for $150.00; b) Ignore it but make sure to email head office to inform them; c) Process a negative invoice/write off $150 on 23 rd November; d) Delete the second $150.00 invoice.

Change the date to 23 rd November and process an invoice correction for $150.00; b) Ignore it but make sure to head office to inform them; c) Process a negative invoice/write off $150 on 23 rd November; d) Delete the second $ invoice..")

23

Question 7 What should you do if you receive a supplier invoice made out to a former principle dentist’s business name or a current clinician’s personal name: a) Send to DPRC as per standard procedure; b) Call the supplier to change the name on the invoice to “Dental Partners T/A practice name”, write a note on the invoice then approve and post the original invoice to DPRC; c) Throw in rubbish bin as supplier has used incorrect details; d) Have the dentist call the company and cancel the account. Inform your PSM to contact the company and create a new account with DPRC.

24

Question 8 What should you do with the daily banking report when you print it out at the end of each day: a) Check the cash and cheque figures against what is left over from your float, then email through the report to DPRC; b) Check the report balances then compare the cash and settlement receipts for EFTPOS and HICAPS to the report and file altogether in a folder, then email the reports to DPRC; c) Email reports to DPRC then check the cash; d) Fold it up and make Japanese origami cranes.

Check the cash and cheque figures against what is left over from your float, then through the report to DPRC; b) Check the report balances then compare the cash and settlement receipts for EFTPOS and HICAPS to the report and file altogether in a folder, then the reports to DPRC; c) reports to DPRC then check the cash; d) Fold it up and make Japanese origami cranes.")

25

Question 9 In relation to credit cards, when should you attach a receipt to Smart Data: a) When you feel like it; b) Purchases of $50.00 or more; c) All receipts; d) Purchases of $102.34 or more.

When you feel like it; b) Purchases of $50.00 or more; c) All receipts; d) Purchases of $ or more.")

26

Question 10 What additional information needs to be on a lab fee invoice: a) “Good work”; b) Please pay ASAP; c) Treatment date; d) Patient name and clinician name.

Good work ; b) Please pay ASAP; c) Treatment date; d) Patient name and clinician name.")

27

Question 11 On 5 th October a patient paid the full amount owing for their treatment. A month later on 5 th November the patient complained about the treatment and, as a goodwill gesture, the dentist has agreed to refund the patient, what should you do; a) Process a refund through your PM Software, inform your PSM you have done so and request the PSM to refund the patient; b) Process a credit note adjustment and date it 5 th October; c) Complete a Patient Refund Requisition, print off the patient ledger, forward directly to your PSM and once confirmed by your PSM, process the refund in PM Software; d) Tell the patient it is easier to do a credit in the system and they can use this next time when they have treatment.

Process a refund through your PM Software, inform your PSM you have done so and request the PSM to refund the patient; b) Process a credit note adjustment and date it 5 th October; c) Complete a Patient Refund Requisition, print off the patient ledger, forward directly to your PSM and once confirmed by your PSM, process the refund in PM Software; d) Tell the patient it is easier to do a credit in the system and they can use this next time when they have treatment..")

28

Question 12 When should you complete a fixed asset disposal form: a) When there is someone you want disposed of; b) When your PSM or awesome practice accountant chases you up for one; c) When you complete a CAPEX for a replacement asset, broken/obsolete assets or for an asset that has been sold; d) Never, because I don’t see any point in it.

When there is someone you want disposed of; b) When your PSM or awesome practice accountant chases you up for one; c) When you complete a CAPEX for a replacement asset, broken/obsolete assets or for an asset that has been sold; d) Never, because I don’t see any point in it.")

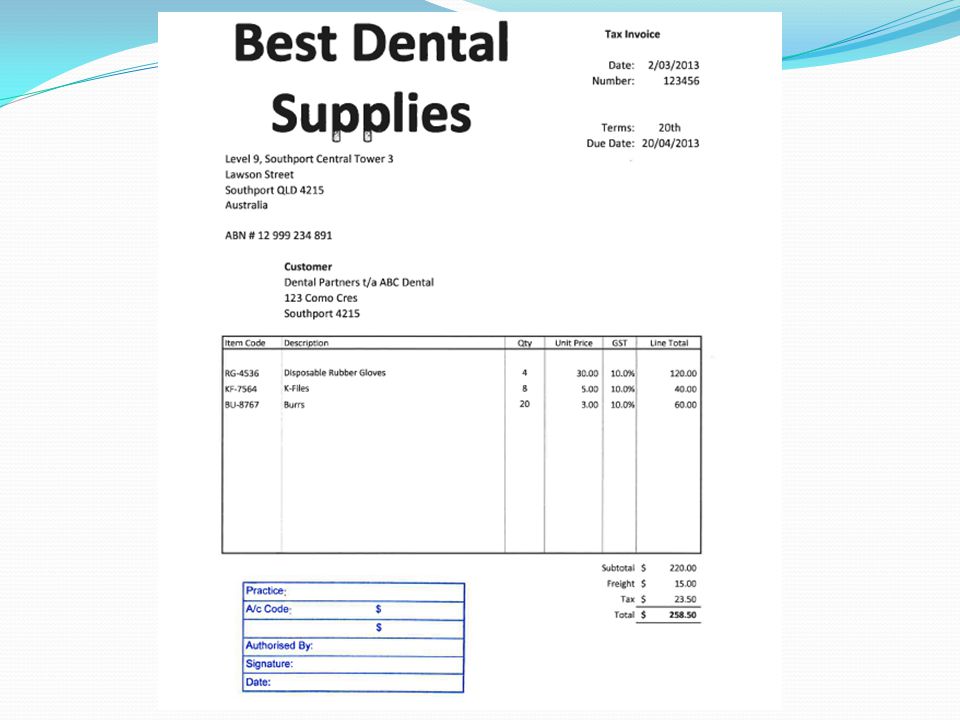

29

Question 13 TASK – correctly code and authorise the attached tax invoice. Additional information: Practice name: ABC Dentistry Practice number: 76 Practice alpha code: ABCD Select from the following account codes: 2030 Lab Fees 2040 Consumables 2050 Dental Equipment Repairs 3330 Uniforms 5162 Freight & Delivery 5170 Printing & Stationery

31

ANSWERS

32

Question 1 Where should cash and cheques received during the day, be kept if banking cannot be completed prior to practice closure: a) Leave the money in a drawer until it is ready to be banked the next day; b) Put the money in a locked safe place; c) Complete deposit slip, place this with money in a quick deposit bag/sealed envelope and put it in a locked safe place; d) Put the money in an envelope, and write the amount on the front.

Leave the money in a drawer until it is ready to be banked the next day; b) Put the money in a locked safe place; c) Complete deposit slip, place this with money in a quick deposit bag/sealed envelope and put it in a locked safe place; d) Put the money in an envelope, and write the amount on the front.")

33

Question 2 On the 16th of November you discover that an EFTPOS amount of $200.00 you receipted on the 15th of November actually declined, what do you do: a) Delete the payment; and call the patient to bring another card in to process the payment; b) Process negative invoice/refund through your banking bag or banking slip for the transaction on the 16 th November; c) Ring Malcolm Lean at head office; d) Back date the correction to the 15 th November.

Delete the payment; and call the patient to bring another card in to process the payment; b) Process negative invoice/refund through your banking bag or banking slip for the transaction on the 16 th November; c) Ring Malcolm Lean at head office; d) Back date the correction to the 15 th November.")

34

Question 3 What components make up an official Tax Invoice: a) Supplier name, ABN, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; b) Supplier name, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; c) Supplier name, ACN, date, amount of FBT (if any), detailed description of sale and indication that the document is intended to be a statement; d) Hand written note on a scrap of paper.

Supplier name, ABN, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; b) Supplier name, date, amount of GST (if any), brief description of sale and indication that the document is intended to be a tax invoice; c) Supplier name, ACN, date, amount of FBT (if any), detailed description of sale and indication that the document is intended to be a statement; d) Hand written note on a scrap of paper.")

35

Question 4 What should you do when you receive a credit note: a) Stamp, code, approve then fax, email and post the original invoice to DPRC; b) Stamp, code, approve then post the original credit note to DPRC; c) Post to DPRC. d) Put it in the bottom draw and forget about it; e) Set it on fire.

Put it in the bottom draw and forget about it; e) Set it on fire..")

36

Question 5 What should you do when you receive a supplier statement: a) Stamp, code, approve then fax, email and post the original supplier statement to DPRC; b) Stamp, code, approve then post the original supplier statement to DPRC; c) Post the original supplier statement to DPRC; d) Put it in the rubbish bin; e) Keep them at the practice to reconcile the invoices you receive.

Stamp, code, approve then fax, and post the original supplier statement to DPRC; b) Stamp, code, approve then post the original supplier statement to DPRC; c) Post the original supplier statement to DPRC; d) Put it in the rubbish bin; e) Keep them at the practice to reconcile the invoices you receive.")

37

Question 6 On 20 th November a patient was invoiced $150.00 twice for the same procedure, but only paid once. You discover this error on 23 rd November, what do you do: a) Change the date to 23 rd November and process an invoice correction for $150.00; b) Ignore it but make sure to email head office to inform them; c) Process a negative invoice/write off $150 on 23 rd November; d) Delete the second $150.00 invoice.

Change the date to 23 rd November and process an invoice correction for $150.00; b) Ignore it but make sure to head office to inform them; c) Process a negative invoice/write off $150 on 23 rd November; d) Delete the second $ invoice..")

38

Question 7 What should you do if you receive a supplier invoice made out to a former principle dentist’s business name or a current clinician’s personal name: a) Send to DPRC as per standard procedure; b) Call the supplier to change the name on the invoice to “Dental Partners T/A practice name”, write a note on the invoice then approve and post the original invoice to DPRC; c) Throw in rubbish bin as supplier has used incorrect details; d) Have the dentist call the company and cancel the account. Inform your PSM to contact the company and create a new account with DPRC.

39

Question 8 What should you do with the daily banking report when you print it out at the end of each day: a) Check the cash and cheque figures against what is left over from your float, then email through the report to DPRC; b) Check the report balances then compare the cash and settlement receipts for EFTPOS and HICAPS to the report and file altogether in a folder, then email the reports to DPRC; c) Email reports to DPRC then check the cash; d) Fold it up and make Japanese origami cranes.

Check the cash and cheque figures against what is left over from your float, then through the report to DPRC; b) Check the report balances then compare the cash and settlement receipts for EFTPOS and HICAPS to the report and file altogether in a folder, then the reports to DPRC; c) reports to DPRC then check the cash; d) Fold it up and make Japanese origami cranes.")

40

Question 9 In relation to credit cards, when should you attach a receipt to Smart Data: a) When you feel like it; b) Purchases of $50.00 or more; c) All receipts; d) Purchases of $102.34 or more.

When you feel like it; b) Purchases of $50.00 or more; c) All receipts; d) Purchases of $ or more.")

41

Question 10 What additional information needs to be on a lab fee invoice: a) “Good work”; b) Please pay ASAP; c) Treatment date; d) Patient name and clinician name.

Good work ; b) Please pay ASAP; c) Treatment date; d) Patient name and clinician name.")

42

Question 11 On 5 th October a patient paid the full amount owing for their treatment. A month later on 5 th November the patient complained about the treatment and, as a goodwill gesture, the dentist has agreed to refund the patient, what should you do; a) Process a refund through your PM Software, inform your PSM you have done so and request the PSM to refund the patient; b) Process a credit note adjustment and date it 5 th October; c) Complete a Patient Refund Requisition, print off the patient ledger, forward directly to your PSM once confirmed by your PSM, process the refund in PM Software; d) Tell the patient it is easier to do a credit in the system and they can use this next time when they have treatment.

Process a refund through your PM Software, inform your PSM you have done so and request the PSM to refund the patient; b) Process a credit note adjustment and date it 5 th October; c) Complete a Patient Refund Requisition, print off the patient ledger, forward directly to your PSM once confirmed by your PSM, process the refund in PM Software; d) Tell the patient it is easier to do a credit in the system and they can use this next time when they have treatment..")

43

Question 12 When should you complete a fixed asset disposal form: a) When there is someone you want disposed of; b) When your PSM or awesome practice accountant chases you up for one; c) When you complete a CAPEX for a replacement asset, broken/obsolete assets or for an asset that has been sold; d) Never, because I don’t see any point in it.

When there is someone you want disposed of; b) When your PSM or awesome practice accountant chases you up for one; c) When you complete a CAPEX for a replacement asset, broken/obsolete assets or for an asset that has been sold; d) Never, because I don’t see any point in it.")

44

Question 13 TASK – correctly code and authorise the attached tax invoice. Additional information: Practice name: ABC Dentistry Practice number: 76 Practice alpha code: ABCD Select from the following account codes: 2030 Lab Fees 2040 Consumables 2050 Dental Equipment Repairs 3330 Uniforms 5162 Freight & Delivery 5170 Printing & Stationery

45

ABCD - 76 2040 5162 220.00 15.00 Malcolm Lean 02/03/201 3 There are 8 pieces of information required with this authorisation, points allocated as follows: 3 or 4 correct = 1 mark 5 or 6 correct = 2 marks 7 correct = 3 marks 8 correct = 4 marks

Similar presentations

>")

1. Does your group need to prepare a budget? Yes this part is of the financial report that needs to.>")

HAREFIELD.>")