Download presentation

Presentation is loading. Please wait.

1

Airport & Airline Economics

Jeff Borowiec, Ph.D. Texas Transportation Institute If you want to be a millionaire, start with a billion dollars and open an airline. Soon enough you will be a millionaire. – Sir Richard Branson, Founder Virgin Atlantic Airlines

2

Outline Air Transportation Industry Airports Airlines

Background Significance Structure Cost/revenue framework Airports Where do airports get their money Who pays to operate/improve them How/where do they spend it Airlines Varied and complicated beasts Legacy vs. Low Cost Carriers Economic Characteristics Airspace (time permitting) Its impacts on airport and airlines and their economics Questions

Its impacts on airport and airlines and their economics. Questions.")

3

State of the Industry Airline Bankruptcies

4

State of the Industry Mergers and Acquisitions

5

State of the Industry New Fees

6

The Airport System Airside vs. Landside

7

Airport Design Primary Design Elements Drive Economics

Runways Taxiways Terminal Area/Apron Pavements Airport Site Selection Navigational Aids Airspace Primary Design Guidance: AC Change 15 Passenger Terminals Landside Access Cargo Terminals Security Emergency Services

11

l

14

National Economic Benefits

Civil aviation contributed over $1.315 Trillion 11.5 million jobs $400 Billion in earnings. 5.6 percent of the total U.S. GDP Source FAA/The Economic Impact of Civil Aviation on the U.S. Economy December 2009

15

Importance of the Texas Airport System

Link to national transportation system Connects rural & urban populations Provides 784,000 jobs Generates $49 billion annually

16

Current Status of Industry

New Large Aircraft Very Light Jets – Increased Mobility/Air Taxi services SATS – Small Aircraft Transportation System Recovering Economy Growth in Air Cargo Dependent on Air Transportation System Fractional Ownership

17

Current Status of Industry

Industry consolidation Lower margins Increased Break-Even Load Factors Emerging Aircraft with better costs per seat (Larger RJs and Mainline aircraft) Fewer Small Communities with Air Service

Fewer Small Communities with Air Service.")

18

Current Status of Industry

Half of U.S. airports depend on only one or two destinations to connect them with the air transportation system 44 percent of U.S. airports with at least 5 weekly departures are served by one carrier 39 percent of U.S. airports are served exclusively by turboprop aircraft which are in sharp decline

20

Air Transportation Network

AIRports + AIRplanes + AIRways = AIR Transportation Network Air traffic management is important because of the costs associated with delay

21

Air Transportation Network

Airports are usually locally owned Airlines are publicly held Airplanes are privately owned Airways are controlled by the federal government

22

Aviation Legislation Federal Government’s Role Dates to 1933 and the Civil Works Administration Federal Airport Act of 1946 Airport and Airway Development Act of 1970 Airport Development Aid Program Airport and Airway Improvement Act of 1982 Airport Improvement Program NPIAS airports only Airway Safety and Capacity Expansion Act of 1990 Passenger Facility Charges (PFCs)

")

23

Aviation Legislation U.S. Airline Deregulation Act of 1978

Fly where they want (route choice) Charge what they want (pricing) Resulted in: Hub and spoke network New entrants Increased competition Discount fares Growth in air travel Loyalty programs Certificate of public convenience and necessity/US DOT FAR Part 121 Operating certificate/FAA

Charge what they want (pricing) Resulted in: Hub and spoke network. New entrants. Increased competition. Discount fares. Growth in air travel. Loyalty programs. Certificate of public convenience and necessity/US DOT. FAR Part 121 Operating certificate/FAA.")

24

Regulated…… International Aviation Essential Air Service Safety

Open Skies agreements Essential Air Service DOT/Subsidies to carriers serving domestic locations that are economically challenging Safety FAA

25

Air Transportation Network

Governmental Entities FAA Primarily a SAFETY agency Airport Improvement Program Air Traffic Management NTSB Accident Investigation State Aviation Agencies Block Grant Program

26

Airports Commercial Service Reliever General Aviation

27

Airports Commercial Service Primary: >10,000 enplaned passengers

Non-primary: 2500->10,000 enplaned passengers Hub classification: Large hub: 1% or more of total national enplanements Medium hub: 0.25% to 0.99% Small hub: 0.05% to 0.24% Non-hub: less than 0.05% 2009 National Enplanements = 700 million

28

Airports General Aviation

Everything that is not scheduled passenger service or military Relievers Metropolitan airports that reduce congestion at commercial service airports in the area General aviation airports Airport role Functional class Design standard

29

Airport Ownership Local Governments Private Corporations

Cities Counties Airport Authorities Private Corporations State Governments

30

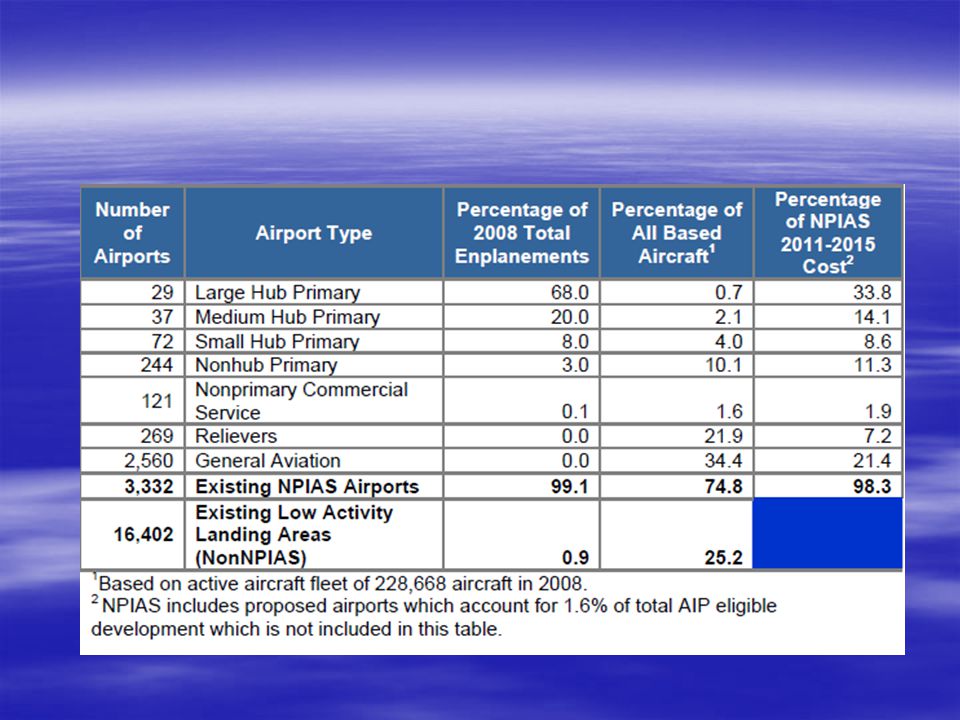

NPIAS National Plan of Integrated Airport Systems

The plan identifies 3,332 existing and 48 proposed public-use airports that are significant to national air transportation and therefore, eligible to receive grants under the Federal Aviation Administration Airport Improvement Program (AIP). The report estimates that over the next 5 years, there will be $52.2 billion of AIP eligible infrastructure development for all segments of civil aviation.

. The report estimates that over the next 5 years, there will be $52.2 billion of AIP eligible infrastructure development for all segments of civil aviation.")

31

NPIAS

32

Airport Finance – Revenues

33

Airport Finance - Expenses

NPIAS Cost by Type of Development – $49.7 B

34

Airport Finance - Expenses

NPIAS Cost by Airport Type

35

Airport Finance: Revenue and Expenses

38

Major U.S. Airport Concentration

39

Texas is BIG!

40

What is the Texas Airport System?

300 Airports & 3 Heliports 26 Primary Commercial Service 1 Non-Primary Commercial Service 25 Relievers 248 General Aviation Non-Relievers 3 Heliports

41

Texas Airport System

42

Airport Finance Who Pays? FAA Commercial Airports

Airport Improvement Program Must meet eligibility requirements Aviation user taxes (i.e., passenger ticket taxes) Commercial Airports Passenger Facility Charges (reduces AIP $) Revenue from advertising, parking, concessions, access fees State Aviation Agencies Airport Sponsors (owners) Local governments

Commercial Airports. Passenger Facility Charges (reduces AIP $) Revenue from advertising, parking, concessions, access fees. State Aviation Agencies. Airport Sponsors (owners) Local governments.")

43

Who Pays…You Do!

44

Ticket Tax Example

45

Airport Finance Airport funding comes from several sources:

Airport bonds 59% AIP grants 21% Passenger Facility Charge 13% State and local funding 4% Airport revenue 4% Source: ASCE/FAA

46

Airline Economics Characteristics Activity Metrics

Impacts of Rising Fuel Prices

47

Airline Economics Industry Characteristics Service Industry

Capital-Intensive Labor-Intensive

48

Airline Structure Operations and Maintenance Sales and Marketing

Reservations and Ticketing Management and Administrative Staff

49

Airline Metrics available seat mile (ASM) One seat transported one mile; the most common measure of airline seating capacity or supply. For example, an aircraft with 100 passenger seats, flown a distance of 100 miles, produces 10,000 ASMs. Sometimes measured in available seat kilometers (ASKs). revenue passenger mile (RPM) One fare-paying passenger transported one mile; the most common measure of demand for air travel. Sometimes measured in revenue passenger kilometers (RPKs).

One seat transported one mile; the most common measure of airline seating capacity or supply. For example, an aircraft with 100 passenger seats, flown a distance of 100 miles, produces 10,000 ASMs. Sometimes measured in available seat kilometers (ASKs). revenue passenger mile (RPM) One fare-paying passenger transported one mile; the most common measure of demand for air travel. Sometimes measured in revenue passenger kilometers (RPKs).")

50

Airline Metrics unit revenue The average amount of revenue received by the airline per unit of capacity available for sale. Most often used to measure the effectiveness with which revenue management activity balances price and volume to generate passenger revenue per ASM, known as PRASM or RASM. yield The average amount of revenue received per revenue passenger mile (RPM) or revenue ton mile (RTM), net of taxes.

or revenue ton mile (RTM), net of taxes.")

51

Airlines Majors Nationals Regionals revenue > $1B

revenue between $100M and $1B Regionals limited service/specific markets/city-pairs fastest growing since deregulation

52

Airlines by Category

53

Top 25 U.S. Airlines

54

Determinants of Demand

Demand = Revenue Passenger Miles (RPMs) Ticket price Competitor’s ticket price Passenger income State of the economy Availability of other modes Customer loyalty In-flight amenities Frequency of service Safety Random factors – SARS, 9/11, terrorism threat

Ticket price. Competitor’s ticket price. Passenger income. State of the economy. Availability of other modes. Customer loyalty. In-flight amenities. Frequency of service. Safety. Random factors – SARS, 9/11, terrorism threat.")

55

Characteristic of Demand

Constant fluctuation Cyclicality Seasonality and peaking Directional flow Perishability Schedule wait time Airport access time Flight time Hub connection time Denied boarding time

56

Factors Affecting Supply

Supply = available seat miles (ASMs) Ticket price Price of resources – aircraft, fuel, labor, maintenance Technological improvements Behavior of the competition Random factors Government regulation

Ticket price. Price of resources – aircraft, fuel, labor, maintenance. Technological improvements. Behavior of the competition. Random factors. Government regulation.")

57

Characteristics of Supply

Two characteristics that shape the industry are: Seasonality Pull existing capacity off of other routes Have excess/idle capacity somewhere in system Rigidity Can be difficult to reduce/increase supply dramatically Schedules are created six months in advance

58

Airline Markets Market Continuum

59

Evolution of U.S. Airline Industry

60

Major U.S. Airline Concentration

61

Recent Airline Mergers Airlines/Announced/Closed/Resulting Entity

62

Airline Costs

63

Airline Cost Trends

64

Airline Cost Index

65

Airlines Keeping Pace?

66

Airline Load Factors

68

Airline Costs by Function

69

Airline Costs by Category

70

Airline Fuel Costs

71

U.S. Air Carrier Traffic Statistics Through November 2010

Twelve Months - System December November 2010 December November 2009 Scheduled Non-Scheduled Total Revenue Passenger Enplanements (000) 718,719 5,845 724,564 704,253 5,390 709,643 Revenue Passenger Miles (000) 795,432,424 11,031,526 806,463,950 769,711,680 10,536,280 780,247,960 Available Seat Miles (000) 969,734,233 19,390,318 989,124,551 959,327,054 18,125,515 977,452,569 Passenger Load Factor (%) 82.03 56.89 81.53 80.23 58.13 79.82 Revenue Freight Ton Miles (000) 7,127,210 66,012 7,193,222 5,615,056 53,199 5,668,255 Total Revenue Ton Miles (000) 87,359,300 1,169,172 88,528,472 83,316,104 1,106,845 84,422,949 Available Ton Miles (000) 140,489,207 3,136,906 143,626,113 138,450,289 2,909,910 141,360,199 Ton Mile Load Factor (%) 62.18 37.27 61.64 60.18 38.04 59.72 Revenue Departures Performed 9,500,010 170,465 9,670,475 9,567,245 153,963 9,721,208 Revenue Aircraft Miles Flown (000) 6,927,463 98,244 7,025,707 6,862,290 89,339 6,951,629 Revenue Aircraft Hours (Airborne) 16,436,281 262,510 16,698,791 16,426,716 238,801 16,665,517 SOURCE: Bureau of Transportation Statistics, T-100 Market and Segment (Excludes all-cargo services. Includes domestic and international)

718,719. 5, , ,253. 5, ,643. Revenue Passenger Miles (000) 795,432, ,031, ,463, ,711, ,536, ,247,960. Available Seat Miles (000) 969,734, ,390, ,124, ,327, ,125, ,452,569. Passenger Load Factor (%) Revenue Freight Ton Miles (000) 7,127, ,012. 7,193,222. 5,615, ,199. 5,668,255. Total Revenue Ton Miles (000) 87,359,300. 1,169, ,528, ,316,104. 1,106, ,422,949. Available Ton Miles (000) 140,489,207. 3,136, ,626, ,450,289. 2,909, ,360,199. Ton Mile Load Factor (%) Revenue Departures Performed. 9,500, ,465. 9,670,475. 9,567, ,963. 9,721,208. Revenue Aircraft Miles Flown (000) 6,927, ,244. 7,025,707. 6,862, ,339. 6,951,629. Revenue Aircraft Hours (Airborne) 16,436, , ,698, ,426, , ,665,517. SOURCE: Bureau of Transportation Statistics, T-100 Market and Segment (Excludes all-cargo services. Includes domestic and international)")

72

U.S. Airlines Annual Pre-Tax Earnings

73

Airline Revenues

78

Low Cost Carriers Carry 1/3 of all US Passengers

LCC Presence in Largest 1,000 Domestic City Pairs Has Increased by More Than 30% Since 2000 Low Cost Carriers Compete In Markets Accounting For 80% Of All Domestic Air Travelers Legacy Carrier Operating Costs Have Gone Down and LCC Costs Have Gone Up

79

Fuel Price Impact

80

Cyclical?

81

Airline Operating Statistics

82

Top 25 Airlines

83

Top U.S. City Pairs

84

Top U.S. Travel Markets

85

Airline Operating Trends

86

Texas Aviation Activity Passenger Enplanements

87

Texas Commercial Service Enplanements

88

Texas Aviation Activity Texas Air Carrier Enplanements (% of U.S.)

")

89

Growth Going Forward U.S. Commercial Air Carriers 2011-2031

Supply (Domestic ASMs annual percentage growth) Mainline 2.8 Regionals 4.1 Demand (Domestic RPMs annual percentage growth) Mainline 2.9 Regionals 4.2 Profitability tied to operating costs Oil

Mainline 2.8. Regionals 4.1. Demand (Domestic RPMs annual percentage growth) Mainline 2.9. Regionals 4.2. Profitability tied to operating costs Oil.")

90

Compelling Issues Influencing/Affecting Air Transportation

Future of airline industry/consolidation Future funding/authorization User fees Other Fees Security Alternative fuels Workforce development Land use/development/encroachment Privatization – efficiency, capital infusion, conversion to tax paying entity NextGen – advanced technologies/air space management/ADS-B

91

Jeff Borowiec

92

Air Traffic Management

Air Traffic Control VFR / IFR Instrument Approaches Landing Non-precision approach/Precision approach Terminal Airspace

93

Delay Costs

94

Air Traffic Management

Phases of Flight ATC Tower TRACON ARTCC RVSM Area of greatest potential for efficiency gains

95

Instrument Approaches

96

Air Traffic Management

97

Air Traffic Management

98

GPS and WAAS The Global Positioning System (GPS) is a system of 24 satellites operated by the Department of Defense (DOD) under joint DOD/Department of Transportation (DOT) management. Wide Area Augmentation System uses a series of ground stations to augment or enhance the GPS signal increasing its accuracy. Allowed for new instrument approaches and reduced minimums.

is a system of 24 satellites operated by the Department of Defense (DOD) under joint DOD/Department of Transportation (DOT) management. Wide Area Augmentation System uses a series of ground stations to augment or enhance the GPS signal increasing its accuracy. Allowed for new instrument approaches and reduced minimums.")

99

Glass Cockpits B-777 Garmin 1000 Cirrus S-22 G550

100

ADS-B An air traffic system that will provide more precise surveillance data to air traffic controllers and to ADS-B equipped aircraft at the same time. This information will significantly enhance pilots’ situational awareness.

101

ADS-B ADS-B uses Global Navigation Satellite System (GNSS) position information processed by aircraft avionics to transmit the aircraft’s location to ground receivers for presentation to air traffic controllers. Pilots with ADS-B avionics will receive traffic and weather information on their cockpit displays. Controllers will see the information on automation displays they are already using, so little additional training will be needed. ADS-B signals are transmitted once per second, providing a more accurate tracking system for pilots and controllers.

position information processed by aircraft avionics to transmit the aircraft’s location to ground receivers for presentation to air traffic controllers. Pilots with ADS-B avionics will receive traffic and weather information on their cockpit displays. Controllers will see the information on automation displays they are already using, so little additional training will be needed. ADS-B signals are transmitted once per second, providing a more accurate tracking system for pilots and controllers.")

102

ADS-B Improved efficiency Improved situational awareness

Improved safety Greater ATC predictability Cost savings

103

Air Traffic Management

104

FAA Part 77 Imaginary Surfaces

Physical Obstacles Ensure and preserve safety of operations in the airspace in the immediate vicinity of airports Surfaces protect approaches to runways, takeoffs, and missed approaches from obstructions Objects can be man-made or natural They impact height-hazard zoning restrictions and could affect construction costs/airport viability

105

FAA Part 77 Imaginary Surfaces

107

Compelling Issues Affecting Air Transportation

Future of airline industry Future funding/authorization User fees Alternative fuels Workforce development Land use/development/encroachment Privatization – efficiency, capital infusion, conversion to tax paying entity NextGen – advanced technologies/air space management

108

Jeff Borowiec

Similar presentations

was an analysis designed to help the Commonwealth identify a.>")

for Aviation United Nations International Committee on GNSS 1 - 2 December, 2005 Ken Alexander United States.>")

Saulo Da Silva>")