Download presentation

Presentation is loading. Please wait.

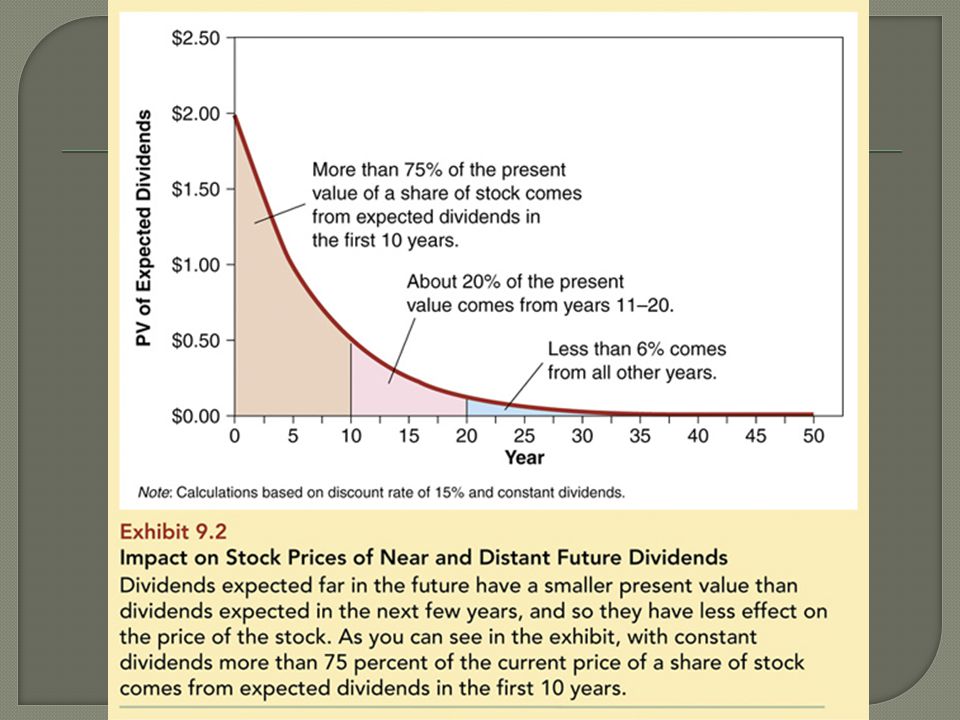

5

Fundamental Analysis – looks at financials, product, mgt., history, etc. PE ratio – Price / E.P.S. Zero-Growth Dividend (preferred stock) Constant Growth Dividend (DCF) Nonconstant Growth

Constant Growth Dividend (DCF) Nonconstant Growth.")

6

Technical Analysis – uses charts to predict future prices

7

Industry Average PE X Companys EPS If company EPS = $2.20 and industry average PE = 20, stock should sell around $_____. Factors affected a companys PE include: Risk Expected future growth Management Dividends

8

Preferred has preference in claims to assets and dividends – must be paid before common. Preferred dividends – fixed Common dividends – fluctuate Preferred usually have no voting rights

10

P 0 = Value of Preferred Stock = PV of ALL dividends discounted at investors Required Rate of Return 52 WeeksYldVol Net HiLoStockSymDiv%PE100sHiLoCloseChg s42½29QuakerOatsOAT1.143.32450673534¼34¼-¾ s36¼25RJR NabiscoRN.08p...12626329¾28 5 / 8 28 7 / 8 -¾ 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾... 7¼5½RJR Nab pfC.609.4...22486½6¼6 3 / 8 - 1 / 8 0 1 2 3 P 0 =23.75D 1 =2.31D 2 =2.31D 3 =2.31D =2.31 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾...

11

P 0 = + + +··· 2.31 (1+ r p ) 2.31 (1+ r p ) 2 2.31 (1+ rk p ) 3 52 WeeksYldVol Net HiLoStockSymDiv%PE100sHiLoCloseChg s42½29QuakerOatsOAT1.143.32450673534¼34¼-¾ s36¼25RJR NabiscoRN.08p...12626329¾28 5 / 8 28 7 / 8 -¾ 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾... 7¼5½RJR Nab pfC.609.4...22486½6¼6 3 / 8 - 1 / 8 0 1 2 3 P 0 =23.75D 1 =2.31D 2 =2.31D 3 =2.31D =2.31 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾... If an investor expects a 10% return, how much are they willing to pay for the stock?

12

P 0 = D R = 2.31 10% = $23.10 P 0 = + + +··· 2.31 (1+ r p ) 2.31 (1+ r p ) 2 2.31 (1+ rk p ) 3 52 WeeksYldVol Net HiLoStockSymDiv%PE100sHiLoCloseChg s42½29QuakerOatsOAT1.143.32450673534¼34¼-¾ s36¼25RJR NabiscoRN.08p...12626329¾28 5 / 8 28 7 / 8 -¾ 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾... 7¼5½RJR Nab pfC.609.4...22486½6¼6 3 / 8 - 1 / 8 0 1 2 3 P 0 =23.75D 1 =2.31D 2 =2.31D 3 =2.31D =2.31 23 7 / 8 20RJR Nab pfB2.319.7...9662423 5 / 8 23¾... Zero-Growth Div. Model

13

P 0 = PV of ALL expected dividends discounted at investors Required Rate of Return Investors do not know the values of D 1, D 2,...., D N. The future dividends must be estimated. D1D1 D2D2 D3D3 P0P0 D 0 1 2 3 P 0 = + + +··· D 1 (1+ r s ) D 2 (1+ r s ) 2 D 3 (1+ r s ) 3

D 2 (1+ r s ) 2 D 3 (1+ r s ) 3.")

14

Assume that dividends grow at a constant rate (g). D 1 =D 0 (1+g) D0D0 D 2 =D 0 (1+g) 2 D 3 =D 0 (1+g) 3 D =D 0 (1+g) 0 1 2 3

D0D0 D 2 =D 0 (1+g) 2 D 3 =D 0 (1+g) 3 D =D 0 (1+g)")

15

Requires r > g Reduces to: P 0 = + + + ··· + D 0 (1+ g) (1+ r s ) D 0 (1+ g) 2 (1+ r s ) 2 D 0 (1+ g) 3 (1+ r s ) 3 P 0 = = D 0 (1+g) r – g D 1 r – g D 1 =D 0 (1+g) D0D0 D 2 =D 0 (1+g) 2 D 3 =D 0 (1+g) 3 D =D 0 (1+g) 0 1 2 3

(1+ r s ) D 0 (1+ g) 2 (1+ r s ) 2 D 0 (1+ g) 3 (1+ r s ) 3 P 0 = = D 0 (1+g) r – g D 1 r – g D 1 =D 0 (1+g) D0D0 D 2 =D 0 (1+g) 2 D 3 =D 0 (1+g) 3 D =D 0 (1+g)")

17

Gordon Growth Company is expected to pay a dividend of $4 next period and dividends are expected to grow at 6% per year. The required return is 16%. What is the current price?

18

What is the price expected to be in year 4?

19

Used with companies that have very high growth rates. Calculate the PV of cash flows or dividends for the high growth period. Solve for the PV of cash flows during the constant growth period that are a perpetuity. The sum of these two is the stock price.

20

9900010203040506070809101112Sales.2M6M86M440M1.4B3B6B10B16B21B23B29B37B50B Net Income -6M-15M7M100M105M 400 M 1.4 B 3B4.2B4.2B6.5B8.5B9.7B 10.7 B

21

Can no longer only use constant growth model. However, growth becomes constant after 3 years.

22

Supernormal growth followed by constant growth: 01234 r=13% = P 0 g = 30% g = 6% D 0 = 2.00 2.603.38 4.39 4.66 ^

23

Supernormal growth followed by constant growth: 01234 r =13% = P 0 g = 30% g = 6% D 0 = 2.00 2.603.38 4.39 4.66 ^

24

Supernormal growth followed by constant growth: 0 2.30 2.65 3.05 46.11 1234 r s =13% 54.11 = P 0 g = 30% g = 6% D 0 = 2.00 2.603.38 4.39 4.66 ^ Do not add in D 0

25

01234 r s =13% g = 0% g = 6% 2.00 2.00 2.00 2.12. P 3...

26

01234 r s =13% g = 0% g = 6% 2.00 2.00 2.00 2.12 2.12. P 3 007 30.29...

27

0 1.77 1.57 1.39 20.99 1234 r s =13% 25.71 g = 0% g = 6% 2.00 2.00 2.00 2.12 2.12. P 3 007 30.29...

28

Terminal Value – the (present) value, at the horizon date, of all future dividends after that date.

value, at the horizon date, of all future dividends after that date.")

29

Suppose a firm is expected to increase dividends by 20% in one year and by 15% in two years. After that dividends will increase at a rate of 5% per year indefinitely. If the last dividend was $1 and the required return is 20%, what is the price of the stock? Remember that we have to find the PV of all expected future dividends.

30

Compute the dividends until growth levels off D 1 = 1(1.2) = $1.20 D 2 = 1.20(1.15) = $1.38 D 3 = 1.38(1.05) = $1.449 Find the expected future price at the beginning of the constant growth period: P 2 = D 3 / (R – g) = 1.449 / (.2 -.05) = 9.66 Find the present value of the expected future cash flows P 0 = 1.20 / (1.2) + (1.38 + 9.66) / (1.2) 2 = 8.67

= $1.20 D 2 = 1.20(1.15) = $1.38 D 3 = 1.38(1.05) = $1.449 Find the expected future price at the beginning of the constant growth period: P 2 = D 3 / (R – g) = / ( ) = 9.66 Find the present value of the expected future cash flows P 0 = 1.20 / (1.2) + ( ) / (1.2) 2 = 8.67")

31

Nonconstant + Constant growth

32

0 1.00 0.96 6.71 123 R = 20% 8.67 = P 0 g = 20%g = 15%g = 5% D 0 = 1.00 1.201.38 1.449 $1.449 P 2 = ^ 0.20 – 0.05 = $9.66

33

The Jones Company has decided to undertake a large project. Consequently, there is a need for additional funds. The financial manager plans to issue preferred stock with a perpetual annual dividend of $5 per share. If the required return on this stock is currently 20 percent, what should be the stock's market value?

34

The Jones Company has decided to undertake a large project. Consequently, there is a need for additional funds. The financial manager plans to issue preferred stock with a perpetual annual dividend of $5 per share. If the required return on this stock is currently 20 percent, what should be the stock's market value? 5.20 = 25

35

A share of preferred stock pays a quarterly dividend of $2.50. If the price of this preferred stock is currently $50, what is the nominal annual rate of return?

36

2.5 X 4 = 10/year 10/50 = 20%

37

McKenna Motors is expected to pay a $1.00 per-share dividend at the end of the year (D1 = $1.00). The stock sells for $20 per share and its required rate of return is 11 percent. The dividend is expected to grow at a constant rate, g, forever. What is the growth rate, g, for this stock? P 0 = D 1 R – g

38

McKenna Motors is expected to pay a $1.00 per-share dividend at the end of the year (D1 = $1.00). The stock sells for $20 per share and its required rate of return is 11 percent. The dividend is expected to grow at a constant rate, g, forever. What is the growth rate, g, for this stock? D 1 /(R-g) = 20 1/(.11-g) = 20 1 = 2.2 – 20g -1.2 = -20g -1.2/-20 = g.06 = g

= 20 1/(.11-g) = 20 1 = 2.2 – 20g -1.2 = -20g -1.2/-20 = g.06 = g.")

39

A share of common stock has just paid a dividend of $2.00. If the expected long- run growth rate for this stock is 15%, and if investors require a 19% rate of return, what is the price of the stock?

40

2.00 X (1.15) = 2.30 = D 1 P = 2.30 / (.19 -.15) P = 2.30 /.04 P = $57.5

= 2.30 = D 1 P = 2.30 / ( ) P = 2.30 /.04 P = $57.5")

41

A firms stock is selling for $10.50. They just paid a $1 dividend and dividends are expected to grow at 5% per year. What is the required return?

42

P 0 = $10.50. D 0 = $1 g = 5% per year. What is the required return?

43

P 0 = $10.50 D 0 = $1 g = 5% per year What is the dividend yield? 1(1.05) / 10.50 = 10% What is the capital gains yield? g = 5% Dividend Capital Gains Yield Yield

/ = 10% What is the capital gains yield. g = 5% Dividend Capital Gains Yield Yield.")

44

Primary vs. Secondary Markets Primary = new-issue market Secondary = existing shares traded among investors Dealers vs. Brokers Dealer: Maintains an inventory Ready to buy or sell at any time Think Used car dealer Broker: Brings buyers and sellers together Think Real estate broker

45

NYSE Merged with Euronext in 2007 NYSE Euronext merged with the American Stock Exchange in 2008 Members (Historically) Buy a trading license (own a seat) Designated market makers, DMMs (formerly known as specialists) Floor brokers

Buy a trading license (own a seat) Designated market makers, DMMs (formerly known as specialists) Floor brokers")

46

Operational goal = attract order flow NYSE DMMs: Assigned broker/dealer Each stock has one assigned DMM All trading in that stock occurs at the DMMs post Trading takes place between customer orders placed with the DMMs and the crowd Crowd = Floor brokers

48

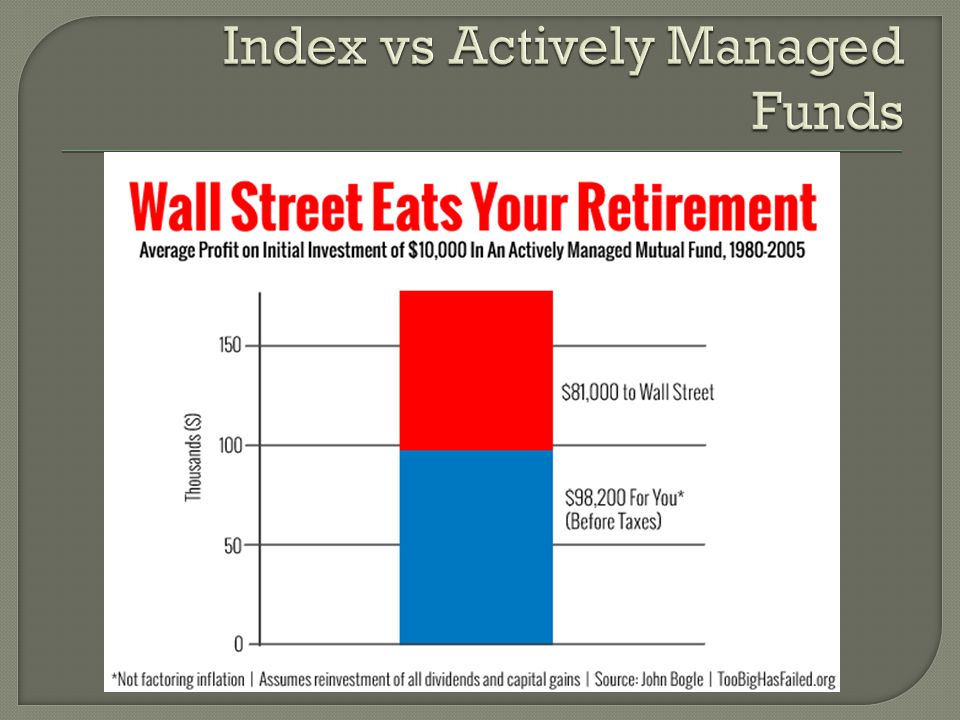

Index funds outperform active funds 80 – 90% of the time.

Similar presentations

>")