Download presentation

Presentation is loading. Please wait.

1

Lessons from the current macroeconomic environment – globally and locally Kenneth Creamer

2

Overview of lecture 1.Introduction 2.Crisis in US 3.Crisis in Europe 4.Impact of global recession on South Africa 5. Economic policy lessons for South Africa 6. Conclusion

3

1.Introduction What is an economic crisis? – It is a period of economic stress and failure in which confidence evaporates, growth rates fall, investment declines, government’s get into debt, banks fail and unemployment rises? The lecture will provide explanations of the causes and dimensions of the current global financial crisis which has been underway since 2009 Even though it is rooted in the developed world there is much we can learn about how economies work by analysing the crisis – we can draw lessons applicable to our own experience Also the ongoing global economic crisis has direct implications for the South African economy it is important to try and understand how the crisis impact on our economy and discuss the policy implications

4

Tale of Two Crises – US and EU US crisis – Private sector financial crisis leading to public sector problems – Failure of regulation of financial system – Fiscal and monetary policy have been used to try and resolve the crisis but there is a strong critique that attempts to re-regulate the financial sector to avoid such crises in future have been inadequate – US has pursued aggressive fiscal and monetary stimulus, but: space for fiscal stimulus is reduced due to huge US govt debt and political discord about raising taxes or cutting spending in future There is not much scope for monetary stimulus as interest rates are close to 0, yet Quantitative Easing is being used to try and reflate the economy

5

EU Crisis European crisis – Government Debt (Public Sector) crisis putting pressure on private banking system – The creation of the common Euro currency has removed the ability of government’s to use monetary policy or exchange rate policy to stimulate the economy and ease fiscal imbalance – Policy makers have not developed consensus on the extent to which European monetary policy can be used to alleviate the crisis, fiscal policy (particularly cutting spending is proving difficult to implement) and efforts to re-regulate the financial system (Basle 3) run the risk of being pro-cyclical i.e. deepening the crisis – Future of EU and Euro at risk as Germany and the ECB are against using monetary stimulus like the US is doing and prefer a route whereby countries undertake fiscal austerity (even giving up sovereignty over fiscal policy)

.")

6

2. US Crisis – regulatory failure A major regulatory change lies at the heart of the current US financial crisis In 1999 the Glass-Steagall Act of 1933 was repealed (New Deal programme after banking crises of the Great Depression late 1920’s early 1930’s) The Glass-Steagall Act had provided for a strict separation of investment banking and commercial banking Under the Glass-Steagall Act depositors money could not be used by commercial banks to invest in high risk securities (this would have been the preserve of investment bank who were taking risk-taking investors money and chasing high return) In a sense it the repeal of the Glass-Steagall Act took away on important regulatory pillar of the process of financial intermediation which matched that risk-averse depositors (with govt-backed deposit insurance) with low risk (lower return) types of investment and disallowed depositors fund to be used in the high risk-high reward “casino” of Wall Street What is financial intermediation? – banks take depositors money and then lend it to investors (i.e. savings are transformed into investments and the banks make a profit as they pay depositors a lower interest rate than the return they make an the investments that they fund i.e. borrowers pay a higher interest rate than depositors receive)

The Glass-Steagall Act had provided for a strict separation of investment banking and commercial banking Under the Glass-Steagall Act depositors money could not be used by commercial banks to invest in high risk securities (this would have been the preserve of investment bank who were taking risk-taking investors money and chasing high return) In a sense it the repeal of the Glass-Steagall Act took away on important regulatory pillar of the process of financial intermediation which matched that risk-averse depositors (with govt-backed deposit insurance) with low risk (lower return) types of investment and disallowed depositors fund to be used in the high risk-high reward casino of Wall Street What is financial intermediation. – banks take depositors money and then lend it to investors (i.e. savings are transformed into investments and the banks make a profit as they pay depositors a lower interest rate than the return they make an the investments that they fund i.e. borrowers pay a higher interest rate than depositors receive).")

7

US Sub-prime crisis In 1999 the year before the repeal of the Glass-Steagall Act sub-prime loans were around 5% of all mortgage lending, in 2008 sub-prime loans were around 30% of all mortgage lending In chasing high returns the less regulated banks started using depositors money to chase the high returns associated with lending people money to buy houses that they probably not be able to afford Sub-prime loan is a housing loan to a person who is due to their poor financial position is going to pay a higher interest rate for the house that they purchase – often with “teaser rates” or with “repayment holiday” clauses Speculators would also buy houses assuming that they could resell these at a higher price in the future (fueled by the “Greenspan put” of very low interest rates “too low for too long” pushing up housing and financial asset prices)

")

8

The securitisation of sub-prime loans Sub-prime loans were securitised i.e. financial companies take 10 000 bonds and rolled them up into a product called “Property Bond Product A” A bank no longer regulated under Glass-Steagall takes depositors money and buys this product “Property Bond Product A” as it offers good returns i.e. the bond repayments of 10 000 families each month as well as the underlying value of the property (which was assumed always to be rising) Furthermore, the rating agencies (S&P, Moodey’s, Fitch, etc) have rated products such as “Property Bond Product A” as a completely safe and secure investment i.e. AAA rated based on the assumption that while one or 10 families may defaults on a bond it is not possible for 10 000 families to default and on the assumption that property prices will always rise Financial companies such as insurance company AIG sold credit default swaps (CSS) which essentially allowed those who wished to bet against the sub-prime billions of $ of insurance if the sub-prim market failed All in the name of “financial innovation”

Furthermore, the rating agencies (S&P, Moodey’s, Fitch, etc) have rated products such as Property Bond Product A as a completely safe and secure investment i.e. AAA rated based on the assumption that while one or 10 families may defaults on a bond it is not possible for families to default and on the assumption that property prices will always rise Financial companies such as insurance company AIG sold credit default swaps (CSS) which essentially allowed those who wished to bet against the sub-prime billions of $ of insurance if the sub-prim market failed All in the name of financial innovation .")

9

Then the wheels feel off…. Families began defaulting on sub-prime bonds and the property bubble burst – property prices began to fall AAA-rated products like “Property Bond Product A” which had been worth hundreds of millions of dollars one day (and had been bought with depositors money were worth almost nothing as the products become illiquid and cannot be sold “toxic”) The US government had to bail out banks that had lost depositors money (or more banks would close like Lehman Brothers) The US government had to bail out the insurance companies (like AIG) that had miscalculated risk and had to pay out billions of $ on credit default swaps (CDS)

The US government had to bail out banks that had lost depositors money (or more banks would close like Lehman Brothers) The US government had to bail out the insurance companies (like AIG) that had miscalculated risk and had to pay out billions of $ on credit default swaps (CDS).")

10

Recession stalks the US Dangers in US - Unemployment is high, confidence is low and government debt is high There is a danger that the US government does not have the instruments to turn the economy around as both fiscal and monetary instruments are appearing impotent – Fiscal policy – govt is heavily indebted and is running a large budget deficit with no political consensus on whether to raise taxes or cut spending (hence the downgrading of US bonds by S&P earlier in the year) – Monetary policy – interest rates are very low and cannot go much lower, resulting in the risk of deflation deflation 0 bound) therefore the Fed is using non-interest rate instruments such as Quantitative Easing (QE) i.e. huge increases in the money supply to try and inject some inflation and liquidity into the system

11

Dangers of Deflation There is the danger of a deflation trap e.g. where nominal interest rates are zero and there is deflation then the real interest rate is positive, – r = i – π (real interest rate) and i ≥ 0 – If i = 0 then r = – π – If π < 0 (deflation) then minimum real rate is positive and r rises as prices fall further (further deflation) Demand channel: If there is continued weak demand and deflation is fueled further this will lead to a rise in the real interest rate (the wrong impulse as it results in further suppression of demand) Financial channel: Deflation means that bond payments go up in real terms (as in nominal terms they are fixed but price and wages are falling) e.g. if you owe R1-million but your wages are falling this leads to increased likelihood of default and banking crisis Consumption channel: Deflation slows consumptions as delayed consumption will be rewarded with lower prices

and i ≥ 0 – If i = 0 then r = – π – If π < 0 (deflation) then minimum real rate is positive and r rises as prices fall further (further deflation) Demand channel: If there is continued weak demand and deflation is fueled further this will lead to a rise in the real interest rate (the wrong impulse as it results in further suppression of demand) Financial channel: Deflation means that bond payments go up in real terms (as in nominal terms they are fixed but price and wages are falling) e.g. if you owe R1-million but your wages are falling this leads to increased likelihood of default and banking crisis Consumption channel: Deflation slows consumptions as delayed consumption will be rewarded with lower prices.")

12

3.European Crisis At the root of the crisis – government borrowing by countries such as Greece and Italy Expenditure = Tax revenue + Borrowings Borrowing = Expenditure – Tax Revenue In order to borrow govt’s sell bonds e.g. govt sells a bond for Euro 1 bn “follow the money” – this means govt is given Euro 1 bn and makes a commitment to pay this bond back with interest NB – the amount of interest you must pay depends on how risky you are perceived to be by lenders (what is important here is often subjective and based on herd mentality – behavioural vs rational economics)

.")

13

European bond market Greece and Italy and increasingly France are beginning to be perceived as more risky so there cost of borrowing is rising Language of the bond market – “the yield spreads are rising” i.e. the amount of interest that they will have to pay on the Euro 1 bn that Greece is borrowing will be much more than the interest rate that Germany has to pay (as Germany is perceived to be less risky) The result for Greece is that its fiscal position appears to be shifting from precarious to unsustainable i.e. there is a risk that it will not be able to re-pay its debt and this results in a vicious circle where the risk of default pushes up interest rates and makes it even harder for Greece to pay its debts

The result for Greece is that its fiscal position appears to be shifting from precarious to unsustainable i.e. there is a risk that it will not be able to re-pay its debt and this results in a vicious circle where the risk of default pushes up interest rates and makes it even harder for Greece to pay its debts.")

14

The Market for Greek Debt If supply rises of something prices come down (Greeks need to borrow) If demand falls for something then prices come down (perceptions of Greek risk rising) As Greek position worsens they may wish to sell a bond for Euro 1bn Originally the could have sold this bond (a commitment to repay Euro 1bn in 10 years) for Euro 950 million [case 1] During the crisis as Supply is up and Demand is down they may only be able to sell the bond for Euro 700 million) [case 2] The bond yield, interest rate or cost of borrowing is calculated as follows: – Case 1 (1 + Interest Rate) 10 = 1000/950 => Interest Rate = (1000/950) 1/10 – 1 = 0.51% per year – Case 2 (1 + Interest Rate) 10 = 1000/700 => Interest Rate = (1000/700) 1/10 – 1 = 3.63% per year So the bonds spread between Case 1 and Case 2 is 3.12% or 312 basis points The Greek cost of borrowing has risen – what are the implications?

![The Market for Greek Debt If supply rises of something prices come down (Greeks need to borrow) If demand falls for something then prices come down (perceptions of Greek risk rising) As Greek position worsens they may wish to sell a bond for Euro 1bn Originally the could have sold this bond (a commitment to repay Euro 1bn in 10 years) for Euro 950 million [case 1] During the crisis as Supply is up and Demand is down they may only be able to sell the bond for Euro 700 million) [case 2] The bond yield, interest rate or cost of borrowing is calculated as follows: – Case 1 (1 + Interest Rate) 10 = 1000/950 => Interest Rate = (1000/950) 1/10 – 1 = 0.51% per year – Case 2 (1 + Interest Rate) 10 = 1000/700 => Interest Rate = (1000/700) 1/10 – 1 = 3.63% per year So the bonds spread between Case 1 and Case 2 is 3.12% or 312 basis points The Greek cost of borrowing has risen – what are the implications](http://images.slideplayer.com/36/10608573/slides/slide_14.jpg "The Market for Greek Debt If supply rises of something prices come down (Greeks need to borrow) If demand falls for something then prices come down (perceptions of Greek risk rising) As Greek position worsens they may wish to sell a bond for Euro 1bn Originally the could have sold this bond (a commitment to repay Euro 1bn in 10 years) for Euro 950 million [case 1] During the crisis as Supply is up and Demand is down they may only be able to sell the bond for Euro 700 million) [case 2] The bond yield, interest rate or cost of borrowing is calculated as follows: – Case 1 (1 + Interest Rate) 10 = 1000/950 => Interest Rate = (1000/950) 1/10 – 1 = 0.51% per year – Case 2 (1 + Interest Rate) 10 = 1000/700 => Interest Rate = (1000/700) 1/10 – 1 = 3.63% per year So the bonds spread between Case 1 and Case 2 is 3.12% or 312 basis points The Greek cost of borrowing has risen – what are the implications")

15

Budget or fiscal implications Rising interest rates crowds out other spending As interest rates rises a higher an higher portion of tax revenues have to paid in interest payments Year 1 Tax (950) + Borrowing (50) = Spending (1000) (comprising salaries and consumption 750 + investment 240 + interest repayments 10) Year 2 (after interest rates borrowing costs rise) Tax (950) + Borrowing (50) = Spending (1000) (comprising salaries and consumption 750 + investment 210 + interest repayments 40) Notes: – In year 2 interest payments have risen sharply “crowding-out” investments (as salaries and consumption are typically more difficult to reduce) – If interest rates and interest rates continue to rise then country may enter a debt trap where money is borrowed just to pay short-term debts (and is not invested in growth generating projects which would push up revenue and make it possible to repay debts)

+ Borrowing (50) = Spending (1000) (comprising salaries and consumption investment interest repayments 10) Year 2 (after interest rates borrowing costs rise) Tax (950) + Borrowing (50) = Spending (1000) (comprising salaries and consumption investment interest repayments 40) Notes: – In year 2 interest payments have risen sharply crowding-out investments (as salaries and consumption are typically more difficult to reduce) – If interest rates and interest rates continue to rise then country may enter a debt trap where money is borrowed just to pay short-term debts (and is not invested in growth generating projects which would push up revenue and make it possible to repay debts)")

16

Europe’s perfect storm Greek’s have a low income tax compliance putting further pressure on fiscus The move to the Euro has resulted in: – A move from high inflation to low inflation which created the climate for a property bubble – Euro has meant that Greece and other countries have lost access to their monetary and currency instruments

17

Housing Bubble Moving from high inflation to low inflation e.g. countries like Greece, Italy and Spain - money illusion in buying houses Housing bubble occurs as property prices are perceived to be lower (due to lower nominal payments, but over time the real payments are higher due to lower inflation) (see next slide) As a result there is an investment boom in housing stock and then when it is revealed that people cannot afford housing then housing price fall and housing developments are left unfinished This puts further pressure on economy and banks as defaults rise

(see next slide) As a result there is an investment boom in housing stock and then when it is revealed that people cannot afford housing then housing price fall and housing developments are left unfinished This puts further pressure on economy and banks as defaults rise.")

18

Money illusion – moving from high to low inflation High Inflation Case: Initial bond payment is Euro 10000 but with inflation at 25% p.a. the real bond payments rapidly decrease over 20 years Low Inflation Case: Initial bond payment is Euro 1000 but but with inflation at 5% p.a. the real bond payments are comparatively higher over the 20 year life of the bond Due to misperception that the low inflation case is cheaper (Euro 1000) than the high inflation case (Euro 10 000) a housing bubble develops Current debate in policy about the role of monetary policy or macro prudential policy in avoiding the development of asset bubbles e.g. push up taxes / transfer duties on houses when you move from high inflation to low inflation (e.g. Singapore)

than the high inflation case (Euro ) a housing bubble develops Current debate in policy about the role of monetary policy or macro prudential policy in avoiding the development of asset bubbles e.g. push up taxes / transfer duties on houses when you move from high inflation to low inflation (e.g. Singapore).")

19

Loss of monetary and exchange rate instruments Could get out of debt by cutting interest rates or devaluing the currency – cannot be done in Euro area as ECB controls interest rate and there is a single currency Real exchange rate is given by RE = P*e/P, can’t influence P* (foreign inflation) or the nominal exchange rate (e)(the Euro) therefore the must try to reduce P (domestic prices) to devalue the real exchange rate to increase “competitiveness” – but this is politically very difficult e.g. reducing public servants salaries

20

Likely results of European Crisis Euro introduced to avoid currency volatility and currency speculators Now bond markets are exerting discipline and causing imbalances Euro will collapse (countries will leave) or Countries will lose fiscal policy independence as well (e.g. budgets will have to be passed by pan- European govt in Brussels with the aim of preventing too much borrowing or allowing unsustainable spending)

.")

21

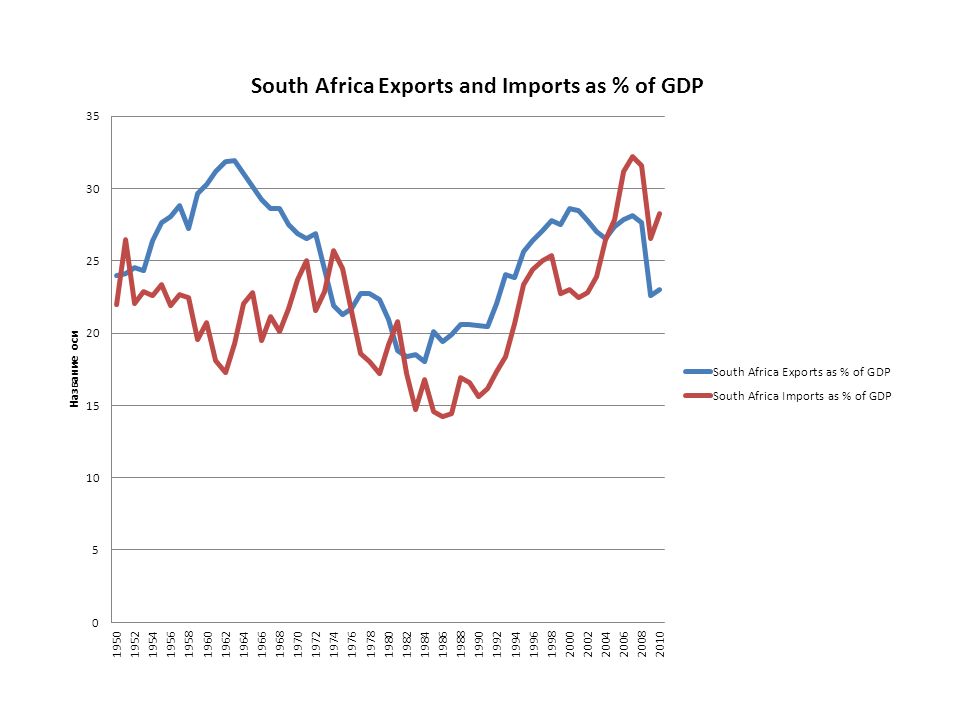

4.Impact of recession on South Africa South Africa is a relatively open economy so when there is an economic crisis in the US and EU this has negative economic consequences for SA Growth is effected, exports are effected, capital flows are effected See diagram showing long run trends from 1950 to 2010 – 1994 represents a clear opening up of the SA economy See recent trends effected by the global recession – Exports decline 2008-2009 as growth in our export markets slows down – Imports decline as growth in SA slows down and imports move with growth – Capital inflows drop sharply – as there is a flight from risk (SA has used this inflows of foreign savings to fund growth enhancing capital projects (investment) beyond our domestic savings pool, but there is an argument that the capital flows can be destabilising – When growth slows this impact on employment in the SA economy with the global recession costing us around 1 million jobs between 2008Q4 and 2010Q4

beyond our domestic savings pool, but there is an argument that the capital flows can be destabilising – When growth slows this impact on employment in the SA economy with the global recession costing us around 1 million jobs between 2008Q4 and 2010Q4")

25

Employment since 2008

26

5.Economic policy lessons for SA From the US crisis – keep appropriate regulation of the financial sector – In SA we have had exchange controls on SA citizens and companies and prudential regulations on the banks (versus ideological position of maximum freedom minimum regulation a la Greenspan) From EU crisis – avoid getting into fiscal distress – In SA we have avoided debt trap (see diagram that we are relatively strong in this regard) – Recently increased budget deficits have meant that govt debt has been on the rise (mostly Rand denominated)

From EU crisis – avoid getting into fiscal distress – In SA we have avoided debt trap (see diagram that we are relatively strong in this regard) – Recently increased budget deficits have meant that govt debt has been on the rise (mostly Rand denominated)")

27

Gross government debt as a % of GDP

28

Developmental state and open economy Benefits of an open economy include foreign funding of job creating infrastructure and private investment, exports provide larger markets and huge growth potential, imports bring in technology and oil, etc. But an open economy is subject to shocks caused elsewhere The developmental state will experience these shocks and cannot make our economy recession proof, but it can look to ways of generating domestic investment in growth and employment generating projects: – creating greater investor certainty, – guiding investment into new sectors (e.g. renewable energy, road, rail and water infrastructure) lengthen the planning horizon in the domestic economy Capital expansion must be done at a sustainable pace so as not to create a fiscal crisis (often private sector finance can be used instead of govt finances and risk e.g. in mining private finance should be used to expand our mining output and create employment albeit in an efficiently regulated manner) If we over extend the fiscus this will requires sharp cut-backs in spending which will have negative social consequences for education and health, teachers and nurses salaries will have to be cut, etc. and a legacy of unfinished projects and unfulfilled promises

lengthen the planning horizon in the domestic economy Capital expansion must be done at a sustainable pace so as not to create a fiscal crisis (often private sector finance can be used instead of govt finances and risk e.g. in mining private finance should be used to expand our mining output and create employment albeit in an efficiently regulated manner) If we over extend the fiscus this will requires sharp cut-backs in spending which will have negative social consequences for education and health, teachers and nurses salaries will have to be cut, etc. and a legacy of unfinished projects and unfulfilled promises.")

29

Prioritise employment creating growth Go for growth difference between 3% growth and 7% growth over 20 years is that the GDP will be more than 2 times larger after 20 years i.e. 1.8 times larger at 3% growth vs 3.9 times larger at 7% growth It is only growth that can generate employment – but growth is necessary but not sufficient But govt policy can assist in shaping the growth to be more employment creating and sustainable growth: – Industrial policy encourages employment generating sectors – Planning encourages changes in infrastructure provision, moves toward new form of energy, etc. – Local content in procurement has vast potential to increase the number of people employed as a result of infrastructure expansion Trade policy to open up exports markets to strong emerging economies and Africa (see slides of potential here)

.")

30

Emerging economies to be key drivers of world growth…

31

Africa’s economic growth accelerated after 2000, making it the world’s third-fastest growing region

32

6. Conclusion In a sense this is an introductory lecture Firstly, a detailed discussion on the current global economic crisis Secondly, in looking at how we should respond in this climate this lecture has offered a foretaste, or a bringing together, of many of the issues that will be dealt with in greater detail during the days ahead in this Political School, such as: – Fiscal and monetary policy – Industrial and minerals policy – Trade policy – Growth and employment policies

Similar presentations

: The total quantity of aggregate output, or real GDP, that all buyers in an.>")

: The quantity of real GDP demanded (total quantity of G&S that all buyers in an economy want to buy) at different price.>")