Download presentation

Presentation is loading. Please wait.

1

Johannes Guigard Chartered Accountant Italy and ACCA

UNIVERSITY OF MOSCOW October General overview on the European Accounting and Auditing legislation Johannes Guigard Chartered Accountant Italy and ACCA

2

Foundation of the European Union (EU)

The EU is a family of democratic European countries, committed to working together for peace and prosperity The historical roots of the EU lie in the WWII. The idea of European integration conceived to prevent such killing and destruction from ever happening again was proposed by the French Foreign Affaires Minister Robert Schuman on 9 May 1950, EU"birthday“, now annually celebrated as Europe Day. Started off with just six countries: Belgium, Germany, France, Italy, Luxembourg and the Netherlands. Denmark, Ireland and the United Kingdom joined in 1973, Greece in 1981, Spain and Portugal in 1986, Austria, Finland and Sweden in In 2004/7 with the enlargement 12 new countries joined. EU is now made of 27 Member States

3

Basic Data* 493 million citizens EU (Russia 143 Million)

Some data*: 493 million citizens EU (Russia 143 Million) Area: 4,4 Million Square Km (Russia 17,1 Million) 1.300 Directives 23 million SMEs, of which 91% are micro-enterprises 7.365 domestic companies ^ 1.400 foreign companies Market capitalisation Euro billion US figures: 6.000 domestic and 850 foreign ( EU) Market capitalisation USD billion * ^ CESR report on enforcement - November 2007

Area: 4,4 Million Square Km (Russia 17,1 Million) Directives. 23 million SMEs, of which 91% are micro-enterprises domestic companies ^ foreign companies. Market capitalisation Euro billion. US figures: domestic and 850 foreign ( EU) Market capitalisation USD billion. *2005 ^ CESR report on enforcement - November")

4

The world and the European Union

Europe’s role Economy: major world power Political and diplomatic role? EU and USA Share same values Competition in trade and technology EU and Mediterranean countries Creation of a free-trade area by 2010 Economic and trading relations Partnership in social and cultural fields EU and Russia Partnership and Cooperation Agreement future “Common Economic Space”:

5

Legal foundations of the European Union (1/2)

Treaty of Paris (1951) European Coal and Steel Community The 2 WWII commodities pooled under an Authority Treaties of Rome (1957) EEC European Economic Community Euratom The nuclear energy treaty The European Monetary System (1979) Currencies fluctuations limited % Single European Act (1987) Foundations of the Single Market Treaty of Maastricht (1992) Plan for EMU’s creation The Monetary Union Upgrade from EEC to European Community-> towards European Union Introduction of the Subsidiarity Principle

European Coal and Steel Community The 2 WWII commodities. pooled under an Authority. Treaties of Rome (1957) EEC European Economic Community. Euratom The nuclear energy treaty. The European Monetary System (1979) Currencies fluctuations limited % Single European Act (1987) Foundations of the Single Market. Treaty of Maastricht (1992) Plan for EMU’s creation The Monetary Union. Upgrade from EEC to European Community-> towards European Union. Introduction of the Subsidiarity Principle.")

6

Legal foundations of the European Union (2/2)

Schengen Agreement (1990) Abolishes borders and checks on persons within many EU countries Introduces a common policy on visas The Single Market (1993) No borders between Members States Treaty of Amsterdam (1997) Stability and growth pact: budget discipline by EU countries on deficits Treaty of Nice (2001) EU Charter of Fundamental Rights, in preparation for the Enlargement Introduction of Euro 1 January January February 2002 Treaty of Lisbon (2007) Change in proposal and adoption of EU legislation.

Abolishes borders and checks on persons within many EU countries. Introduces a common policy on visas. The Single Market (1993) No borders between Members States. Treaty of Amsterdam (1997) Stability and growth pact: budget discipline by EU countries on deficits. Treaty of Nice (2001) EU Charter of Fundamental Rights, in preparation for the Enlargement. Introduction of Euro. 1 January January February Treaty of Lisbon (2007) Change in proposal and adoption of EU legislation.")

7

The European Constitution

2004: Agreement for a new Constitution 2005: Rejected by FRANCE and HOLLAND 2008 Rejected by IRELAND Where will we end up? PLAN C anyone?

8

Agreements with other European Countries

WIPO countries (Norway, Liechtenstein, Iceland) are part of Internal Market EFTA Member Switzerland has agreement Other countries are in the process of asking for membership

are part of Internal Market. EFTA Member Switzerland has agreement. Other countries are in the process of asking for membership.")

9

Treaties of Rome 1957 EEC European Economic Community EURATOM

A common market in a wide range of goods and services EURATOM GOALS OF THE TREATIES → free movement of goods, people, services, capitals → closer relation among the Member States → Increase in stability → Continuous and balanced expansion → Ensuring fair competition between businesses → Protecting consumer interests

10

Treaty of Maastricht 1992 The principle of subsidiarity

EU and its institutions act ONLY IF action is more effective at EU level than at national level: limited EU interference in its citizens’ daily life European Monetary Union by 1999 Maastricht parameters - Budget deficit ≤ 3% of Gross domestic product - public borrowing ≤ 60% of GDP Rights of the EU’s citizens

11

The EU’s Internal Market

Based on the principle of an open market economy with free competition Freedom of establishment free exchange of: Goods NO BORDERS AMONG MEMBER STATES Capitals SIMILAR FINANCIAL RULES People ANYONE CAN SETTLE ANYWHERE IN EU Services STILL TO BE ACHIEVED

12

The Institutional Framework

EU is more than a confederation of countries but not a Federal State The Council of Ministers The European Parliament The Commission The Economic and Social Committee The Court of Justice

13

The Council of Ministers (1/2)

It’s the highest level policymaking body of the EU Brings together all EU countries’ Presidents and Prime Ministers PLUS EU Commission President Shares with the European Parliament legislative power responsibility for the budget Concludes international agreements negotiated by the Commission

14

The Council of Ministers (2/2)

Each country in turn presides over the council for a 6-month period [EU Rotating Presidency] Decisions taken unanimously or by qualified majority Meets in principle 4 times a year

15

European Parliament (1/2)

Elected body, at universal suffrage every 5 years: next elections JUNE 2009 Represents the EU’s citizens Takes part in the legislative process Debates and adopts with Council the EU Budget proposed by the Commission By 2/3 majority may censure and therefore dismiss the Commission

16

European Parliament (2/2)

Located in Strasbourg (plenary sessions) and Brussels Share of Legislative power with the Council 3 different procedures cooperation procedure: gives its opinion on draft Directives and Regulations proposed by the EU assent procedure: Parliament gives its assent to int’l agreements negotiated by the Commission co-decision procedure

and Brussels. Share of Legislative power with the Council. 3 different procedures. cooperation procedure: gives its opinion on draft Directives and Regulations proposed by the EU. assent procedure: Parliament gives its assent to int’l agreements negotiated by the Commission. co-decision procedure.")

17

EU Commission EU’s executive arm

It has a complete political independence It does not take instructions from any Member State Government It’s the only institution that has the right to propose new EU legislation It’s the guardian of the Treaties It’s assisted by 36 Directorates General (DGs) Located in Brussels and Luxembourg

Located in Brussels and Luxembourg.")

18

The European Economic and Social Committee

It’s an advisory body that gives its opinion on EU initiatives Assists EU Commission in adopting detailed technical implementing measures Council and Commission consults EESC in taking decisions in policy areas covered by EC and Euratom treaties Members represent the various interest groups that collectively make up “organised civil society”. Appointed by Council for 4 years.

19

The Court of Justice Ensures that EU law is complied with

Ensures treaties’ interpretation and application Makes void EU legislation’s lawfulness Checks whether EU legislation respects the fundamental rights Made up of one judge by each EU country + 8 Advocates general Each judge is appointed for 6 years Headquarters: Luxembourg

20

The European Central Bank

Manages the European monetary policy Manages the €: sets interest rates and intervention policy Lead by a President and an Executive Board Headquartes: Frankfurt

21

Other institutions Court of auditors European Investment Bank

Committee of the regions …and many others…

22

European Institutional Renewal 2009

1 Jan 2009 The new Constitution was proposing a full time President and a Foreign Policy Chief … but… all this is now postponed In June 2009 the election of new EU Parliament In November 2009 appointment of the new Commission

23

Background to EU Legislation

Primary EU legislation Member States delegate some of their national sovereignty to the Institutions who represents both the national and collective interest by signing Treaties, which constitute the Primary Legislation Secondary EU legislation: Regulations Directives Decisions “Soft law”: (form of guidance) Interpretative Communications Recommendations

Interpretative Communications. Recommendations.")

24

Background to EU Legislation

Comitology A simplified way to amend legislation on technical aspects (non-essential elements) based on a delegation of executive powers from Council to Commission : COMMITTEE OF PUBLIC SERVANTS Member States represented in a Committee chaired by the Commission Parliament informed Comitology with scrutiny: more powers for EP Subsidiarity

based on a delegation of executive powers from Council to Commission : COMMITTEE OF PUBLIC SERVANTS. Member States represented in a Committee chaired by the Commission. Parliament informed. Comitology with scrutiny: more powers for EP. Subsidiarity.")

25

The co-decision procedure (1/2)

Established by Maastricht Treaty Article 251 of EC Treaty Legislative procedure par excellence following adoption of European Constitution Principle of Parity: neither institution (EP or Council) may adopt legislation without the other’s assent Adopted for issues such as Internal Market, education, research, environment, consumer protection, health, culture, free movement of workers

may adopt legislation without the other’s assent. Adopted for issues such as Internal Market, education, research, environment, consumer protection, health, culture, free movement of workers.")

26

The co-decision procedure (2/2)

Commission proposes (right of initiative), Parliament and Council decide jointly. Parliament (1st reading) and Council agree on Commission proposal: it is approved if disagreement, EP (2nd reading) can either accept Council’s (common) position, or reject or amend it by a majority of its members, if Council cannot accept EP’s amendments: conciliation meeting. If agreement found in conciliation, proposal approved. If no agreement, proposal deemed not to have been adopted.

, Parliament and Council decide jointly. Parliament (1st reading) and Council agree on Commission proposal: it is approved. if disagreement, EP (2nd reading) can either accept Council’s (common) position, or reject or amend it by a majority of its members, if Council cannot accept EP’s amendments: conciliation meeting. If agreement found in conciliation, proposal approved. If no agreement, proposal deemed not to have been adopted.")

27

Lisbon Treaty 13 December 2007

Aims at providing EU with streamlined institutions and optimised working methods after the Enlargement To be ratified by Member States by beginning of 2009 Changes to proposal and adoption of EU legislation: Election of President of the EU Council by qualified majority for 2,5 years, renewable once Election of President of EU Commission by simple majority of MEPs following a proposal of the Council Creation of a post of EU Foreign Minister Increased number of fields covered by qualified majority voted by the Council

28

Lisbon Treaty 13 December 2007

Clarification of division of powers Exclusive EU competences in the financial sphere: Euro Competition policy Monetary policy Common commercial policy Member States cannot take measures inconsistent with: Existing liberalization of movement of capitals Damaging of existing financial instruments Competence shared with member States Internal market limited to the following Environment R & D Consumer policy

29

Lisbon Treaty 13 December 2007

European Parliament will have greater legislative and budgetary powers Member States Parliaments will have a role in ensuring that the EU complies with the principle of subsidiarity EU ‘s powers on coordination of economic, industrial and employment policies of the Member States remain the same

30

EU Legislation: the DIRECTIVES

One of the binding legislations of EU Offers OPTIONS to Member States Indicate to the Member States what they have to implement. How they do it’s up to them. The EU Commission supervises GOLD PLATING exercise by Member States, adding accomplishments, but harmonisation makes it difficult to detect.

31

EU Legislation: the REGULATIONS

Have to be implemented into the national legislation of each member State as it is No amendment and no delay are accepted In case of delayed implementation it is nevertheless applicable in the Member State: anyone can ask for ruling at the European Court of Justice, just in case

32

Eu Legislation: the DECISIONS

Decisions are made by the Court on all issues brought to its attention Main interventions are on the areas of: 1.- Taxes 2.- Antitrust Ensures correct application of treaties and of secondary legislation

33

Definition of Recommendation (Article 249/EC)

It’s one of two kinds of non-binding acts as per Treaty of Rome , while Regulations, Directives and Decisions are compulsory No legal force but negotiated and voted according to the appropriate procedure Though without legal force, has political weight Instrument of indirect action aiming at preparation of legislation in Member States, differing from the Directive only by the absence of obligatory power.

34

The Lisbon strategy 2000 (1/2)

AIMS: EU economy expected to be by 2010: a) The most competitive b) The most dynamic IN THE WORLD c) Knowledge based a) Sustainable growth WITH b) more and better jobs c) greater social cohesion a) globalisation REASONS b) technological rivolution

The most competitive. b) The most dynamic IN THE WORLD. c) Knowledge based. a) Sustainable growth. WITH b) more and better jobs. c) greater social cohesion. a) globalisation. REASONS b) technological rivolution.")

35

The Lisbon strategy 2000 (2/2)

Major targets Growth 3% per annum Employment rate 70% 3% GDP to be spent on R&D 20 MILLION new jobs to be created European research area (to link universities) Encourage students (Socrates and other prgms) TOO Many other targets (28+120) Monitoring the development of the strategy Once a year: spring economic summit EU COUNCIL OF MINISTERS

Encourage students (Socrates and other prgms) TOO Many other targets (28+120) Monitoring the development of the strategy. Once a year: spring economic summit EU COUNCIL OF MINISTERS.")

36

The two EU Action Plans The two main pillars of EU legislation are:

Financial Services Action Plan, Capital Markets regulation Lamfalussy approach in four steps Company Law Action Plan 2003 – 2010 Review of co. Law Directives Corporate Governance

37

How to Reach a European Single Financial Market?

Not only: Identify problems to be addressed Coming up with legislative solutions But mainly: Look at the most effective way of ensuring that those solutions actually work Deliver the results everybody want to see

38

Towards Single Financial European Market

Consultation and Transparency in the legislative process all documents out for consultation active role of the professions involved Respond quickly and flexibly to market changes Convergence and Cooperation among European regulators Working together on day by day basis to develop common understanding and approaches Effective Implementation and Enforcement across Member States Look beyond EU: cooperate internationally

39

Transparency in legislative process

Transparency is the core of the European Legislative Process Trust Loyalty It is an investment in Investors need to be able to invest across borders easily and with confidence Not only WHAT information is disclosed Transparency is But also HOW it is disclosed that matters

40

Financial Services Action Plan

42 PLUS measures in order to create a) Integrated European Financial Market b) The break down of barriers 1 Currency 1 Capital Market 1 Set of Financial Rules … and….

Integrated European Financial Market. b) The break down of barriers. 1 Currency. 1 Capital Market. 1 Set of Financial Rules … and….")

41

Financial Services Action Plan

… and… Objective, accurate, comparable financial information throughout the EU Fighting market abuse Efficient fast track decision making

42

Financial Services Action Plan

Amongst other measures: IFRS adoption for all listed Co on EU markets -introduction of fair value - modernisation - update for company law issues Money laundering Directive (3 rd) Revision investment services directive on protection of investors Taxation of savings income Take-over bids directive

Revision investment services directive on protection of investors. Taxation of savings income. Take-over bids directive.")

43

Financial Services Action Plan

Markets in financial instruments Directive MiFID Market abuse Directive Against manipulation of markets Prospectus Directive Detailed document to be filed to the Registrar of Companies before offering the shares to the public 9 Statutory auditor Directive Quality assurance -> UE Recommendation - Auditors’ independence - review of 8 th Directive 10. Transparency - frequency and contents of interim reporting by listed companies

44

EU Company Law legislation (1/2)

Key Political objectives Facilitate participation of shareholders to corporate life Vote in absentia Right to table resolutions Strengthening shareholders rights and third parties protection Modern company law making Efficiency and competition Facilitate cross-border activities Participate to general meetings via electronic means Co web used to inform shareholders and publish info

45

EU Company Law legislation (2/2)

Modern company law making flexible, adaptive instruments principle based, not rule based legislation disclosure, instead of substantive regulation encourage use of modern technology use of company’s website central electronic filing system per Member State connection of Member States archives access to info in advance of AGM

46

Company Law Action Plan

Modernising the Board of Directors Coordination of Corporate Governance in Member States Corporate restructuring and mobility European private Company European Cooperative Society

47

Next step … let’s get into more detail on the Financial Reporting and Auditing…

48

Companies interested in the subject

Listed Non-listed Small medium size entities Micro entities Banks Insurances Plus, in certain cases: 1.- public sector 2.- partnerships 3.- professionals

49

EU Legislation on Financial Reporting

Fourth and Seventh Directives (1978 and 1983) Directive on Banks and other financial institutions Directive on Insurance undertakings 2001 Fair Value Directive 2002 IAS Regulation 2003 Modernisation of the Accounting Directives Adoption of certain IAS + IFRSs in accordance with the IAS Regulation June 2006: Amendments to the 4th and 7th Directives June 2006: Statutory Audit Directive

Directive on Banks and other financial institutions. Directive on Insurance undertakings Fair Value Directive IAS Regulation Modernisation of the Accounting Directives. Adoption of certain IAS + IFRSs in accordance with the IAS Regulation. June 2006: Amendments to the 4th and 7th Directives. June 2006: Statutory Audit Directive.")

50

EU Legislation on Financial Reporting and Auditing

National “auditable” entities 4th, 7th and Statutory Audit Directives Small companies National companies with statutory audit Other legal forms Transparency Prospectus Directives and IAS Regulation Listed companies Specific sector Directives on financial institutions Foreign listed

51

IFRS – Changing Accounting

52

EU Developments – IAS Regulation 1606/2002

Objective: harmonise financial information Scope: Requirement for EU listed companies to use endorsed IAS in their consolidated accounts from 2005 Optional: Consolidated accounts of unlisted companies Individual accounts Main issues: High quality, global, principle based standards Comprehensive set of IFRS for Europe, identical to full IFRS Convergence IFRS and US GAAP

53

The Endorsement Process

Objective of the EU process is to get political and legal endorsement of IFRS Endorsed IAS/IFRS and SIC/IFRIC published in full in all official languages of the Community in the EU Official Journal and available on the EC website New IFRS and IFRIC endorsed as they go along Criteria IFRS not contrary to “true and fair view” principle of Accounting Directives IFRS must be conducive to public good (competitiveness and convergence) IFRS must be understandable, relevant, reliable and comparable

IFRS must be understandable, relevant, reliable and comparable.")

54

The Endorsement Process

IASB European Commission European Parliament EFRAG SARG Council ARC Accounting Regulatory Committee Interest groups

55

IFRS endorsement Status

Endorsed IFRS Full FRS ? Timing differences: if delayed -> major uncertainties Non endorsement create major problems Therefore it is essential to monitor IASB from “inside” Endorsed IFRS: all, except: some provisions of IAS 39 Certain provisions of IAS 39 related to hedge accounting are carved out Discussions between the IASB and the European Business Forum IFRS 8 on segment reporting accepted after long debate by EP Framework implementation under scrutiny

56

Implications of partial endorsement

SEC drops reconciliation statement requirement ONLY for FULL IFRS Cost to European companies: Extra disclosures to explain differences Information system changes implications Cost to credibility of global standards: Precedent setting Cost to global capital markets Limiting convergence IFRS and US GAAP

57

Why Does Endorsement Take Time?

ARC opinion IASB approval EFRAG advice Translations EU review EU-Parliament SARG advice EU Institutions Endorsed by EC

58

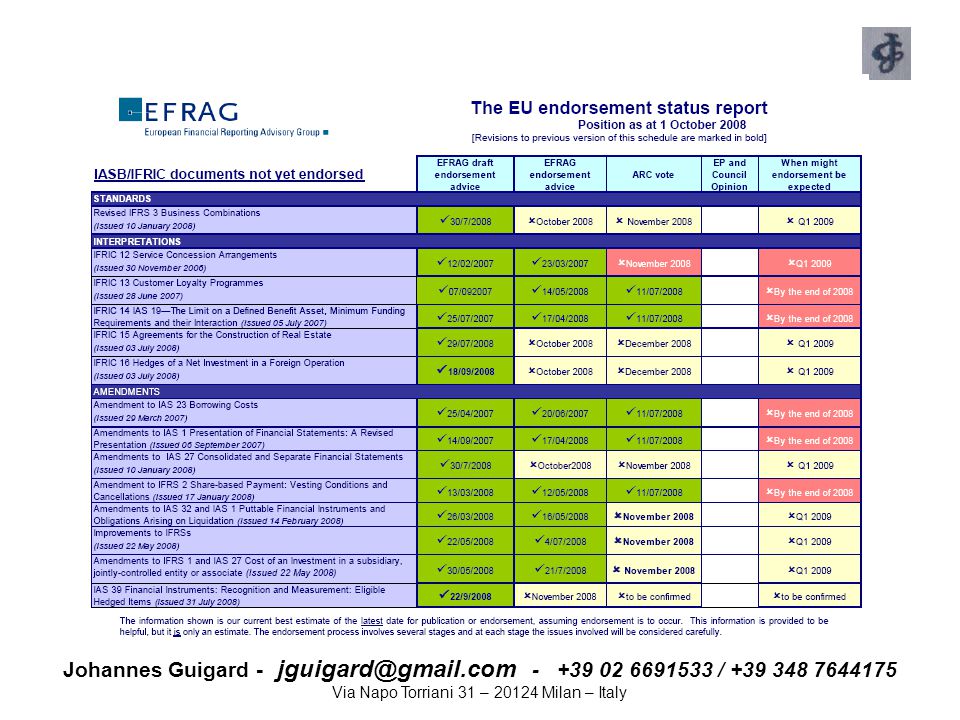

EFRAG Endorsement Status Report as at 1 October 2008

All IFRS (1 TO 8) AND ALL IFRIC Interpretations (1,2, 4 to 11) Existant standards and interpretations as at 1 March 2002, other than IAS 32 and 39 and related interpretations. (In other words, IASs 1, 2, 7, 8, 10, 11, 12, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 26, 27, 28, 29, 30, 31, 33, 34, 35, 36, 37, 38, 40 and 41; and SIC 1, 2, 3, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 18, 19, 20, 21, 22, 23, 24, 25, 27, 28, 29, 30, 31, 32 and 33.)

AND ALL IFRIC Interpretations (1,2, 4 to 11) Existant standards and interpretations as at 1 March 2002, other than IAS 32 and 39 and related interpretations. (In other words, IASs 1, 2, 7, 8, 10, 11, 12, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 26, 27, 28, 29, 30, 31, 33, 34, 35, 36, 37, 38, 40 and 41; and SIC 1, 2, 3, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 18, 19, 20, 21, 22, 23, 24, 25, 27, 28, 29, 30, 31, 32 and 33.)")

60

Institutional Cooperation

IASB – sets standards EFRAG – influence the international standard setting process from an European perspective and advises on technical acceptability SARG – reviews EFRAG due process ARC – considers political acceptability EP – endorsement advice, comitology with scrutiny EC – formally endorses IFRS EC Roundtable on consistent application of IFRS within the EU CESR and other enforcement bodies such as review panels - enforces

61

EFRAG – European Financial Reporting Advisory Group

Set up in 2001 Private sector organisation Founding fathers: FEE with 9 European Stakeholders organisations Main objectives: Proactive contribution to the work of IASB and IFRIC: Contribute to and influence IASB standard setting process BEFORE a standard is issued Endorsement advice to the Commission Technical assessment of IFRS and IFRIC interpretation AFTER they are issued Advising on changes to the EU Accounting Directives PAAinE (Proactive Accounting Activities in Europe) with national standard setters Governance structure EFRAG reviewed aiming for faster integration with National Standard Setters: “reinforcing structure” paper in 2008 Supplies the resources to influence IASB, balancing the US lobby

with national standard setters. Governance structure EFRAG reviewed aiming for faster integration with National Standard Setters: reinforcing structure paper in Supplies the resources to influence IASB, balancing the US lobby.")

62

EFRAG’s Due Process Monitors progress in IASB

Publishes initial reactions to a new ED Obtains comments from public Completes responses to IASB Follows similar process for final standards and interpretations Sends endorsement advice to EU Commission SARG: to verify due process

63

SARG (Standard Advice Review Group)

SARG created by EU Commission to review objectivity and neutrality of EFRAG (which is a private body) Advice to the Commission on EFRAG’s opinions related to endorsement proposals - Whether these opinions are well-balanced and objective Short deadline to express advice (max 3 weeks) Opinions/reports adopted by consensus Deliberations are confidential.

Advice to the Commission on EFRAG’s opinions related to endorsement proposals - Whether these opinions are well-balanced and objective. Short deadline to express advice (max 3 weeks) Opinions/reports adopted by consensus. Deliberations are confidential.")

64

Accounting Regulatory Committee

POLITICAL ACCEPTABILITY Created by the EU Commission Provides an opinion on Commission’s proposals to endorse an International Accounting Standard Composed by Representatives from Member States (Ministry of Finance, of Justice etc…) Chaired by EU Commission Observers: EFRAG, European Central Bank, CESR

Chaired by EU Commission. Observers: EFRAG, European Central Bank, CESR.")

65

CESR Committee of European Securities Regulators

Improves coordination among securities regulators a Multilateral MOU ensures surveillance and enforcement of securities activities on day by day basis Overviews on timely and day by day EU Legislation implementation in Member States CESR Vice Chairman, Review panel and 2 Working Groups Advice to EU Commission preparing draft implementing measures of EU FRAMEWORK DIRECTIVES in the field of Securities

66

IFRS Convergence process

US is now moving towards adoption of IFRS: this is a confirmation that EU made a good decision: will IFRS be allowed for US issuers by 2011? Also Japan is planning to give up Japanese GAAP for IFRS It may also be equivalence and mutual recognition Consistence does not mean identical application Increased cooperation CESR-SEC

67

Current work in the Accounting area (1/2)

IASB Discussion Papers: Reducing Complexity in Reporting Financial Instruments Amendments to IAS 19 employee benefits IFRS 5 non current assets held for sale and discontinued operations Measuring and disclosing fair value in markets that are no longer active IASB Exposure Draft of an Improved Conceptual Framework for Financial Reporting

68

Current work in the accounting area (2/2)

PAAinE Discussion Papers: The Financial Reporting of Pensions Distinguishing between Liabilities and Equiy IFRS branding Translation of Ifac Audit standards Assessment risk management systems Statutory Audit Directive …and many other…

69

The Audit issue - Audit Regulatory Committee

EU Communication 21 May 2003 led to Directive 2006/43/EC, modernization of 8 th Directive 84/253/EEC, not yet in force in all Member States Adoption of ISAs when clarity project completed Two Committees in force: - Audit Regulatory Committee - Audit Advisory Committee: Member States and professionals Liability and liability cap Widening the number of active audit companies

70

Directive on Statutory Audit 17 May 2006 (2006/43/EC)

Main Issues Education and registration requirements Standards on auditing and ethics Quality assurance (see EU Recommendation) Public oversight on auditors Public interest entities Independence of auditors

Public oversight on auditors. Public interest entities. Independence of auditors.")

71

What Is Statutory Audit?

‘Statutory audit’ means an audit of annual or consolidated accounts in so far as required by Community Law Mandatory for all publicly-traded companies EU Fourth Directive applies to all limited liability companies Member States option to ease reporting and audit of SMEs Small, if not exceed for 2 consecutive years, 2 of the 3 criteria: Balance sheet: € Net turnover: € Average number employees: 50 Use of options ranges from 0 to maximum The EC Simplification Project might amend this

72

www.europa.eu It is all on the web

For full information about the European Union visit the EU’s multilingual web portal:

73

Financial Reporting TECHNOLGY: THE XBRL

74

XBRL (1/4) It’s not only technology, it’s a cultural change

All data to be organised into a dictionary-like classification, describing the contents of each data in Finstats and business documents, the TAXONOMY, and from there a technology-driven system can extract – and combine - any needed information Electronic filing: - saves time - saves money - avoids data entry errors - allows automated extraction of data from Co website by all interested parties (Securities Commissions, stats bureuas, etc)

")

75

XBRL (2/4) Utilisation of Internet capacity and potential

- internet used as a reporting tool - the user may select specific info of interest Financial info may be better disclosed if supported by speaking, animation and interactive functions Distribution of data is improved and more economically efficient Future reporting will be on Internet and interactive The user may “personalise” financial information by selecting figures relevant to him/her

76

XBRL Examples (3/4) Real time information

Create connection from business to financial figures for a normal user Focus on visual and audio communication Internal and external communication Focus on presentation of financial key figures Real time information

77

XBRL (4/4) It is the future: EU Commission firmly believes it is the way forward and will coordinate the existing systems Who drives the IT technical development? New or adapted softwares or dedicated XBRL solutions needed Where is the accounting and audit profession? Accounting experts and professionals should be the ones to drive the new ideas forward

78

Financial Reporting ROLE OF THE ACCOUNTING PROFESSION IN THE EU

79

Challenge today for the Accounting Profession (1/2)

IFRSs Corporate governance Audit issues Role of the Accountant/Auditor

80

Challenge Today for the Accounting Profession (2/2)

IFRSs: Application of IFRS in Europe from 2005 Enforcement of IFRS in Europe Convergence of US GAAP and IFRS IFRS for SMEs Simplification by EU CORPORATE GOVERNANCE INITIATIVE: EU ACTION PLAN AUDIT ISSUES Implementation of the Statutory Audit Directive ISAs as adopted by the EC? Internal control and risk management ROLE OF THE ACCOUNTANT/AUDITOR System of public oversight Quality assurance: monitoring and monitored peer review Auditors liability

81

The Accounting Profession Today (1/2)

Are we a profession or a business? Are we working just only to make money? Standardisation and technology implementation might bring to less revenue for the accountants: most of the work carried out by IT Where is the Accounting Profession? NIVRA is developing a model to make our work, on this subject, reliable A new vision is needed: Simplification Uncertainty of value of audit, and perception it doubles the cost of accounting services

82

The accounting profession today (2/2)

Is it the right way to proceed with 27 sets of laws Different reporting for listed, non listed, SMEs, Micros, financial entities, public entities… With reports prepared only once a year, all on paper when we daily access hundred of times our s on the web… A new type of added value service has to be offered Understand and cope with the new demands on e-filing and other applications

83

Johannes Guigard Chartered Accountant Italy and ACCA

UNIVERSITY OF MOSCOW 13/17 October General overview on the European Accounting and Auditing legislation Johannes Guigard Chartered Accountant Italy and ACCA

Similar presentations

>")