Download presentation

Presentation is loading. Please wait.

1

American Barrick Resources Corporation

2

How Sensitive Would Barrick Stock Be to Changes in Gold Price in the Absence of Risk Management?

4

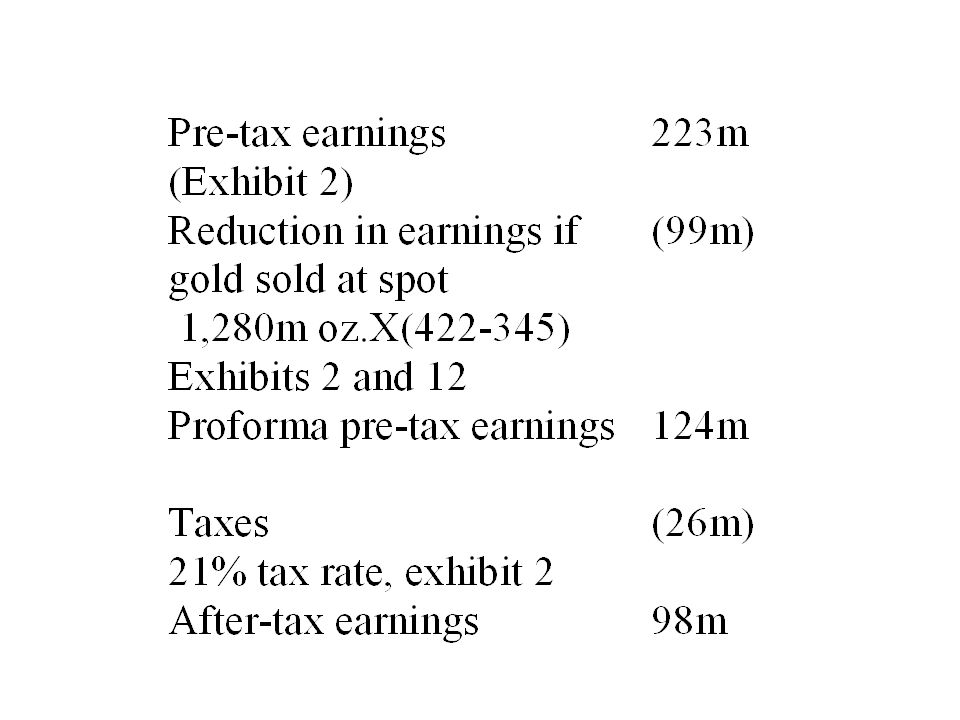

Elasticity of Earnings and Profits for 1% Change in Gold Price

Number of ounces 1,280m Additional pre-tax profits $4.4m Additional after-tax profits $3.5 Additional profits as % of earnings 3.5% Cash flow = Earnings + Noncash charges = 98m + 69m = 167m Additional profits as % of cash flow 2.1%

5

What is Barrick’s Risk Management Program?

6

Guidelines Fully protected against price declines for 3 years output.

20-25% for next decade.

7

Why Manage Gold Price Exposures?

8

Arguments Pure bet on operational efficiencies for investors.

Do they want that or do they want gold? Have funds available to invest when external financing is costly. Eliminating deadweight costs of distress. Tax arguments: If net income is negative, lose use of tax shields.

9

Ownership and Risk Management

If managers have large stake in firm, they don’t want the risk. Eliminating hedgeable risks makes it possible to have concentrated ownership. Barrick management owns 29.6% of Barrick for a value of $900m. Let’s look at the other firms: Exhibit 3.

10

What Instruments Did They Use to Manage Risks?

11

Gold Financing of Acquisitions

Cullaton gold trust: 3% of mine output when gold price was below $399 per ounce. Rising to 10% when gold price was at $1,000 per ounce. How to value this?

12

Tricky: Nonlinear Fraction paid:

Min[( *Max((P - 400)/600),0), 0.1] Example: 600, *0.33 = Payoff: Min[( *Max((P - 400)/600),0), 0.1]*P Example: 0.03* *600 = 32.

/600),0), 0.1] Example: 600, *0.33 = Payoff: Min[( *Max((P - 400)/600),0), 0.1]*P. Example: 0.03* *600 = 32.")

13

Payoff Gold price

14

Gold Loans Gold loan is equivalent to risk-free loan plus forward sale of gold.

15

Forward Price and Contango

To get gold at future date: Solution one: Invest at risk-free rate + Long forward. Solution two: Buy gold today. Twist: Since you don’t need gold until future date, you can lend it and earn gold lease rate.

16

Example: Exhibit 9 Interest rate is 16.83%; lease rate 2%.

Cost of forward strategy for one year: F/1.1683 Cost of spot strategy. Since you gain 2% by leasing, you need 1/1.02 units of gold to get one at maturity: S/1.02 F = S*1.1683/1.02 = S*1.1545or forward exceeds spot by 15.45%

17

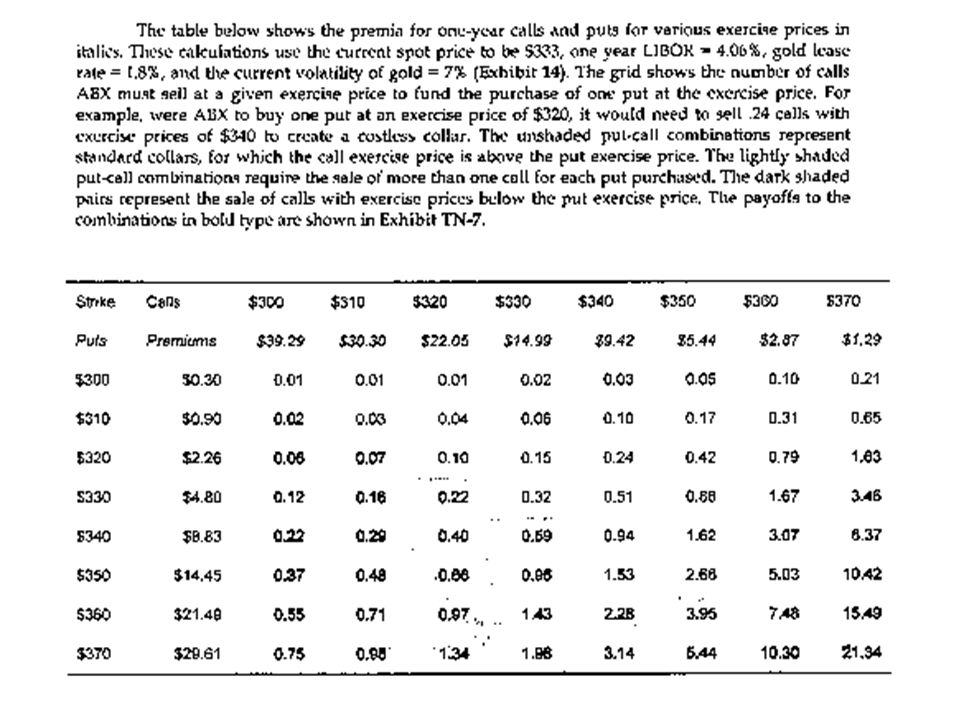

Collars Barrick was willing to use options, but only in the form of costless collars. Buy put and sell call so that premium of put equals premium of call. Example: One year, gold at $333, LIBOR at 4%, gold lease rate at 1.8%, and volatility of gold at 7%.

18

Examples Put at $300 strike, premium is $0.30.

Call at $350 strike, premium is $5.44. To create a costless collar, sell call for each put. If call is at $370 strike instead, premium is $1.29. You have to sell 0.23 calls.

20

Spot Deferred Contracts

What are they?

21

Spot at t = 0 is $300, LIBOR is 6% and lease rate is 2%

Forward at t=0 $312 Production 200 oz. 200 oz. t = 0 t = 1 t = 2 t = 3

22

Case 1: Hedge With Forwards, Spot Is at $500 at t = 1

Value of production sold at forward: 200 x 312 = $62,400. Value of production sold at spot: 200 x 500 = $100,000. Value of forward contract just before t=1: -$37,600

23

Case 2: SDC contracts At t = 0, Barrick enters in contract to sell either at t = 1 or at t = 2. If at t = 1, it chooses not to deliver on contracts, it sells on spot market at $500. The price set so that “both parties are indifferent between rolling over the contract for another year or closing out the SDC contract and initiating a new one-year forward contract”

24

Setting the Price Keep LIBOR and gold lease rate constant.

Forward at t=1 is then: 500 x ( ) = 520 Barrick made a loss of $188 that has to be carried forward at 6%. So, new price is $188 x (1.06) = $320.72

= 520. Barrick made a loss of $188 that has to be carried forward at 6%. So, new price is $188 x (1.06) = $")

25

Did Barrick Follow Its Policy?

26

No. Stopped writing options in 1990 and used only spot deferred.

By 1992, historical low for gold and gold volatilities. In 1992, it could insure against gold prices falling below $330 at $4.8 an ounce. With a collar, it had to give up 88% of upside above $350. Refused to do so.

27

In 1992, could have sold forward at $340 for cash costs of $205.

Was not willing to do so. So, Barrick’s risk management involved substantial speculation.

28

Who Uses Derivatives? Many surveys. Let’s look at the 1998 Wharton/CIBC survey. Sent out to 1,928 firms. 399 responded. 50% use derivatives. 42% have increased usage since previous year; 46% kept constant. Users: 83% of large firms; 45% of medium size companies; 12% of small firms.

29

Most commonly managed risks for users

FX, 96%. Interest rate, 76%. Commodity, 56%. Equity, 34%.

30

Concerns Accounting treatment (high concern for 37%).

Market risk (31%). Monitoring/evaluating hedging results (29%). Credit risk (25%). Liquidity (21%). SEC disclosure (21%). Reaction by analysts, investors (18%).

. Monitoring/evaluating hedging results (29%). Credit risk (25%). Liquidity (21%). SEC disclosure (21%). Reaction by analysts, investors (18%).")

31

Which FX hedging Balance sheet commitments (frequently for 54%; average exposure hedged, 49%). Off balance sheet commitments (24%; 23%). Anticipated transactions less than 1 yr (46%; 42%). Anticipated transactions more than 1 yr (12%; 16%). Hedge competitive exposure (11%; 7%). Hedge translation (14%; 12%).

. Anticipated transactions more than 1 yr (12%; 16%). Hedge competitive exposure (11%; 7%). Hedge translation (14%; 12%).")

32

Maturity effect for FX hedging

Percentage of responding firms Maturity of exposure

33

Does market view matter?

49% sometimes alter timing of hedges and 51% sometimes alter size according to market view. 6% frequently take positions, 26% do so sometimes, to exploit market view.

34

Interest rate derivatives

Almost all firms using interest rate derivatives report swapping from floating to fixed.

35

Options 68% of firms use options; 44% use FX options.

42% use European, 38% use American, 19% use average rate, 9% use basket, 13% use barrier. 47% of FX derivatives users use basket options, 39% use average rate, and 69% use barrier!

36

Reporting and valuation

4% report to directors monthly, 23% quarterly, and 17% annually. 19% value daily; 9% weekly; 27% monthly. 40% want risk management to decrease volatility; 22% want increased profit. 60% of those who do not use do so because lack of exposure.

37

Tufano’s analysis Looks at gold industry.

Advantage: Detailed data on exposures and hedges. Disadvantage: One industry. Key result: Managerial options and ownership are important.

41

Why the Spectacular Success of Derivatives?

They enable you to alter risk. Derivatives can allow you to take risks that are advantageous. Derivatives make it possible for you to shed risks that are costly. It is only recently that finance figured out how to do all this well.

Similar presentations

Swap (slides 7-17)>")