Download presentation

Presentation is loading. Please wait.

1

GRAIN OUTLOOK Agricultural Lenders Conference 2007 Mike Woolverton Kansas State University mikewool@agecon.ksu.edu

2

WHEAT

3

PRODUCTION PROJECTIONS, MAJOR WHEAT EXPORTERS, 2006/07 - 2007/08 (MMT) 2006/07 2007/08 EU-27 124.80 121.83 EU-27 124.80 121.83 United States 49.32 57.53 United States 49.32 57.53 Canada 25.27 20.30 Canada 25.27 20.30 Australia 9.90 21.00 (15.5) Australia 9.90 21.00 (15.5) Argentina 15.20 14.00 Argentina 15.20 14.00 Total World Prod. 593.07 606.24 Total World Prod. 593.07 606.24 Ending Stocks 125.08 112.36 Ending Stocks 125.08 112.36

4

Wheat Balance Sheet 05-06 06-07 07/08 Plant A. (mil.) 57.2 57.3 60.5 Harvest A. (mil.) 50.1 46.8 52.1 Bu./A. 42.0 38.7 40.6 Production 2,105 1,812 2,114 Production 2,105 1,812 2,114 Imports 82 122 85 Imports 82 122 85 Carryover 540 571 456 Carryover 540 571 456 Total Supply 2,727 2,505 2,655 Total Supply 2,727 2,505 2,655Utilization: Feed and Residual 154 129 170 Feed and Residual 154 129 170 Food 914 930 940 Food 914 930 940 Seed 78 81 83 Seed 78 81 83 Exports 1,009 909 1,100 Exports 1,009 909 1,100 Total Utilization 2,155 2,049 2,293 Carryover 571 (26%) 456 (22%) 362 (16%) U.S. Farm Price $3.42 $4.26 $5.50-6.10

Bu./A Production 2,105 1,812 2,114 Production 2,105 1,812 2,114 Imports Imports Carryover Carryover Total Supply 2,727 2,505 2,655 Total Supply 2,727 2,505 2,655Utilization: Feed and Residual Feed and Residual Food Food Seed Seed Exports 1, ,100 Exports 1, ,100 Total Utilization 2,155 2,049 2,293 Carryover 571 (26%) 456 (22%) 362 (16%) U.S. Farm Price $3.42 $4.26 $")

9

Share of World Wheat Exports, 2007/08, USDA

10

SOYBEANS

11

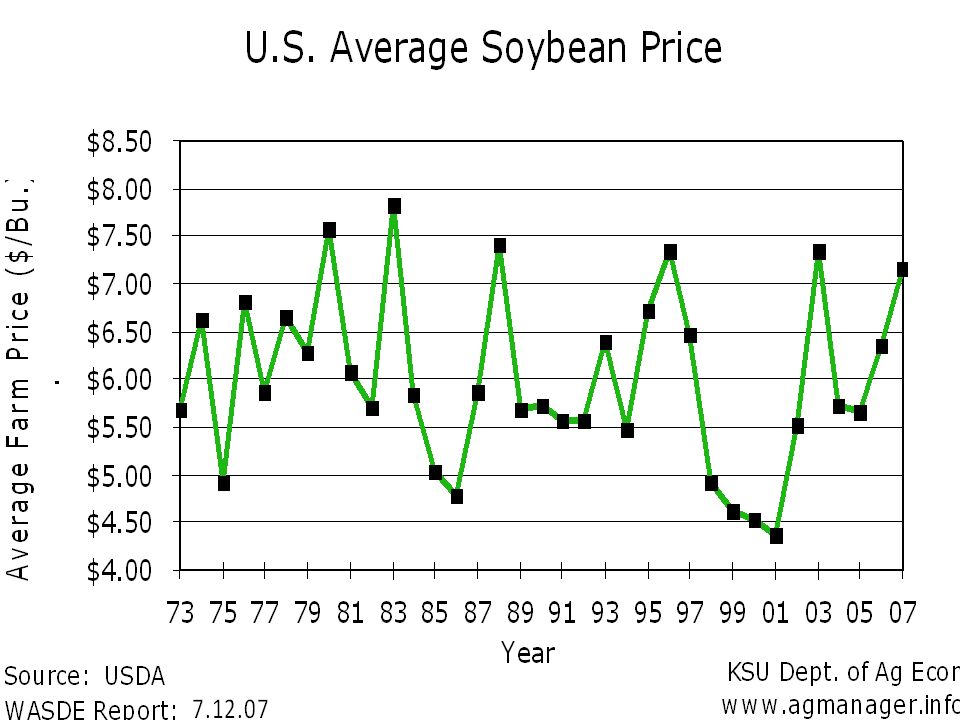

Soybean Balance Sheet 05-06 06-0707/08 Plant A. (mil.) 72.0 75.5 64.1 Harvest A. (mil.) 71.3 74.6 63.3 Bu./A. 43.0 42.7 41.4 Production 3,063 3,188 2,619 Imports 3 8 6 Imports 3 8 6 Beginning Carryover 256 449 555 Beginning Carryover 256 449 555 Total Supply 3,322 3,646 3,180 Total Supply 3,322 3,646 3,180Utilization: Crushings 1,739 1,805 1,825 Crushings 1,739 1,805 1,825 Seed 93 79 85 Seed 93 79 85 Exports 947 1,115 975 Exports 947 1,115 975 Residual 93 92 79 Residual 93 92 79 Total Utilization2,873 3,091 2,964 Ending Carryover 449 (16%) 555 (18%) 215 (7%) Ending Carryover 449 (16%) 555 (18%) 215 (7%) U.S. Farm Price$5.66 $6.40 $7.35-8.35

Bu./A Production 3,063 3,188 2,619 Imports Imports Beginning Carryover Beginning Carryover Total Supply 3,322 3,646 3,180 Total Supply 3,322 3,646 3,180Utilization: Crushings 1,739 1,805 1,825 Crushings 1,739 1,805 1,825 Seed Seed Exports 947 1, Exports 947 1, Residual Residual Total Utilization2,873 3,091 2,964 Ending Carryover 449 (16%) 555 (18%) 215 (7%) Ending Carryover 449 (16%) 555 (18%) 215 (7%) U.S. Farm Price$5.66 $6.40 $")

16

Share of World Soybean Exports, 2007/08, USDA

17

CORN

18

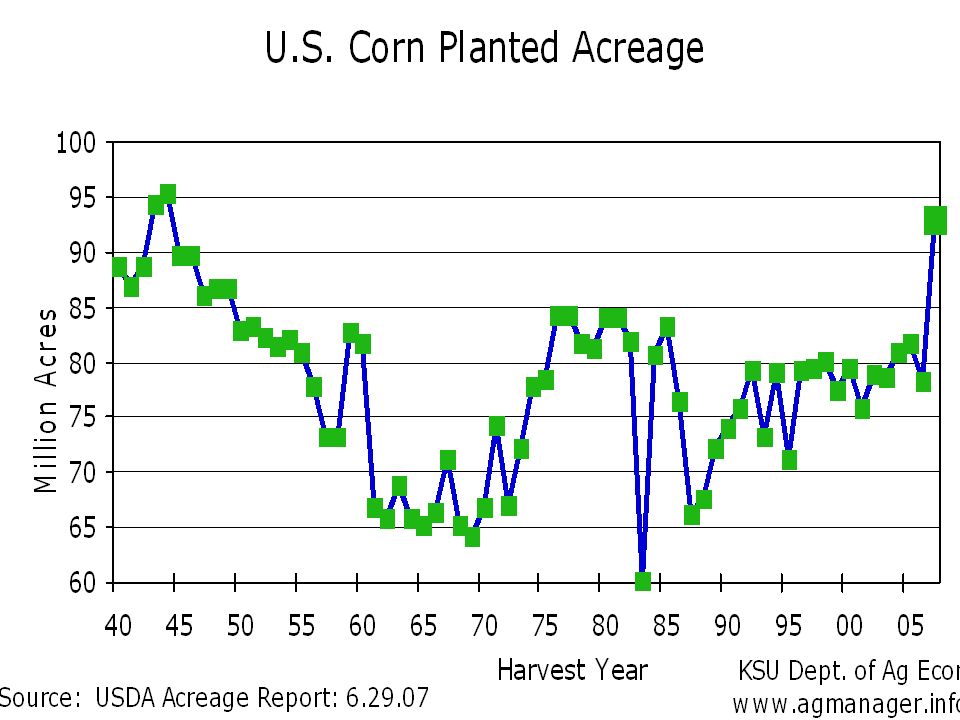

Corn Balance Sheet 05-06 06-07 07/08 05-06 06-07 07/08 Plant A. (mil.) 81.8 78.3 92.9 Harvest A. (mil.) 75.1 70.6 85.4 Bu./A. 148.0 149.1 152.8 Production 11,114 10,535 13,054 Imports 9 10 15 Imports 9 10 15 Beginning Carryover 2,114 1,967 1,137 Beginning Carryover 2,114 1,967 1,137 Total Supply 13,237 12,512 14,206 Total Supply 13,237 12,512 14,206Utilization: Feed and Residual 6,141 5,750 5,750 Feed and Residual 6,141 5,750 5,750 Food, seed, industrial 2,981 3,525 4,790 Food, seed, industrial 2,981 3,525 4,790 Ethanol for fuel 1,603 (14%) 2,150 (20%) 3,400 (26%) Ethanol for fuel 1,603 (14%) 2,150 (20%) 3,400 (26%) Exports 2,147 2,100 2,150 Exports 2,147 2,100 2,150 Total Utilization 11,270 11,375 12,690 Ending Carryover 1,967 (17%) 1,137 (10%) 1,516 (12%) Ending Carryover 1,967 (17%) 1,137 (10%) 1,516 (12%) U.S. Farm Price $2.00 $3.00 $2.80-3.40

Harvest A. (mil.) Bu./A Production 11,114 10,535 13,054 Imports Imports Beginning Carryover 2,114 1,967 1,137 Beginning Carryover 2,114 1,967 1,137 Total Supply 13,237 12,512 14,206 Total Supply 13,237 12,512 14,206Utilization: Feed and Residual 6,141 5,750 5,750 Feed and Residual 6,141 5,750 5,750 Food, seed, industrial 2,981 3,525 4,790 Food, seed, industrial 2,981 3,525 4,790 Ethanol for fuel 1,603 (14%) 2,150 (20%) 3,400 (26%) Ethanol for fuel 1,603 (14%) 2,150 (20%) 3,400 (26%) Exports 2,147 2,100 2,150 Exports 2,147 2,100 2,150 Total Utilization 11,270 11,375 12,690 Ending Carryover 1,967 (17%) 1,137 (10%) 1,516 (12%) Ending Carryover 1,967 (17%) 1,137 (10%) 1,516 (12%) U.S. Farm Price $2.00 $3.00 $")

24

Corn Usage Estimates (Millions of Bushels) USDA/WASDE USDA/WASDE USDA/WASDE USDA/WASDE 2006/07 2007/08 est. 2006/07 2007/08 est. Feed and Residual 5,750 5,700 1 (-1%) Food, Seed, and Industrial 1,375 1,390 2 (+1%) Ethanol for Fuel 2,150 3,400 (+58%) Net Exports 2,100 2,000 (-5%) Ending Stocks 1,137 1,502 Total Usage 12,512 13,992 (+12%) 1 Assumes DDGS retain 30% of the feed value of corn and are included in the feed and residual category by the USDA. 2 Industrial, food, and seed less ethanol.

Food, Seed, and Industrial 1,375 1,390 2 (+1%) Ethanol for Fuel 2,150 3,400 (+58%) Net Exports 2,100 2,000 (-5%) Ending Stocks 1,137 1,502 Total Usage 12,512 13,992 (+12%) 1 Assumes DDGS retain 30% of the feed value of corn and are included in the feed and residual category by the USDA. 2 Industrial, food, and seed less ethanol..")

26

World Corn Production and Consumption Global production up 10% from 2006/07. Demand up 6%. Global production up 10% from 2006/07. Demand up 6%. Production will be 4.5 MMT (176 mil. Bu.) greater than consumption. Production will be 4.5 MMT (176 mil. Bu.) greater than consumption. Ending stocks forecast to increase slightly from last year to 14 % of usage. Ending stocks forecast to increase slightly from last year to 14 % of usage. Million MT

greater than consumption. Production will be 4.5 MMT (176 mil. Bu.) greater than consumption. Ending stocks forecast to increase slightly from last year to 14 % of usage. Ending stocks forecast to increase slightly from last year to 14 % of usage. Million MT.")

27

Share of World Corn Exports, 2007/08, USDA

28

Land in Crops (Millions of acres) 5 yr. Ave. 07/08USDA Proj. 08/09 5 yr. Ave. 07/08USDA Proj. 08/09 Corn 79.6 92.9 88.2 (-5%) Soybeans 74.2 64.1 68.9 (+7%) Hay 62.4 61.8 61.8 (--) Wheat 59.5 60.5 62.6 (+2%) Cotton 14.1 11.1 10.0 (-11%) Grain Sorghum 8.1 7.8 7.4 (-5%) Principle Crops 322.0 320.1 321.1 CRP 35.9 34.9 (-3%) Total crop land in the United States – 441.6 million acres

Soybeans (+7%) Hay (--) Wheat (+2%) Cotton (-11%) Grain Sorghum (-5%) Principle Crops CRP (-3%) Total crop land in the United States – million acres.")

29

Crop Acres Coming Out of CRP, 2007–2017, Millions of Acres Source: USDA, FSA

30

Land in CRP, Leading States, 2007 Millions of Acres Source: USDA, FSA

31

Grain Marketing Considerations Wheat – Global shortage of quality milling wheat, Australian production, and acres planted N. Hemisphere. Wheat – Global shortage of quality milling wheat, Australian production, and acres planted N. Hemisphere. Corn/G.S. – Strong demand from domestic livestock and overseas buyers, ethanol demand, and bid for acres. Corn/G.S. – Strong demand from domestic livestock and overseas buyers, ethanol demand, and bid for acres. Soybeans – national average yield, hectares in Brazil and acres in the U.S., growing demand for SBO for biodiesel. Soybeans – national average yield, hectares in Brazil and acres in the U.S., growing demand for SBO for biodiesel. Factors to Watch: Global S/D balances Global S/D balances Battle for Acres Battle for Acres Southern Hemisphere Crops Southern Hemisphere Crops Ethanol Price Ethanol Price

Similar presentations