Download presentation

Presentation is loading. Please wait.

1

Grain Market Outlook Ag Profitability Conference Wakeeney, Kansas December 20, 2007 Mike Woolverton & Daniel OBrien K-State Research and Extension mikewool@agecon.ksu.edumikewool@agecon.ksu.edu dobrien@oznet.ksu.edu mikewool@agecon.ksu.edu

2

Historic vs Current Grain Prices, Dollars per Bushel 2000-07 Average 12/17/07 Wheat $3.36 $9.56 Corn $2.27 $4.24 Grain Sorghum $2.20 $4.19 Soybeans $5.64 $10.93 1 Average price per bushel, 2000-2007. 2 Kansas City cash truck bids, 17 December 2007.

3

Wheat Markets

4

Wakeeney, KS Cash Wheat Prices Midwest Coop, Wakeeney, Kansas Jan. 19 – Dec. 18, 2007 Source: DTN Bid Analyzer

5

March 2008 HRW Wheat Futures KCBT: April 2006-December 2007 2008 Old Crop March HRW Contract Contract Volume & Open Interest

6

July 2008 HRW Wheat Futures KCBT: April 2006-December 2007 2008 New Crop July HRW Contract Contract Volume & Open Interest

7

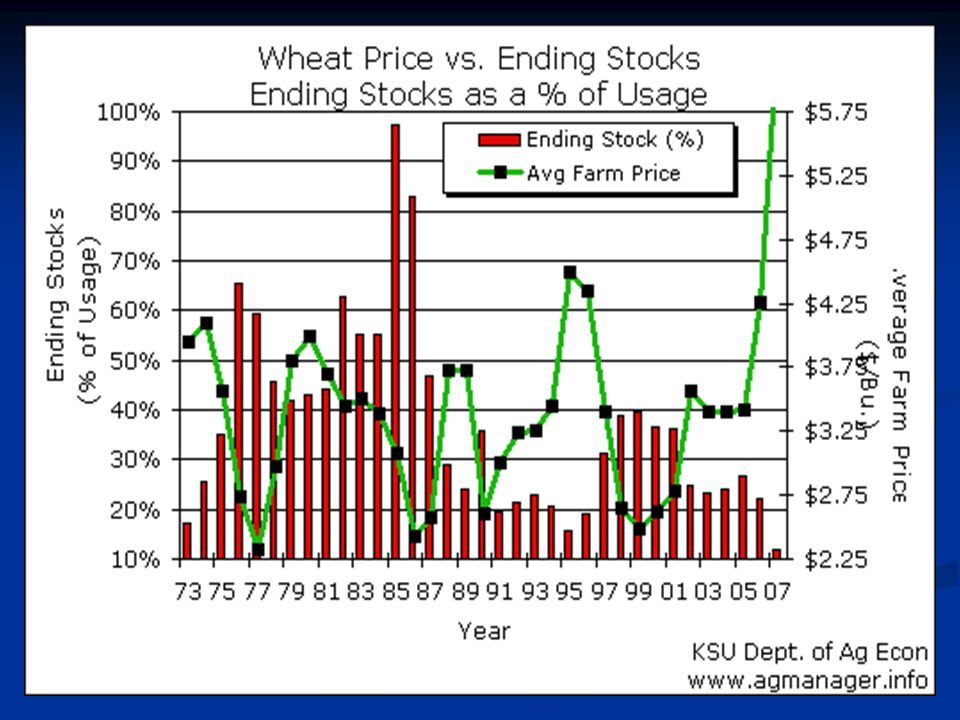

U.S. Wheat Supply-Demand

12

Production of Major Wheat Exporters Million Metric Tons 2006/07 2007/08 2006/07 2007/08 EU-27 124.80 120.50 EU-27 124.80 120.50 United States 49.32 56.25 United States 49.32 56.25 Canada 25.27 20.05 Canada 25.27 20.05 Australia 9.90 13.00 (12.7) Australia 9.90 13.00 (12.7) Argentina 15.20 15.00 Argentina 15.20 15.00 World Production 593.07 602.31 World Production 593.07 602.31 World Ending Stocks 125.08 110.06 World Ending Stocks 125.08 110.06

Australia (12.7) Argentina Argentina World Production World Production World Ending Stocks World Ending Stocks")

15

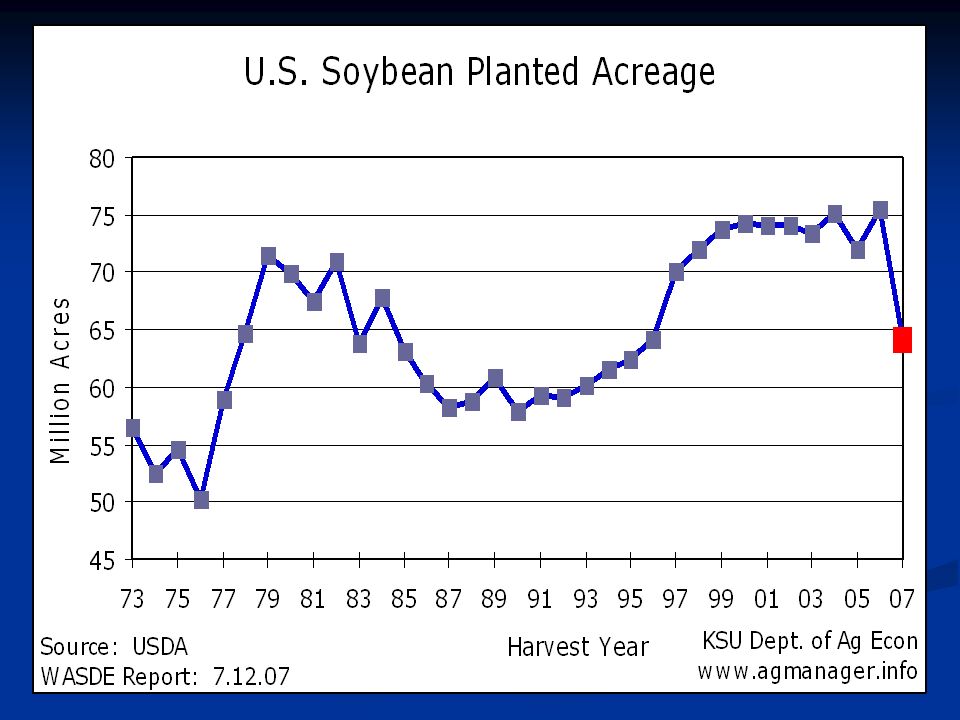

Soybean Markets

16

Hays, KS Cash Soybean $s Midland Marketing - Hays, Kansas Jan. 19 – Dec. 18, 2007 Source: DTN Bid Analyzer

17

March 2008 E-Soybean Futures CBOT: April 2006-December 2007 2008 Old Crop Soybean Contract Contract Volume & Open Interest

18

November 2008 E-Soybean Futures CBOT: April 2006-December 2007 2008 Old Crop Soybean Contract Contract Volume & Open Interest

19

U.S. Soybean Supply-Demand

26

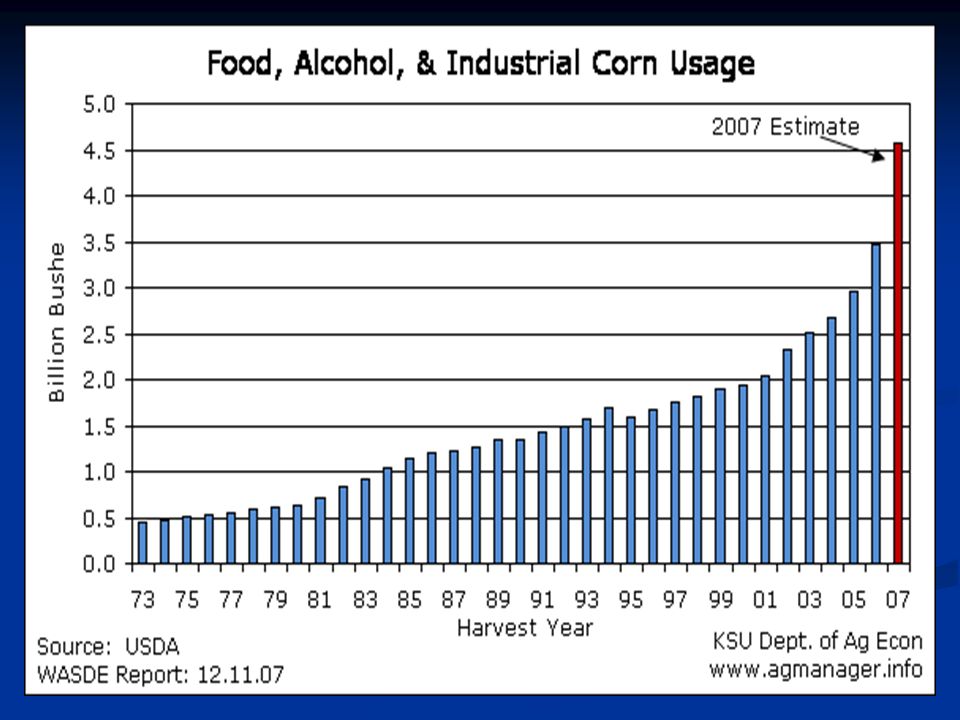

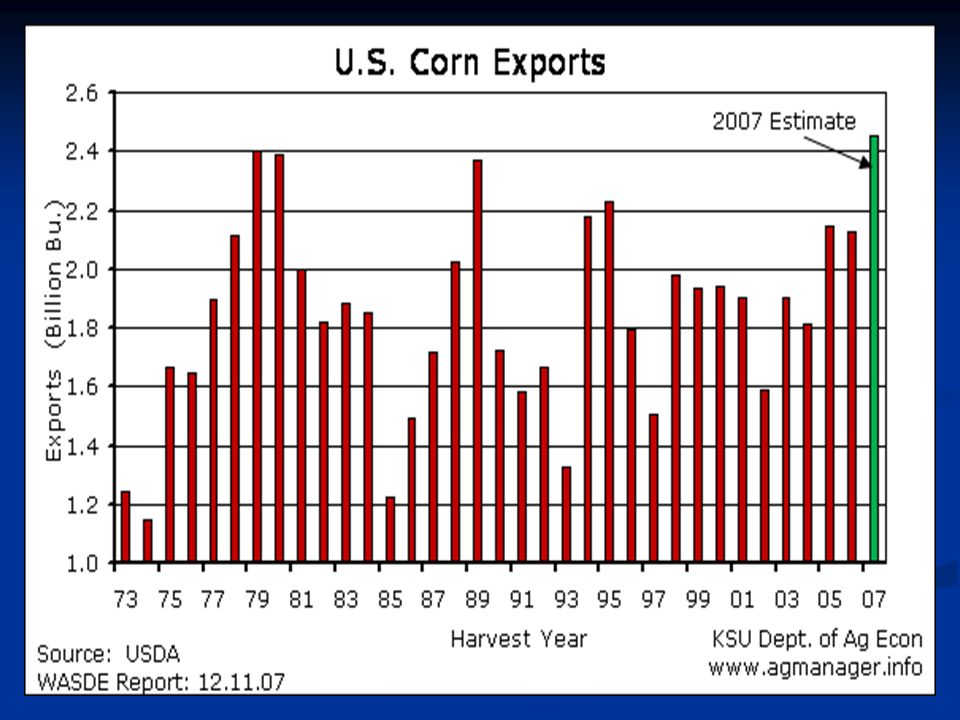

Feedgrain Markets: Corn & Grain Sorghum

27

Wakeeney, KS Corn Cash Prices Midwest Coop, Wakeeney, KS Jan. 19 – Dec. 18, 2007 Source: DTN Bid Analyzer

28

Wakeeney, KS Grain Sorghum Cash Prices Midwest Coop, Wakeeney, KS Jan. 19 – Dec. 18, 2007 Source: DTN Bid Analyzer

29

March 2008 E-Corn Futures CBOT: April 2006-December 2007 2008 Old Crop Corn Contract Contract Volume & Open Interest

30

December 2008 E-Corn Futures CBOT: April 2006-December 2007 2008 New Crop Corn Contract Contract Volume & Open Interest

31

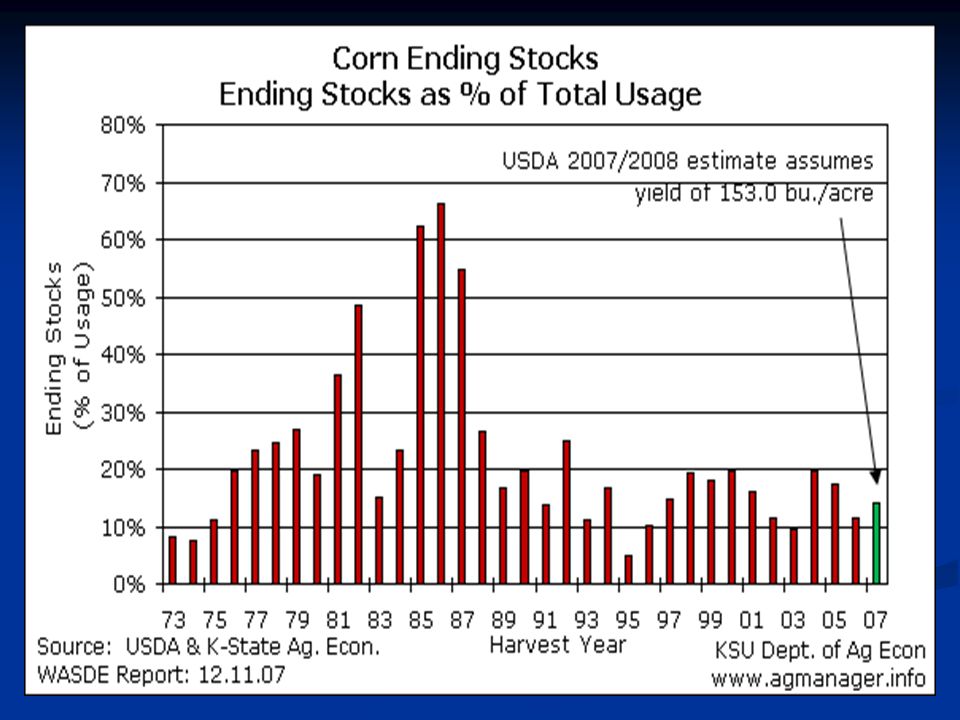

U.S. Corn Supply-Demand

32

U.S. Grain Sorghum Supply-Demand

41

Dynamics of U.S. Corn Usage USDA/WASDE USDA/WASDE USDA/WASDE USDA/WASDE 2006/07 2007/08 est. 2006/07 2007/08 est. Feed and Residual 5,5985,650 1 (+1%) Food, Seed, and Industrial 1,3711,390 2 (+1%) Ethanol for Fuel 2,117 3,200 (+51%) Net Exports 2,1252,450 (+15%) Ending Stocks 1,304 1,797 (+38%) Total Usage 12,515 14,487 (+16%) Production 10,535 13,168 (+25%) 1 Assumes DDGS retain 30% of the feed value of corn and are included in the feed and residual category by the USDA. 2 Industrial, food, and seed less ethanol.

Food, Seed, and Industrial 1,3711,390 2 (+1%) Ethanol for Fuel 2,117 3,200 (+51%) Net Exports 2,1252,450 (+15%) Ending Stocks 1,304 1,797 (+38%) Total Usage 12,515 14,487 (+16%) Production 10,535 13,168 (+25%) 1 Assumes DDGS retain 30% of the feed value of corn and are included in the feed and residual category by the USDA. 2 Industrial, food, and seed less ethanol..")

42

World Corn Production & Consumption Global production up 9% from 2006/07. Demand up 6%. Production will be 2.9 MMT (114 mil. Bu.) greater than consumption. Ending stocks forecast to increase slightly from last year to 14 % of usage. Million MT

greater than consumption. Ending stocks forecast to increase slightly from last year to 14 % of usage. Million MT.")

43

Land in Crops (Millions of acres) 5 yr. Ave. 07/08USDA Proj. 08/09 5 yr. Ave. 07/08USDA Proj. 08/09 Corn 79.6 93.6 88.0 (-6%) Soybeans 74.2 63.7 70.0 (+10%) Hay 62.4 61.8 61.8 (--) Wheat 59.5 60.4 62.2 (+3%) Cotton 14.1 10.9 10.0 (-8%) Grain Sorghum 8.1 7.7 7.4 (-4%) Principle Crops 297.9 298.1 299.4 CRP 35.9 34.9 (-3%) Total crop land in the United States – 441.6 million acres

Soybeans (+10%) Hay (--) Wheat (+3%) Cotton (-8%) Grain Sorghum (-4%) Principle Crops CRP (-3%) Total crop land in the United States – million acres.")

44

Crop Acres Coming Out of CRP 2007–2017, Millions of Acres Source: USDA, FSA

45

Grain Marketing Considerations Wheat – Global shortage of quality milling wheat, reduced Australian and Argentinean production, and acres planted N. Hemisphere. Wheat – Global shortage of quality milling wheat, reduced Australian and Argentinean production, and acres planted N. Hemisphere. Corn/G.S. – Strong demand from overseas buyers, ethanol demand, and bid for acres. Corn/G.S. – Strong demand from overseas buyers, ethanol demand, and bid for acres. Soybeans – Dryness hurting Argentinean and Brazilian crops, hectares in Brazil up only 1%, and critically low carryover in the U.S. Soybeans – Dryness hurting Argentinean and Brazilian crops, hectares in Brazil up only 1%, and critically low carryover in the U.S. Factors to Watch: Tight global S/D balances for wheat and soybeans Tight global S/D balances for wheat and soybeans Battle for acres this spring Battle for acres this spring Harvest of Southern Hemisphere crops Harvest of Southern Hemisphere crops

46

Questions??? K-State Extension Agricultural Economics: AgManager.info

Similar presentations