Download presentation

Presentation is loading. Please wait.

1

Theory of production

2

Production theory forms the foundation for the theory of supply

Managerial decision making involves four types of production decisions: 1. Whether to produce or to shut down 2. How much output to produce 3. What input combination to use 4. What type of technology to use

3

Production involves transformation of inputs such as capital, equipment, labor, and land into output - goods and services In this production process, the manager is concerned with efficiency in the use of the inputs - technical vs. economical efficiency

4

Two Concepts of Efficiency

Economic efficiency: occurs when the cost of producing a given output is as low as possible Technological efficiency: occurs when it is not possible to increase output without increasing inputs

5

When a firm makes choices, it faces many constraints:

Constraints imposed by the firms customers Constraints imposed by the firms competitors Constraints imposed by nature Nature imposes constraints that there are only certain kinds of technological choices that are possible

6

The Technology of Production

The Production Process Combining inputs or factors of production to achieve an output Categories of Inputs (factors of production) Labor Materials Capital 4

Labor. Materials. Capital. 4.")

7

The Organization of Production

Inputs Labor, Capital, Land Fixed Inputs Variable Inputs Short Run At least one input is fixed Long Run All inputs are variable

10

Long run and the short run

In the short run there are some factors of production that are fixed at pre-determined levels. (farming and land) In the long run, all factors of production can be varied. There is no specific time interval implied in the definition of short and long run. It depends on what kinds of choices we are examining

In the long run, all factors of production can be varied. There is no specific time interval implied in the definition of short and long run. It depends on what kinds of choices we are examining.")

11

The Technology of Production

Production Function: Indicates the highest output that a firm can produce for every specified combination of inputs given the state of technology. Shows what is technically feasible when the firm operates efficiently. 5

12

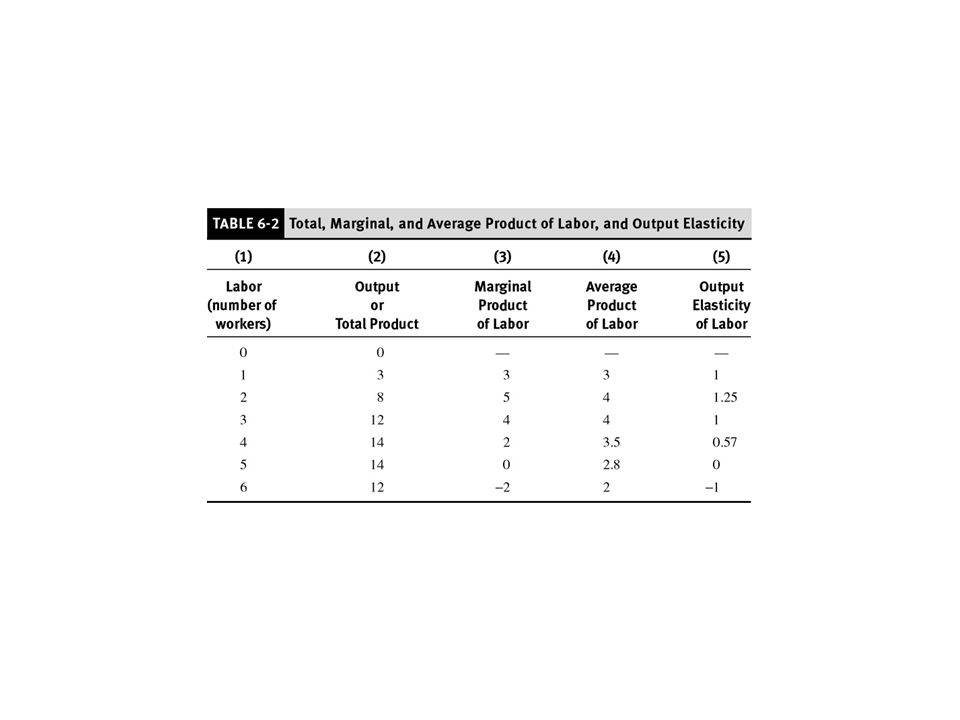

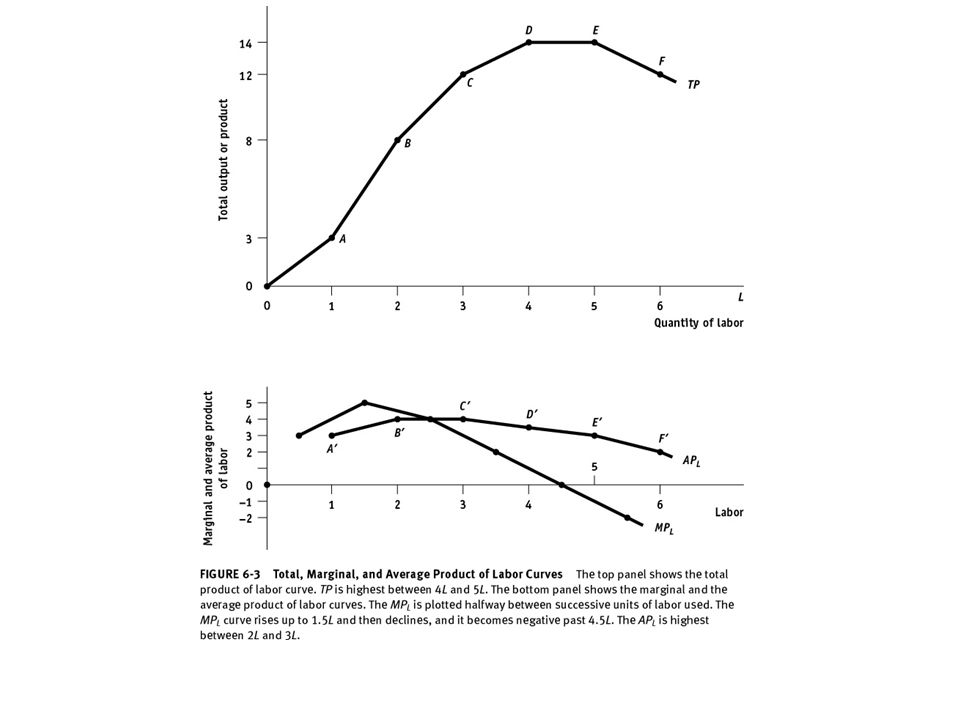

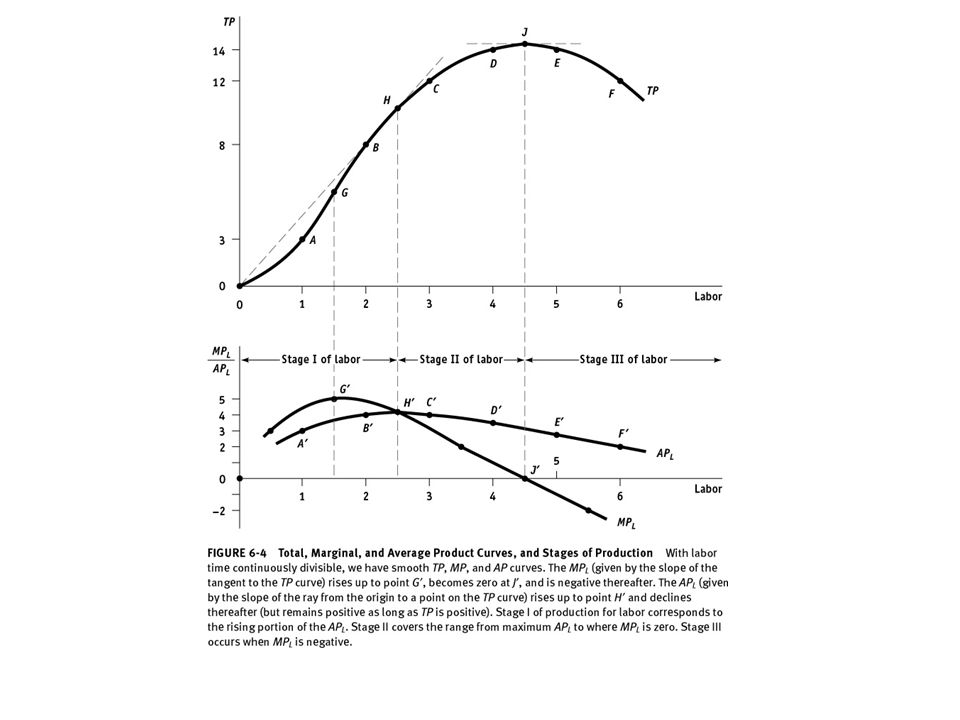

Production Function with One Variable Input

Total Product TP = Q = f(L) MPL = TP L Marginal Product APL = TP L Average Product EL = MPL APL Production or Output Elasticity

MPL = TP L. Marginal Product. APL = TP L. Average Product. EL = MPL APL. Production or Output Elasticity.")

16

Optimal Use of the Variable Input

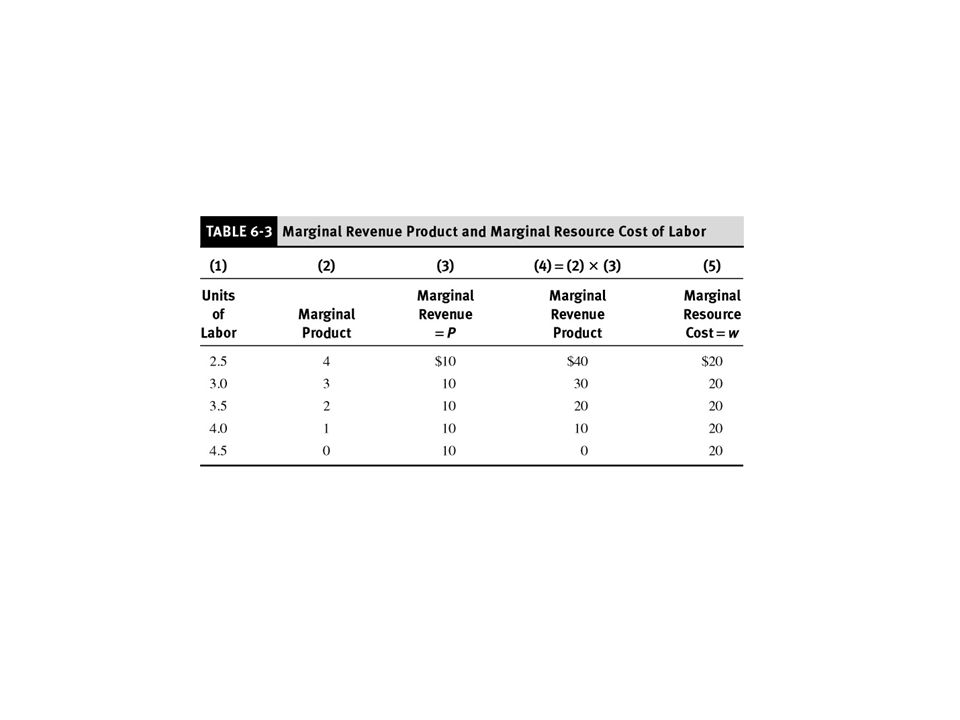

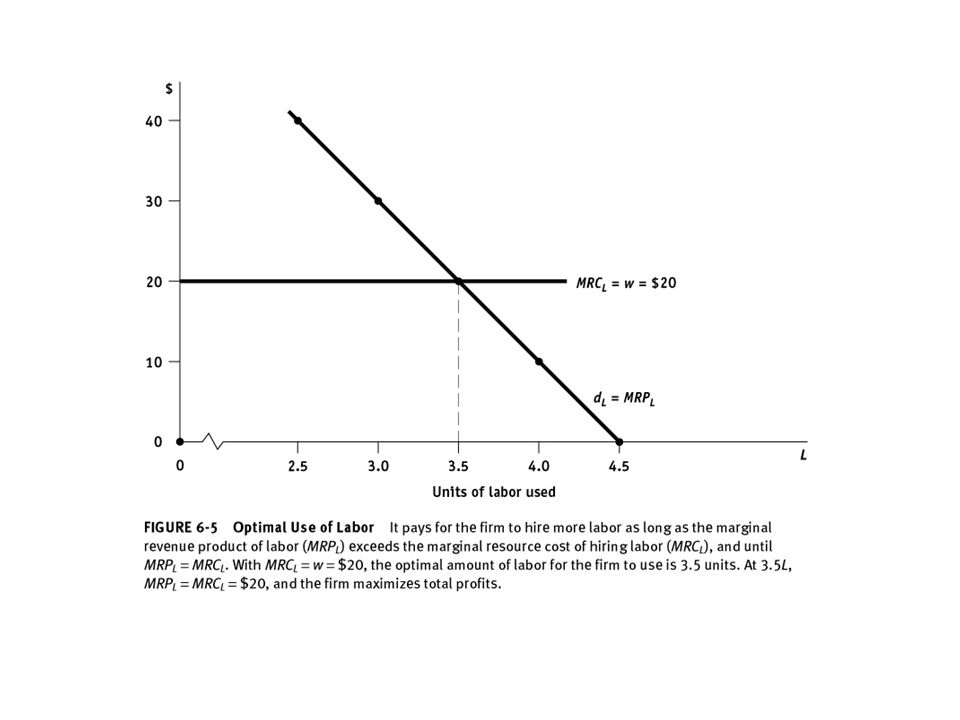

Marginal Revenue Product of Labor MRPL = (MPL)(MR) Marginal Resource Cost of Labor TC L MRCL = Optimal Use of Labor MRPL = MRCL

(MR) Marginal Resource Cost of Labor. TC L. MRCL = Optimal Use of Labor. MRPL = MRCL.")

19

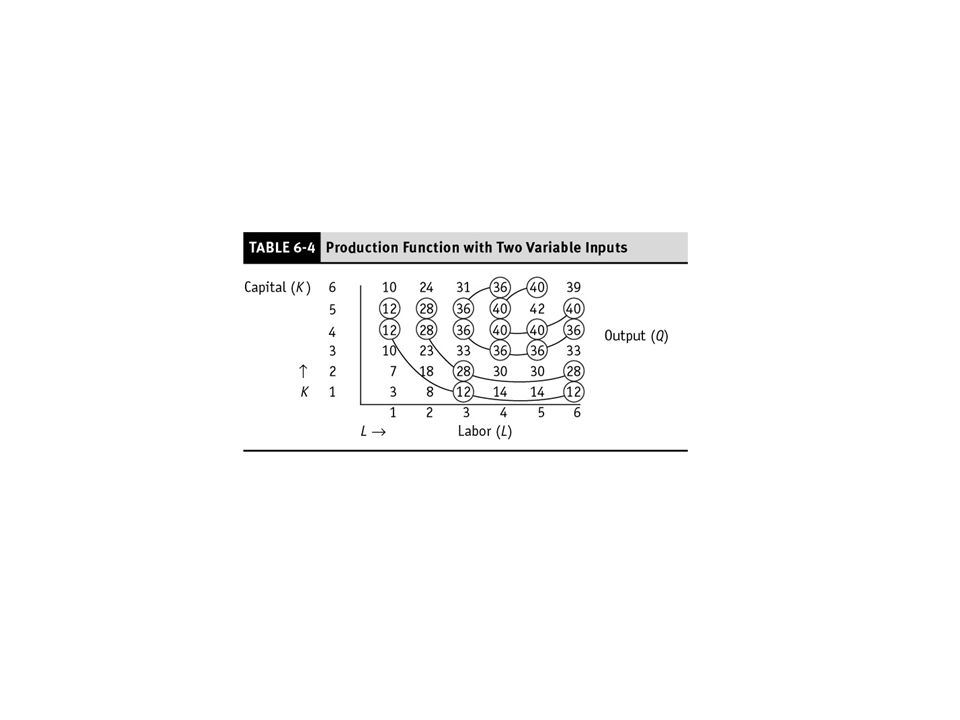

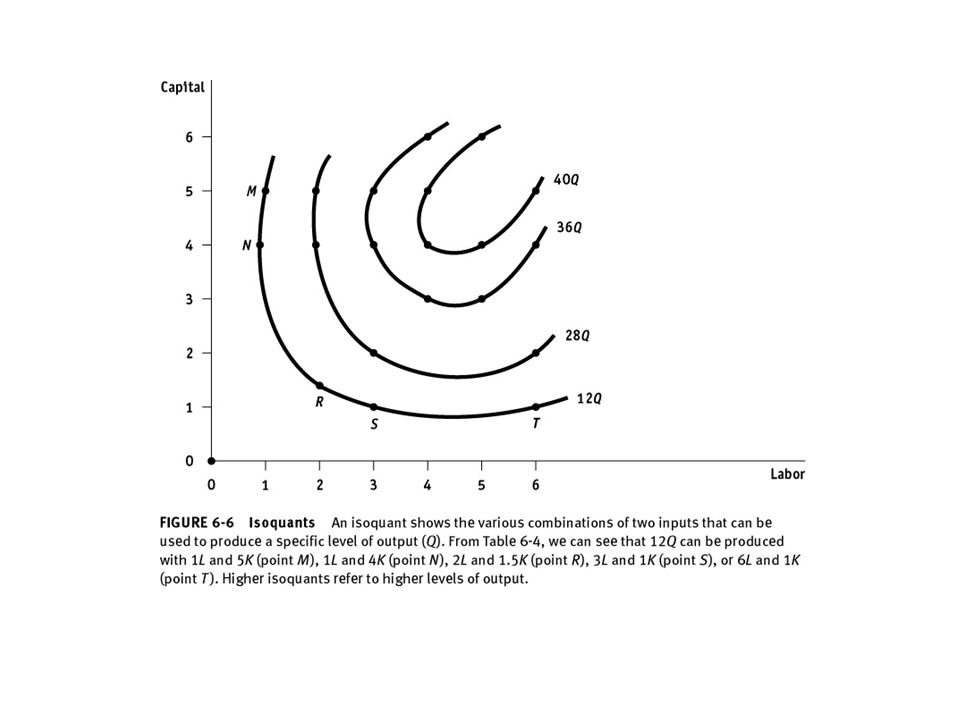

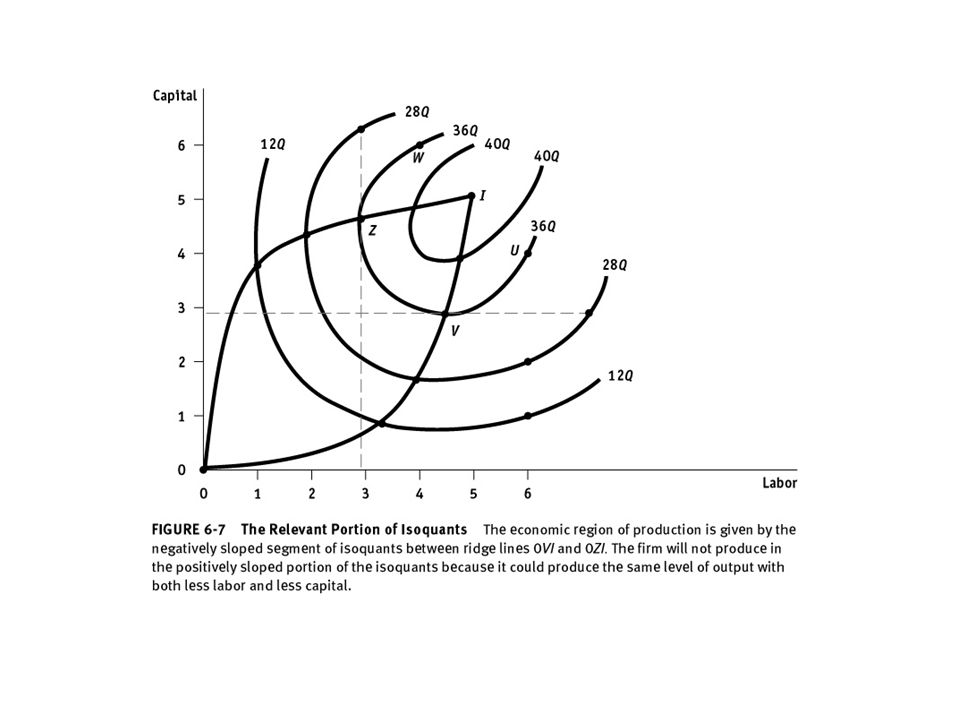

Production with Two Variable Inputs

Isoquants show combinations of two inputs that can produce the same level of output. Firms will only use combinations of two inputs that are in the economic region of production, which is defined by the portion of each isoquant that is negatively sloped.

23

Isoquants When Inputs are Perfectly Substitutable

Capital per month Q1 Q2 Q3 A B C Labor per month 64

24

Production with Two Variable Inputs

Perfect Substitutes Observations when inputs are perfectly substitutable: 1) The MRTS is constant at all points on the isoquant. 65

The MRTS is constant at all points on the isoquant. 65.")

25

Production with Two Variable Inputs

Perfect Substitutes Observations when inputs are perfectly substitutable: 2) For a given output, any combination of inputs can be chosen (A, B, or C) to generate the same level of output (e.g. toll booths & musical instruments) 65

For a given output, any combination of inputs can be chosen (A, B, or C) to generate the same level of output (e.g. toll booths & musical instruments) 65.")

26

Fixed-Proportions Production Function

L1 K1 Q1 Q2 Q3 A B C Capital per month Labor per month 66

27

Production with Two Variable Inputs

Fixed-Proportions Production Function Observations when inputs must be in a fixed- proportion: 1) No substitution is possible.Each output requires a specific amount of each input (e.g. labor and jackhammers). 67

No substitution is possible.Each output requires a specific amount of each input (e.g. labor and jackhammers). 67.")

28

Production with Two Variable Inputs

Fixed-Proportions Production Function Observations when inputs must be in a fixed- proportion: 2) To increase output requires more labor and capital (i.e. moving from A to B to C which is technically efficient). 67

To increase output requires more labor and capital (i.e. moving from A to B to C which is technically efficient). 67.")

29

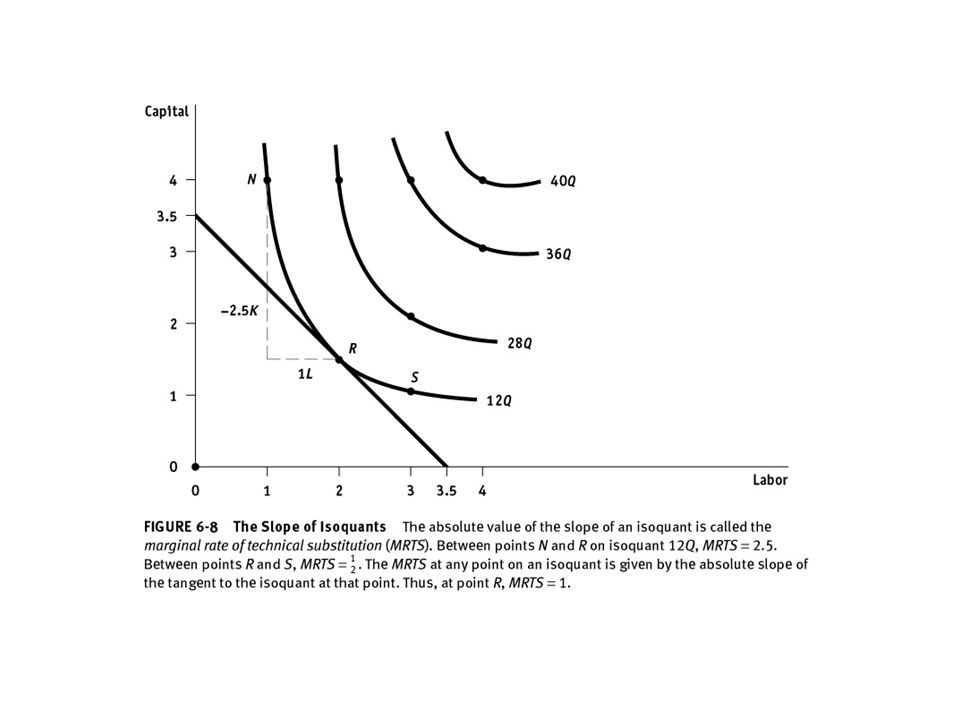

Production with Two Variable Inputs

Marginal Rate of Technical Substitution MRTS = -K/L = MPL/MPK

31

Curves showing all possible combinations of inputs that yield the same output

An isoquant is a curve showing all possible combinations of inputs physically capable of producing a given fixed level of output The isoquants emphasize how different input combinations can be used to produce the same output. This information allows the producer to respond efficiently to changes in the markets for inputs.

32

Example 2 Production Table

Units of K Employed Isoquant

33

An Isoquant

36

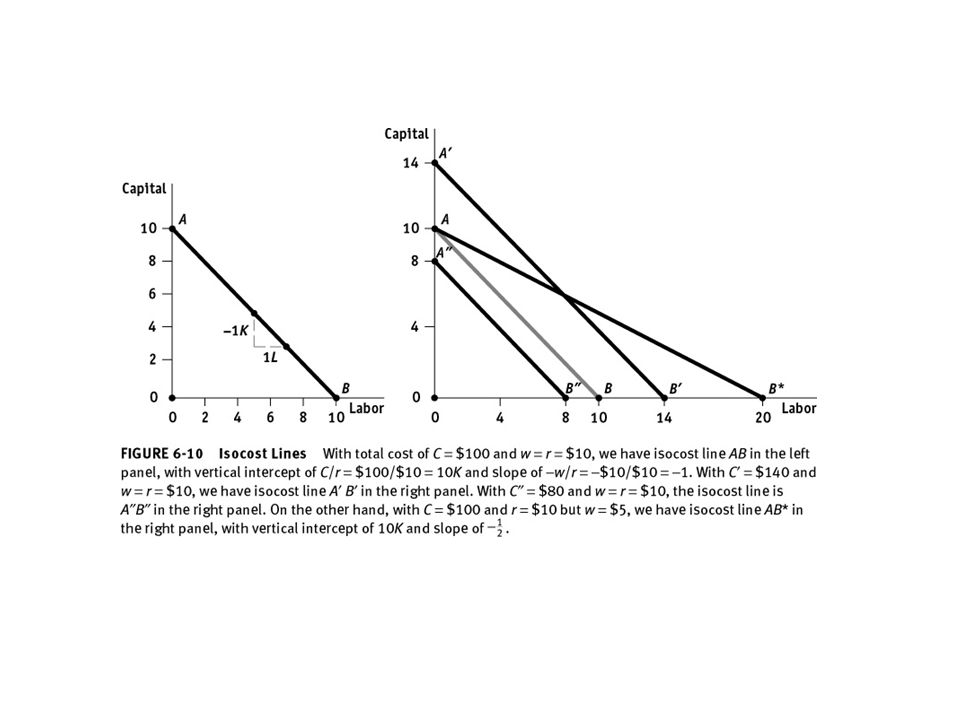

Isocost Line Isocost line: shows all possible K/L combos that can be purchased for a given TC. TC = C = w*L + r*K ; Rewrite as equation of a line: K = C/r – (w/r)*L Slope = K/L = -(w/r). Interpret slope: * shows rate at which K and L can be traded off, keeping TC the same. Relate to consumer’s budget constraint: * slope = ratio of prices with price from horizontal axis in numerator. Vertical intercept = C/r. Horizontal intercept = C/w.

*L. Slope = K/L = -(w/r). Interpret slope: * shows rate at which K and L can be traded off, keeping TC the same. Relate to consumer’s budget constraint: * slope = ratio of prices with price from horizontal axis in numerator. Vertical intercept = C/r. Horizontal intercept = C/w.")

37

Units of Y 12 10 8 B = $1,000 B = $2,000 6 B = $3,000 4 2 Units of X 2

Production and Costs Optimal combination of multiple inputs Isocost curves. All combinations of products that can be purchased for a fixed dollar amount Units of Y 12 10 Downward sloping curve. 8 B = $1,000 1 Shift B 2 = $2,000 6 B 3 = $3,000 4 Slope 2 Units of X 2 4 6

38

Optimal Combination of Inputs

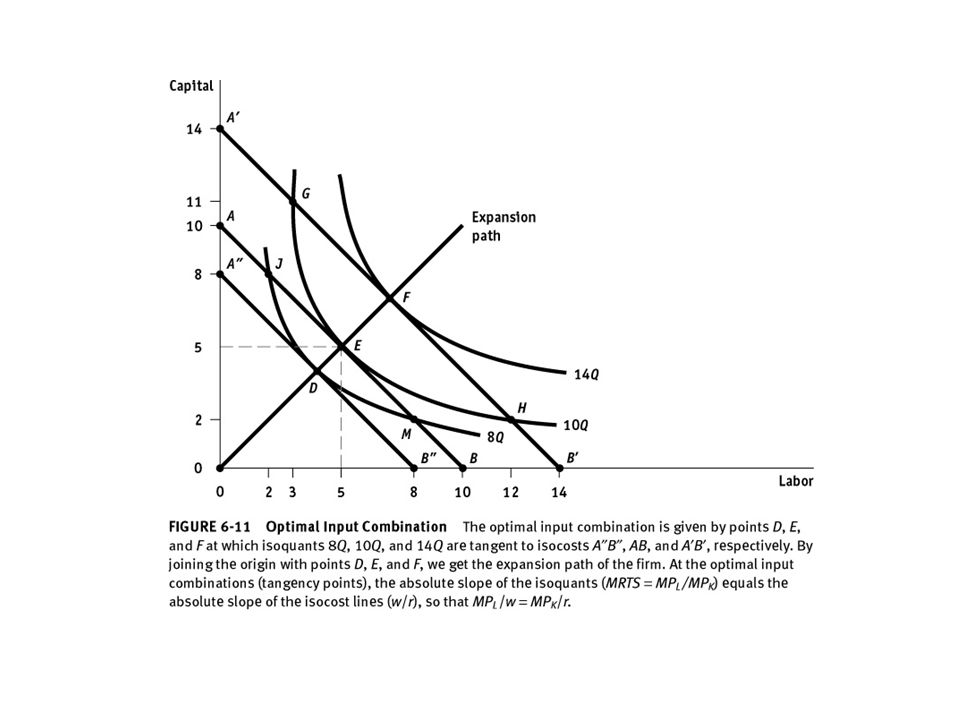

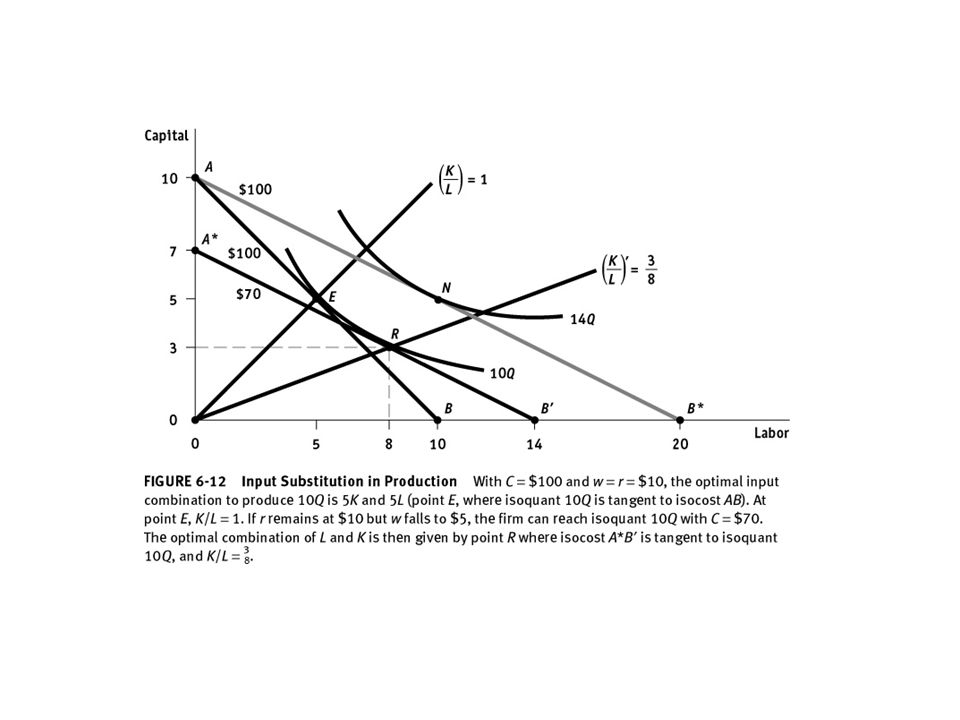

Isocost lines represent all combinations of two inputs that a firm can purchase with the same total cost.

40

Optimal combination of multiple inputs

Production and Costs Optimal combination of multiple inputs Optimal combination corresponds to the point of tangency of the isoquant and isocost. Units of Y B 3 B 2 B 1 Expansion path Y 3 C Y 2 B Y 1 A Q 3 Q 2 Q 1 X 1 X 2 X 3 Units of X

41

Optimal combination of multiple inputs

Production and Costs Optimal combination of multiple inputs Budget Lines Least-cost production occurs when MPX/PX = MPY/PY and PX/PY = MPX/MPY Expansion Path Shows efficient input combinations as output grows. Illustration of Optimal Input Proportions Input proportions are optimal when no additional output could be produced for the same cost. Optimal input proportions is a necessary but not sufficient condition for profit maximization. Optimal combination corresponds to the point of tangency isoquant and isocost. Units of Y B 3 B 2 B 1 Expansion path Y 3 Y 2 C Y B 1 A Q 3 Q 2 Q 1 X 1 X 2 X 3 Units of X

42

Optimal combination of multiple inputs

Production and Costs Optimal combination of multiple inputs Profits are maximized when MRPX = PX for all inputs. Profit maximization requires optimal input proportions plus an optimal level of output. Optimal combination corresponds to the point of tangency isoquant and isocost. Units of Y B 3 B 2 B 1 Expansion path Y 3 Y 2 C Y B 1 A Q 3 Q 2 Q 1 X 1 X 2 X 3 Units of X

45

Production Function Q = f(L, K)

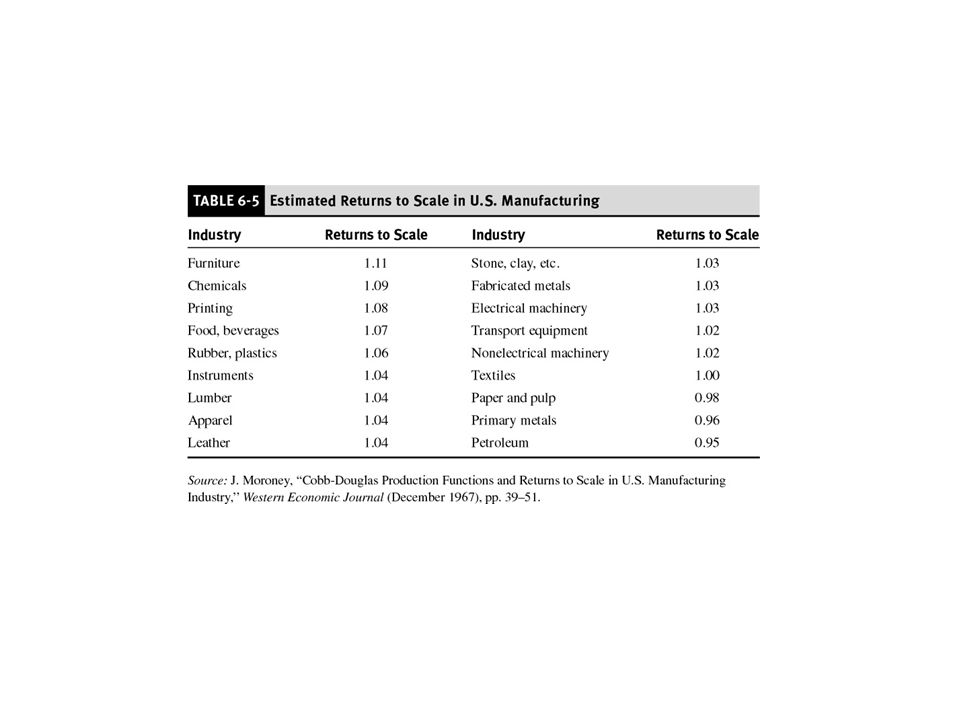

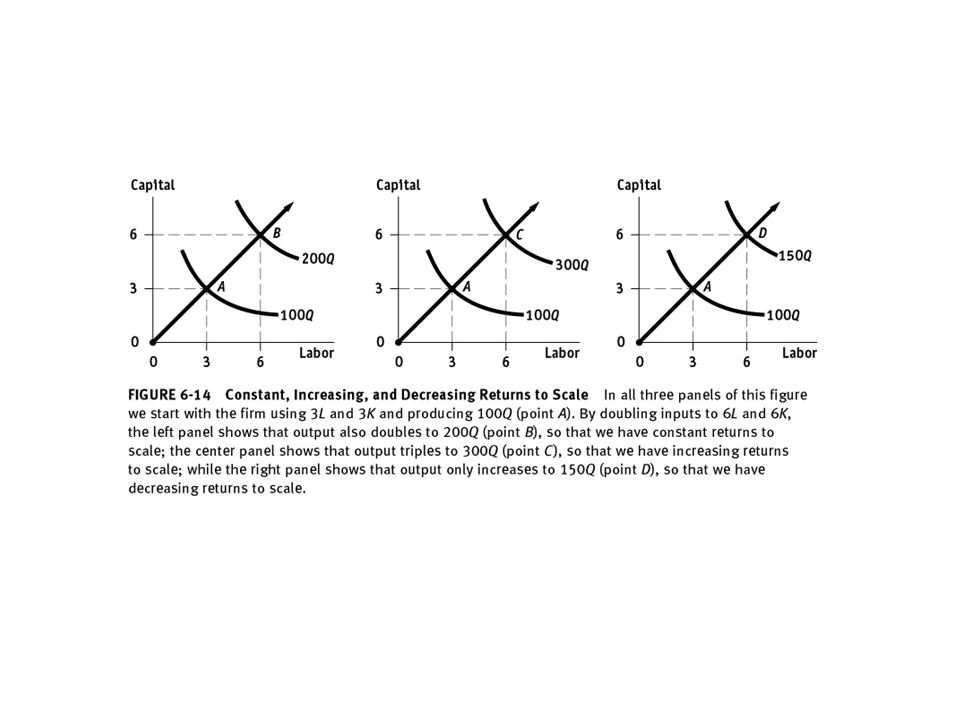

Returns to Scale Production Function Q = f(L, K) Q = f(hL, hK) If = h, then f has constant returns to scale. If > h, then f has increasing returns to scale. If < h, then f has decreasing returns to scale.

Q = f(hL, hK) If = h, then f has constant returns to scale. If > h, then f has increasing returns to scale. If < h, then f has decreasing returns to scale.")

46

Returns to Scale Measuring the relationship between the scale (size) of a firm and output 1) Increasing returns to scale: output more than doubles when all inputs are doubled Larger output associated with lower cost (autos) One firm is more efficient than many (utilities) The isoquants get closer together 74

Increasing returns to scale: output more than doubles when all inputs are doubled. Larger output associated with lower cost (autos) One firm is more efficient than many (utilities) The isoquants get closer together. 74.")

47

Returns to Scale Increasing Returns:

The isoquants move closer together 5 10 2 4 A Capital (machine hours) 10 20 30 Labor (hours) 75

Labor (hours) 75.")

48

Returns to Scale Measuring the relationship between the scale (size) of a firm and output 2) Constant returns to scale: output doubles when all inputs are doubled Size does not affect productivity May have a large number of producers Isoquants are equidistant apart 76

Constant returns to scale: output doubles when all inputs are doubled. Size does not affect productivity. May have a large number of producers. Isoquants are equidistant apart. 76.")

49

Returns to Scale 10 20 30 15 5 10 2 4 A 6 Constant Returns:

Capital (machine hours) 15 5 10 2 4 A 6 Constant Returns: Isoquants are equally spaced Labor (hours) 75

A. 6. Constant Returns: Isoquants are equally spaced. Labor (hours) 75.")

50

Returns to Scale Measuring the relationship between the scale (size) of a firm and output 3) Decreasing returns to scale: output less than doubles when all inputs are doubled Decreasing efficiency with large size Reduction of entrepreneurial abilities Isoquants become farther apart 78

Decreasing returns to scale: output less than doubles when all inputs are doubled. Decreasing efficiency with large size. Reduction of entrepreneurial abilities. Isoquants become farther apart. 78.")

51

Returns to Scale 5 10 2 4 A 10 20 30 Decreasing Returns:

Capital (machine hours) 5 10 2 4 A 10 20 30 Decreasing Returns: Isoquants get further apart Labor (hours) 75

A Decreasing Returns: Isoquants get further. apart. Labor (hours) 75.")

52

Decreasing returns to scale

If an increase in all inputs in the same proportion k leads to an increase of output of a proportion less than k, we have decreasing returns to scale. Example: If we increase the inputs to a dairy farm (cows, land, barns, feed, labor, everything) by 50% and milk output increases by only 40%, we have decreasing returns to scale in dairy farming. This is also known as "diseconomies of scale," since production is less cheap when the scale is larger. Constant returns to scale If an increase in all inputs in the same proportion k leads to an increase of output in the same proportion k, we have constant returns to scale. Example: If we increase the number of machinists and machine tools each by 50%, and the number of standard pieces produced increases also by 50%, then we have constant returns in machinery production. Increasing returns to scale If an increase in all inputs in the same proportion k leads to an increase of output of a proportion greater than k, we have increasing returns to scale. Example: If we increase the inputs to a software engineering firm by 50% output and increases by 60%, we have increasing returns to scale in software engineering. (This might occur because in the larger work force, some programmers can concentrate more on particular kinds of programming, and get better at them). This is also known as "economies of scale," since production is cheaper when the scale is larger.

by 50% and milk output increases by only 40%, we have decreasing returns to scale in dairy farming. This is also known as diseconomies of scale, since production is less cheap when the scale is larger. Constant returns to scale. If an increase in all inputs in the same proportion k leads to an increase of output in the same proportion k, we have constant returns to scale. Example: If we increase the number of machinists and machine tools each by 50%, and the number of standard pieces produced increases also by 50%, then we have constant returns in machinery production. Increasing returns to scale. If an increase in all inputs in the same proportion k leads to an increase of output of a proportion greater than k, we have increasing returns to scale. Example: If we increase the inputs to a software engineering firm by 50% output and increases by 60%, we have increasing returns to scale in software engineering. (This might occur because in the larger work force, some programmers can concentrate more on particular kinds of programming, and get better at them). This is also known as economies of scale, since production is cheaper when the scale is larger.")

53

Determine the returns to scale of the following production functions:

1. F (z1, z2) = [z12 + z22]1/2. 2. F (z1, z2) = (z1 + z2)1/2. 3. F (z1, z2) = z11/2 + z2. F (z1, 2) = [2z12 + 2z22]1/2 = (2)1/2(z12 + z22)1/2 = F (z1, z2). Thus this production function has CRTS. F (z1, z2) = (z1 + z2)1/2 = 1/2(z1 + z2)1/2 = 1/2F (z1, z2). Thus this production function has DRTS. F (z1, z2) = 1/2z11/2 + z2 < (z11/2 + z2) = F (z1, z2) for > 1. Thus this production function has DRTS

= [z12 + z22]1/2. 2. F (z1, z2) = (z1 + z2)1/2. 3. F (z1, z2) = z11/2 + z2. F (z1, 2) = [2z12 + 2z22]1/2 = (2)1/2(z12 + z22)1/2 = F (z1, z2). Thus this production function has CRTS. F (z1, z2) = (z1 + z2)1/2 = 1/2(z1 + z2)1/2 = 1/2F (z1, z2). Thus this production function has DRTS. F (z1, z2) = 1/2z11/2 + z2 < (z11/2 + z2) = F (z1, z2) for > 1. Thus this production function has DRTS.")

56

Empirical Production Functions

Cobb-Douglas Production Function Q = AKaLb Estimated Using Natural Logarithms ln Q = ln A + a ln K + b ln L

57

Cobb-Douglas Production Function Example: Q = F(K,L) = K.5 L.5

K is fixed at 16 units. Short run production function: Q = (16).5 L.5 = 4 L.5 Production when 100 units of labor are used? Q = 4 (100).5 = 4(10) = 40 units

.5 L.5 = 4 L.5. Production when 100 units of labor are used Q = 4 (100).5 = 4(10) = 40 units.")

58

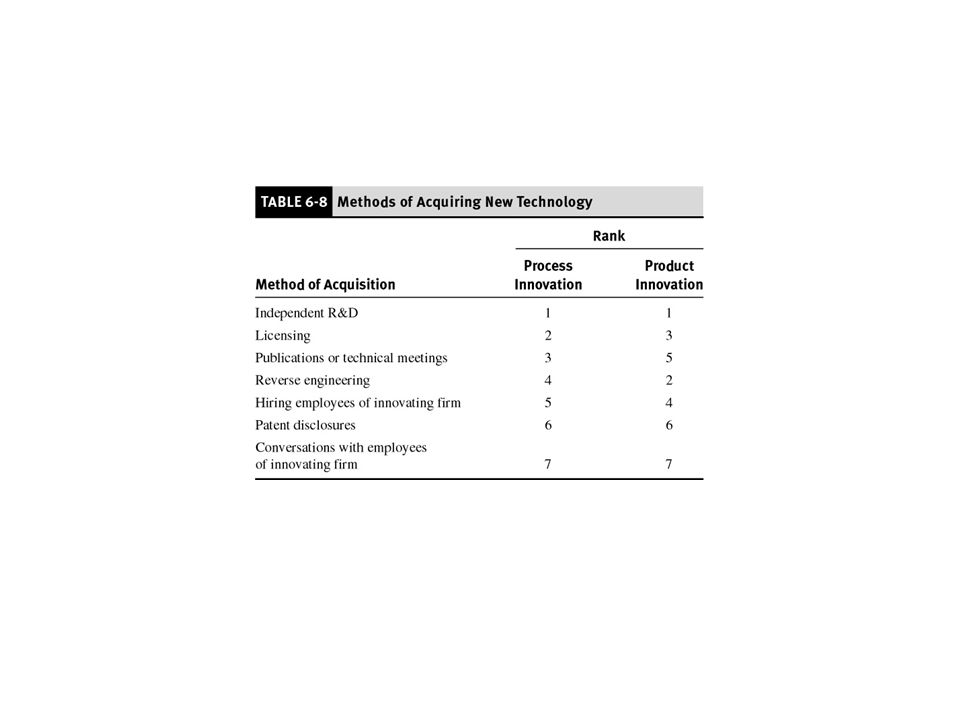

Innovations and Global Competitiveness

Product Innovation Process Innovation Product Cycle Model Just-In-Time Production System Competitive Benchmarking Computer-Aided Design (CAD) Computer-Aided Manufacturing (CAM) PowerPoint Slides Prepared by Robert F. Brooker, Ph.D. Slide 58

Computer-Aided Manufacturing (CAM) PowerPoint Slides Prepared by Robert F. Brooker, Ph.D. Slide 58.")

Similar presentations

Firm’s costs of production: Accounting costs: actual dollars spent on labor, rental price of bldg, etc. Economic costs: includes.>")

Production.>")