Download presentation

Presentation is loading. Please wait.

1

Applied Econometric Time Series Third Edition

Walter Enders, University of Alabama Copyright © 2010 John Wiley & Sons, Inc.

2

Chapter 4 MODELS WITH TREND

3

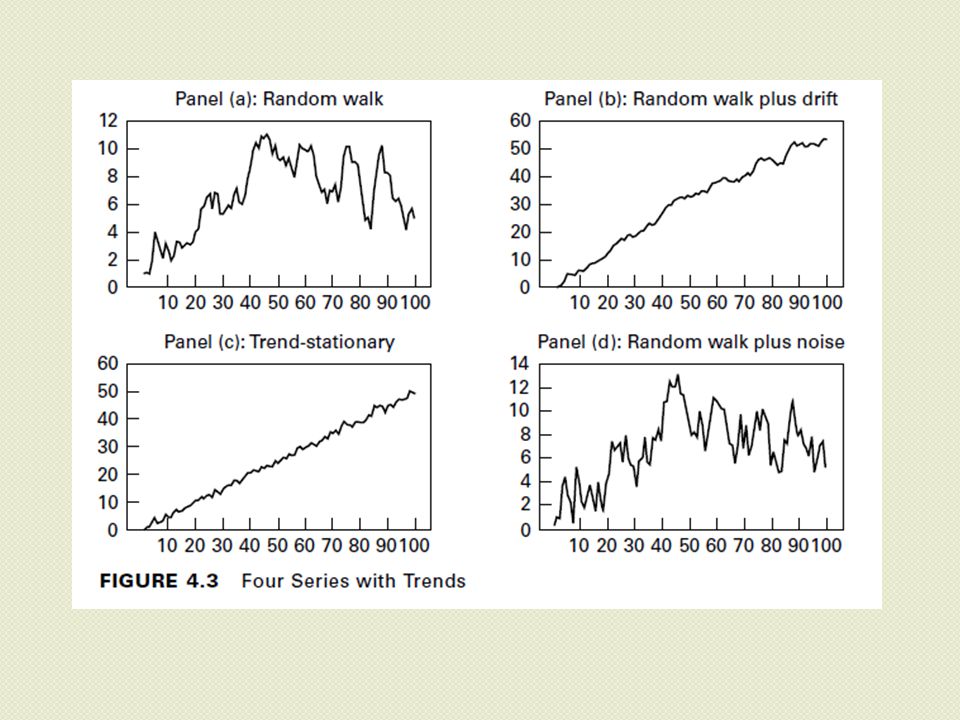

1. DETERMINISTIC AND STOCHASTIC TRENDS

The Random Walk Model The Random Walk Plus Drift Model Generalizations of the Stochastic Trend Model

7

2. REMOVING THE TREND Differencing Detrending

Difference versus Trend-Stationary Models Are There Business Cycles? The Trend in Real GDP

11

3. UNIT ROOTS AND REGRESSION RESIDUALS

12

4. THE MONTE CARLO METHOD Monte Carlo Experiments

Example of the Monte Carlo Method Generating the Dickey–Fuller Distribution

15

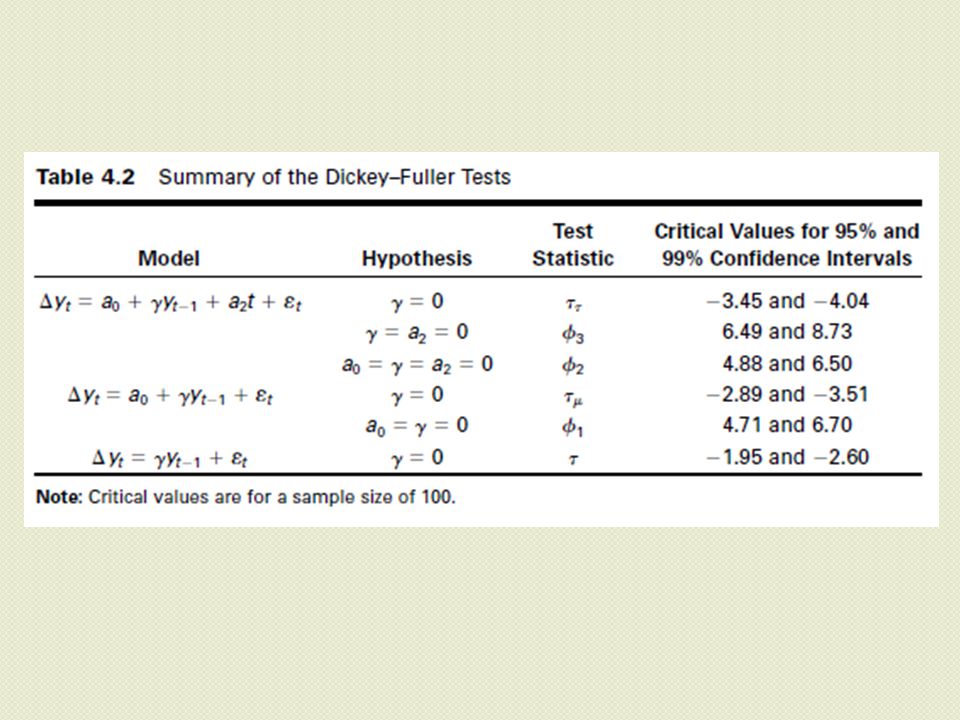

5. DICKEY–FULLER TESTS An Example

17

6. EXAMPLES OF THE DICKEY–FULLER TEST

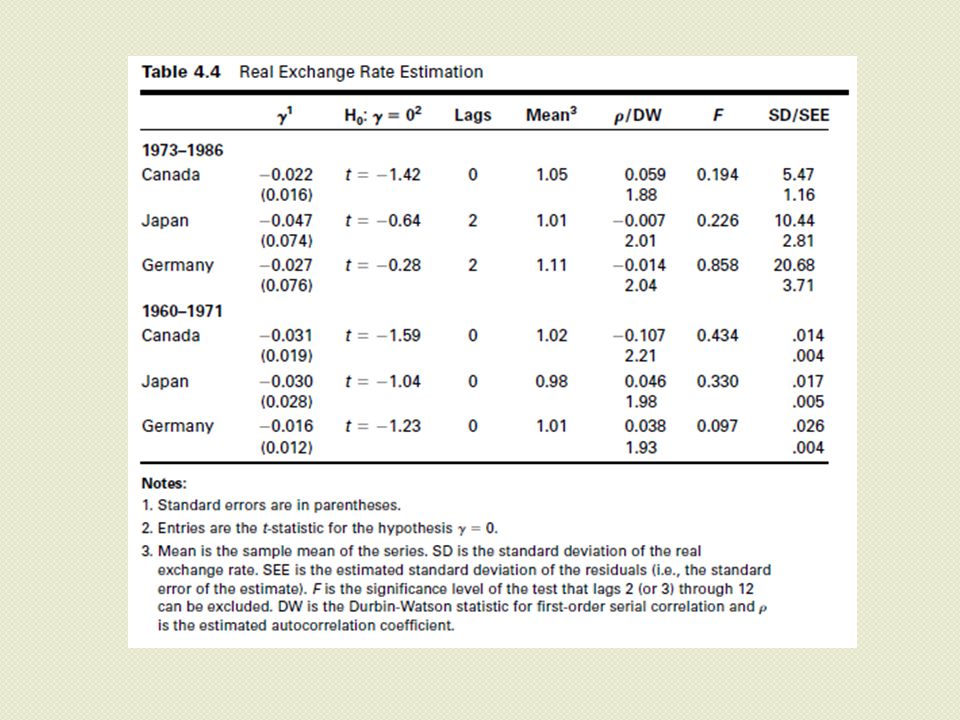

Quarterly Real U.S. GDP Unit Roots and Purchasing Power Parity

21

7. EXTENSIONS OF THE DICKEY–FULLER TEST

Selection of the Lag Length The Test with MA Components Lag Lengths and Negative MA Terms Multiple Roots Seasonal Unit Roots

24

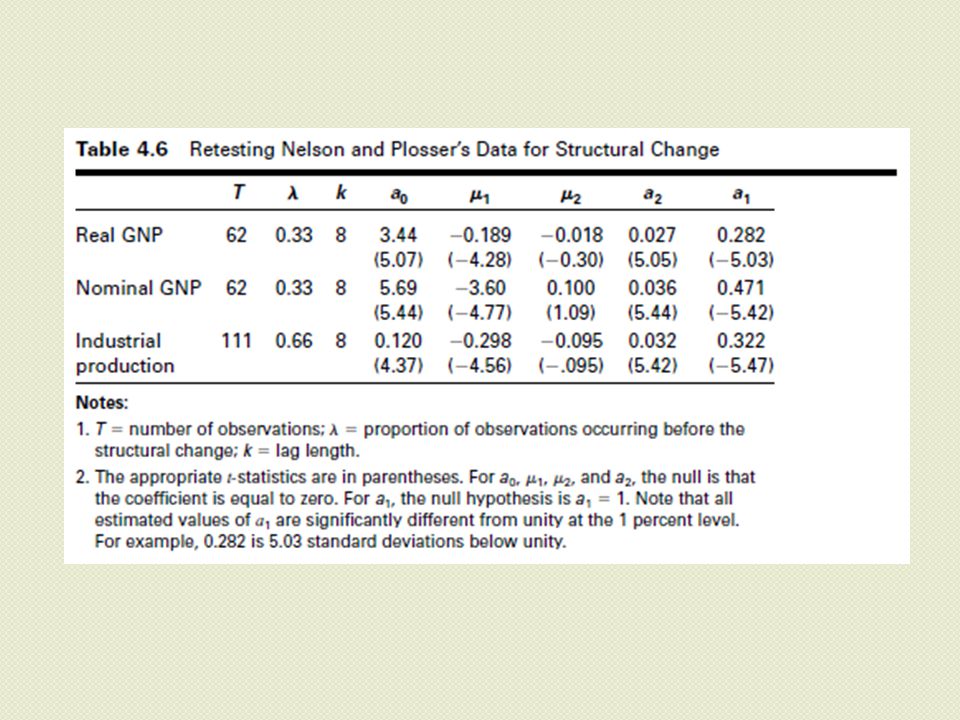

8. STRUCTURAL CHANGE Perron’s Test for Structural Change

Perron’s Test and Real Output Tests with Simulated Data

28

9. POWER AND THE DETERMINISTIC REGRESSORS

Determination of the Deterministic Regressors

30

10. TESTS WITH MORE POWER An Example

31

11. PANEL UNIT ROOT TESTS Limitations of the Panel Unit Root Test

34

12. TRENDS AND UNIVARIATE DECOMPOSITIONS

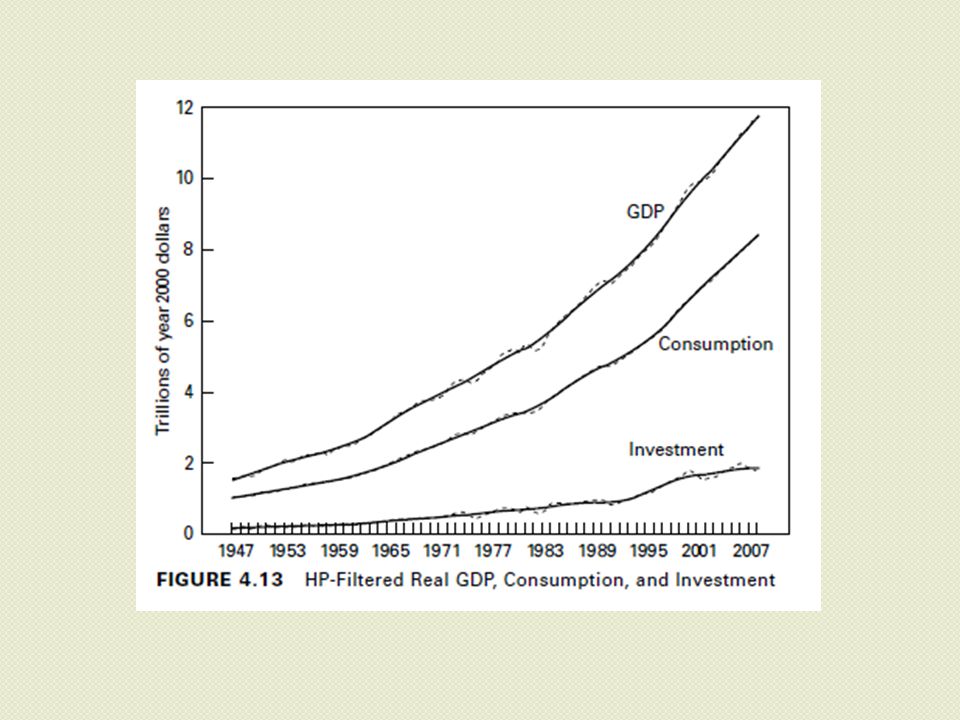

The General ARIMA (p, 1, q) Model The Unobserved Components Decomposition The Hodrick–Prescott Decomposition

Model. The Unobserved Components Decomposition. The Hodrick–Prescott Decomposition.")

36

13. SUMMARY AND CONCLUSIONS

37

APPENDIX 4.1: THE BOOTSTRAP

Bootstrapping Regression Coefficients

38

APPENDIX 4.2: DETERMINATION OF THE DETERMINISTIC REGRESSORS

GDP and Unit Roots

Similar presentations

: You are free to use and modify these slides for educational purposes, but please if you improve this material send us your new.>")

Material.>")

Slideshow: nonstationary processes Original citation: Dougherty, C. (2012) EC220.>")