Download presentation

Presentation is loading. Please wait.

1

Unit Root Tests: Methods and Problems

Roger Perman Applied Econometrics Lecture 12

2

How do you find out if a series is stationary or not?

Unit Root Tests How do you find out if a series is stationary or not?

3

Y = b0 + Y + e ® I (1) D Y = Y - Y = b0 + e ® I (0)

Order of Integration of a Series A series which is stationary after being differenced once is said to be integrated of order 1 and is denoted by I(1). In general a series which is stationary after being differenced d times is said to be integrated of order d, denoted I(d). A series, which is stationary without differencing, is said to be I(0) Y = b0 + Y + e I (1) t t - 1 t D Y = Y - Y = b0 + e I (0) t t t - 1 t

. In general a series which is stationary after being. differenced d times is said to be integrated of order d, denoted I(d). A series, which is stationary without. differencing, is said to be I(0) Y. = b0. + Y. + e. I. (1) t. t t. D. Y. = Y. - Y. = b0. + e. I. (0) t. t. t t.")

4

Informal Procedures to identify non-stationary processes

(1) Eye ball the data (a) Constant mean? (b) Constant variance?

Eye ball the data (a) Constant mean (b) Constant variance")

5

Informal Procedures to identify non-stationary processes

(2) Diagnostic test - Correlogram Correlation between 1980 and k. For stationary process correlogram dies out rapidly. Series has no memory is not related to 1985.

Diagnostic test - Correlogram. Correlation between 1980 and k. For stationary process correlogram dies out rapidly. Series has no memory is not related to")

6

Informal Procedures to identify non-stationary processes

(2) Diagnostic test - Correlogram For a random walk the correlogram does not die out. High autocorrelation for large values of k

Diagnostic test - Correlogram. For a random walk the correlogram does not die out. High autocorrelation for large values of k.")

7

Statistical Tests for stationarity: Simple t-test

Set up AR(1) process with drift (b0) Yt = b0 + b1Yt-1 + t t ~ iid(0,σ2) (1) Simple approach is to estimate eqn (1) using OLS and examine estimated b1 Use a t-test with null Ho: b1 = 1 (non-stationary) against alternative Ha: b1 < 1 (stationary). Test Statistic: TS = (b1 – 1) / (Std. Err.(b1)) reject null hypothesis when test statistic is large negative - 5% critical value is -1.65

process with drift (b0) Yt = b0 + b1Yt-1 + t t ~ iid(0,σ2) (1) Simple approach is to estimate eqn (1) using OLS and examine estimated b1. Use a t-test with null Ho: b1 = 1 (non-stationary) against alternative Ha: b1 < 1 (stationary). Test Statistic: TS = (b1 – 1) / (Std. Err.(b1)) reject null hypothesis when test statistic is large negative. - 5% critical value is")

8

Statistical Tests for stationarity: Simple t-test

Simple t-test based on AR(1) process with drift (b0) Yt = b0 + b1Yt-1 + t t ~ iid(0,σ2) (1) Problem with simple t-test approach (1) lagged dependent variables => b1 biased downwards in small samples (i.e. dynamic bias) (2) When b1 =1, we have non-stationary process and standard regression analysis is invalid (i.e. non-standard distribution)

process with drift (b0) Yt = b0 + b1Yt-1 + t t ~ iid(0,σ2) (1) Problem with simple t-test approach. (1) lagged dependent variables => b1 biased downwards in small samples (i.e. dynamic bias) (2) When b1 =1, we have non-stationary process and standard regression analysis is invalid. (i.e. non-standard distribution)")

9

Dickey Fuller (DF) approach to non- stationarity testing

Dickey and Fuller (1979) suggest we subtract Yt-1 from both sides of eqn. (1) Yt - Yt-1 = b0 + b1Yt-1 - Yt-1 + t t ~ iid(0,σ2) ΔYt = b0 + Yt-1 + t = b1 – (2) Use a t-test with: null Ho: = 0 (non-stationary or Unit Root) against alternative Ha: < 0 (stationary). - Large negative test statistics reject non- stationarity - This is known as unit root test since in eqn. (1) Ho: b1 =1.

suggest we subtract Yt-1 from both sides of eqn. (1) Yt - Yt-1 = b0 + b1Yt-1 - Yt-1 + t t ~ iid(0,σ2) ΔYt = b0 + Yt-1 + t = b1 –1 (2) Use a t-test with: null Ho: = 0 (non-stationary or Unit Root) against alternative Ha: < 0 (stationary). - Large negative test statistics reject non- stationarity. - This is known as unit root test since in eqn. (1) Ho: b1 =1.")

10

The difference between the three regressions concerns the

Variants of DF test Three different regression can be used to test the presence of a unit root The difference between the three regressions concerns the presence of deterministic elements b0 and b2t. 1 – For testing if Y is a pure Random Walk 2 – For testing if Y is a Random Walk with Drift 3 – For testing if Y is a Random walk with Drift and Deterministic Trend

11

The simplest model (appropriate only if you think there are no

other terms present in the ‘true’ regression model) Use the t statistic and compare it with the the table of critical values computed by Dickey and Fuller. If your t value is outside the confidence interval, the null hypothesis of unit root is rejected Statistic

Use the t statistic and compare it with the the table of critical values computed by Dickey and Fuller. If your t value is outside the confidence interval, the null hypothesis of unit root is rejected. Statistic.")

12

A more general model (allowing for ‘drift’)

Statistic - Use the F statistic to check if = b0 = 0 using the non standard tables Statistic - use the t statistic to check if =0 , again using non-standard tables

13

Example Sample size of n = 25 at 5% level of significance for eqn. (2) τμ-critical value = t-test critical value = -1.65 Δpt-1 = pt-1 (-1.05) (-1.49) = τμ = > -3.00 hence cannot reject H0 and so unit root.

(-1.49) = τμ = > hence cannot reject H0 and so unit root.")

14

Incorporating time trends in DF test for unit root

Some time series clearly display an upward or downward trend (non-stationary mean). Should therefore incorporate trend in the regression used for the DF test. ΔYt = b0 + Yt-1 + b2 trend + t (4) It may be the case that Yt will be stationary around a trend. Although if a trend is not included series is non-stationary.

. Should therefore incorporate trend in the regression used for the DF test. ΔYt = b0 + Yt-1 + b2 trend + t (4) It may be the case that Yt will be stationary around a trend. Although if a trend is not included series is non-stationary.")

15

ττ ΔYt = b0 + βYt-1 + b2 trend + t

Different DF tests – Summary t-type test ττ ΔYt = b0 + βYt-1 + b2 trend + t (a) Ho: β = 0 Ha: β < 0 τμ ΔYt = b0 + βYt-1 + t (b) Ho: β = 0 Ha: β < 0 τ ΔYt = βYt-1 + t (c) Ho: β = 0 Ha: β < 0 Critical values from Fuller (1976)

Ho: β = 0 Ha: β < 0. τμ ΔYt = b0 + βYt-1 + t. (b) Ho: β = 0 Ha: β < 0. τ ΔYt = βYt-1 + t. (c) Ho: β = 0 Ha: β < 0. Critical values from Fuller (1976)")

16

Φ3 ΔYt = b0 + Yt-1 + b2 trend + t

Different DF tests – Summary F-type test Φ3 ΔYt = b0 + Yt-1 + b2 trend + t (a) Ho: β = b2 = 0 Ha: 0 and/or b2 0 Φ1 ΔYt = b0 + Yt-1 + t (b) Ho: = b0 = 0 Ha: 0 and/or b0 0 Critical values from Dickey and Fuller (1981)

Ho: β = b2 = 0 Ha: 0 and/or b2 0. Φ1 ΔYt = b0 + Yt-1 + t. (b) Ho: = b0 = 0 Ha: 0 and/or b0 0. Critical values from Dickey and Fuller (1981)")

17

Summary of Dickey-Fuller Tests

(Critical values for n = 100)

")

18

Augmented Dickey Fuller (ADF) test for unit root

Dickey Fuller tests assume that the residuals t in the DF regression are non- autocorrelated. Solution: incorporate lagged dependent variables. For quarterly data add up to four lags. ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + θ4ΔYt-4 + t (3) Problem arises of differentiating between models. Use a general to specific approach to eliminate insignificant variables Check final parsimonious model for autocorrelation. Check F-test for significant variables Use Information Criteria. Trade-off parsimony vs. residual variance.

Problem arises of differentiating between models. Use a general to specific approach to eliminate insignificant variables. Check final parsimonious model for autocorrelation. Check F-test for significant variables. Use Information Criteria. Trade-off parsimony vs. residual variance.")

19

Consider The Following Series and Its Correlogram

This variable Y is clearly trended and you have to determine if this trend is stochastic or deterministic. After having created the difference variable Y estimate the following model, with as many lags of Y as you think appropriate. (in the example I choose 4 lags of the variable Y)

")

23

Choose Between Alternative Models - The Model-Progress Results

Both the F-Test and the Schwarz Information Criteria indicates that MODEL 4 is the one to be preferred

24

To do this perform an F-Test and use the statistic

Unit Root Testing After having estimated, according to the previous analysis, the following equation the relevant hypotheses to examine are (in this particular case) H : b , b , b = b , , 2 v H : b , b , b b , , 1 2 To do this perform an F-Test and use the statistic

H. : b. , b. , b. = b. , , 2. v. H. : b. , b. , b. b. , , To do this perform an F-Test and use the statistic.")

25

PcGive output of test result:

Wald test for linear restrictions: Subset LinRes F( 2,493) = [0.0066] ** Be careful here. The value is not significant at the 5% critical value, although PcGive marks it as significant (it is using the conventional F distribution). Therefore we cannot reject the null hypothesis, and so infer that we do not have a deterministic time trend in the equation. Hence, we can continue the analysis using and then use statistic - use the F statistic to check if = b0 = 0 using the non standard tables statistic - use the t statistic to check if =0 , again using non-standard tables

= [0.0066] ** Be careful here. The value is not significant at the 5% critical value, although PcGive marks it as significant (it is using the conventional F distribution). Therefore we cannot reject the null hypothesis, and so infer that we do not have a deterministic time trend in the equation. Hence, we can continue the analysis using. and then use. statistic - use the F statistic to check if = b0 = 0 using the. non standard tables. statistic - use the t statistic to check if =0 , again using. non-standard tables.")

26

The t-stat cannot reject the null hypothesis of Unit Root while the F-stat

rejects the null hypothesis that the drift is equal to zero. Therefore we can conclude that the model most likely to describe the true DGP is

27

Reject Accept Reject Accept Reject Accept Reject Accept

Look at the Series – Is there a Trend? Yes No Estimate Estimate Use Use to test to test H : b , b = , H : b , b , b = b , , 2 v v H : b , b , b 1 H : b , b , b , , 1 2 Reject Accept Reject Accept test =0 using the t-stat. from step 1 using Pure Random Walk test =0 using the t-stat. from step 1 using Reject Accept Reject Accept No Unit Root Unit Root +Trend Stable Series, use normal test to check the drift Random Walk + Drift Use Normal Test procedure to determine the presence of Time trend or Drift To determine if there is a drift as well

28

Alternative statistical test for stationarity

One further approach is the Sargan and Bhargava (1983) test which uses the Durbin-Watson statistic. If Yt is regressed on a constant alone, we then examine the residuals for serial correlation. Serial correlation in the residuals (long memory) will fail the DW test and result in a low value for this test. This test has not proven so popular.

test which uses the Durbin-Watson statistic. If Yt is regressed on a constant alone, we then examine the residuals for serial correlation. Serial correlation in the residuals (long memory) will fail the DW test and result in a low value for this test. This test has not proven so popular.")

29

Testing Strategy for Unit Roots

Three main aspects of Unit root testing - Deterministic components (constant, time trend). - ADF Augmented Dickey Fuller test - lag length - use F-test or Schwarz Information Criteria - In what sequence should we test? - Phi and tau tests

. - ADF Augmented Dickey Fuller test - lag length. - use F-test or Schwarz Information Criteria. - In what sequence should we test - Phi and tau tests.")

30

Testing Strategy for Unit Roots

Formal Strategy (A) Set up Model (1) Use informal tests – eye ball data and correlogram (2) Incorporate Time trend if data is upwards trending (3) Specification of ADF test – how many lags should we incorporate to avoid serial correlation?

Set up Model. (1) Use informal tests – eye ball data and correlogram. (2) Incorporate Time trend if data is upwards trending. (3) Specification of ADF test. – how many lags should we incorporate to avoid serial correlation")

31

Example- Real GDP (2000 Prices) Seasonally Adjusted

(1) Plot Time Series - Non-Stationary (i.e. time varying mean and correlogram non-zero) GDP Time r k

Plot Time Series - Non-Stationary. (i.e. time varying mean and correlogram non-zero) GDP. Time. r. k.")

32

(1) Plot First Difference of Time Series - Stationary

Unit Root Testing (1) Plot First Difference of Time Series - Stationary (i.e. constant mean and correlogram zero) Time r k

Plot First Difference of Time Series - Stationary. (i.e. constant mean and correlogram zero) Time. r. k.")

33

Unit Root Testing (2) Incorporate Linear Trend since data is trending upwards

Incorporate Linear Trend since data is trending upwards")

34

(3) Determine Lag length of ADF test

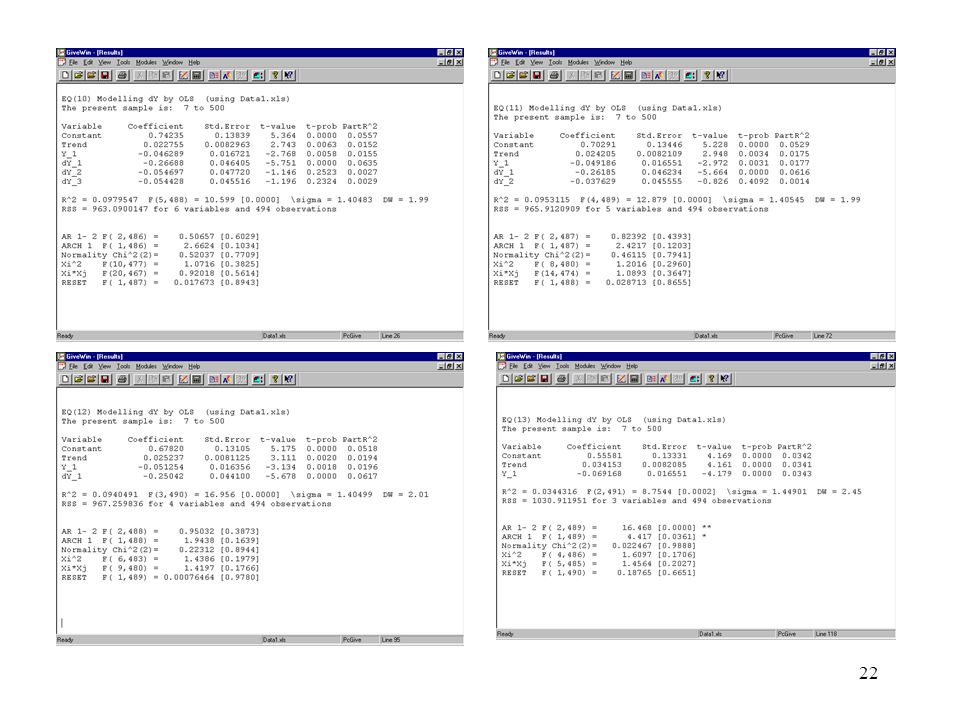

Unit Root Testing (3) Determine Lag length of ADF test Estimate general model and test for serial correlation EQ ( 1) ΔYt = b0 +b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + θ4ΔYt-4 + t EQ( 1) Modelling DY by OLS (using Lab2.in7) The estimation sample is: 1956 (2) to 2003 (3) n = 190 Coefficient Std.Error t-value t-prob Part.R^2 Constant Trend Y_ DY_ DY_ DY_ DY_ AR 1-5 test: F(5,178) = [0.1308] Test accepts null of no serial correlation. Nevertheless we use F-test and Schwarz Criteria to check model.

Determine Lag length of ADF test. Estimate general model and test for serial correlation. EQ ( 1) ΔYt = b0 +b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + θ4ΔYt-4 + t. EQ( 1) Modelling DY by OLS (using Lab2.in7) The estimation sample is: 1956 (2) to 2003 (3) n = 190. Coefficient Std.Error t-value t-prob Part.R^2. Constant Trend Y_ DY_ DY_ DY_ DY_ AR 1-5 test: F(5,178) = [0.1308] Test accepts null of no serial correlation. Nevertheless we use F-test and Schwarz Criteria to check model.")

35

(3) Determine Lag length of ADF test

Unit Root Testing (3) Determine Lag length of ADF test Model EQ ( 1) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + θ4ΔYt-4 + t EQ ( 2) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t EQ ( 3) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + t EQ ( 4) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + t EQ ( 5) ΔYt = b0+b2 trend+ Yt-1 + t Use both the F-test and the Schwarz information Criteria (SC). Reduce number of lags where F-test accepts. Choose equation where SC is the lowest i.e. minimise residual variance and number of estimated parameters.

Determine Lag length of ADF test. Model. EQ ( 1) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + θ4ΔYt-4 + t. EQ ( 2) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t. EQ ( 3) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + t. EQ ( 4) ΔYt = b0+b2 trend+ Yt-1 + θ1ΔYt-1 + t. EQ ( 5) ΔYt = b0+b2 trend+ Yt-1 + t. Use both the F-test and the Schwarz information Criteria (SC). Reduce number of lags where F-test accepts. Choose equation where SC is the lowest. i.e. minimise residual variance and number of estimated parameters.")

36

(3) Determine Lag length of ADF test

Unit Root Testing (3) Determine Lag length of ADF test Progress to date Model T p log-likelihood Schwarz Criteria EQ( 1) OLS EQ( 2) OLS EQ( 3) OLS EQ( 4) OLS EQ( 5) OLS Tests of model reduction EQ( 1) --> EQ( 2): F(1,183) = [0.5259] Accept model reduction EQ( 1) --> EQ( 3): F(2,183) = [0.0357]* Reject model reduction EQ( 1) --> EQ( 4): F(3,183) = [0.0173]* EQ( 1) --> EQ( 5): F(4,183) = [0.0374]* Some conflict in results. F-tests suggest equation (2) is preferred to equation (1) and equation (3) is not preferred to equation (2). Additionally, the relative performance of these three equations is confirmed by information criteria. Therefore adopt equation (2).

Determine Lag length of ADF test. Progress to date. Model T p log-likelihood Schwarz Criteria. EQ( 1) OLS EQ( 2) OLS EQ( 3) OLS EQ( 4) OLS EQ( 5) OLS Tests of model reduction. EQ( 1) --> EQ( 2): F(1,183) = [0.5259] Accept model reduction. EQ( 1) --> EQ( 3): F(2,183) = [0.0357]* Reject model reduction. EQ( 1) --> EQ( 4): F(3,183) = [0.0173]* EQ( 1) --> EQ( 5): F(4,183) = [0.0374]* Some conflict in results. F-tests suggest equation (2) is preferred to equation (1) and equation (3) is not preferred to equation (2). Additionally, the relative performance of these three equations is confirmed by information criteria. Therefore adopt equation (2).")

37

(B) Conduct Formal Tests

Unit Root Testing (B) Conduct Formal Tests EQ( 2) Modelling DY by OLS (using Lab2.in7) The estimation sample is: 1956 (2) to 2003 (3) Coefficient Std.Error t-value t-prob Part.R^2 Constant Trend Y_ DY_ DY_ DY_ AR 1-5 test: F(5,179) = [0.6357] Main issue is serial correlation assumption for this test. Can we accept the null hypothesis of no serial correlation? Yes!

Conduct Formal Tests. EQ( 2) Modelling DY by OLS (using Lab2.in7) The estimation sample is: 1956 (2) to 2003 (3) Coefficient Std.Error t-value t-prob Part.R^2. Constant Trend Y_ DY_ DY_ DY_ AR 1-5 test: F(5,179) = [0.6357] Main issue is serial correlation assumption for this test. Can we accept the null hypothesis of no serial correlation Yes!")

38

Unit Root Testing Apply F-type test - Include time trend in specification Φ3: ΔYt = b0 + b2 trend + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t (a) Ho: = b2 = 0 Ha: β 0 and/or b2 0 PcGive Output : Test/Exclusion Restrictions. Test for excluding: [0] = Trend [1] = Y_1 F(2,184) = < 6.39 = 5% C.V. (by interpolation). Hence accept joint null hypothesis of unit root and no time trend (next test whether drift term is required). NB Critical Values (C.V.) from Dickey and Fuller (1981) for Φ3 Sample Size (n) C.V. at 5%

Ho: = b2 = 0 Ha: β 0 and/or b2 0. PcGive Output : Test/Exclusion Restrictions. Test for excluding: [0] = Trend [1] = Y_1. F(2,184) = 2.29 < 6.39 = 5% C.V. (by interpolation). Hence accept joint null hypothesis of unit root and no time trend. (next test whether drift term is required). NB Critical Values (C.V.) from Dickey and Fuller (1981) for Φ3. Sample Size (n) C.V. at 5%")

39

Φ1: ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t

Unit Root Testing Apply F-type test - Exclude time trend from specification Φ1: ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t (b) Ho: = b0 = 0 Ha: 0 and/or b0 0 PcGive Output : Test/Exclusion Restrictions. Test for excluding: [0] = Constant[1] = Y_1 F(2,185) = > 4.65 = 5% C.V. Hence reject joint null hypothesis of unit root and no drift. NB Critical Values (C.V.) from Dickey and Fuller (1981) for Φ1 Sample Size (n) C.V. at 5%

Ho: = b0 = 0 Ha: 0 and/or b0 0. PcGive Output : Test/Exclusion Restrictions. Test for excluding: [0] = Constant[1] = Y_1. F(2,185) = > 4.65 = 5% C.V. Hence reject joint null hypothesis of unit root and no drift. NB Critical Values (C.V.) from Dickey and Fuller (1981) for Φ1. Sample Size (n) C.V. at 5%")

40

τμ ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t

Unit Root Testing Apply t-type test (τμ) τμ ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t (b) Ho: = 0 Ha: < 0 τμ = > = 5% C.V. Hence accept null of unit root. N.B. Critical Values (C.V.) from Fuller (1976) for τμ Sample Size (n) C.V. at 5%

τμ ΔYt = b0 + Yt-1 + θ1ΔYt-1 + θ2ΔYt-2 + θ3ΔYt-3 + t. (b) Ho: = 0 Ha: < 0. τμ = 1.64 > = 5% C.V. Hence accept null of unit root. N.B. Critical Values (C.V.) from Fuller (1976) for τμ. Sample Size (n) C.V. at 5%")

41

Unit Root Testing EQ(2a) Modelling DY by OLS (using Lab2.in7) The estimation sample is: 1956 (2) to 2003 (3) Coefficient Std.Error t-value t-prob Part.R^2 Constant Y_ DY_ DY_ DY_ AR 1-5 test: F(5,180) = [0.7725] τμ = > (5% C.V.) hence we can not reject the null of unit root.

= [0.7725] τμ = 1.64 > (5% C.V.) hence we can not reject the null of unit root.")

42

Problems With Unit Root Tests

43

Problem Number 1: Structural Breaks

Perron (1989) - He argues that most macroeconomic variables are not unit root processes. They are Trend Stationary with Structural Breaks For example 1929 Depression Oil Shocks Technological Change All these events have changed the mean of a process like GDP If you do not recognize the structural break, you’ll find unit root where there is not With Structural Change All Unit Root Tests Are Biased Towards the Non Rejection of a Unit Root

- He argues that most macroeconomic variables. are not unit root processes. They are Trend Stationary with. Structural Breaks. For example Depression. Oil Shocks. Technological Change. All these events have changed the mean of a process like GDP. If you do not recognize the structural break, you’ll find unit root. where there is not. With Structural Change All Unit Root Tests Are Biased. Towards the Non Rejection of a Unit Root.")

44

The Unit Root Hypothesis is not rejected.

Unit Root Test For Y Dickey-Fuller test for Y; DY on Variable Coefficient Std.Error t-value Y_ \sigma = DW = DW(Y) = DF(Y) = Critical values used in DF test: 5%= %=-2.587 RSS = for 1 variables and 98 observations Information Criteria: SC = HQ = FPE= AIC = The Unit Root Hypothesis is not rejected. Perron proposed a method to overcome this problem - But you need to know when the structural break happened

= DF(Y) = Critical values used in DF test: 5%= %= RSS = for 1 variables and 98 observations. Information Criteria: SC = HQ = FPE= AIC = The Unit Root Hypothesis is not rejected. Perron proposed a method to overcome this problem - But you. need to know when the structural break happened.")

45

Consider The Following Variable

Y = . 5 Y + D + e t t - 1 t for t = . . 49 D = t 2 for t = 50 . . 100

46

The Power of a test is the probability of rejecting a false

Problem Number Two : Low Power The Power of a test is the probability of rejecting a false Null Hypothesis - Unit Root Tests Low Power to Distinguish Between Unit and near Unit Root Low Power to Distinguish Between Trend and Drift Y is a unit root series; Z is a near-unit root series

47

Test result is based on the standard error of

Is = 0 in ΔYt = b0 + Yt-1 + t Test result is based on the standard error of - Measure of how accurate is our estimated coefficient - with increasing observations we become more certain. In this case, power of the test is the ability to reject the null of non-stationarity when it is false (equivalently, the ability to accept alternative hypothesis of stationarity). Low power implies a series may be stationary but Dickey-Fuller test suggests unit root. Low power is especially a problem when series is stationary but close to being unit root. One solution to low power is to increase the number of observations by increasing the span of data. However, there may be differences in economic structure or policy which should be modelled differently. Alternative solution to low power is a number of joint ADF tests. - Take information from a number of countries. - And pool coefficients. (i.e. combine information).

. Low power implies a series may be stationary but Dickey-Fuller test suggests unit root. Low power is especially a problem when series is stationary but close to being unit root. One solution to low power is to increase the number of observations by increasing the span of data. However, there may be differences in economic structure or policy which should be modelled differently. Alternative solution to low power is a number of joint ADF tests. - Take information from a number of countries. - And pool coefficients. (i.e. combine information).")

Similar presentations

Models>")