Download presentation

Presentation is loading. Please wait.

1

OPPORTUNITIES AND ROAD BLOCKS

2

Seafood exports vary between US$ 250 to US$ 275 Million Annually. AUP ( Average Unit Price) US$ 2.00 90% By Volume Exported Products are Un- processed Frozen. 2 Canning Plants in Operation. 1 Bulk Surimi Plant More than 35 Processing Units on Baluchistan Coastal Belt Un-operational.

US$ 2.00 90% By Volume Exported Products are Un- processed Frozen. 2 Canning Plants in Operation. 1 Bulk Surimi Plant More than 35 Processing Units on Baluchistan Coastal Belt Un-operational..")

3

0% Shrimp Aquaculture 10% Or Less Farmed Fish Being Exported Existing Processing Units Running On 25% Capacity Annually. 80% Of Product Landed On Our Harbors End Up at Fish Meal Plants. Use Of Illegal Nets On The Rise. 100% Fishing Boats Carry These Nets. Use of Illegal Nets in Creeks ( natural Hatcheries) going Un checked.

going Un checked..")

4

Ban On Exports To EU Still In Place By Air Shipment Ban to Jeddah, Saudi Arabia. Indonesia bans Products available in their seas. Survey by Norwegian Research Vessel Dr Fridtjof Nansen confirms decline in Fisheries Resources.

6

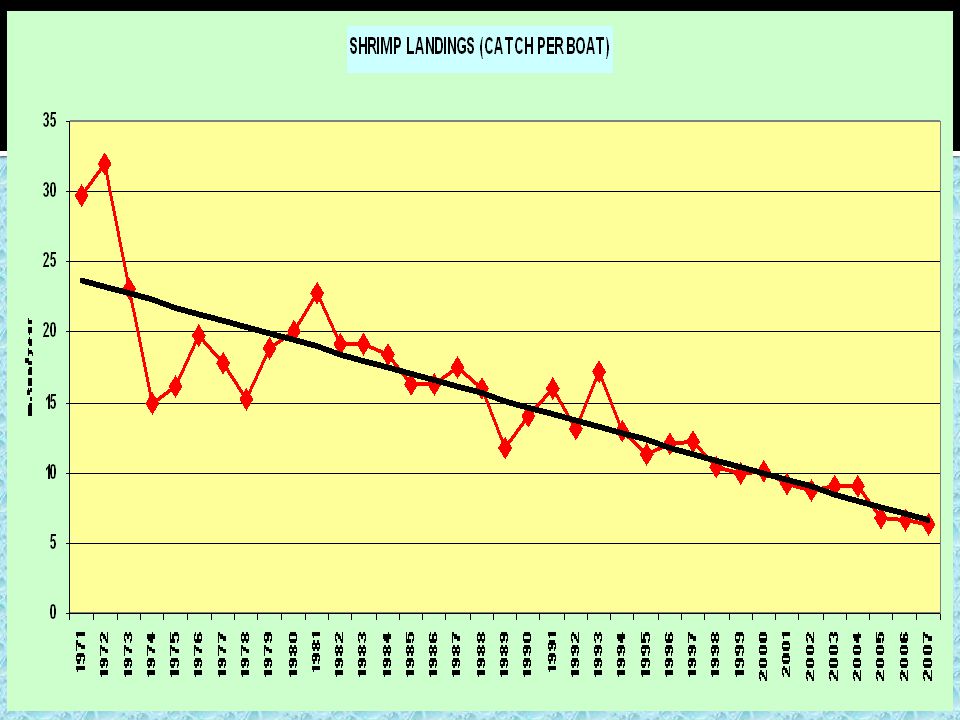

Following Charts Will Explain How Increase In The No. Of Fishing Vessels And Use Of Illegal Nets Have Drastically Reduced Our Raw Material Catch.

7

EXPLODING FLEET SIZE

13

RIBBON FISH CURRENT MARKET PRICE RS 250/KG RED SNAPPER ----- RS. 500/KG POMFRET------ RS. 1500/KG RED SEA BREAM---- RS. 80/KG TONGUE SOLE----- RS 300/KG * PRICES OF EXPORTABLE SIZE.

14

Auction practices and Conditions are at its Worse. Auction done on Un hygienic Floors. Sewerage overflow Market Timings unique. Only Country in the world where Auction is held 9 to 5. Around the world the markets are held from Midnight till before sun rise. ensuring quality.

15

Due to excessive Political Involvement there is ZERO ACCOUNTABILITY. Money meant for Fishermen welfare unscrupulously going into the pockets of the “C” Due to Severe un hygienic Conditions at the harbor product quality is suffering thus reducing Export quantities and increasing rejections at factories.

17

The Port designed to handle 500 fishing vessels now house more than 4000. 100,000 people move on and around the Harbor daily. Impossible to control this huge volumes Authority unable to exert its control Law and order situation not under control.

18

Destruction of Mangroves unchecked. Industrial and Domestic Waste goes to sea Untreated. No waste treatment policy in place. Oil spillages at Commercial Ports Converting Creeks into Housing Projects.

19

WITHOUT A SUSTAINABLE FISHING POLICY THIS INDUSTRY WILL COLLAPSE.

20

All Is Not Bleak in this Sector According to the Survey Of Dr Fridtjof Nansen the Part of the Ocean Touching Our Shores “The Arabian Sea constitutes one of the world’s most unique and complex oceanographic regions and is ranked one of the most biologically productive areas. “

21

Implement Strictly June July Fishing Ban Ban on Use of Illegal Nets. Preservation of Mangroves Implement waste treatment policy.

22

In Order to Take a Quantum Leap in Increasing Our Exports We Need To Focus On Only One Thing AQUA CULTURE

23

Pakistan Is Probably The Only Coastal Country in The World That Has 0% SHRIMP FARMING

24

Fisheries Exports Of India Are Crossing US$ 3 Billion Mark Bangladesh Is Over US$ 1 Billion Vietnam US$ 5 Billion Thailand US$ 10 Billion Iran And Saudi Arabia Have Made Remarkable Headways In Shrimp Farming.

25

These Achievements Have Only Been Possible Due To The Adoption Of A Very Strong Aqua Culture Policy By These Countries.

28

The Game Is Wide Open In This Sector In Order To Sustain Our Industry And Reducing The Pressure On Our Marine Resources We Have To Develop The Aqua Culture Sector. No Need To Invent The Wheel Again Foreign Companies In Our Region Already Involved In This Business Must Be Given An Opportunity to Come and Develop This Sector With Us On JV Basis.

29

There Are Certain Issues that Need to Be Resolved In Order to Jump Start this Sector Enforcing Writ Of The Govt. On The Coastal Belt Investment Friendly Land Lease Policy Govt. Support In Infrastructure Improvement.

30

A 3 Billion Rupees Project in Jeopardy due to Devolution (18 th Amendment) Extremely Important for the future of Fisheries in Pakistan. Need for reorganizing its priorities. Focus on Coastal Belt Emphasis on Shrimp farming Main focus on Poverty Alleviation of fishermen living on the coastal belt.

31

Development Of Cluster Of Farms With Govt. Providing the infrastructure. And Technical Support. Developing a DATA BANK of Experts, Scientists and Technicians Available locally for Private sector use.

32

Once the Raw Material Availability is Guaranteed Through Aqua culture the Processing Industry Will Confidently Invest In Value Addition Equipments to Reinforce their Processing and thus their Profitability.

41

The very Survival of the Fisheries Industry Lies in The Change of Thought Process of the People Involved in this Industry alongwith the Strong Political Will Of The Government To Provide The Enabling Environment for this Sector To Grow.

Similar presentations

N°1005/2008 OF 29 SEPTEMBER 2008 ESTABLISHING.>")

>")