Download presentation

Presentation is loading. Please wait.

1

Mary Bender, REAP Administrator State Conservation Commission Ag Environment Partnership Webinar, March 3, 2009 Welcome to a REAP Update

2

Resource Enhancement and Protection (REAP) Program Mary Bender, REAP Administrator State Conservation Commission

Program Mary Bender, REAP Administrator State Conservation Commission")

3

Overview of Today Presentation Overview of REAP Program Overview of REAP Program REAP FY08-09 Status Summary REAP FY08-09 Status Summary Using/Selling a REAP Tax Credit Using/Selling a REAP Tax Credit Fiscal Year 2009-2010 – What Next? Fiscal Year 2009-2010 – What Next? Compliance Compliance

4

Overview of REAP Program The REAP Program has received funding allocations in the State fiscal year 2007-08 and 2008-09 The REAP Program has received funding allocations in the State fiscal year 2007-08 and 2008-09 Overview of the program Overview of the program

5

REAP FY 2007-08 Overview The FY 2007-08 REAP appropriation was $10 million The FY 2007-08 REAP appropriation was $10 million Applications were accepted by the SCC on Applications were accepted by the SCC on January 2, 2008 on a first come, first served basis January 2, 2008 on a first come, first served basis The entire $10 million was allocated to eligible projects within 10 business days The entire $10 million was allocated to eligible projects within 10 business days Approved REAP Tax Credits continue to be awarded to eligible REAP applicants as the BMP’s are completed. Approved REAP Tax Credits continue to be awarded to eligible REAP applicants as the BMP’s are completed.

6

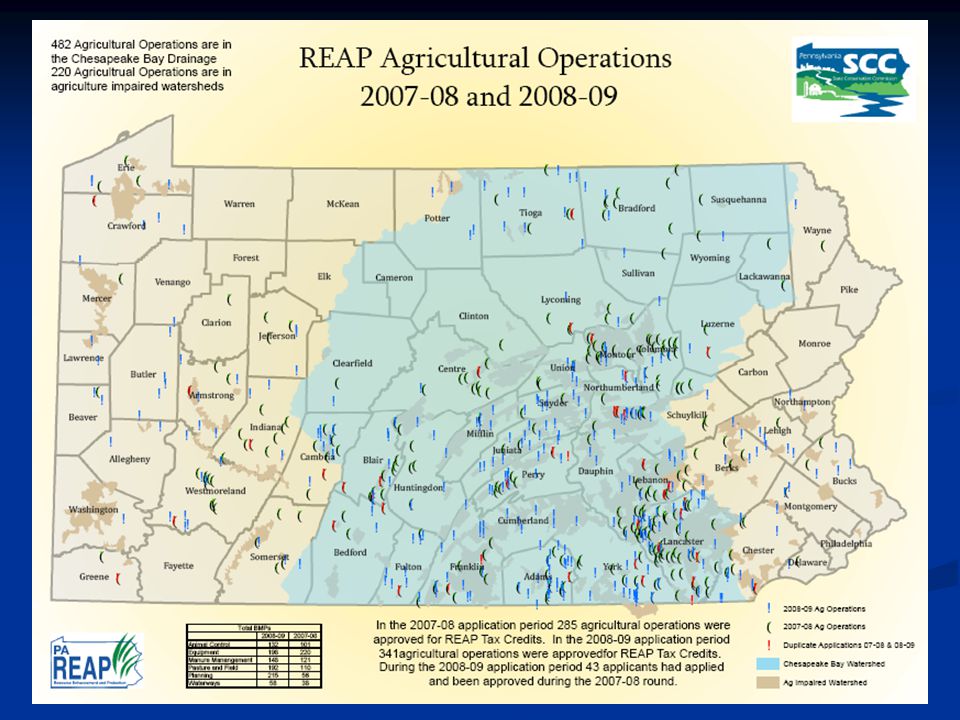

REAP FY 2007-08 Status Summary Status# of BMPS Total Project Cost Total Public Money used REAP Tax Credit Sum for BMP Complete Credit Awarded 350$12,993,571.75$1,283,333.36$5,867,416.16 Sum for Application Approved/ Pending Award 260$ 9,713,474.67$2,012,351.65$3,590,104.68 Sum for Non Compliant w/DOR 16$282,405.27$133,823.47$76,468.78 Sum for Complete Pending with DOR 17$640,928.18$4,140.00$315,127.80 Grand Total643$23,630,379.87 $3,433,648.48$9,849,117.06 * Difference = withdrawn BMPs or application where total costs were less than the approved eligible amount.

7

REAP FY 2008-09 Overview The FY 2008-09 appropriation was $10 million The FY 2008-09 appropriation was $10 million Applications were accepted by the SCC on August 2, 2008 on a first come, first served basis Applications were accepted by the SCC on August 2, 2008 on a first come, first served basis The entire $10 million was allocated to eligible projects on the first day The entire $10 million was allocated to eligible projects on the first day Over $13.5 million in applications were received on the first day Over $13.5 million in applications were received on the first day Approved REAP Tax Credits continue to be awarded to eligible REAP projects as they are completed Approved REAP Tax Credits continue to be awarded to eligible REAP projects as they are completed

8

REAP FY 2008-09 Status Summary StatusNumber Of BMPS Total Project Cost Total Public Money used REAP Tax Credit Sum for BMP Complete-Credit Awarded 273$4,705,462.89$497,074.02$2,089,875.82 Sum for Application Approved/ Pending Award 644$17,816,305.59$2,088,645.58$7,624,339.08 Sum for Non Compliant w/DOR 5$70,750.00$1,125.00$34,968.75 Sum for Complete Pending with DOR 20$463,391.77$85,474.50$192,868.86 Grand Total942$23,055,910.25$2,672,319.10$9,942,052.51 * Difference = withdrawn BMPs or application where total costs were less than the approved eligible amount.

10

Using or Selling a REAP Tax Credit The first REAP tax credits were granted beginning in March, 2008, so credits will begin to be eligible for sale in March 2009. The first REAP tax credits were granted beginning in March, 2008, so credits will begin to be eligible for sale in March 2009. On January 22, 2008, the State Conservation Commission approved revised guidelines and an application for the sale or assignment of REAP tax credits. On January 22, 2008, the State Conservation Commission approved revised guidelines and an application for the sale or assignment of REAP tax credits. These documents have been mailed to all approved REAP applicants and are posted on the REAP website. (www.agriculture.state.pa.us/REAP) These documents have been mailed to all approved REAP applicants and are posted on the REAP website. (www.agriculture.state.pa.us/REAP)www.agriculture.state.pa.us/REAP

11

Sale/Assignment Application

12

What can I do with the REAP Tax Credits once I receive them? What can I do with the REAP Tax Credits once I receive them? The tax credit must be applied against the applicants own tax liability for the first year. The tax credit must be applied against the applicants own tax liability for the first year. The applicant may choose to hold the credit and use it for up to 15 years. The applicant may choose to hold the credit and use it for up to 15 years. The applicant may sell the tax credit after one year from the date issued. The applicant may sell the tax credit after one year from the date issued. Using or Selling a REAP Tax Credit Frequently Asked Questions

13

Which taxes can the REAP tax credits be used for? Which taxes can the REAP tax credits be used for? Personal Income Tax, Corporate Net Income Tax, Capital Stock and Franchise Tax, Bank Shares Tax, Title Insurance Company Tax, Insurance Premiums Tax, and Mutual Thrift Institutions Tax. Personal Income Tax, Corporate Net Income Tax, Capital Stock and Franchise Tax, Bank Shares Tax, Title Insurance Company Tax, Insurance Premiums Tax, and Mutual Thrift Institutions Tax.

14

Using or Selling a REAP Tax Credit Frequently Asked Questions I want to sell my tax credit, what do I do? I want to sell my tax credit, what do I do? The tax credit must be applied against the applicants own tax liability for the year in which it was issued. The tax credit must be applied against the applicants own tax liability for the year in which it was issued. Apply to the State Conservation Commission for the sale/assignment of the approved unused tax credit, one year from the date the credit is granted by the Department of Revenue. Apply to the State Conservation Commission for the sale/assignment of the approved unused tax credit, one year from the date the credit is granted by the Department of Revenue.

15

Using or Selling a REAP Tax Credit Frequently Asked Questions Do I need to hire a broker or agent to sell a REAP Tax Credit? Do I need to hire a broker or agent to sell a REAP Tax Credit? No - While the State Conservation Commission is aware of brokers/agents who may assist in the sale of REAP tax credits, an applicant is not required to use the services of a broker to sell a REAP tax credit. No - While the State Conservation Commission is aware of brokers/agents who may assist in the sale of REAP tax credits, an applicant is not required to use the services of a broker to sell a REAP tax credit.

16

Using or Selling a REAP Tax Credit Frequently Asked Questions Where can I find more information about selling/assigning tax credits? Where can I find more information about selling/assigning tax credits? Guidance documents from the PA Department of Revenue are posted on the SCC website at: www.agriculture.state.pa.us/REAP Guidance documents from the PA Department of Revenue are posted on the SCC website at: www.agriculture.state.pa.us/REAP www.agriculture.state.pa.us/REAP

18

Guidance from PA Department of Revenue

19

Fiscal Year 2009-2010 – What’s Next The Governor’s proposed fiscal year 2009- 2010 budget includes a $10 million appropriation for REAP. The Governor’s proposed fiscal year 2009- 2010 budget includes a $10 million appropriation for REAP. The SCC plans to release 2009-10 REAP guidelines and applications in June 2009, and plans to accept completed applications beginning August 3, 2009. The SCC plans to release 2009-10 REAP guidelines and applications in June 2009, and plans to accept completed applications beginning August 3, 2009. Applications will be accepted on a first- come, first-served basis Applications will be accepted on a first- come, first-served basis

20

Fiscal Year 2009-2010 – What’s Next BMPs which are completed, or equipment which is purchased or delivered, this spring are eligible for REAP tax credits in the 2009- 10 funding round. BMPs which are completed, or equipment which is purchased or delivered, this spring are eligible for REAP tax credits in the 2009- 10 funding round. No major changes to the guidelines are anticipated. No major changes to the guidelines are anticipated.

21

Fiscal Year 2009-2010 – What’s Next Frequently Asked Questions My application was not approved last year due to lack of available credits, do I have to reapply this year? My application was not approved last year due to lack of available credits, do I have to reapply this year? Applicants will be mailed a short “re- application” which may be used as a 2009-10 application. These applicants may chose to “re- activate” their 2008-09 application, but must still compete in the first-come, first-served approval process. Applicants will be mailed a short “re- application” which may be used as a 2009-10 application. These applicants may chose to “re- activate” their 2008-09 application, but must still compete in the first-come, first-served approval process.

22

Compliance All Best Management Practices which were approved for the award of REAP tax credits have a “lifespan”. Practices must be maintained for the number of years established in the guidelines. All Best Management Practices which were approved for the award of REAP tax credits have a “lifespan”. Practices must be maintained for the number of years established in the guidelines. The SCC will conduct compliance checks on completed practices beginning Spring 2009 to ensure that the practices which were awarded are being properly maintained. The SCC will conduct compliance checks on completed practices beginning Spring 2009 to ensure that the practices which were awarded are being properly maintained.

23

Questions & Answers www.agriculture.state.pa.us/REAP Mary Bender REAP Administrator State Conservation Commission

24

Next REAP Webinar March 11, 2009 2 PM to 3 PM Program Sponsor S TATE C ONSERVATION C OMMISSION A G E NVIRONMENT P ARTNERSHIP WEBINAR SITE HOSTED BY Penn State University – College of Agricultural Sciences Pennsylvania Cooperative Extension and the Agriculture & Environment Center www.aec.psu.edu A G E NVIRONMENT P ARTNERSHIP WEBINAR SITE HOSTED BY Penn State University – College of Agricultural Sciences Pennsylvania Cooperative Extension and the Agriculture & Environment Center www.aec.psu.edu

Similar presentations

>")

Business Introduction.>")

Program Overview PASFAA – Fall 2014.>")