Download presentation

Presentation is loading. Please wait.

1

Energy workshop for groups working on Burma: Thai and Burmese energy sector

2

topics Burmese energy sector (compiled by MEE NET)

Structure of Thai power sector Centralized structure and its problems Governance issues Consumption patterns PDP, load forecast, over-investment Decentralized generation Renewable energy (target, VSPP regulations)

")

3

Infographic about Burma’s Power sector

Burma Power Sector Infographic about Burma’s Power sector Links Decision Making Structure Actors Generation mix

4

Decision Making Structure

The electricity system is centralized and under the control and management of the government and state enterprises. Ministry of Electricity Power 2 Gas-fired Thermal power plant Transmission & Distribution System Link to See Structure Ministry of Electricity Power 1 Hydropower & Coal Fired power plants Link to See Structure Dpt. Of Electric Power Dpt. of Hydropower Planning Dpt. of Hydropower Implementation Hydropower Generation Enterprise Myanmar Electricity Power Enterprise Generation,Transmission & Distribution System Electric Supply Enterprise Yangon City Electricity Supply Board (YESB) Ministry of Electricity Power established in 1997 and in 2006 was restructured and separated into 2 ministries: Ministry of Electricity power 1 (MOEP-1) takes responsibilities for: - Planning and Development of new hydropower plants and also operation and maintenance of hydropower stations and coal fired power plants. - Selling electricity to Ministry of Electricity power 2

Ministry of Electricity Power established in 1997 and in 2006 was restructured and separated into 2 ministries: Ministry of Electricity power 1 (MOEP-1) takes responsibilities for: - Planning and Development of new hydropower plants and also operation and maintenance of hydropower stations and coal fired power plants. - Selling electricity to Ministry of Electricity power 2.")

5

Decision Making Structure (Con’t)

Ministry of Electricity power 2 (MOEP-2) in charge of transmission and distribution of electricity generated by Ministry of Electricity power 1 Myanmar Electric Power Enterprise (MEPE) is a State own enterprise established in It is an implementing agency responsible for power generation, transmission and distribution throughout the country. - Thermal power plants: Operation and maintenance of Gas Turbine Power Stations and Combined Cycle Power Plants - Construction of Transmission, Distribution and substation Yangon City Electricity Supply Board (YESB) was formed in 2005 and is tasked with approving businesses to supply electricity in areas that cannot be fully supplied. Other ministries and authorities involved with the energy is as follows: Ministry of Energy and Myanmar Oil and Gas Enterprise (MOGE) in charge of Oil and Gas management Ministry of Mines in charge of Coal business Ministry of Forestry is responsible for Biomass and Fuel Wood Ministry of Science and Technology is responsible for Renewable Energy

in charge of transmission and distribution of electricity generated by Ministry of Electricity power 1. Myanmar Electric Power Enterprise (MEPE) is a State own enterprise established in It is an implementing agency responsible for power generation, transmission and distribution throughout the country. - Thermal power plants: Operation and maintenance of Gas Turbine Power Stations and Combined Cycle Power Plants. - Construction of Transmission, Distribution and substation. Yangon City Electricity Supply Board (YESB) was formed in 2005 and is tasked with approving businesses to supply electricity in areas that cannot be fully supplied. Other ministries and authorities involved with the energy is as follows: Ministry of Energy and Myanmar Oil and Gas Enterprise (MOGE) in charge of Oil and Gas management. Ministry of Mines in charge of Coal business. Ministry of Forestry is responsible for Biomass and Fuel Wood. Ministry of Science and Technology is responsible for Renewable Energy.")

6

Actors in the Power Sector

MOPE-1 Hydropower, Coal MEPE Gas Turbine, CCPP IPPs Small privates Generation Transmission MEPE & MOEP-2 MEPE Small Privates Distribution Export to India, China Domestic Customer Transmission system is under the control of the MEPE and MOEP-2. They will finance, construct and operate the transmission system. MEPE distributes electricity through the national grid to 5 states and 6 divisions. IPPs cannot own transmission lines. However, about private participation, private sector has been allowed to cooperate with MOEP-1, MOEP-2 and MEPE in generation, distribution, sale and service. IPPs can jointly invest with the ministries. Small generator enterprises can supply power to consumers.

8

Generation Mix Hydropower is the main fuel source in the country. In 2008, electricity generated from hydroelectricity was 60.83% of total generation. Gas and steam power are the second ranked fuel used. Currently, there are the following power projects: -14 Hydropower stations -10 gas turbine and thermal power plants -1 Coal fired power station

9

Electricity Installed Capacity and Peak Demand

2000 2001 2002 2003 2004 2005 2006 2007 2008 Installed Capacity 976 1008.5 1038.5 1546.9 1571.9 1719.9 Peak Demand 721.1 692.5 701.2 708.3 864 966.4 995.7 1005 1061.2 Per capita electricity consumption 75.43 68.68 78.06 85.53 86.35 81.00 92.19 94.00 92.80 Source : Myanmar Ministry of Electricity World Bank, World Development Indicators From the figures, it is clear that there is a gap between installed capacity and highest demand for electricity. This can be due to a number of factors including the low efficiency of power plants in generating power. Another possible reason is that power generated is also exported to neighboring countries (peak demand in the graph is only an indicator for domestic demand).

.")

11

Trans-Burma dual pipelines construction begin soon

12

Dynamics of Electricity Sector

After Burma attained independence in 1948, the government established the Electricity Supply Board in 1951 and thus began the government’s monopoly on utilities (before that, some local business were able to generate electricity). In 1972, Electricity Supply Board was reorganized to become the ‘Electricity Power Corporation (EPC). The Ministry of Energy was also formed in 1985 as was responsible for the oil and gas sectors as well as for electricity generation and distribution. Ultimately, on the 15th of November 1997, under the State Law and Order Restoration Council, the Ministry of Electricity Power was established. The Myanmar Electric Power Enterprise (MEPE) was also formed at this time. MEPE continues to serve as the State utility company while the the Ministry restructured into to two ministries, the Ministry of Electricity Power (1) and (2). See Burma Power Sector Steps towards Privatization In late November 2005, to meet increasing demands from new satellite towns and industrial zones, the government started to allow private agencies to supply electricity. Under the Yangon City Electricity Supply Board Law, small businesses in Yangon can generate and sell power to consumers. However, once implemented the government encountered protests from consumers who faced high costs from small generators fueled by an expensive commodity, oil. In addition, generators and other suppliers also faced higher costs once they had to conform to standards set by the government. Though the government has allowed for private investments, the main generation plants and the entire transmission system are still under the control of Burma’s government.

. In 1972, Electricity Supply Board was reorganized to become the ‘Electricity Power Corporation (EPC). The Ministry of Energy was also formed in 1985 as was responsible for the oil and gas sectors as well as for electricity generation and distribution. Ultimately, on the 15th of November 1997, under the State Law and Order Restoration Council, the Ministry of Electricity Power was established. The Myanmar Electric Power Enterprise (MEPE) was also formed at this time. MEPE continues to serve as the State utility company while the the Ministry restructured into to two ministries, the Ministry of Electricity Power (1) and (2). See Burma Power Sector. Steps towards Privatization. In late November 2005, to meet increasing demands from new satellite towns and industrial zones, the government started to allow private agencies to supply electricity. Under the Yangon City Electricity Supply Board Law, small businesses in Yangon can generate and sell power to consumers. However, once implemented the government encountered protests from consumers who faced high costs from small generators fueled by an expensive commodity, oil. In addition, generators and other suppliers also faced higher costs once they had to conform to standards set by the government. Though the government has allowed for private investments, the main generation plants and the entire transmission system are still under the control of Burma’s government.")

13

Burma Power Policy Burma’s economic development strategies, especially in its energy sector are driven by centralized government decision-making. The Burmese domestic energy market is influenced both by regional and international investment flows from major regional states looking for energy resources. Burma’s natural resource rich country including an abundance of gas and oil reserves and high hydropower potential are being exploited. Investors from the region including Thailand, China, South Asian Countries, South Korean, and the GMS countries are all involved in extractive industries within the country. In addition to reaping high profits from these trade opportunities, the government is also using the investment ventures as useful tools in its battle with minority ethnic groups who currently occupy large swathes of resource rich lands. In the name of development, the government has been expelling the groups from construction sites and economic development zones. Though the Burmese government claims that energy sector development is vital for meeting the population’s basic needs and overall development strategy, Burma’s electrification rate is very low, even after years of resource exploitation. In 2008, 42.8 Million of Burma’s million population lived without electricity. Or, according to UN statistics, only 5% of all Burmese citizens have access to electricity even though the government’s stated goal is to increase electrification rates to 60% by 2020. During , Burma’s energy sector plans to continue oil and gas pipeline construction, oil and gas extraction plans, hydroelectric power development, and transmission line construction both for domestic use and for regional interconnection plans. Links Power Planning Subpage Dynamics of Electricity Sector Subpage

14

Burma Power Planning In order to achieve its economic and social development plans of 12% annual GDP Growth, Burma’s Fourth Short-Term Five-Year Plan (2006/ /2011) was formulated to meet this stated target. One of power-related objectives in the five year plan is ‘To develop electric power and energy sector to be in conformity with developing trend industries’. In addition, specific Long-term Policy for the Energy Sector is as follows: Sustainable use of natural resources to support the economic growth in a sustainable manner; Efficient utilization of available energy resources; Smooth and reliable energy supplies for building a modem agro industrial based nation; A well balanced use of energy resources by the creation of an equal distribution of the share of various primary energy sources for conservation; Promoting the development and utilization of all available renewable energy resources; Creating an attractive base for further investment in energy and energy related ventures. Regional policy and cooperation in infrastructure development in order to support investment and trade in the region results in the Government’s plans for near term cross-country cooperation activities as follows: Linked infrastructure including hydropower power plants, power lines, pipelines and supporting road networks Shared infrastructure including road s, channels for navigations, bridges and etc. Shared link or independent infrastructure for import and export of oil, gas petrochemicals and other related products Myanmar Electric Power Enterprise (MEPE), a state-owned enterprise, has been distributing electricity generated by major hydropower and gas turbine stations. The national grid supplies 94 % of the nation’s power needs while another 6% comes from off-grid isolated energy sources. MEPE’s objectives for the country’s development is as follows: Developing Hydropower for base load and gas turbine for peak load In order to optimize the use of natural gas by gas turbine, combined cycle power plants are implemented To expand the national grid To revive the study of alternative production of electricity by using waste products including rice husks, etc. Using electricity by firing boilers to generate electricity meeting local requirements instead of utilizing the main grid’s power is encouraged To reduce loss of electricity incurred from transmission and distribution In remote areas where electricity from hydropower through the national grid cannot be utilized, the generation and distribution of electricity will be performed by diesel generating sets, wind and solar facilitates

was formulated to meet this stated target. One of power-related objectives in the five year plan is ‘To develop electric power and energy sector to be in conformity with developing trend industries’. In addition, specific Long-term Policy for the Energy Sector is as follows: Sustainable use of natural resources to support the economic growth in a sustainable manner; Efficient utilization of available energy resources; Smooth and reliable energy supplies for building a modem agro industrial based nation; A well balanced use of energy resources by the creation of an equal distribution of the share of various primary energy sources for conservation; Promoting the development and utilization of all available renewable energy resources; Creating an attractive base for further investment in energy and energy related ventures. Regional policy and cooperation in infrastructure development in order to support investment and trade in the region results in the. Government’s plans for near term cross-country cooperation activities as follows: Linked infrastructure including hydropower power plants, power lines, pipelines and supporting road networks. Shared infrastructure including road s, channels for navigations, bridges and etc. Shared link or independent infrastructure for import and export of oil, gas petrochemicals and other related products. Myanmar Electric Power Enterprise (MEPE), a state-owned enterprise, has been distributing electricity generated by major hydropower and gas turbine stations. The national grid supplies 94 % of the nation’s power needs while another 6% comes from off-grid isolated energy sources. MEPE’s objectives for the country’s development is as follows: Developing Hydropower for base load and gas turbine for peak load. In order to optimize the use of natural gas by gas turbine, combined cycle power plants are implemented. To expand the national grid. To revive the study of alternative production of electricity by using waste products including rice husks, etc. Using electricity by firing boilers to generate electricity meeting local requirements instead of utilizing the main grid’s power is encouraged. To reduce loss of electricity incurred from transmission and distribution. In remote areas where electricity from hydropower through the national grid cannot be utilized, the generation and distribution of electricity will be performed by diesel generating sets, wind and solar facilitates.")

15

Burma Power Planning (Con’t)

Power Development Plans and Transmission Interconnection Projects According to its power demand forecast, in 2030, Burma will have a peak demand of 7, MW (peak demand in 2008 was 1,061.2 MW). During , several projects will be Developed. At present, 19 hydroelectric power projects are under construction. Furthermore, 18 cross border hydropower power projects are currently being planned through investments by companies and/or state owned enterprises from China, Thailand and India. If these projects are completed, their total installed capacity will rise to 19,413 MW. Meanwhile, in 2009 Burma current installed capacity is only 2,255.9 MW. Transmission system To facilitate power transmission, during , the government plans to construct 62 transmission lines throughout Burma in the near future (at present, transmission lines are in operation )

. During , several projects will be. Developed. At present, 19 hydroelectric power. projects are under construction. Furthermore, 18 cross border hydropower power projects. are currently being planned through investments by companies and/or state. owned enterprises from China, Thailand and India. If these projects are completed, their total installed capacity will rise to 19,413 MW. Meanwhile, in 2009 Burma current installed capacity is only 2,255.9 MW. Transmission system. To facilitate power transmission, during , the government plans to construct 62 transmission lines throughout Burma in the near future (at present, 129 transmission lines are in operation )")

16

Infographic about Thailand’s Power sector

Thailand Power Sector Infographic about Thailand’s Power sector Links Decision Making Structure Actors Generation mix

17

Decision Making Structure

Thailand has Centralized Electricity Structure. Policy determination and planning including system operation are in hands of the government and the state owned enterprise; the Ministry of Energy and the Electricity Generation Authority of Thailand (EGAT). EPPO and EGAT are responsible for electricity supply planning. DEDE is mainly responsible for alternative energy development ERC was established in 2009, as an independent authority, to regulate and ensure efficiency and transparency of electricity management, review final draft PDP, license to power producers Cabinet National Energy Policy Committee (NEPC) Energy Regulatory Commission (ERC) Ministry of Energy EGAT Energy Policy and Planning Office (EPPO) PTT Public Co., Ltd. (State Enterprise) Dpt. of Alternative Energy Development and Efficiency (DEDE) Bangchak Petroleum Pub Co., Ltd. (State Enterprise) Dpt. of Energy Business Energy Fund Administration Institute (EFAI) (Public Organization) Dpt. of Mineral Fuels

. EPPO and EGAT are responsible for electricity supply planning. DEDE is mainly responsible for alternative energy development. ERC was established in 2009, as an independent authority, to regulate and ensure efficiency and transparency of electricity management, review final draft PDP, license to power producers. Cabinet. National Energy Policy Committee (NEPC) Energy Regulatory Commission (ERC) Ministry of Energy. EGAT. Energy Policy and Planning Office (EPPO) PTT Public Co., Ltd. (State Enterprise) Dpt. of Alternative Energy Development and Efficiency (DEDE) Bangchak Petroleum Pub Co., Ltd. (State Enterprise) Dpt. of Energy Business. Energy Fund Administration Institute (EFAI) (Public Organization) Dpt. of Mineral Fuels.")

18

Actors in Power Sector Generation Power Purchaser, System Operation,

SPPs IPPs EGAT Power Plants R E G U L A T O Power Purchaser, System Operation, and Transmission Power Purchase System Operation Transmission Bulk Power Supply EGAT Energy Regulatory Commission (ERC) Distribution/ Retail Supply PEA MEA End Users End Users VSPP Direct Customers Under Thailand ‘Enhanced Single Buyer Structure’, all producers have to sell electricity to EGAT that holds a monopoly over the transmission system. EGAT then sells power to MEA and PEA for distribution to consumers. Only a small amount of consumers directly purchase electricity rom EGAT/ IPPs/ SPPs, most of them are industries. In addition, ERC serves as a regulator in the system.

Distribution/ Retail Supply. PEA. MEA. End Users. End Users. VSPP. Direct. Customers. Under Thailand ‘Enhanced Single Buyer Structure’, all producers have to sell electricity to EGAT that holds a monopoly over the transmission system. EGAT then sells power to MEA and PEA for distribution to consumers. Only a small amount of consumers directly purchase electricity rom EGAT/ IPPs/ SPPs, most of them are industries. In addition, ERC serves as a regulator in the system.")

19

Generation Mix Thailand uses natural gas as its major fuel to generate electricity, 72.5% in Lignite and coal are used 11% and 8.4% respectively. Installed generating capacity from April until August in 2010 reached 30, MW. In 2009, the installed capacity was 29, MW. Share of Power Generation by Fuel Type January to October 2010 The accumulated power generation from January to October is 134, GWh. At the end of 2008, the generation reached 148, Meanwhile, in 2009, the total generation was 145, GWh which represents a decrease between 2008 and 2009 of 2.04%. Peak Demand of 2010 happened in May, at 24,009.9 MW whereas in 2008 and 2009 peak demands were 22,045 MW and 22,568.9 MW respectively.

20

Thailand Power Policy Overview Thailand’s power policy is driven by two key factors: continued economic growth driven by the industrial sector and energy sector financiers as well as ambitious plans to be the energy leader in the region. Thailand’s stated goal of being the “Hub of the ASEAN Grid” is at the core of its energy investments. Thailand’s centralized power planning structure emphasizes increasing energy supplies to meet expected demands. These needs can only be met through continued investments in large scale power projects both domestically as well as in neighboring countries. Power planning also includes expectations that the regional transmission network will be realized allowing for both exports and imports of electricity with neighboring countries. International concern about climate change is also playing a role in Thailand’s power development plans. By pledging to reduce greenhouse gas emissions in the energy sector by 30% by 2020, Thailand is planning on increased investments in nuclear power projects, hydropower projects and the promotion of Clean Development Mechanism projects. Meanwhile, renewable energy development, Energy Efficiency and Demand-side management (DSM) are not adequately being promoted by the government. Links Power Planning History of Electricity Reform

are not adequately being promoted by the government. Links Power Planning History of Electricity Reform.")

21

Power Planning Sub page

The centralized government planning process and the National Economic and Social Development Plan in addition to regional development and power development plans are crucial in Thailand’s power sector planning. The National Economic and Social Development Plan such as Southern and Eastern Seaboard Development Projects, which are focused on heavy industries utilize large amounts of energy consumption and require infrastructure development that includes huge power plants. been Moreover, current ‘Framework of Thailand’s Power Strategies’ have also been devised by the government, Ministry of Energy and state-owned enterprise Electricity Generating Authority of Thailand (EGAT) to include the following: Maintaining energy stability and security: supplying sufficient energy to meet demand, promoting public participation especially in national power planning process, preparing readiness for gas supplied emergency Regulating energy businesses Strengthening energy utilities and authorities Promoting generation and supply of alternative energy Reducing energy use and lower greenhouse gas emission Power Development Plan (PDP) Thus far, Thailand electricity sector propelled by PDP 2010 ( ) ลิ้งค์ไปที่ PDP 2010, the latest 20 year PDP approved in early 2010. It has been formulated according to the Ministry of Energy’s framework with specific investment and projects as illustrated In the figure on Installed Capacity classified by Fuel Type for Combined-cycle gas power plants are main source, followed by power purchase from Laos and coal fired power plants. Importantly, the Ministry of Energy is adamant to construct nuclear power plants Even while opposition exists from local people living around the proposed sites. Renewable energy will be account for 7-8% of the generation during the ext 20 years. throughout 20 years. According to the plan, Thailand’s installed capacity will reach 65,547 MW whereas present installed capacity is 30, MW PDP 2010 : GDP (Base Case) Diesel Renewable Energy Heavy Fuel Oil Import Natural Gas Imported Coal Lignite Nuclear Hydro

to include the following: Maintaining energy stability and security: supplying sufficient energy to meet demand, promoting public participation especially in national power planning process, preparing readiness for gas supplied emergency. Regulating energy businesses. Strengthening energy utilities and authorities. Promoting generation and supply of alternative energy. Reducing energy use and lower greenhouse gas emission. Power Development Plan (PDP) Thus far, Thailand electricity sector propelled by. PDP 2010 ( ) ลิ้งค์ไปที่ PDP 2010, the latest 20 year PDP approved in early It has been formulated according to. the Ministry of Energy’s framework with specific. investment and projects as illustrated. In the figure on Installed Capacity classified by. Fuel Type for Combined-cycle gas. power plants are main source, followed by. power purchase from Laos and coal fired power plants. Importantly, the Ministry of Energy is adamant to. construct nuclear power plants. Even while opposition exists from local people living. around the proposed sites. Renewable energy will. be account for 7-8% of the generation during the ext 20 years. throughout 20 years. According to the plan, Thailand’s installed capacity will reach 65,547 MW whereas present installed capacity is 30, MW. PDP 2010 : GDP (Base Case) Diesel. Renewable Energy. Heavy Fuel Oil. Import. Natural Gas. Imported Coal. Lignite. Nuclear. Hydro")

22

Power Planning Sub page (Con’t)

Arguments made during PDP 2010: Thailand’s civil society criticized the 2010 PDP approval process due to lack of transparency and genuine public participation. The national plan was approved by National Energy Policy Council during the chaotic political situation that occurred in April in Thailand. It is the first PDP covering a 20 year period (Previous plans last 5 years and 15 years). Therefore, long-term demand forecast and investment planning will be less accurate and err from the reality. Notably, even though Thailand’s PDP noted an aspiration to harmonize its renewable energy component with its Link to 15-year Alternative Energy Development Plan (AEDP), for , developed by Department of Alternative Energy Development and Efficiency under Ministry of Energy, this is not reflected in the official PDP. According to the AEDP, generation capacity from AEDP is to reach 5,608 MW, however the official PDP only includes plans to increase generation capacity from renewable energy sources to 4,049.5 MW Unenthusiastic promotion on renewable energy such as decreasing adders (money support per unit) for solar power and excuse that limitations on the transmission system to support electricity from any renewable energy sources for the national grid EGAT has tried to preserve major shares in the generation market by determining that EGAT’s proportion in new power plants must be at least 50% Process of PDP development and approval: EGAT draft and propose to Ministry of Energy and Energy Regulatory Commission to review Approval process by National Energy Policy Committee (NEPC) comprised of Ministers, representatives from the National Economic and Social Development Board while the Prime Minister serves as Chairman. PDP will be proposed to the Cabinet as a final step In addition to PDP and AEDP, the government had just conducted a preliminary study of a 20 year energy- saving plan, which aims to review potential of all sectors in reducing energy demand by 25 % by 2030. LINKS Articles

. Therefore, long-term demand forecast and investment planning will be less accurate and err from the reality. Notably, even though Thailand’s PDP noted an aspiration to harmonize its renewable energy component with its Link to 15-year Alternative Energy Development Plan (AEDP), for , developed by Department of Alternative Energy Development and Efficiency under Ministry of Energy, this is not reflected in the official PDP. According to the AEDP, generation capacity from AEDP is to reach 5,608 MW, however the official PDP only includes plans to increase generation capacity from renewable energy sources to 4,049.5 MW. Unenthusiastic promotion on renewable energy such as decreasing adders (money support per unit) for solar power and excuse that limitations on the transmission system to support electricity from any renewable energy sources for the national grid. EGAT has tried to preserve major shares in the generation market by determining that EGAT’s proportion in new power plants must be at least 50% Process of PDP development and approval: EGAT draft and propose to Ministry of Energy and Energy Regulatory Commission to review. Approval process by National Energy Policy Committee (NEPC) comprised of Ministers, representatives from the National Economic and Social Development Board while the Prime Minister serves as Chairman. PDP will be proposed to the Cabinet as a final step. In addition to PDP and AEDP, the government had just conducted a preliminary study of a 20 year energy- saving plan, which aims to review potential of all sectors in reducing energy demand by 25 % by LINKS. Articles.")

23

History of Electricity Reform Subpage

Thailand’s initial centralized economic and social planning saw electricity projects as basic investments providing Thai citizen’s with basic infrastructure to improve their livelihoods and to to drive economic growth. Mega projects including generation stations, hydropower, coal fired power projects and transmission system were constructed gradually. State Control The government decided that the most efficient model for managing the power sector was to establish its own state owned enterprise. This led in 1968, to the consolidation of regional state owned generating companies into a central national electricity termed the Electricity Generating Authority of Thailand (EGAT). The distribution networks, Metropolitan Electricity Authority (MEA) and Provincial Electricity Authority (PEA) were respectively set up in 1958 and MEA became responsible for power distribution in Bangkok and neighboring provinces while PEA was responsible for power distribution in the remaining provinces. By the end of the 1960s, the power system was centralized under EGAT and the two distribution companies. Privates allowed to generation In 1992, Independent Private Power Producers (IPPs) were allowed into the system through long term concessions operative power plants in accordance with Power Purchase Agreements (PPAs) with EGAT. EGAT continued to hold sole control over the transmission system operation. At the same time, the Thai government also launched a Small Power Producers (SPPs) program to promote the use of clean efficient energy or the use of renewable energy sources for domestic use. However, the plan was also criticized for the overwhelming preference for large industrial producers (who received SPP licenses) over smaller power producers including rural cooperatives, municipalities, hospitals. The first step of privatization was completed with the relaxation of power tariffs. At that time the National Energy Policy Office (under the Ministry of Energy today) believed that marketizing the power tariff would lead to lower tariffs over time. However, the marketization of power tariffs led to a rapid increase due to rising oil and gas prices at the same time.

. The distribution networks, Metropolitan Electricity Authority (MEA) and Provincial Electricity Authority (PEA) were respectively set up in 1958 and MEA became responsible for power distribution in Bangkok and neighboring provinces while PEA was responsible for power distribution in the remaining provinces. By the end of the 1960s, the power system was centralized under EGAT and the two distribution companies. Privates allowed to generation In 1992, Independent Private Power Producers (IPPs) were allowed into the system through long term concessions operative power plants in accordance with Power Purchase Agreements (PPAs) with EGAT. EGAT continued to hold sole control over the transmission system operation. At the same time, the Thai government also launched a Small Power Producers (SPPs) program to promote the use of clean efficient energy or the use of renewable energy sources for domestic use. However, the plan was also criticized for the overwhelming preference for large industrial producers (who received SPP licenses) over smaller power producers including rural cooperatives, municipalities, hospitals. The first step of privatization was completed with the relaxation of power tariffs. At that time the National Energy Policy Office (under the Ministry of Energy today) believed that marketizing the power tariff would lead to lower tariffs over time. However, the marketization of power tariffs led to a rapid increase due to rising oil and gas prices at the same time.")

24

History of Electricity Reform Subpage (Con’t)

‘Privatization without Extensive Liberalization’ In 2000, the second step of privatization involving the introduction of the power pool model along with the unbundling of the generation, transmission and distribution systems was introduced. These were in preparation for complete market competition in the power market by However, with such attempt, it was However, the attempt at privatization was not a success. Many arguments were raised by parties including academics and consumers that it was too risky to allow for a market mechanism to control prices, regulatory body, etc. Two other options were proposed introduced, EGAT proposed a Third Party Access Model which allows consumers to independently choose suppliers while Academics proposed Single Buyer Model which allows for public ownership of distribution and even transmission. Later, EGAT proposed a different model moving from ‘private sector participation competition to achieve efficiency’ to one that allows for ‘national efficiency and competitiveness and secure regional leadership” and ‘To build strong national champions in the energy sector’. Within this model, EGAT would need remain a large major player in order to compete against multinational energy companies in the region. ‘National Champion’ and Enhanced Single Buyer (ESB) in the present model Under this proposed model EGAT can be the National Champion and maintain its monopoly position. This model is different from a single buyer in which private entities have to compete with EGAT in generation but EGAT retains a monopoly on the transmission system and a majority of generation. EGAT had plans to reform itself into a private company, listing itself on the stock market to raise capital and expand in the region. However, this plan finally failed in 2006. LINKS Articles

in the present model. Under this proposed model EGAT can be the National Champion and maintain its monopoly position. This model. is different from a single buyer in which private entities have to compete with EGAT in generation but EGAT retains a. monopoly on the transmission system and a majority of generation. EGAT had plans to reform itself into a private company, listing itself on the stock market to raise capital and expand in. the region. However, this plan finally failed in LINKS. Articles.")

25

Structure and Overview of Thai Power Sector

26

... Steps involved to deliver electricity to end-users

Fuel procurement Power Generation Retail, Meter Reading, Billing & settlement Transmission Distribution

27

Structure of Thai power sector

Generation (% share) SPPs (7%) EGAT (50%) IPPs (41%) Import (2%) VSPPs (<<1%) Govt. ERC EGAT (100%) SO Transmission Distribution PEA (67%) MEA (31%) Direct Customers (2%) Users Users Remarks: - Figure of % Share in 2008 - ERC = Energy Regulatory Commission ที่มา: EPPO Aug 2009

SPPs. (7%) EGAT. (50%) IPPs. (41%) Import. (2%) VSPPs. (<<1%) Govt. ERC. EGAT (100%) SO. Transmission. Distribution. PEA. (67%) MEA. (31%) Direct Customers. (2%) Users. Users. Remarks: - Figure of % Share in ERC = Energy Regulatory Commission. ที่มา: EPPO Aug")

28

Generation by fuel type

Power generation (May 2009) Generation by fuel type Generation by sources Oil, 0.1% Natural Gas, 70% Hydro, 6% Coal & Lignite, 21% Import & Others, 3% IPP 12,151 MW (43%) EGAT, 13,615 MW (48%) SPP 2,073 MW (7%) Import & Exchange 640 MW (2%) Total: 28,482 MW ที่มา: EPPO Aug 2009

Generation by fuel type. Generation by sources. Oil, 0.1% Natural Gas, 70% Hydro, 6% Coal & Lignite, 21% Import & Others, 3% IPP 12,151 MW (43%) EGAT, 13,615 MW (48%) SPP 2,073 MW (7%) Import & Exchange 640 MW (2%) Total: 28,482 MW. ที่มา: EPPO Aug")

29

Power Supply Management

Review the Power Development Plan (PDP) every 6 months to be in line with the changing demand situation Maintain the reserve margin to be no less than 15% Diversify fuel types in power generation: Give importance to SPPs and VSPPs using renewable energy as fuel Study the feasibility of nuclear power generation. Promote Clean Coal Technology for coal-fired power generation International cooperation in power development projects: Power purchase from LPDR, Myanmar, China, Cambodia and Malaysia ที่มา: EPPO Aug 2009

every 6 months to be in line with the changing demand situation. Maintain the reserve margin to be no less than 15% Diversify fuel types in power generation: Give importance to SPPs and VSPPs using renewable energy as fuel. Study the feasibility of nuclear power generation. Promote Clean Coal Technology for coal-fired power generation. International cooperation in power development projects: Power purchase from LPDR, Myanmar, China, Cambodia and Malaysia. ที่มา: EPPO Aug")

30

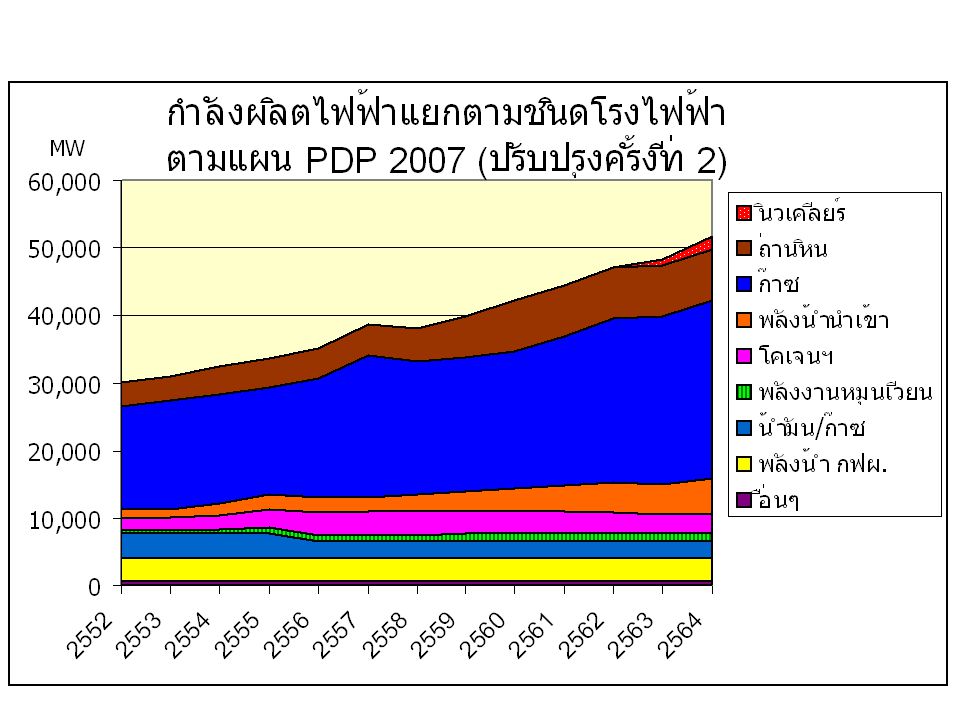

Overview of Electricity Generating Capacity PDP 2007 (Revision 2: @ Mar09)

Installed capacity as at Dec ,140 MW Total increased capacity ( ) 30,155 MW ,605 MW ,550 MW Decommissioned plants -7,502 MW Total generating capacity up to ,792 MW Comparison of New Generating Capacity by Source of Supply (in MW) Year PDP 2007 Revision 1 PDP 2007 Revision 2 EGAT IPP SPP Purchase from Abroad VSPP New Projects 4,615 4,400 1,193 5,473 3,769 1,985 264 2,187 - 8,900 1,400 575 8,690 8,000 1,600 300 2,850 4,800 Total Increased Capacity 13,515 5,800 1,768 14,163 11,769 6,000 564 5,037 35,246 30,155 Difference of New Capacity when compared with PDP 2007 (Revision 1) - 5,091 ที่มา: EPPO Aug 2009

30,155 MW ,605 MW ,550 MW. Decommissioned plants -7,502 MW. Total generating capacity up to ,792 MW. Comparison of New Generating Capacity by Source of Supply (in MW) Year. PDP Revision 1. PDP 2007 Revision 2. EGAT. IPP. SPP. Purchase from Abroad. VSPP. New Projects ,615. 4,400. 1,193. 5,473. 3,769. 1, , ,900. 1, ,690. 8,000. 1, ,850. 4,800. Total Increased Capacity. 13,515. 5,800. 1, , ,769. 6, , , ,155. Difference of New Capacity when compared with PDP 2007 (Revision 1) - 5,091. ที่มา: EPPO Aug")

31

IPPs: 1st IPP Solicitation in 1994 7 Selected IPPs with PPA Signed

IPP Plant Location Fuel Gen. Capacity (MW) COD IPT Aow Pay, Chonburi Natural Gas 700 15 Aug 2000 TECO Ratchaburi 1 Jul 2000 Ratchburi Power 1,400 Unit 1: 1 Mar 2008 Unit 2: 1 Jun 2008 Gulf Power Khaeng Koi, Saraburi 1,468 Unit 1: 1 Mar 2007 Unit 2: 1 Mar 2008 BLCP Pluakdaeng, Rayong Coal 1,346.5 Unit 1: 13 Aug 2006 Unit 2: 14 Nov 2006 Glow IPP Bowin, Chonburi 713 31 Jan 2003 EPEC Klong Mai, Samut Prakarn 350 25 Mar 2003 Total 6,677.5 ที่มา: EPPO Aug 2009

COD. IPT. Aow Pay, Chonburi. Natural Gas Aug TECO. Ratchaburi. 1 Jul Ratchburi Power. 1,400. Unit 1: 1 Mar Unit 2: 1 Jun Gulf Power. Khaeng Koi, Saraburi. 1,468. Unit 1: 1 Mar Unit 2: 1 Mar BLCP. Pluakdaeng, Rayong. Coal. 1, Unit 1: 13 Aug Unit 2: 14 Nov Glow IPP. Bowin, Chonburi Jan EPEC. Klong Mai, Samut Prakarn Mar Total. 6, ที่มา: EPPO Aug")

32

IPPs: 2nd IPP Solicitation in 2007 4 Selected IPPs with PPA Signed

IPP Plant Project’s Shareholder Fuel Type Capacity (MW) Location SCOD GHECO-One GLOW IPP2: 65% Hemaraj: 35% Coal 660 Rayong Nov 2011 National Power Supply (NPS) NPS: 99.99% 6 Thai Individuals: 0.01% 540 Chachoengsao Nov 2012/ Mar 2013 Siam Energy Gulf JP: 99.94% 6 Thai Individuals: 0.06% Gas 1,600 Mar 2012/ Sep 2012 Power Generation Supply Individual Investors: 0.06% Saraburi Jun 2014/ Dec 2014 Total 4,400 Remarks: 7 Dec 07: NEPC approved the next IPP Solicitation for power procurement during ที่มา: EPPO Aug 2009

Location. SCOD. GHECO-One. GLOW IPP2: 65% Hemaraj: 35% Coal Rayong. Nov National Power Supply (NPS) NPS: 99.99% 6 Thai Individuals: 0.01% 540. Chachoengsao. Nov 2012/ Mar Siam Energy. Gulf JP: 99.94% 6 Thai Individuals: 0.06% Gas. 1,600. Mar 2012/ Sep Power Generation Supply. Individual Investors: 0.06% Saraburi. Jun 2014/ Dec Total. 4,400. Remarks: 7 Dec 07: NEPC approved the next IPP Solicitation for power procurement during ที่มา: EPPO Aug")

33

Promotion of SPP/VSPP Power Generation

Small Power Producer (SPP)/ Very Small Power Producer (VSPP): A generator of a private entity, state agency, state-owned enterprise, using cogeneration system or renewable energy, agricultural waste or residues, residues from agricultural or industrial production processes to produce electricity. SPP Sale of electricity to the Electricity Generating Authority of Thailand (EGAT), is >10 MW up to 90 MW. Firm contract: years Non-firm contract: 5 years and renewed automatically VSPP Sale of electricity to the Distribution Utility, i.e. Metropolitan Electricity Authority (MEA) and Provincial Electricity Authority (PEA), is no more than 10 MW. ที่มา: EPPO Aug 2009

/ Very Small Power Producer (VSPP): A generator of a private entity, state agency, state-owned enterprise, using cogeneration system or renewable energy, agricultural waste or residues, residues from agricultural or industrial production processes to produce electricity. SPP Sale of electricity to the Electricity Generating Authority of Thailand (EGAT), is >10 MW up to 90 MW. Firm contract: years. Non-firm contract: 5 years and renewed automatically. VSPP Sale of electricity to the Distribution Utility, i.e. Metropolitan Electricity Authority (MEA) and Provincial Electricity Authority (PEA), is no more than 10 MW. ที่มา: EPPO Aug")

34

Fuel Diversification in Power Generation

Oil, 0.1% Natural Gas, 70% Hydro, 6% Coal & Lignite, 21% Import & Others, 3% Share of Power Generation by Fuel Type May 2009) Currently, Thailand’s power generation depends heavily on natural gas as fuel. - Efforts are being made to boost greater use of renewable energy as fuel. Status of Power Generation from Renewable Energy and Potential & Target in 2011 Existing MW Target MW Potential MW Biomass Existing 1,610 MW Target ,800 MW Potential 4,400 MW Wind Existing MW Target MW Potential 1, MW Hydro - Sugarcane industry, etc. - Biomass power plants - Community power plants Wind farm in southern Thailand Mini Hydro and Micro Hydro Existing MW Target MW Potential MW Existing MW Target MW Potential 50,000 MW Existing MW Target MW Potential MW Biogas Solar PV MSW - Urban areas Solar homes His Majesty’s projects 0.1% of installation areas Biogas from livestock farms and agro, palm industry - Bangkok 9,000 tons/day - Municipality 6,300 tons/day - Industry 1,000 tons/day (Data as at Jan2009) ที่มา: EPPO Aug 2009

Currently, Thailand’s power generation depends heavily on natural gas as fuel. - Efforts are being made to boost greater use of renewable energy as fuel. Status of Power Generation from Renewable Energy and Potential & Target in Existing 56 MW. Target 165 MW. Potential 700 MW. Biomass. Existing 1,610 MW. Target 2,800 MW. Potential 4,400 MW. Wind. Existing 1 MW. Target 115 MW. Potential 1,600 MW. Hydro. - Sugarcane industry, etc. - Biomass power plants. - Community power plants. Wind farm in southern. Thailand. Mini Hydro and Micro Hydro. Existing 46 MW. Target 60 MW. Potential 190 MW. Existing 32 MW. Target 55 MW. Potential 50,000 MW. Existing 5 MW. Target 78 MW. Potential 400 MW. Biogas. Solar PV. MSW. - Urban areas. Solar homes. His Majesty’s projects. 0.1% of installation areas. Biogas from livestock farms and agro, palm industry. - Bangkok 9,000 tons/day. - Municipality 6,300 tons/day. - Industry 1,000 tons/day. (Data as at Jan2009) ที่มา: EPPO Aug")

35

Power Purchase from Neighboring Countries

Thailand has cooperated in hydropower development with neighboring countries, on a bilateral basis. MOUs on power purchase have been signed with Laos, China and Myanmar, with a total power purchase of 11,500 MW. MOUs on Power Purchase Signed Country Signing Date Purchase Cap. (MW) Within Year LPDR 22 Dec 2007 7,000 2015 Myanmar 14 Jul 1997 1,500 2010 PR China 12 Nov 1998 3,000 2017 Imported power being supplied to Thailand’s Grid: LPDR 313 MW Malaysia 300 MW [High Voltage Direct Current (HVDC)] ที่มา: EPPO Aug 2009

Within Year. LPDR. 22 Dec , Myanmar. 14 Jul , PR China. 12 Nov , Imported power being supplied to Thailand’s Grid: LPDR 313 MW. Malaysia 300 MW [High Voltage Direct Current (HVDC)] ที่มา: EPPO Aug")

36

Power Purchase from LPDR

Project Sale to Thailand (MW) COD 1) Currently supplying power to Thailand 1.1 Nam Theun-Hinboun 187 31 Mar 1998 1.2 Houay Hoa 126 3 Sep 1999 Sub-total 313 2) PPA signed but not yet supplied power to Thailand 2.1 Nam Theun 2 920 Dec 2009 2.2 Nam Ngum 2 615 Mar 2011 2.3 Theun-Hinboun Expansion 220 Mar 2012 1,755 3) Tariff MOU signed 3.1 Hongsa Lignite 1,473 2013 GRAND TOTAL 3,541 Status as at Jun09. ที่มา: EPPO Aug 2009

COD. 1) Currently supplying power to Thailand. 1.1 Nam Theun-Hinboun Mar Houay Hoa Sep Sub-total ) PPA signed but not yet supplied power to Thailand. 2.1 Nam Theun Dec Nam Ngum Mar Theun-Hinboun Expansion Mar ,755. 3) Tariff MOU signed. 3.1 Hongsa Lignite. 1, GRAND TOTAL. 3,541. Status as at Jun09. ที่มา: EPPO Aug")

37

Power Purchase from Myanmar

14 Jul 1997: MOU on Power Purchase from Myanmar (~1,500 MW by 2010). 30 Nov 2005: MOU on Cooperation in the Development of Power Projects on Thanlwin and Tanintharyi Rivers. Initially, Myanmar has proposed 2 power projects on Thanlwin River: (1) Hutgyi hydropower project, 1,200 MW (2) Tasang hydropower project, 7,000 MW Also, Tariff MOU signed for Mai Khot coal-fired power project (369MW) Tasang 7,000 MW (Other potential projects: Upper/Lower Thanlwin , 4, MW) Hutgyi 1,200 MW (Tanintharyi 600 MW) ที่มา: EPPO Aug 2009

. 30 Nov 2005: MOU on Cooperation in the Development of Power Projects on Thanlwin and Tanintharyi Rivers. Initially, Myanmar has proposed 2 power projects on Thanlwin River: (1) Hutgyi hydropower project, 1,200 MW. (2) Tasang hydropower project, 7,000 MW. Also, Tariff MOU signed for Mai Khot coal-fired power project (369MW) Tasang. 7,000 MW. (Other potential projects: Upper/Lower Thanlwin , 4, MW) Hutgyi. 1,200 MW. (Tanintharyi. 600 MW) ที่มา: EPPO Aug")

38

Power Purchase from Cambodia

Feasibility study is being conducted on 2 potential projects: Strung Nam Hydropower Project MW Koh Kong Coal-fired Power Project 3,660 MW Power Purchase from Malaysia Thailand (EGAT) and Malaysia (TNB) have had power trade between each other since 1980, starting with 80 MW. Current trade: 300 MW via HVDC (High Voltage Direct Current) system. ที่มา: EPPO Aug 2009

and Malaysia (TNB) have had power trade between each other since 1980, starting with 80 MW. Current trade: 300 MW via HVDC (High Voltage Direct Current) system. ที่มา: EPPO Aug")

39

NPIEP Milestones for Nuclear Power Program Implementation

(17 November 2007) NPIEP Milestones for Nuclear Power Program Implementation NPI: Nuclear Power Infrastructure NPIEP: NPI Establishment Plan NPPDO: Nuclear Power Program Development Office NPP: Nuclear Power Plant NRB: Nuclear Regulatory Body 1st Milestone 2nd Milestone 3rd Milestone MS 0.1 MS 0.2 MS 1: Policy Decision MS 2 : Call for Bids MS 3: Start Operation Nuclear power option included in PDP2007 To prepare for policy decision Knowledgeable Commitment Financial Commitments Commissioning 1st NPP GO NUCLEAR Phase 0.1: Preliminary Phase NPIPC & 7 Sub-committees appointed Issues & Milestones considered NPIEP prepared Phase 1: Pre-project Activity Phase - approve NPIEP - set up NPPDO - infrastructure work started - survey of potential sites - feasibility study completed - public information & participation Phase 2: Program Implementation Phase - implement NPIEP with Milestones - full NRB established - legislation & international protocols enacted - suitable sites for bid selected - technology/qualified suppliers selected - prepare to call bids Phase 3: Construction Phase - NPIEP fully implemented - bidding process completed - design & engineering - manufacturing - construction & installation - test runs & inspection NPP commissioning license Phase 4: Operation Phase - commercial operation - O&M - planning for expansion industrial and technology development plan 1 year 3 years 3 years 6 years 2007 2008 2011 2014 2020 ที่มา: EPPO Aug 2009

NPIEP Milestones for Nuclear Power Program Implementation. NPI: Nuclear Power Infrastructure. NPIEP: NPI Establishment Plan. NPPDO: Nuclear Power Program Development Office. NPP: Nuclear Power Plant. NRB: Nuclear Regulatory Body. 1st Milestone. 2nd Milestone. 3rd Milestone. MS 0.1. MS 0.2. MS 1: Policy Decision. MS 2 : Call for Bids. MS 3: Start Operation. Nuclear power option included in PDP2007. To prepare for policy decision. Knowledgeable Commitment. Financial Commitments. Commissioning 1st NPP. GO NUCLEAR. Phase 0.1: Preliminary Phase. NPIPC & 7 Sub-committees appointed. Issues & Milestones considered. NPIEP prepared. Phase 1: Pre-project Activity Phase. - approve NPIEP. - set up NPPDO. - infrastructure work started. - survey of potential sites. - feasibility study completed. - public information & participation. Phase 2: Program Implementation Phase. - implement NPIEP with Milestones. - full NRB established. - legislation & international protocols enacted. - suitable sites for bid selected. - technology/qualified suppliers selected. - prepare to call bids. Phase 3: Construction Phase. - NPIEP fully implemented. - bidding process completed. - design & engineering. - manufacturing. - construction & installation. - test runs & inspection. NPP commissioning license. Phase 4: Operation Phase. - commercial operation. - O&M. - planning for expansion. industrial and technology development plan. 1 year. 3 years. 3 years. 6 years ที่มา: EPPO Aug")

40

Centralized structure

41

Centralized structure of electricity

Conflicts are a result of centralized structure of control Loss of livelihood/health/forests for local people for the benefits of others, mainly urban commercial and industrial interests Centralized grid: in many cases, makes economic and technical sense, however… Control of a central grid need not be monopolized by one group Structure of control determined by Cold War politics, not technical superiority

42

Problems with centralized control (1)

Separation of consumption and production leads to inefficient consumption “Out of sight, out of mind” Ratio of Power demand growth to GDP growth = 1.4 Perverse incentives to exclude customer-owned generation The more to invest, the more to profit. Small-scale, renewable generators lack access Energy conservation measures are viewed as a threat to EGAT’s profits.

43

Centralized & decentralized generation

Cogeneration Gasifier

44

Centralized & decentralized generation

Cogeneration Gasifier

45

Choice of supply options considered in the PDP by EGAT

700 MW Coal-fired power plant 700 MW gas-fired combined cycle plant 230 MW gas-fired open cycle plant 1,000 MW nuclear plant Hydro imports are politically negotiated outside of PDP process DSM/EE, RE, Distributed generation not considered as supply options

46

Centralized energy is also more costly

Thailand PDP 2007 requires 2 trillion baht to implement, comprising: million B generation 1,482,000 transmission ,000 Transmission adds 40% to generation costs Decentralized generation brings down costs Ireland – retail costs for new capacity to 2021 Source: World Alliance for Decentralized Energy, April 2005

47

Centralized generation wastes a lot of energy

(~70% of heat value is lost & adds to climate change problem) Combined cycle 13,540 MW 47.5 % Hydro 3,424.2 MW 12.0 % Thermal 9,666.6 MW 33.9 % Gas turbines, diesel 971.4 MW 3.4 % Hydro import 1.2 % Renewables 288.1 MW 1.0 % Import from Malaysia Total at end of ,530.3 MW Installed capacity by types of generation in 2007 Loss in conversion process 61% Station use (in power plants) 1% Loss in transmission 3% Loss in distribution 5-8% Useful electricity to end-users <30%

Combined cycle. 13,540 MW % Hydro. 3,424.2 MW % Thermal. 9,666.6 MW % Gas turbines, diesel MW. 3.4 % Hydro import. 1.2 % Renewables MW. 1.0 % Import from Malaysia. Total at end of ,530.3 MW. Installed capacity by types of generation in Loss in conversion process. 61% Station use (in power plants) 1% Loss in transmission. 3% Loss in distribution. 5-8% Useful electricity to end-users. <30%")

48

Problems with centralized control (2)

Lack of accountability, transparency, participation in centralized planning processes Political decisions masked in technical language “Big is beautiful”, fossil fuels dominate Social and environmental concerns are ignored “Cost plus” incentive structure passes risks to consumers “Overcapacity worth 400 billion Baht” (from total assets of 700 billion Baht and annual turnover of 240 billion Baht) – Prime Minister Thaksin Shinwatra

– Prime Minister Thaksin Shinwatra.")

49

Governance issues

50

Energy policy and its impacts on share prices of energy companies in the stock market

The coup-installed government announced its policy on energy investment opportunities on 3 Oct 2006 Energy policy, PDP approval and IPP bidding resulted in significant windfall benefits for selected companies 1 year later, the share prices of companies benefiting from the PDP jumped 66% (other companies had a 8.7% rise)

")

51

Change in energy companie’s share prices within 1 yr

52

Conflict of interest : policy v business

Board of directors Permanent secretary of ministry of energy Chairman of PTT Chairman of EGAT Board member of PTT chemical Chairman of Rayong refinery Director general,Energy fuel Dep. permanent secretary Board member of Thai oil Dep. permanent secretary Board member of RATCH Dep. permanent secretary Board member of PTTEP Director general of energy business Board member of PTT Director general of Department of Alternative Energy Development and Efficiency energy Board member of RATCH Director of Energy Policy and Planning official Board member of PTTEP Senior official of ministry of energy Board member of Aromatics PLC Senior official of ministry of energy Board member of Bang chak Board member of RATCH Board member of Ratchaburi generation company Senior official of ministry of energy 52

53

Performance of high-level energy officials in serving the government vs. PTT Plc. (Thai gas/oil utility, the largest list company in Thailand) Attendance of PTT board meetings* Attendance of Automatic tariff (Ft) mechanism mtgs** Permanent secretary 13/13 4/6 Director of EPPO 8/9 5/6 100% 67% 90% 83% *จากรายงานประจำปีบมจ. ปตท. ปี 2546 **ตั้งแต่มีการปรับองค์ประกอบคณะอนุกรรมการ Ft โดยแต่งตั้งให้นายเชิดพงษ์เป็นประธาน และนายเมตตาเป็นรองประธาน (ปลายปี 46) Government officials serve energy companies better than the Thai public? 53

mechanism mtgs** Permanent secretary. 13/13. 4/6. Director of EPPO. 8/9. 5/6. 100% 67% 90% 83% *จากรายงานประจำปีบมจ. ปตท. ปี **ตั้งแต่มีการปรับองค์ประกอบคณะอนุกรรมการ Ft โดยแต่งตั้งให้นายเชิดพงษ์เป็นประธาน และนายเมตตาเป็นรองประธาน (ปลายปี 46) Government officials serve energy companies better than the Thai public 53.")

54

Structure reform of power sector proposed by Thai civil society

กฟผ. (โรงไฟฟ้าพลังความร้อน) ~ 15,000 MW ไฟฟ้าพลังงานหมุนเวียน /ชุมชนท้องถิ่น /รายย่อย/ cogen สัญญาซื้อขายไฟฟ้า (IPP/Egco/Ratch/SPP) ~ 10,000 MW โรงไฟฟ้าใหม่ การไฟฟ้าฝ่ายระบบส่ง ระบบส่ง ศูนย์ควบคุมระบบ เขื่อน การไฟฟ้าฝ่ายจำหน่าย (กฟน./กฟภ.) จัดหา/ค้าปลีกไฟฟ้า * ระบบจำหน่าย ความต้องการที่เพิ่มขึ้น (บ้าน/รายเล็ก/อื่นๆ ) ความต้องการที่เพิ่มขึ้น (รายใหญ่) * ในกรณีชุมชน/องค์กรท้องถิ่น มีความพร้อมและความสนใจ ให้สามารถใช้สิทธิในการจัดการและจัดหาไฟฟ้าได้เอง โดย กฟน./กฟภ. ทำหน้าที่เป็นเพียงผู้ให้บริการระบบสายจำหน่าย แต่ไม่ผูกขาดสิทธิในการจัดหา ความต้องการใช้ไฟฟ้าในปัจจุบัน ~ 19,000 MW รัฐ รัฐ/เอกชน องค์ กร กำ กับ ดู แล อิสระ

~ 15,000 MW. ไฟฟ้าพลังงานหมุนเวียน /ชุมชนท้องถิ่น /รายย่อย/ cogen. สัญญาซื้อขายไฟฟ้า. (IPP/Egco/Ratch/SPP) ~ 10,000 MW. โรงไฟฟ้าใหม่ การไฟฟ้าฝ่ายระบบส่ง. ระบบส่ง. ศูนย์ควบคุมระบบ. เขื่อน. การไฟฟ้าฝ่ายจำหน่าย (กฟน./กฟภ.) จัดหา/ค้าปลีกไฟฟ้า * ระบบจำหน่าย. ความต้องการที่เพิ่มขึ้น (บ้าน/รายเล็ก/อื่นๆ ) ความต้องการที่เพิ่มขึ้น (รายใหญ่) * ในกรณีชุมชน/องค์กรท้องถิ่น มีความพร้อมและความสนใจ ให้สามารถใช้สิทธิในการจัดการและจัดหาไฟฟ้าได้เอง. โดย กฟน./กฟภ. ทำหน้าที่เป็นเพียงผู้ให้บริการระบบสายจำหน่าย แต่ไม่ผูกขาดสิทธิในการจัดหา. ความต้องการใช้ไฟฟ้าในปัจจุบัน. ~ 19,000 MW. รัฐ. รัฐ/เอกชน. องค์ กร. กำ. กับ. ดู แล. อิสระ.")

55

Consumption patterns

56

Electrical consumption by sector in 2007

Others 5% Residential 21% Industrial 49% Commercial 25% การใช้พลังงานไฟฟ้าแยกตามประเภทผู้ใช้ 133,132 GWh ที่มา กฟผ.

57

การกระจายตัวของการใช้ไฟฟ้าแยกตามพื้นที่ Distribution of electricity consumption by region

South North Northeast Central Source: Figure 19, Statistical Report Fiscal Year 2003 Power Forecast and Statistics Analysis Department System Control and Operation Division. Report No. SOD-FSSR

58

Comparison of electricity consumption of three big malls vs

Comparison of electricity consumption of three big malls vs. 16 provinces Siam Paragon GWh 123 MBK 81 278 GWh Central World 75 ที่มา: การไฟฟ้านครหลวง 2549 ที่มา: พพ. รายงานการใช้ไฟฟ้า ปี 2549

59

Siam Paragon MBK Pak Mun Central World 65 Dams Malls Province

Electricity production and consumption (GWh) MBK 123 81 75 Siam Paragon Central World Impacts of Pak Mun Dam alone 1700 families relocated Loss of livelihood for >6200 families Loss of 116 fish species (44%) Fishery yield down 80% Source: MEA, EGAT, Searin, Graphic: Green World Foundation Pak Mun 65 Mae Hong Song Dams Malls Province 59

MBK Siam Paragon. Central World. Impacts of Pak Mun Dam alone families. relocated. Loss of livelihood. for >6200 families. Loss of 116. fish species (44%) Fishery yield. down 80% Source: MEA, EGAT, Searin, Graphic: Green World Foundation. Pak Mun. 65. Mae. Hong. Song. Dams Malls Province. 59.")

60

การกระจายของจำนวนผู้ใช้ไฟและปริมาณการใช้ไฟฟ้า Distribution of number of power users & energy consumed Agricultural pumping Government Specific businesses Large industrial/commercial) Small industrial/commercial Small industrial/commercial Large houses (>150 kWh/mo) Small houses (<150 kWh/mo) Number of customers Electricity consumption ที่มา : รายงานการปรับโครงสร้างอัตราค่าไฟฟ้า (มติ ค.ร.ม. วันที่ 3 ตุลาคม 2543)

Small industrial/commercial. Small industrial/commercial. Large houses (>150 kWh/mo) Small houses (<150 kWh/mo) Number of customers. Electricity consumption. ที่มา : รายงานการปรับโครงสร้างอัตราค่าไฟฟ้า (มติ ค.ร.ม. วันที่ 3 ตุลาคม 2543)")

61

"Nature has enough for our need, but not enough for our greed."

- Gandhi "Nature has enough for our need, but not enough for our greed." -- Ghandi 61 61

62

Hourly Power Demand (2002) > 1,000 MW in 66 hours

> 1,000 MW in 66 hours")

63

Source: EPPO, 2007.

64

พลังไฟฟ้า (เมกะวัตต์)

Load profile on the day of annual highest consumption Notice the rise of air-conditioning load 2551 2550 2549 พลังไฟฟ้า (เมกะวัตต์) 2548 2534 2533 2532 เวลา (ชั่วโมง)

เวลา (ชั่วโมง)")

65

PDP, demand forecast over-investment

66

Power demand projection Sep 2007 (PDP 2007 revision 1)

MW Economic Development Plan (years) Average GDP growth rate/year Average demand growth rate/year 10th plan ( ) 5.0 5.86 11th plan ( ) 5.6 5.95 12th plan ( ) 5.54 48,958 MW 2,477 2,399 2,287 37,382 MW 2,235 2,178 2,131 2,035 27,996 MW 1,832 Demand increase per year 1,759 1,629 1,361 1,410 1,268 1,444 1,449 2550 – average increase 1,386 MW 2555 – average increase 1,877 MW 2560 – average increase 2,315 MW แผนพัฒนาฯ ฉบับที่ 10 แผนพัฒนาฯ ฉบับที่ 11 แผนพัฒนาฯ ฉบับที่ 12 ที่มา กฟผ.

Average GDP growth rate/year. Average demand growth rate/year. 10th plan ( ) th plan ( ) th plan ( ) ,958 MW. 2,477. 2,399. 2, ,382 MW. 2,235. 2,178. 2,131. 2, ,996 MW. 1,832. Demand increase per year. 1,759. 1,629. 1,361. 1,410. 1,268. 1,444. 1, – 2554 average increase 1,386 MW – 2559 average increase 1,877 MW – 2564 average increase 2,315 MW. แผนพัฒนาฯ ฉบับที่ 10. แผนพัฒนาฯ ฉบับที่ 11. แผนพัฒนาฯ ฉบับที่ 12. ที่มา กฟผ.")

67

Planning of capacity additions

(Total capacity requirement = peak demand + 15% reserve margin)

")

68

Power Demand: Projections vs

Power Demand: Projections vs. Actual 1992 – 2008 If no systemic bias, the chance of over-projecting demand 12 times in a row should be 1/4096!! MW

69

Incentive structure for utilities: the more expansion, the more profits

Financial criteria for utilities link profits to investments Thailand uses outdated return-based regulation WB’s promoted financial criteria such as self financing ratio (SFR) also have similar effects ROIC (Return on Invested Capital means: the more you invest, the more profits ROIC = Net profit after tax Invested capital EGAT 8.4% MEA PEA 4.8% Result : Demand forecast have systemic bias toward over-projections Too many expensive power projects get built

also have similar effects. ROIC (Return on Invested Capital means: the more you invest, the more profits. ROIC = Net profit after tax. Invested capital. EGAT 8.4% MEA. PEA. 4.8% Result : Demand forecast have systemic bias toward over-projections. Too many expensive power projects get built.")

70

Cycle of over-expansion under the centralized monopoly system

Deterministic planning based on demand forecast leads to over-investment in capital-intensive power projects Power demand (over-)projections 1 2 Utilities’ Profits 3 Tariff structure that allows pass-through of unnecessary investments

projections Utilities’ Profits. 3. Tariff structure that allows pass-through. of unnecessary investments.")

71

Comparison of trend lines with historical peak consumption

Exponential Linear Past demand trajectory was linear but how come the official demand projections have always assumed exponential trend and over-estimated?

72

The government forecast was based on the assumption of exponential growth

21 power plants

74

ที่มา:แผนพัฒนาพลังงานทดแทน 15 ปีพ.ศ.2551 -2565

76

Cost estimate (Baht/kWh)

Supply options Cost estimate (Baht/kWh) Generation Transmission1 Distribution2 CO2 3 Other envi impacts 4 Social impacts Total DSM 0.50 – 1.505 - SPP cogeneration (PES > 10%) 2.60 6 0.44 0.08 0.71 3.83 VSPP (Renewable) Bulk supply tariff (~ 2.62) + Adder (0.3 – 8) 0 – 0.63 0 – low 2.92 – 10.62 gas CC 2.25 7 0.37 0.09 0.79 low – medium 3.93 Coal 2.11 7 0.15 2.76 High 5.82 Nuclear 2.087–7.308 High – very high หมายเหตุ ใช้สมมติฐานว่าต้นทุนร้อยละ 12.4 ของค่าไฟฟ้ามาจากธุรกิจสายส่ง 2. ใช้สมมติฐานว่าต้นทุนร้อยละ 14.5 ของค่าไฟฟ้ามาจากธุรกิจจำหน่าย 3. ค่า CO2 ที่ 10 ยูโร/ตัน 4. ค่า Externality ตามการศึกษา Extern E ของสหภาพยุโรป และนำมาปรับลดตามค่า GDP ต่อหัวของไทย The World Bank, Impact of Energy Conservation, DSM and Renewable Energy Generation on EGAT’s PDP, 6. ตามระเบียบ SPP 7. ที่มา : กฟผ. 8. California Public Utilities Commission (CPUC), 2050 Multi-Sector CO2 Emissions Abatement Analysis Calculator, 2009 9. Cost of liability protection, Journal “Regulation” 2002 – 2003.

Generation. Transmission1. Distribution2. CO2 3. Other envi impacts 4. Social impacts. Total. DSM – SPP. cogeneration. (PES > 10%) VSPP. (Renewable) Bulk supply tariff. (~ 2.62) + Adder. (0.3 – 8) 0 – – low – gas CC low – medium Coal High Nuclear – High – very high หมายเหตุ 1. ใช้สมมติฐานว่าต้นทุนร้อยละ 12.4 ของค่าไฟฟ้ามาจากธุรกิจสายส่ง. 2. ใช้สมมติฐานว่าต้นทุนร้อยละ 14.5 ของค่าไฟฟ้ามาจากธุรกิจจำหน่าย. 3. ค่า CO2 ที่ 10 ยูโร/ตัน. 4. ค่า Externality ตามการศึกษา Extern E ของสหภาพยุโรป และนำมาปรับลดตามค่า GDP ต่อหัวของไทย The World Bank, Impact of Energy Conservation, DSM and Renewable Energy Generation on EGAT’s PDP, ตามระเบียบ SPP. 7. ที่มา : กฟผ. 8. California Public Utilities Commission (CPUC), 2050 Multi-Sector CO2 Emissions Abatement Analysis Calculator, Cost of liability protection, Journal Regulation 2002 –")

77

Time to review gov’t subsidy to polluting industries with low value added to economy and low competitiveness? BOI investment privileges should take into account energy and environmental considerations High energy intensity Low value added Low competitiveness

78

Macroeconomic Analysis

Office of the National Economic and Social Development Board O F F I C E O F T H E P R I M E M I N I S T E R Low Quality Education Low Quality labour Enabling factors: MACROECONOMIC MANAGEMENT Low Value Creation High Import Contents & Sheer size of export to GDP Energy Intensity & Low Efficiency & Unsustainable structure (Low margin/return) Low Quality for Raw-material, machinery and equipment Insufficient in R&D Investment No immunity/ High volatility Financial System Lack of Saving Lack of regulation on industrial product’s quality control Low Basic infrastructure and Logistic development Slow Technology Development

Low Quality for Raw-material, machinery and equipment. Insufficient in R&D Investment. No immunity/ High volatility Financial System. Lack of Saving. Lack of regulation on industrial product’s quality control. Low Basic infrastructure and Logistic development. Slow Technology Development.")

79

Decentralized generation

Decentralized generation: generation of electricity near where it is used

80

Energy efficient end-use

Old way New way Power plant Power plant Biomass Wind power Biomass Solar Customers Energy efficient end-use

82

Energy waste in a typical pumping system

83

Sankey Energy Flow Diagram

84

Cogeneration Combined Heat and Power (CHP)

")

85

85

87

Very Small Power Producer (VSPP)

These Thai policymakers also knew that rice mills had a lot of waste rice husk. Pig farms have a lot of manure. Sugar factories have sugar cane bagasse. Sawmills have wood scraps. Each of these is a renewable energy source that can contribute to the national power mix, but only if generators have a market for their power. Selling to the national grid is a perfect market because it’s there 24 hours a day. 87 87

88

$ VSPP regulations essentially have two components: a set of technical regulations that provide for a safe flow of electricity from these generators to the national grid; and a set of commercial regulations regarding the flows of money to the VSPP generators. 88

89

$ Technical regulations: Allowable voltage, frequency, THD variations

Protective relays 1-line diagrams for all cases: Induction Synchronous Inverters Single/multiple Connecting at different voltage levels (LV or MV) Communication channels Commercial regulations: Definitions of renewable energy, and efficient cogeneration Cost allocation Principle of standardized tariff determination Invoicing and payment arrangements Arbitration Technical regulations include topics like allowable voltage, frequency variations and specify required protective relays. The commercial regulations focus on how costs are allocated, how tariff amounts are determined, and what happens in the event of disputes. A standardized PPA eliminates lengthy case-by-case negotiations with utilities. 89

Communication channels. Commercial regulations: Definitions of renewable energy, and efficient cogeneration. Cost allocation. Principle of standardized tariff determination. Invoicing and payment arrangements. Arbitration. Technical regulations include topics like allowable voltage, frequency variations and specify required protective relays. The commercial regulations focus on how costs are allocated, how tariff amounts are determined, and what happens in the event of disputes. A standardized PPA eliminates lengthy case-by-case negotiations with utilities. 89.")

90

Evolution of Thai VSPP regulations

2002 VSPP regulations drafted, approved by Cabinet Up to 1 MW export, renewables only Tariffs set at avoided cost (bulk supply tariff + FT) 2006 Up to 10 MW export, renewables + cogeneration Feed-in tariff “adder” If > 1 MW then utility only pays for 98% of energy 2009 Tariff adder increase, more for projects that offset diesel The Thai regulations were approved in Projects were allowed to come into the program as long as they used reenewable energy and they exported less than 1 MW. The tariffs were essentially set at the cost per kWh that Thailand’s distribution utilities pay for power they buy from EGAT. In 2006 the utilities felt comfortable enough with the initial VSPP projects to allow an increase in project size to 10 MW export and efficient cogeneration was also allowed. The government also recognized that VSPP could play a larger role in meeting the nation’s commitment of 8% renewable energy by the year 2011 (recently raised to 20% by year 2022). The upgrade to the regulations also created a technology-specific feed-in tariff subsidy adder. In 2009 the feed-in tariff was changed to provide additional payments for projects that offset diesel generation, which is still used in Thailand in some remote mountain and island areas. English versions of the Thai regulations are available at this website: for English version of regulations, and model PPA 90

Up to 10 MW export, renewables + cogeneration. Feed-in tariff adder If > 1 MW then utility only pays for 98% of energy Tariff adder increase, more for projects that offset diesel. The Thai regulations were approved in Projects were allowed to come into the program as long as they used reenewable energy and they exported less than 1 MW. The tariffs were essentially set at the cost per kWh that Thailand’s distribution utilities pay for power they buy from EGAT. In 2006 the utilities felt comfortable enough with the initial VSPP projects to allow an increase in project size to 10 MW export and efficient cogeneration was also allowed. The government also recognized that VSPP could play a larger role in meeting the nation’s commitment of 8% renewable energy by the year 2011 (recently raised to 20% by year 2022). The upgrade to the regulations also created a technology-specific feed-in tariff subsidy adder. In 2009 the feed-in tariff was changed to provide additional payments for projects that offset diesel generation, which is still used in Thailand in some remote mountain and island areas. English versions of the Thai regulations are available at this website: for English version of regulations, and model PPA. 90.")

91

Thai VSPP feed-in tariffs

Fuel Adder Additional for diesel offsetting areas Additional for 3 southern provinces Years effective Biomass Capacity <= 1 MW $ $ 7 Capacity > 1 MW $ Biogas <= 1 MW > 1 MW Waste (community waste, non-hazardous industrial and not organic matter) Fermentation $ Thermal process $ Wind <= 50 kW $ $ 10 > 50 kW Micro-hydro 50 kW - <200 kW $ <50 kW $ Solar $ This table shows the current VSPP tariffs. Tariffs have evolved to vary depending on: Fuel type Geographic location (more for provinces in 3 conflict-prone southern provinces) Whether or not the project offsets diesel Capacity The total tariff is equal to this adder pluse the utility’s avoided cost of power. Ultimately consumers pay for the adder through a per-kWh pass-through mechanism to all consumers. Assumes exchange rate 1 Thai baht = U.S. dollars Tariff = adder(s) + bulk supply tariff + FT charge Biomass tariff = $ $ $ = $0.085/kWh 91

Fermentation. $ Thermal process. $ Wind. <= 50 kW. $ $ > 50 kW. Micro-hydro. 50 kW - <200 kW. $ <50 kW. $ Solar. $ This table shows the current VSPP tariffs. Tariffs have evolved to vary depending on: Fuel type. Geographic location (more for provinces in 3 conflict-prone southern provinces) Whether or not the project offsets diesel. Capacity. The total tariff is equal to this adder pluse the utility’s avoided cost of power. Ultimately consumers pay for the adder through a per-kWh pass-through mechanism to all consumers. Assumes exchange rate 1 Thai baht = U.S. dollars. Tariff = adder(s) + bulk supply tariff + FT charge. Biomass tariff = $ $ $0.027 = $0.085/kWh. 91.")

92

Korat Waste to Energy – biogas … an early Thai VSPP project

Uses waste water from cassava to make methane Produces gas for all factory heat (30 MW thermal) + 3 MW of electricity 3 x 1 MW gas generators Here are some of VSPP projects in operation in Thailand. Thailand is the world’s second largest producer of Cassava, much of which is turned into tapioca flower. The process generates waste water that, when digested, makes a lot of methane. The digester is a covered lagoon the size of a couple football fields – here you can see the lagoon’s black plastic cover. Methane provides thermal energy and electricity for the tapioca factory and excess is sold to the grid under the VSPP program. 92 92

+ 3 MW of electricity. 3 x 1 MW gas generators. Here are some of VSPP projects in operation in Thailand. Thailand is the world’s second largest producer of Cassava, much of which is turned into tapioca flower. The process generates waste water that, when digested, makes a lot of methane. The digester is a covered lagoon the size of a couple football fields – here you can see the lagoon’s black plastic cover. Methane provides thermal energy and electricity for the tapioca factory and excess is sold to the grid under the VSPP program")

93

Biogas from Pig Farms Reduces air and water pollution

Produces fertilizer Produces electricity 8 x 70 kW generator Ratchaburi Biogas from Pig Farms 93 93

94

Biogas from Pig Farms 5000 pigs $31 / day elec. 94

95

Micro hydropower 40 kW Mae Kam Pong, Chiang Mai, Thailand

This community run 40 kW micro-hydro project produces about $13,000 per year worth of electricity in the VSPP program. 40 kW Mae Kam Pong, Chiang Mai, Thailand 95

96

Rice husk-fired power plant

9.8 MW Roi Et, Thailand In Thailand there are many rice mills. This is a 9.8 MW SPP that burns rice husk to generate electricity with a steam turbine. 96

97

Bangkok Solar 1 MW PV Project size: 1 MW Uses self-manufactured a-Si

Feed-in tariffs have helped strengthen a burgeoning solar electric manufacturing industry in Thailand. This 1 MW plant uses solar panels manufactured in Thailand. 97

98

Thai VSPP MW applied, received permission, PPA signed, and selling – as of September 2009

Industry has responded strongly to the Thai VSPP program. This chart gives some indication of the pipeline of projects. The columns on the right are MW of VSPP generators that are currently online. There are over 100 projects with a combined capacity of over 725 MW. PPAs have been signed for over 2600 MW. Over 4000 MW have been approved. And over 7200 MW have applied. Clearly not all of the projects that have applied will end up being built, but at the very least it indicates considerable interest by industry. For reference, Thailand’s 2009 peak load was a bit over 22,000 MW. Cambodia’s peak load in 2007 of 262 MW is shown as this blue square.. 98

Similar presentations

, Medium - and Long – term Investment Plan and the Role of the Private Sector Mr. Rangsan Sarochawikasit.>")