Download presentation

Presentation is loading. Please wait.

1

Flow of Presentation Objective. History. Reasons for Merger; a) Strategic Analyses b) Technical Analyses Valuation. Funding Current Scenario Conclusion.

Strategic Analyses b) Technical Analyses Valuation. Funding Current Scenario Conclusion..")

2

Objective Learning Process of M&A. Know how to do valuation. How to make profit my learning M&A.

3

Overview of companies Cincinnati Based Established in yr.1837 Work force : 110,000 Market Capitalization :$141 bill. Suppliers : 85000 Manufacturing plants : 106 in 41 countries. Pre-acquisition revenues (2004) : $51 bill. Boston based Established in yr. 1895 Work force : 29400 Market capitalization : $45 billion. Suppliers : 26000 Manufacturing plants : 31 in 14 countries. Pre-acquisition revenues (2004) : $9.8 bill.

: $51 bill. Boston based Established in yr Work force : Market capitalization : $45 billion. Suppliers : Manufacturing plants : 31 in 14 countries. Pre-acquisition revenues (2004) : $9.8 bill..")

4

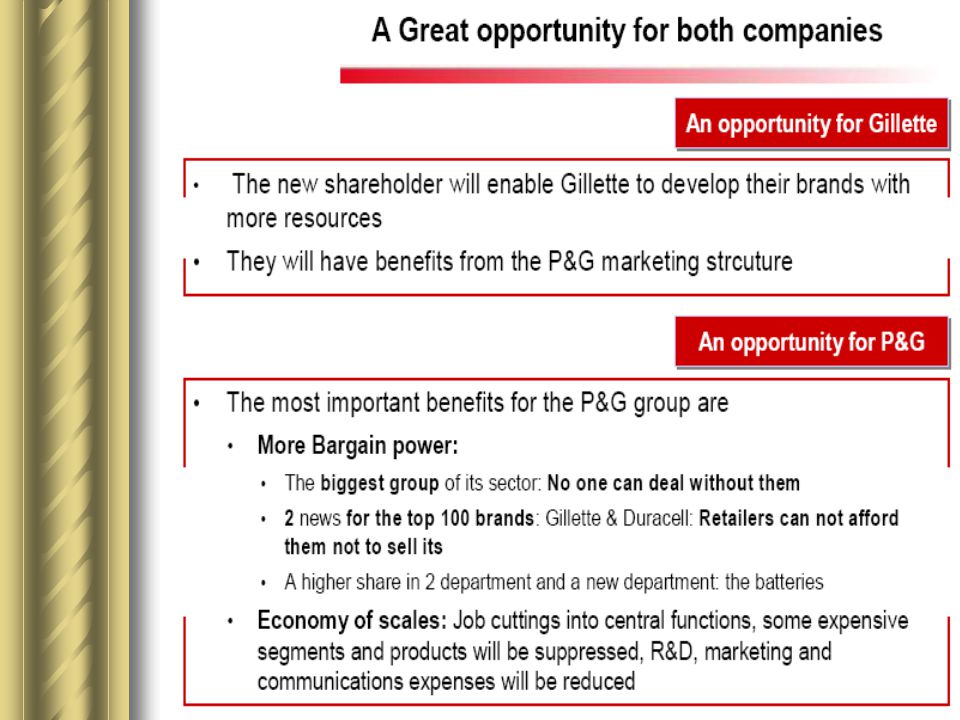

Strategic Analysis

6

Marketing Approach Global Regional Culture Innovative Social - Responsib ility + + Synergy Economy of Scale P&G can have benefits from the Gillette R&D structure and use its Brand Loyalty P&G can have benefits if they adopt an HYBRID STRUCTURE ; But every change require some cost and they have to do INTEGRATION EFFORT. Risk in Merger :

7

Technical Analysis Sales & Growth Ratio Profit Margin Leverage Conclusion.

8

Sale

9

Sale Growth Rate

10

Operating Profit Margin.

12

Debt to Equity Ratio.

13

Assumption about sale's growth % of net sale 2004 sales' growth in 2005 Weightage growth % of projected sales 2005 sales' growth after 2005 Weightage sales' growth Blades & Razor 41.32%14.00%5.78%41.15%12.00%4.94% Duracell21.30%9.00%1.92%20.28%10.00%2.03% Oral Care15.17%25.00%3.79%16.57%25.00%4.14% Braun13.04%15.00%1.96%13.10%15.00%1.97% Personal Care 9.17%11.00%1.01%8.89%11.00%0.98% Total 100.00 % 14.46% 100.00% 14.05%

14

Assumption about EBIT margin % PFO 2004 PFO‘ growth in 2005 Weightage PFO 's growth %of projected PFO 2005 PFO'growth after 2005 Weightage PFO ' growth Blades & Razor 63.68%30.00%19.10%65.97%30.00%19.79% Duracell 19.16%22.00%4.22%18.63%22.00%4.10% Oral Care 9.73%14.50%1.41%8.88%14.50%1.29% Braun 3.71%10.50%0.39%3.27%10.50%0.34% Personal Care 3.72%10.00%0.37%3.26%10.00%0.33% Total 100.00% 25.49% 100.00% 25.84%

15

Assets to Sale 2004200320022001 Operating Working Capital ($mill.) 0.00170.00708.001333.00 Operating Working Capital as %of sale NA2.00%8.00%16.00% Net Long term assets 5731.005614.004968.004979.00 Net Long term assets turnover 1.831.651.701.62 Capital expenditures ($mill.) 616.00408.00405.00624.00 Capital expenditures % net sales 6.00%4.00%5.00%8.00%

Operating Working Capital as %of sale NA2.00%8.00%16.00% Net Long term assets Net Long term assets turnover Capital expenditures ($mill.) Capital expenditures % net sales 6.00%4.00%5.00%8.00%")

16

Valuation Individual Valuation of Firm Individual Valuation of Firm Valuation After Acquisition Valuation After Acquisition Assumption for the Valuation 2005 After 2005 Sales' Growth Rate14.86% 14.05% EBIT Margin25.49% 25.85% Tax Rate30.00% Operating Working Capital to sale1.00% Net Long term Assets to sale60.00%

17

FCFF Valuation Method. FCFF = NOPAT + depreciation & amortization – changes in NWC – Capex Discount Rate = WACC.

18

Dream Deal Total Deal Value : $57 bnMarket Cap. : $48bn @ 18% Premium.975 P&G Share = 1 Gillette Share Issued 962mn shares Issued 79mn stock options Buyback $22bn of shares Investment Banker : Goldman Sachs & UBS AG

Similar presentations