Download presentation

Presentation is loading. Please wait.

1

Housing Price, Mortgage Lending and Speculative Bubble: a UK perspective Dr Qin Xiao University of Aberdeen Business School q.xiao@abdn.ac.uk

2

Contents 1. Introduction 2. Model 3. Empirical Investigations 4. Tentative Conclusions

3

1. Introduction

4

Introduction Experiments in laboratory asset markets suggest that When an asset market involves a large number of uninformed and inexperienced participants, bubble is a standard state of affairs. As bubble arises, even the informed and experienced traders may also ride on the bubble. (Smith, Suchanek et al. 1988; Caginalp, Porter et al. 1998; Caginalp, Porter et al. 2000a; Caginalp, Porter et al. 2000b; Caginalp, Porter et al. 2001) Such observations call for modifications to the conventional analytical framework which assumes that asset markets are continuously efficient.

Such observations call for modifications to the conventional analytical framework which assumes that asset markets are continuously efficient..")

5

Introduction Speculative asset price bubble is potentially an interesting topic to both policy makers and market investors Although they may not use the term “bubble” when talking about one. Investors are interested in making the most out of a bull market, without being stranded when the bubble deflates It is also an important issue for the policy makers, although most of them are so far reluctant to face it.

6

Introduction The bubble literature can be roughly divided into three strands. i. To prove or disprove the existence of a bubble in an asset price. ii. To measure the proportion of that price which is purely bubble. iii. To forecast How fast the bubble increases How likely the bubble will burst in the next period; When the bubble is purged eventually, in what manner will that happen?

7

2. Model

8

Model Model is based on (Caginalp and Ermentrout 1990; and Caginalp and Balenovich 1999)

")

9

Model Assumptions prices adjust as a result of excess demand; excess demand depends on the relative supply of the housing to the mortgage supply, both finite though not fixed; The supply of the mortgage is a function of the price dynamics

10

Model Each unit of wealth is in one of two states: housing or cash. The fraction of the wealth in housing asset is (1)

.")

11

Model Participants are both housing and cash holders. At any time, a typical investor will buy housing with probability k and sell it with probability 1-k Hence, the flow demand function for housing And the flow supply function (2) (3)

(3).")

12

Model k is a function of investor sentiment, (t). with (t) driven by two forces: trend following and mean reverting (5)

driven by two forces: trend following and mean reverting (5).")

13

Model 1: Bubble generation mechanism 2: price correction mechanism Price Dynamics (6)

")

14

Model Substitute equation 1 - 5 into 6, and define (7) LPLP

LPLP")

15

Model Assume the dynamics of the liquidity (8) P relax borrowing constraint L

P relax borrowing constraint L ")

16

3. Empirical Investigations

17

Empirical Questions How much of the house price and mortgage growth in UK can be explained by this model? The model implies two forces are at play: one is a stabilizer, the other destabilizer What is the empirical evidence on the relative strengths of the two?

19

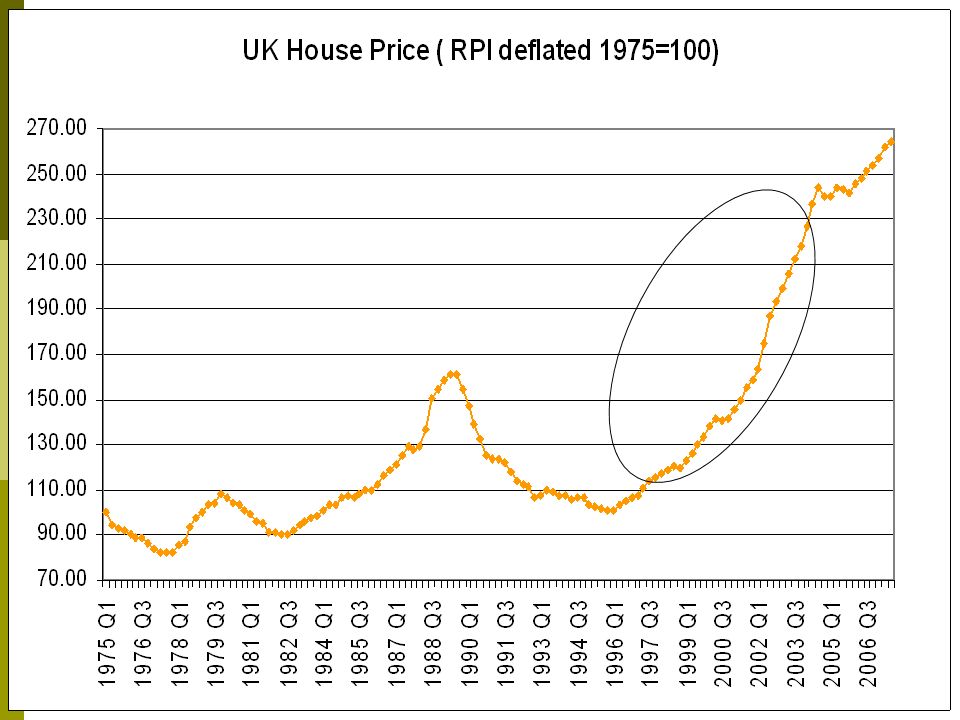

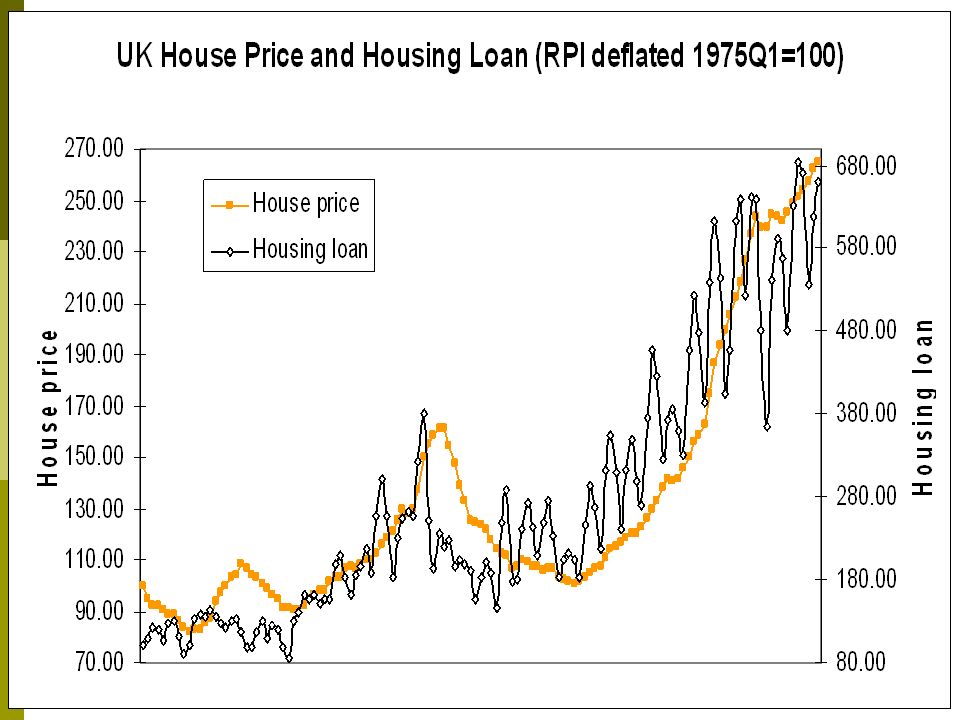

Adjust scale Show log changes

21

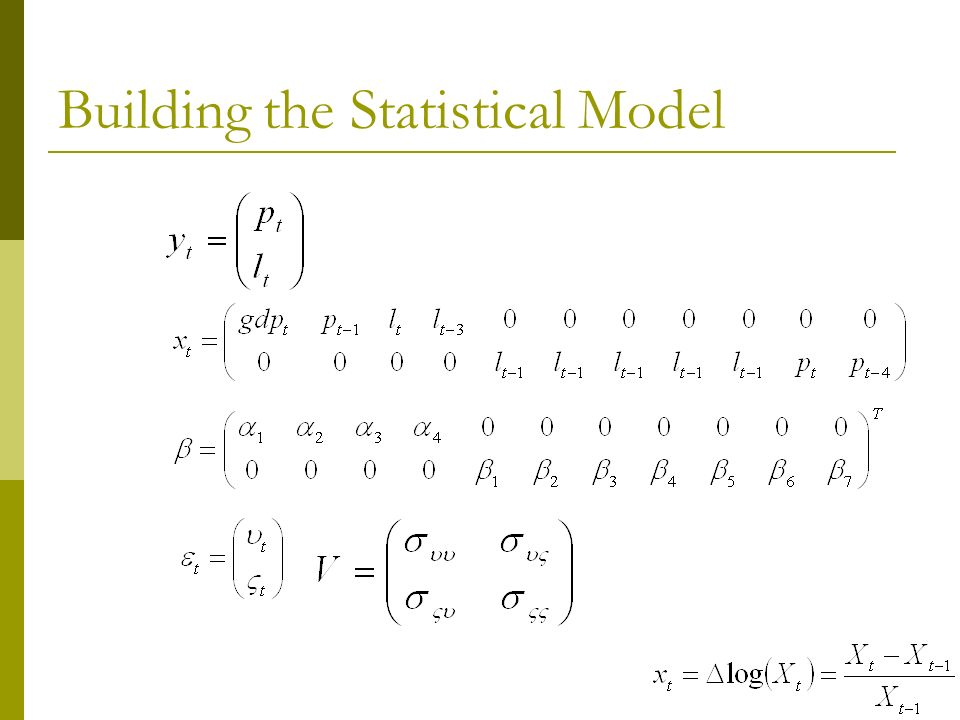

Building the Statistical Model The fundamental price: approximated by GDP. The liquidity: approximated by housing loan Cross products between pairs of regressors implied by the model are also examined. Variables are deflated by RPI if appropriate The regressors are selected using stepwise regressions.

22

Building the Statistical Model

24

It is possible that agents in the housing and/or the mortgage market behave asymmetrically in different phases of a market cycle.

25

Building the Statistical Model St: a state variable following a first-order two-state Markov chain, with transition probabilities

26

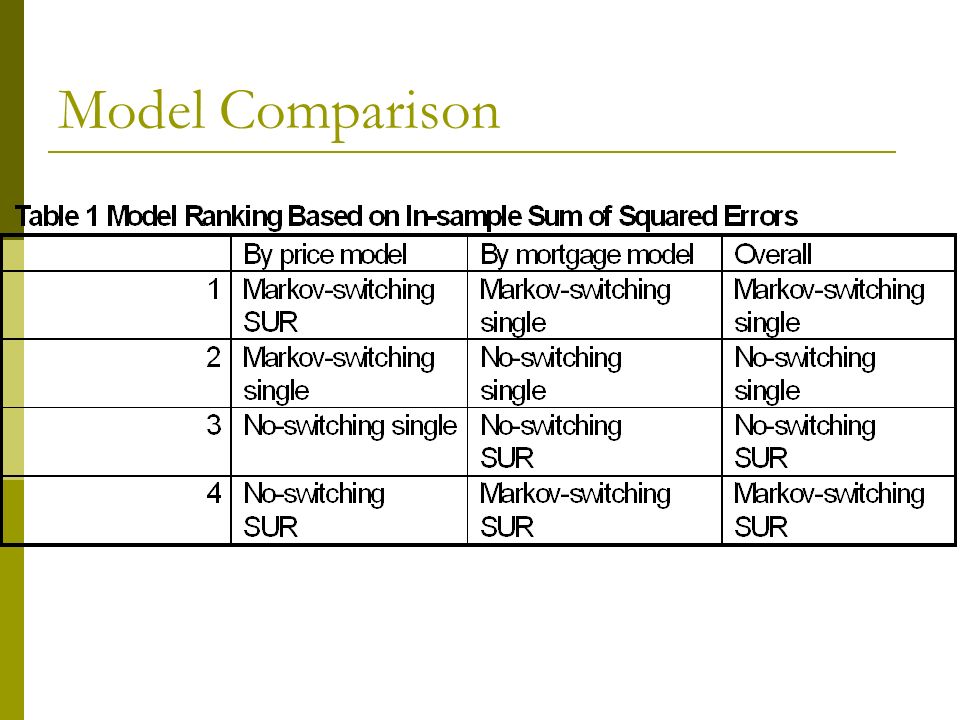

Model Estimation Four models are estimated by assuming no-switching and 0 (no switching SUR) With switching and 0 (Markov- switching SUR) No witching and = 0 (no switching single) With switching and = 0 (Markov- switching single)

With switching and 0 (Markov- switching SUR) No witching and = 0 (no switching single) With switching and = 0 (Markov- switching single)")

27

Model Comparison

29

Parameter Estimates Price is mean revertin g distablizer

30

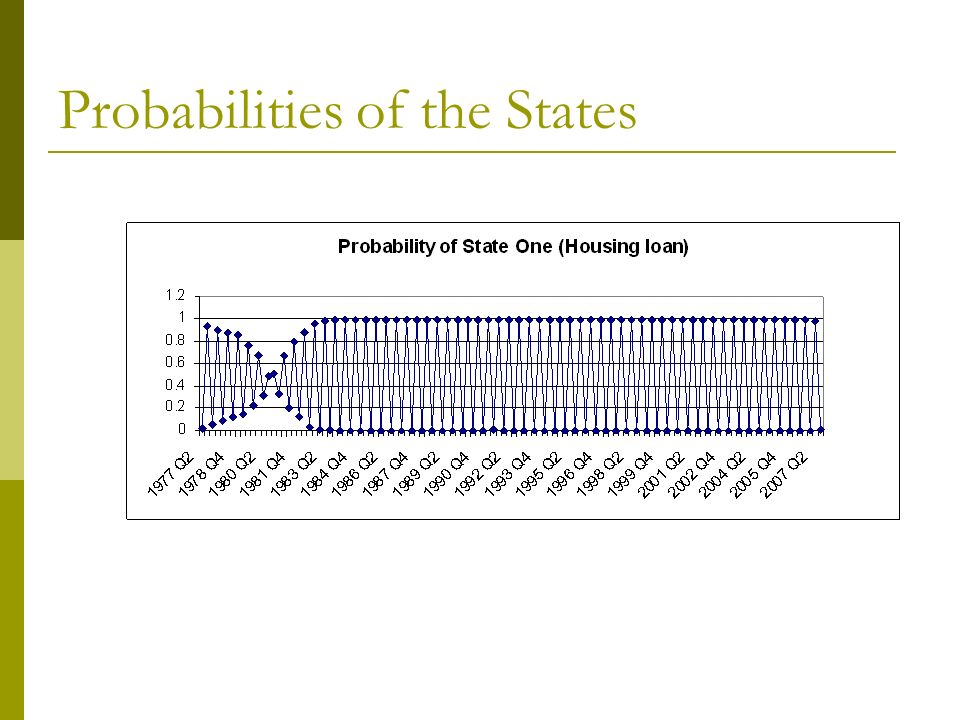

Probabilities of the States

32

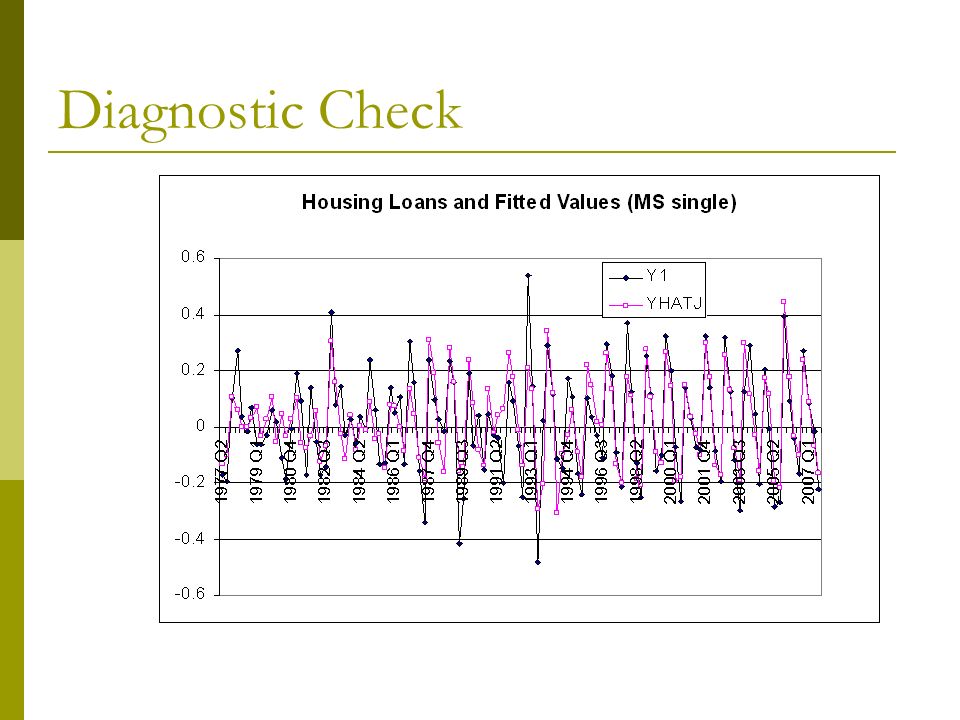

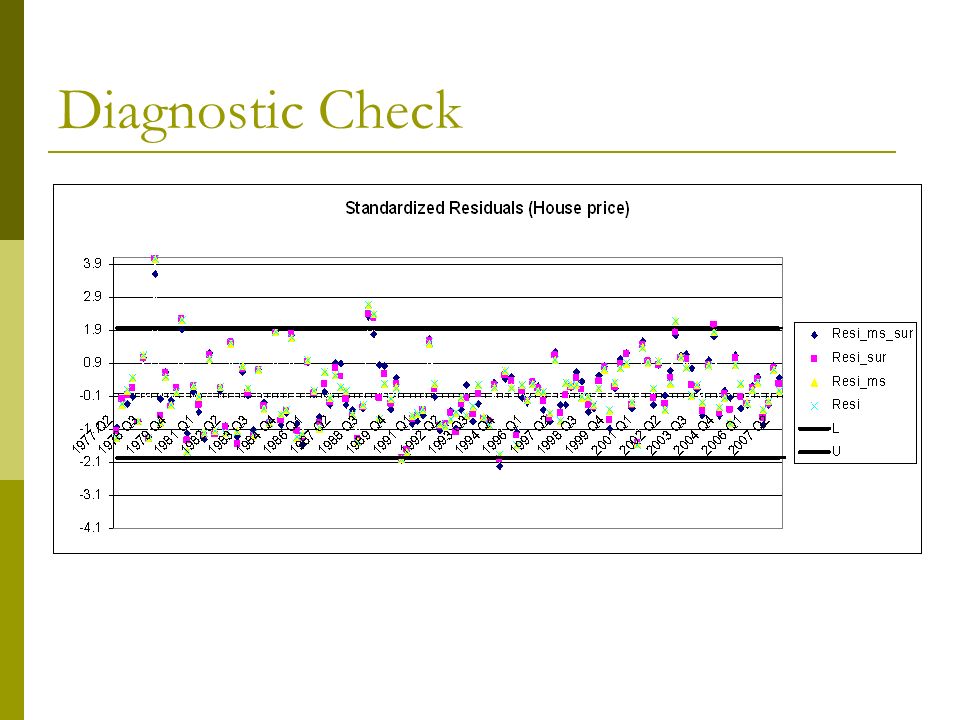

Diagnostic Check

36

Work remains Use a convergence measure to investigate the forecast power of the model The significance level of the Markov-switching model is to be established using Monte Carlo experiments Simulate the time paths of house price and housing loans implied by the statistical model to illustrate The origin of the bubble The propagation mechanism of the bubble The stability of the system

37

4. Tentative Conclusions

38

Tentative Conclusions We have investigated a model in which a housing price bubble arises as a result of trend following sentiment The model takes into account of the feedback effects between housing prices and mortgage lending; It also accounts for changing sentiment in the market The application of this model to UK housing market confirms that the model roughly explains 70% of the overall variations of both prices and housing loans. The significance and forecast ability of the model are still to be established

39

The End Thank you! Comments?

Similar presentations

Shanghai, China An Behavioral Model of Various Stock Market Dynamic Regimes Yu Tongkui (于同奎) Department of Systems Science, School of Management,>")