Download presentation

Presentation is loading. Please wait.

1

Steve R. Meyer, Ph.D. Vice-President, Pork Analysis EMI Analytics NPB Swine Educators – September 2015 U.S. Proteins Situation, Outlook & Issues

2

Key Issues for 2015 and Beyond U.S. corn and soybean crops – Done deal HPAI PEDv Beef herd rebuilding – pace and length Sow herd expansion – equity, incentive Broiler expansion – flock, productivity Domestic demand – economy, consumers Exports – World economy, U.S. dollar

5

Good/Exc ratings have trailed 2014 all year...... But exceeded 5-yr avgs. and not deteriorated

6

BIG difference in vegetative health vs. ‘14... and regionally

18

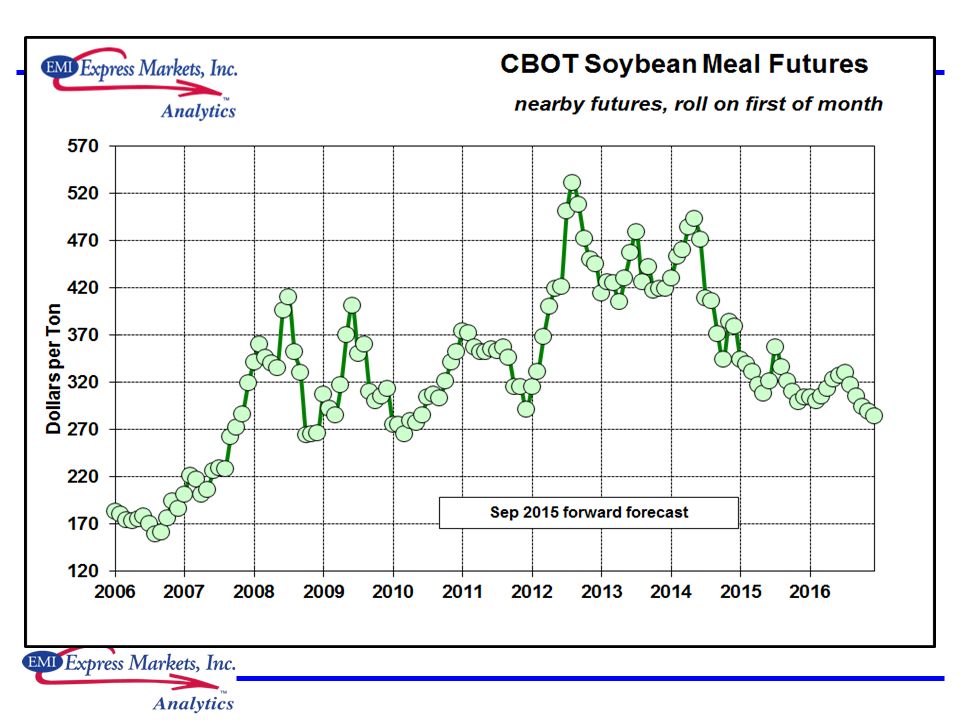

Grain prices imply lowest hog costs since ‘07...... With best operations at $63-$64/cwt carcass

19

3-species RPCE continues to grow...... But yr/yr gains are moderating – THEY HAD TO!

20

Chicken and beef still strong, yr/yr; pork slower

21

’14 per capita consumption was 201 lbs....... forecast to increase to 210 in ‘15 & ‘16

22

The evidence of strong demand is prices..... Beef record high; pork slightly higher in July

23

Consumer attitudes still improving-Peaking? Both indexes are still near their highs since ‘07

24

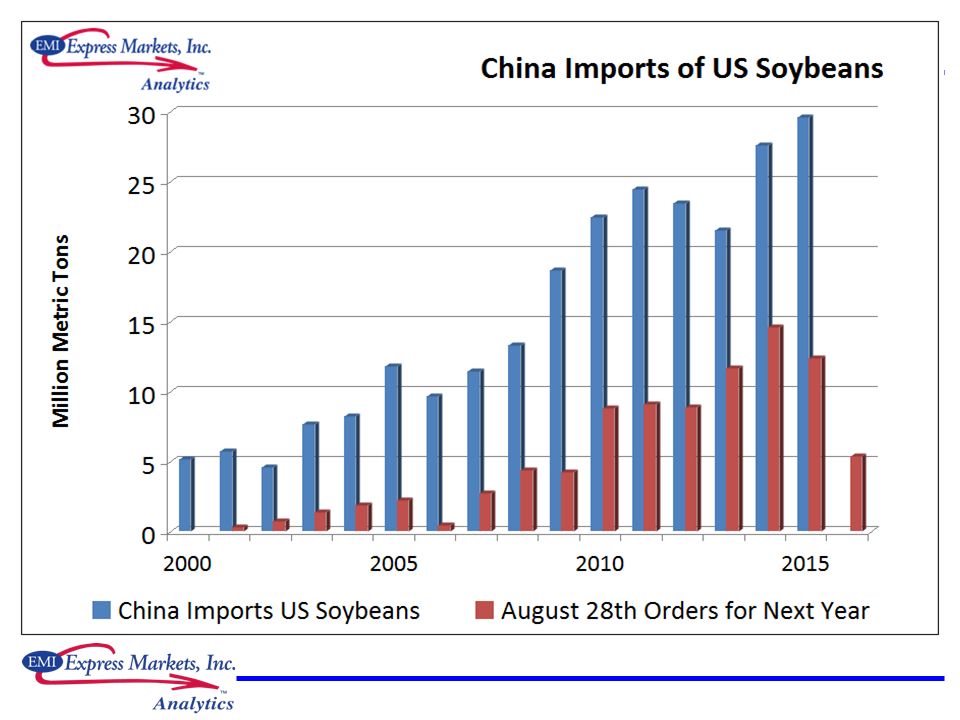

The biggest demand challenge is EXPORTS Beef and pork struggled in 2014 – esp H2

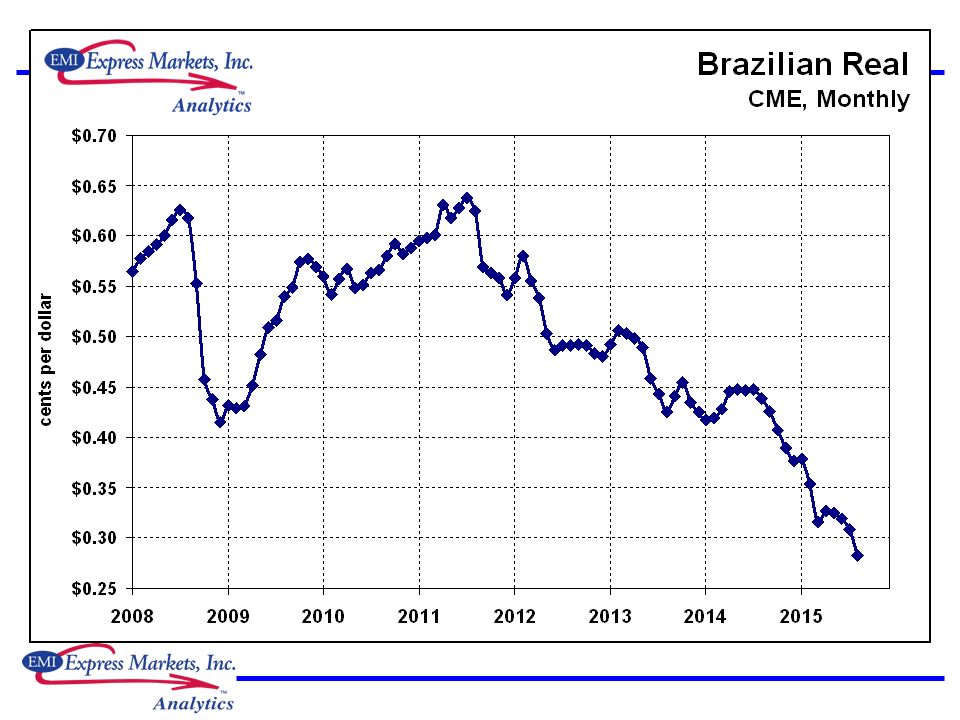

25

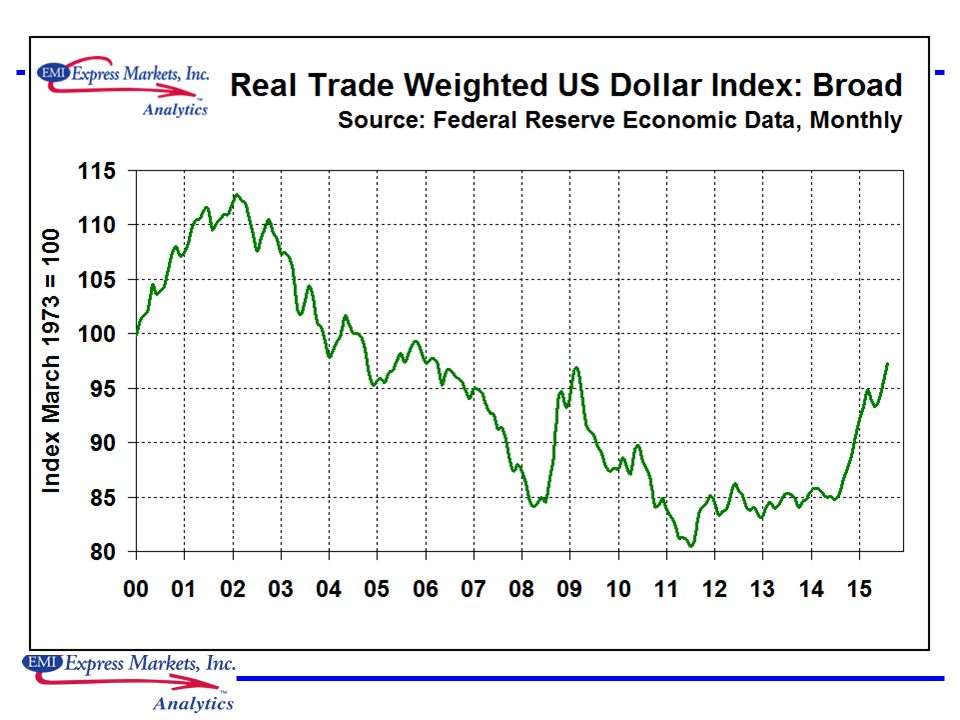

U.S. dollar – Yr/yr +20% on 7/4 but now “stable”

26

The key for beef growth is still WEATHER!

27

Beef: Unprecedented cow/calf profits!

28

Sharply lower female slaughter has led to... Significantly lower fed beef production MUCH tighter grinding beef supplies

29

USDA July 1 report shows expansion

30

Friday’s Cattle On Feed report

31

COF is gaining slightly on ’14 levels... The problem is front-end supplies of BIG cattle – 120+ supply was up 19% on 9/1 Cattle <$130, Choice cutout <$220... But placements are still BELOW 5-yr. lows

32

Wholesale ratios are back close to “normal”

33

Cattle and beef summary... Profits + Pastures = GROWTH – FINALLY! Some output growth in 2016 – calf crop, higher heifer and cow slaughter compared to very low rates this year, higher weights Fed cattle under tremendous pressure from large long-fed supplies – FINALLY taking their toll! Feeders pressured by feds – below $180 but for how long? Cows still near $100 but under seasonal pressure Question: Long-term impacts of VERY HIGH prices?

34

EMI Poultry Outlook Conference, April 23, 2015 Copyright © EMI, All Rights Reserved

35

North American Migratory Bird Flyways Source: US Fish and Wildlife Service

36

EMI Protein Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

37

EMI Protein Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

38

EMI Poultry Outlook Conference, April 23, 2015 Copyright © EMI, All Rights Reserved

39

EMI Protein Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

40

EMI Protein Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

41

EMI Protein Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

42

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

43

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

44

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

45

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

46

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

47

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

48

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

49

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

50

EMI Poultry Outlook Conference, September 2015 Copyright © EMI, All Rights Reserved

51

Hogs & pork: Key issue is far fewer PEDv accessions ‘14-’15 high wk. of 3/15 at 161 vs. 291 last year Many are G/F monitoring – NOT MUCH DEATH LOSS

52

More important: Few sow herd breaks Data from 902 sow farm, 22 of 26 large systems reporting, 2.376 mil. sows! Worst weeks in ‘15: 9 sow herds broke in two week in late February Anecdotal: MUCH smaller piglet losses even on farms that broke this year!

53

Sept H&P report was much as expected - neutral...... Still large front-end supplies, ’16 much like ‘15

54

Are the farrowing intentions reasonable? Recall that June intentions were VERY low – due to high numbers LAST YEAR 2015 Sep-Nov farrowing RATE is slightly below historical levels – omitting ‘13 and ‘14 Dec-Feb rate is VERY close to historicals We think the NUMBERS are reasonable – with Sep-Nov perhaps a bit low

55

And what about litter sizes? June-Aug was RECORD HIGH again! Litter growth is back on (or at least near!) the 2%/yr growth trend \ Normal seasonal – Sep- Nov and Dec-Feb will be lower Mar-May and Jun-Aug will likely be record highs What will PEDv do this winter???

the 2%/yr growth trend \ Normal seasonal – Sep- Nov and Dec-Feb will be lower Mar-May and Jun-Aug will likely be record highs What will PEDv do this winter .")

56

Weights: Lower than in ’15, rising seasonally... Weight reduction vs. year ago was a big reason for higher- than-expected slaughter in Q1-- ~2/3 of total Q1 change Weights were 208.6 last week – will rise to ~214 in Nov Normal seasonal implies -2 to -3% in Q3, -1 to 1.5% in Q4.. will REDUCE ‘15 prod by 1.5-2%, maybe more

57

2014 prod was down only 1.4%; ‘15 is up 8.1% YTD...Forecasts: Q3 up ~8%, Q4 up 3.7%, H1-’16 Unchg’d

58

Cutout: a normal seasonal – not so for hogs...... a normal fall seasonal puts us in mid-$60s in Q4

59

Pork packer margins struggled thru June..... But have recovered well – in spite of drop values

60

June H&P report has been VERY ACCURATE..... Sept report suggests steady yr/yr numbers

61

LH rally has taken ’15 back to profits...... And pushed ’16 to highest levels to date

62

Slaughter forecasts from Sept H&P

63

Price forecasts – a good year to come

64

Hog and pork summary Domestic demand growth has slowed – stay > zero? Export demand is recovering and will gain, yr/yr, vs. ‘14 for the rest of ‘15 – Likely finish at +2 to +4% Breeding herd is growing SLOWLY -- +60k from June to Sept, +230k since Dec ‘13 low -Plenty of equity and borrowing capacity -Some “pent up” expansion??? Q1 to Q3-’16 look very good for now Still some risk for Q4-’16 with hog numbers & pork supplies up 2 to 4% Packing capacity – new plants not up until ‘17

65

Risks MCOOL retaliatory tariffs – likely! How big? Major export disruption – small prob, HUGE impact PEDv impact this winter – immunity levels??? HPAI – will it get in SE US broiler areas this fall? Will it have any market impact? Will it be negative or positive? Slower demand growth or – GASP – lower demand? -Domestic: Will positive preferences continue? -Exports: World economy, strong $U.S. How much expansion in pigs and chicken?

66

Questions and Discussion?

Similar presentations