Download presentation

Presentation is loading. Please wait.

1

Copenhagen, 6 October Claus Schultze DG MARE Financing investments in Blue Growth

2

1. Funding landscape 2. Blue growth as smart specialisation 3. Interregional mapping and matching 4. Conclusions and next steps

3

Strategic + synergetic use of funds Significant ESIF and other EU funds are available for Blue Growth themes, in particular through ERDF. The fragmented nature of the funding landscape calls for: a)setting clear priorities on strategic and transformative activities creating value and impact b)maximising synergies between the funds. Up to one third of ESIF funding goes towards R+I, SME competitiveness and Climate Change. A significant amount of that will be channelled through Smart Specialisation strategies (RIS3) RIS3 determine the priority areas and roadmaps for ERDF R+I investments and set a framework for seeking synergies with other funds + programmes.

setting clear priorities on strategic and transformative activities creating value and impact b)maximising synergies between the funds. Up to one third of ESIF funding goes towards R+I, SME competitiveness and Climate Change. A significant amount of that will be channelled through Smart Specialisation strategies (RIS3) RIS3 determine the priority areas and roadmaps for ERDF R+I investments and set a framework for seeking synergies with other funds + programmes..")

4

Shared vs. direct funds All ESI Funds (ERDF (incl. ETC), ESF, Cohesion Fund = € 350 billion, EAFRD = €95.6 billion, EMFF= €5.7 billion) via grants, financial instruments, public procurement, trans-nat. cooperation, feasibility studies, administrative capacity building, tech. assistance Horizon2020 for mostly transnational research and innovation projects, incl. non-EU, grants, financial instruments…: €79.4 billion + BONUS progr. COSME for SME competitiveness, financial instruments, business support services, etc.: € 2 billion Erasmus+ for students, teachers, pupils mobility + training: €14.5 bn Creative Europe for culture & creative sector; grants, fin.instrument: €1.4 billion Digital service part of CEF for EU wide e-government and open data platforms: procurment and grants (€0.85 billion) LIFE programme for environment and climate, incl. financial instruments: € 3,4 billion Programme for Employment and Social Innovation ("EaSI"): € 0.92 billion European Fund for Strategic Investments (EFSI), € 315 billion Shared management Around €162 billion in 5 different ESI funds for innovation-drivers and take-up, i.e. research and innovation, SME competitiveness, digital growth and energy efficiency / renewable energies.

, ESF, Cohesion Fund = € 350 billion, EAFRD = €95.6 billion, EMFF= €5.7 billion) via grants, financial instruments, public procurement, trans-nat. cooperation, feasibility studies, administrative capacity building, tech. assistance Horizon2020 for mostly transnational research and innovation projects, incl. non-EU, grants, financial instruments…: €79.4 billion + BONUS progr. COSME for SME competitiveness, financial instruments, business support services, etc.: € 2 billion Erasmus+ for students, teachers, pupils mobility + training: €14.5 bn Creative Europe for culture & creative sector; grants, fin.instrument: €1.4 billion Digital service part of CEF for EU wide e-government and open data platforms: procurment and grants (€0.85 billion) LIFE programme for environment and climate, incl. financial instruments: € 3,4 billion Programme for Employment and Social Innovation ( EaSI ): € 0.92 billion European Fund for Strategic Investments (EFSI), € 315 billion Shared management Around €162 billion in 5 different ESI funds for innovation-drivers and take-up, i.e. research and innovation, SME competitiveness, digital growth and energy efficiency / renewable energies..")

5

Pl. Note: for DE and PL figure includes only OPs of regions with Baltic Sea Cost Available funding for Baltic Sea ERDF + ESF OPs

6

Alignment of EU funding to BSR goals Theoretically the ERDF OPs of the BSR MS/regions should already match the EUSBR priorities as the ERDF regulation asked for a certain alignment to mobilise mainstream funding (and not only INTERREG funding) for the implementation of macro-regional and sea-basin strategies. However among all the things MS/regions had to comply with this aspect has played out rather weakly: A June 2015 INTERACT Study looked into how the different OPs of MS/regions in the BSR region comes inter alia to the following conclusions: "EUSBR actors are not systematically involved in the elaboration of programmes" "proposals from different countries and OPs are insufficiently coordinated, and to a significant extent incompatible with each other" "Smart specialisation could guide cooperation efforts as one would seek to capitalise on complementarities… However, none of the programmes have yet developed a fully convincing cooperation model." http://admin.interact- eu.net/downloads/9401/Final_Report_Cooperation_methods_and_tools_to_support_the_EUSBSR.pdf

7

Smart Specialisation Priorities Blue Growth as a Smart Specialisation Priority Source: http://s3platform.jrc.ec.europa.eu/eye-ris3

8

Smart Specialisation is what successful regions and successful larger companies do in globalised economies. National or regional agenda for economic transformation Select economic activities with high transformative potential for the economy Valorise existing strengths and local specificities Mobilize local economic players as the main actors of economic change Seek interregional co-operation based on complementarity Coordinate financial and entrepreneurial resources to support the selected economic activities (synergies!) Define governance and monitoring mechanisms What is Smart Specialisation?

Define governance and monitoring mechanisms What is Smart Specialisation .")

9

10 most common RIS3 priorities in BSR Sustainable innovation ICT, creative media and Digital Agenda Health and Wellness Energy, Sustainable energy & renewables Tourism, restaurants & recreation KETs -Advanced manufacturing systems Agro-food KETs - Advanced materials Transporting & storage Service innovation

10

Detailed mapping of RIS3 priorities in the BSR is needed: mapping The Smart specialisation priorities/strategies of the BSR countries and regions are not just a paper exercise, they determine to a large extent the priorities for research, innovation and technology development funding by the ERDF/ESIF! A first mapping of RIS3 priorities related to blue growth has already been done by the Smart Specialisation Platform and presented in a meeting by the BSR PA Innovation in Malmo last year. To enable synergies and inform any future Baltic Masterplan approach as well as the future strategic action plan for the PA Innovation in the EUBSR we need an understanding/a mapping of what are relevant RIS3 priorities and sub-priorities in the BSR countries and regions related to blue growth value chains.

11

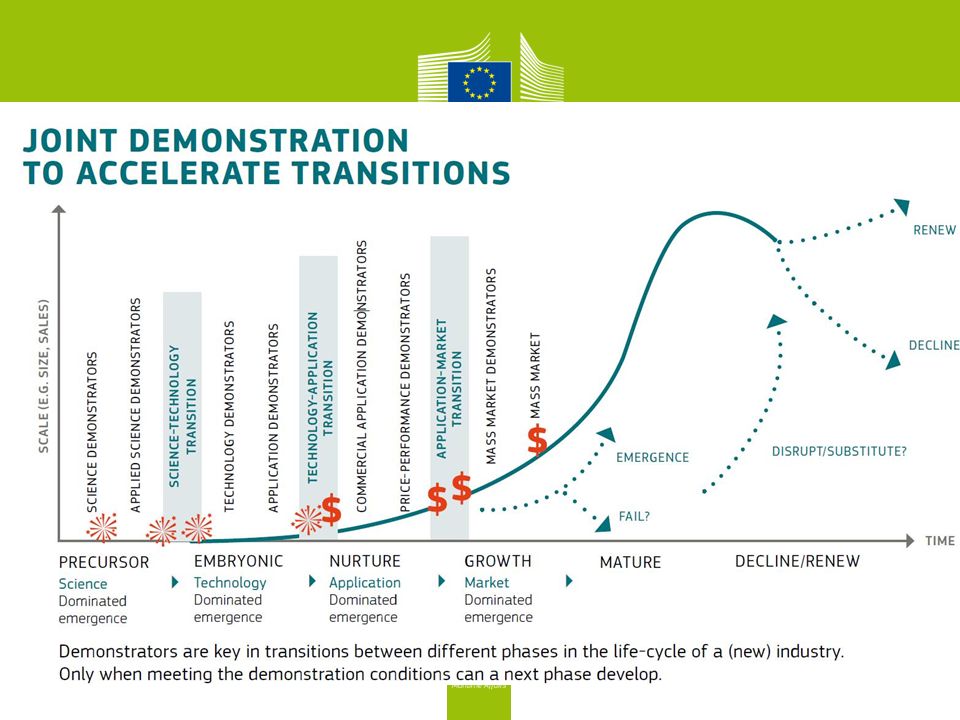

The interregional dimension: matching In RIS3 the interregional dimension is important for achieving critical mass, related variety and building stronger 'world-class' clusters But there are other benefits in particular in very diverse value chains such as the marine & maritime industry: There value creation is often remote from the end market (e.g. advanced non- marine engineering capacity supporting marine innovation). Many markets require an increasing proportion of value-adding services. This represents a major opportunity for joint growth as these larger value chains are not zero sum games. New markets such as in blue growth must build on expertise from the 'bed rock' firms active in traditional markets. Value chain analysis and interregional mapping and matching of core capabilities and cluster capacities can therefore be useful tools and open up opportunities for actors/regions with different capacities. They can help upscale local solutions and help build a project pipeline of strategic demonstrators for co-investment attractive to private R+I investment.

. Many markets require an increasing proportion of value-adding services. This represents a major opportunity for joint growth as these larger value chains are not zero sum games. New markets such as in blue growth must build on expertise from the bed rock firms active in traditional markets. Value chain analysis and interregional mapping and matching of core capabilities and cluster capacities can therefore be useful tools and open up opportunities for actors/regions with different capacities. They can help upscale local solutions and help build a project pipeline of strategic demonstrators for co-investment attractive to private R+I investment..")

12

Example: Offshore Wind Value Chain Source: Vanguard Initiative/Technopolis – RIS3 platform for advanced manufacturing scoping paper Why cooperate? Smart specialisation for several EU regions European value chains not well integrated, little knowledge exchange Industry-led interregional collaboration can generate economies of scale, enhance competitiveness, and create new opportunities

13

Conclusions and possible next steps Baltic Sea MS and regions should prioritise strategic and transformative blue growth investment in their RIS3/OP implementation (e.g. by putting a premium on such projects in their selection criteria, in particular innovative projects coming from SMEs) MS and regions (COM to support) should map the complementarities in their planned blue growth RIS3/ESIF investments to enable synergies and more targeted support in priority areas, work towards more joint programming (such as the JPI Oceans but for innovation) and common implementation roadmaps. S3 blue growth platforms should be set up or existing platforms used (e.g. the BSR Pas) to coordinate RIS3 blue growth-related investments. A model could be the 'Vanguard regions, which map regional activities and roadmaps in specific value chains related to RIS3 priority areas, followed by the targeted matching of cluster actors on specific investment opportunities/demonstrator ideas to facilitate joint/aligned investments and targeted demonstrator projects.

MS and regions (COM to support) should map the complementarities in their planned blue growth RIS3/ESIF investments to enable synergies and more targeted support in priority areas, work towards more joint programming (such as the JPI Oceans but for innovation) and common implementation roadmaps. S3 blue growth platforms should be set up or existing platforms used (e.g. the BSR Pas) to coordinate RIS3 blue growth-related investments. A model could be the Vanguard regions, which map regional activities and roadmaps in specific value chains related to RIS3 priority areas, followed by the targeted matching of cluster actors on specific investment opportunities/demonstrator ideas to facilitate joint/aligned investments and targeted demonstrator projects..")

14

Methodology for mapping/matching The first step is to collect data on regional activities in the subject area (Eye@RIS3 and the Region OP database) based on relevant keywords/categories. A list of such keywords/categories need to be composed. On that basis the (lead)regions can be identified that are likely to engage themselves in European matchmaking. The second step is to start the inventory of relevant strategic frameworks and (regional) networks in the domain, e.g. the European Blue Growth Action Plan, the BSR Action Plan. This exercise will focus on the type on investments that are targeted in the smart specialisation areas (focus on demonstration?). The EFSI Advisory Hub can be closely involved to co-define a thematic Investment Platform. In parallel, the (lead)regions and the relevant regional cluster organisations have to be brought around the table (to co-define the priorities and provide the more detailed information for mapping the value chains). This requires adequate governance on the operational level to give them ownership.

regions can be identified that are likely to engage themselves in European matchmaking. The second step is to start the inventory of relevant strategic frameworks and (regional) networks in the domain, e.g. the European Blue Growth Action Plan, the BSR Action Plan. This exercise will focus on the type on investments that are targeted in the smart specialisation areas (focus on demonstration ). The EFSI Advisory Hub can be closely involved to co-define a thematic Investment Platform. In parallel, the (lead)regions and the relevant regional cluster organisations have to be brought around the table (to co-define the priorities and provide the more detailed information for mapping the value chains). This requires adequate governance on the operational level to give them ownership..")

15

The VI maps regional activities and roadmaps in specific value chains related to RIS3 priority areas, followed by the targeted matching of cluster actors on specific investment opportunities/demonstrator ideas to facilitate joint/aligned investments and targeted demonstrator projects.

19

Forthcoming maritime-related events EUBSR Maritime Stakeholders, Copenhagen, 06/10 S3 Platform, Blue Growth Workshop, Canary Islands, 08- 09/10 Blue Careers 2015, Cyprus, 08-09/10 MedCoast Coastal Management, Varna, 13-15/10 Waste Free Oceans, Brussels, 14/10 Regional Cruise Dialogue in the Med, Olbia, 16-17/10 EMODNET Open Conference, Oostende, 20/10 Ocean Energy, High Level Meeting, Dublin, 20/10 Atlantic Stakeholder Platform, Brest, 29/10 Safer Seeas, Brest, 26-30/10 Union for the Mediterranean, Ministerial on Blue Economy, 17-18/11 UfM, Forum on Blue Economy, 1/12

Similar presentations