Download presentation

Presentation is loading. Please wait.

1

Chapter 13 Money and Banking Monetary Policy (Federal Reserve)

")

2

Money any object that is generally accepted as payment for goods and services and repayment of debts in a given country or socio-economic context wampum

3

the three functions of money 1. As a Medium of Exchange. Otherwise we’d have to barter for everything we need.

4

the three functions of money 2. Money as a unit of Account, measure of value: In other words, a way to compare the values of goods and services.

5

the three functions of money 3. Money as a Store of Value: money keeps its value if you hang on to it in your wallet and you can spend it in the future.

6

4. Standard of Deferred Payment money is used as a standard benchmark for specifying future payments for current purchases, that is, buying now and paying later. A common example is a car loan. The amount of those future payments are stated in terms of money.

7

The 6 Characteristics of Money 1. Durability 2. Portability 3. Divisibility 4. Uniformity 5. Limited Supply 6. Acceptability

8

Sources of Money’s Value 1. Commodity Money: a commodity is an object that has value such as cattle, precious stones and salt. These have been used in various societies as commodity money.

9

2. Representative Money In other words the holder can exchange money for something else of value.

10

Money Supply the total amount of money available in an economy at a particular point in time.

11

Velocity of money (also called velocity of circulation) the rate at which money changes hands. If velocity is high, money is changing hands quickly, and a relatively small money supply can fund a relatively large amount of purchases. Velocity associates the amount of economic activity associated with a given money supply. V = Y/M where V is the velocity, Y is the real GDP, M is total Money Supply (or M s ).

..")

12

Money supply: M1 M1: amount of money in circulation and money held in current (checking or demand) accounts. The narrowest measure of money supply. Cash (coins & currency) makes up the greatest part of M1 M1 is used to forecast inflation (think of the cash you can get your hands on in an hour’s notice: wallet, ATM) “You have 1 hour to get me $500, or I drop your little bear!”

makes up the greatest part of M1 M1 is used to forecast inflation (think of the cash you can get your hands on in an hour’s notice: wallet, ATM) You have 1 hour to get me $500, or I drop your little bear! .")

13

Money supply: M2 M1 + money held in savings account or other deposits which are not immediately available. (“You have until 9:00 AM to get me the $500, or I shred your little bear!) other deposits: time deposits, money market accounts

other deposits: time deposits, money market accounts.")

14

Money supply: M3 M2 + longer term deposits such as time deposits and repos Repos or Repurchase agreements A form of short-term borrowing for dealers in government securities. The dealer sells the government securities to investors, usually on an overnight basis, and buys them back the following day. Since 2006, M3 is no longer published or revealed to the public by the Fed (“You have 4 days to get me the $500, or I shred your little bear!)

.")

15

Credit cards = money Short term loan (at crazy high interest rates! 18% or more) http://abcnews.go.com/video/playerIndex?id=8075403

id=")

16

Commercial Banks A financial institution that provides services such as a accepting deposits and giving business loans. (and individuals too)

.")

17

Savings and Loans (S&Ls) An institution that accepts savings at interest and lends money to savers chiefly for home mortgage loans and may offer checking accounts and other services.

An institution that accepts savings at interest and lends money to savers chiefly for home mortgage loans and may offer checking accounts and other services.")

18

Commercial Banks vs S&Ls Both give out loans to both businesses & individuals Both deposit money in interest bearing accounts from businesses & individuals: checking accounts, savings accounts & CDs Used be difference, with deregulation during Reagan’s administration they’ve become the same.

19

How the value of the dollar is determined In the early 1930s, the U.S. set the value of the dollar at a single, unchanging level: 1 ounce of gold was worth $35. After the gold standard ended in 1933, the US dollar was no longer based on gold. United States Bullion Depository Fort Knox http://www.youtube.com/watch?v=4ua1LdV Fe9I

20

British Pound The pound sterling (silver), established in 1560–61 by Elizabeth I

, established in 1560–61 by Elizabeth I")

21

Fiat Money (Not the Italian Car) A Fiat is an order of decree, the US Government decreed that the dollar is “legal tender”.

A Fiat is an order of decree, the US Government decreed that the dollar is legal tender .")

22

“In God We Trust” Fiat money is based solely on faith in the government’s ability to maintain the currency’s value. Currency’s value is maintained by controlling the Money Supply Actually, in the Federal Reserve We Trust

23

How the value of the dollar is determined Floating currency exchange: Countries all over the world purchase other countries currencies, which determines the value. http://money.cnn.com/data/currencies/

24

How the value of the dollar is determined The American Dollar is strong because many many countries buy a whole lot of US Dollars. Why? 75% of all global business transactions are done in $US.

25

FEDERAL RESERVE NOTES The Federal Reserve Act of 1913, made US Dollars the dominant form of paper currency in America.

26

It is important for the government to “manage” money B/C the Money Supply determines the value of $US, printing money can devalue the $US and create inflation and chaos.

27

the demand for money Transactions demand (Dt) : Consumers need cash for purchases. Asset Demand (Da): As an alternative asset to stocks, bonds or baseball cards. Dt + Da = Dm (Total Money Demand

: As an alternative asset to stocks, bonds or baseball cards. Dt + Da = Dm (Total Money Demand.")

28

Federal Reserve, b. 1914 Ben Bernanke and the Federal Reserve control the Supply of Money (how many dollars are out there circulating) so as to maintain the value of the $ US. Alan Greenspan Ben Bernanke

so as to maintain the value of the $ US. Alan Greenspan Ben Bernanke.")

29

http://www.youtube.com/watch?v=ol3mEe8TH7w

30

The structural parts of the Federal Reserve System: A) Board of Governors: the 7 members are appointed by the President and confirmed by the Senate to serve 14- year terms of office.

Board of Governors: the 7 members are appointed by the President and confirmed by the Senate to serve 14- year terms of office.")

31

The structural parts of the Federal Reserve System: B) Open Market Committee: the 7 members of the Board of Governors and five Reserve Bank presidents

Open Market Committee: the 7 members of the Board of Governors and five Reserve Bank presidents")

32

The structural parts of the Federal Reserve System: C) Federal Advisory Council: The 12 Presidents of the 12 Reserve Banks advises the Board.

Federal Advisory Council: The 12 Presidents of the 12 Reserve Banks advises the Board.")

33

The structural parts of the Federal Reserve System: D) The 12 Reserve Banks: The Bankers’ Banks. Carry out Monetary Policy

34

The structural parts of the Federal Reserve System: E) Commercial Banks: privately held banks borrow money from Federal Reserve Banks @ DISCOUNT RATE. Are regulated by gov’t agencies SEPARATE from the FED.

35

Commercial Banks Banks borrow $$ from each other (to maintain reserved requirements) @ the FEDERAL FUND RATE (higher than Discount Rate)

")

36

The structural parts of the Federal Reserve System: F) State Banks: The twelve regional Reserve Banks supervise state member banks. Provides services that help banks’ reputations Bradley, OK

37

The structural parts of the Federal Reserve System: G) National Banks: an ordinary private bank operating within a specific regulatory structure, which may or may not operate nationally. Chartered by the Fed. They must maintain minimum levels of reserves with one of the 12 Federal Reserve banks

38

The structural parts of the Federal Reserve System: H) Thrift Institutions: a depository for consumer savings, most common: savings and loan associations and savings banks

Thrift Institutions: a depository for consumer savings, most common: savings and loan associations and savings banks")

39

The 7 functions of the Federal Reserve System 1.Issue Currency: coins/prints $$ Retires tired old dollar bills, shreds them and replaces them with new bills.

40

The 7 functions of the Federal Reserve System 2. Set Reserve Requirements (or cash reserve ratio) for banks: the % of deposits banks must hold in vault for demand withdrawals. 10% of deposits must be in bank Money Multiplier = 1/RR or 10 1/ Reserve requirement multiple Banking System can expand Money supply (Ms) by. Run on a Bank

for banks: the % of deposits banks must hold in vault for demand withdrawals. 10% of deposits must be in bank Money Multiplier = 1/RR or 10 1/ Reserve requirement multiple Banking System can expand Money supply (Ms) by. Run on a Bank.")

41

The 7 functions of the Federal Reserve System 3. Lend $$ to member Banks: rate of interest charged DISCOUNT RATE Major Monetary Policy tool

42

DISCOUNT RATE Major Monetary Policy tool

43

The 7 functions of the Federal Reserve System 4. Check Collection between banks: the Fed banks transfer the $ from one bank to another. if your grandmother sends you a check & you deposit in your bank, it goes through http://www.youtube.com/watch?v=DCOm4osfWn8

44

The 7 functions of the Federal Reserve System 5. Fiscal Agent for Fed Gov’t: taxes, Gov’t spends $$ deposited sells/buys Gov’t Bonds aka OPEN MARKETS OPERATIONS MAJOR Monetary Policy Tool to regulate Money Supply Increase Ms – Buy bonds Decrease Ms – Sell Bonds

45

The 7 functions of the Federal Reserve System 6. Supervise Banks: pop visit banks to make sure regulations are met. reserve requirements are adequate, loans are properly secure

46

The 7 functions of the Federal Reserve System 7. Control Money Supply: thru Discount Rate, Buy/Sell Bonds & Reserve Requirements % (almost never used) The Money Supply determines the value of money (price) Inflation: value decreases Recession/Depression: value increases

The Money Supply determines the value of money (price) Inflation: value decreases Recession/Depression: value increases.")

47

2 reasons why bank and thrift failures are bad 1) People won’t put their $$ in a Bank: Banks have no $$ to lend to Businesses and new jobs are not created 2) The failure on one bank can create a domino effect and many more banks also fail.

People won’t put their $$ in a Bank: Banks have no $$ to lend to Businesses and new jobs are not created 2) The failure on one bank can create a domino effect and many more banks also fail.")

48

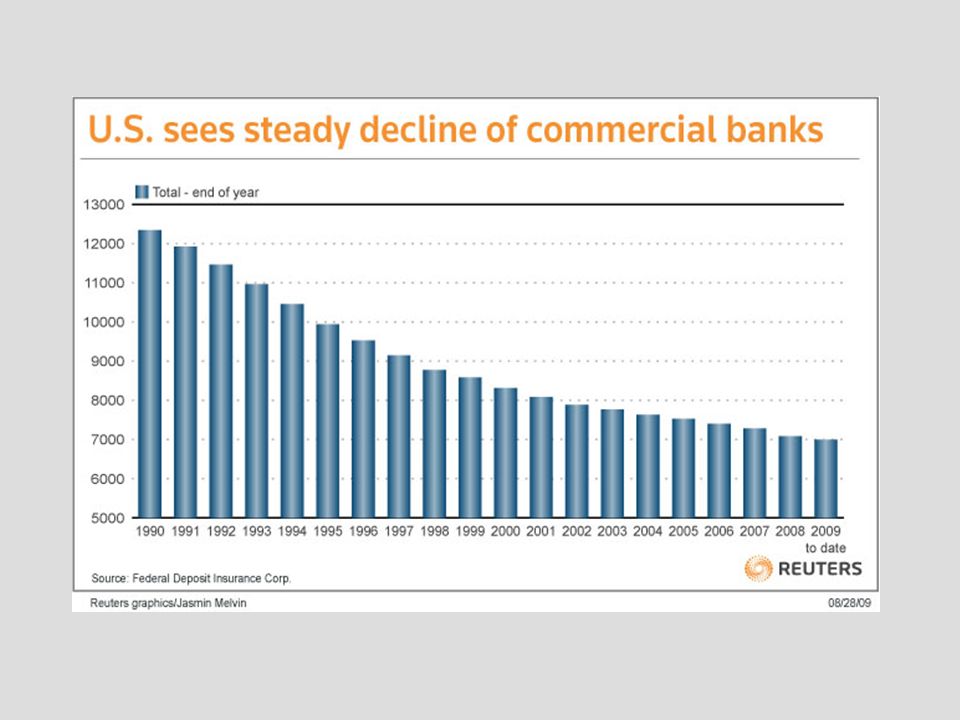

Why banks and thrifts have declined In 1980 Banks & thrifts held 60% of US financial assets, by 2002 only 30%. A) Other asset management institutions have grown: pension funds, insurance & Mutual Funds expanded their holdings B) Consolidation: one bank absorbs others C) Banks that couldn’t keep up failed

Other asset management institutions have grown: pension funds, insurance & Mutual Funds expanded their holdings B) Consolidation: one bank absorbs others C) Banks that couldn’t keep up failed.")

50

Electronic Money Internet banking: credit card transfers, paying bills on-line

Similar presentations