Download presentation

Presentation is loading. Please wait.

1

ACTG 3110 Chapter 2 – Conceptual Framework Underlying Financial Accounting

2

The Conceptual Framework Underlying rationale; theoretical basis for standards Used to support new principles Provide consistency among existing principles Speed up deliberations and passage of new principles Seven concepts; six in use (1,2,4,5,6,7)

")

3

Basic Components SFAC 1 - Objectives SFAC 2 - Qualitative Characteristics SFAC 3 - Superseded by SFAC 6 SFAC 4 - Nonprofit reporting SFAC 5 - Recognition and Measurement Criteria SFAC 6 - Elements of Financial Statements SFAC 7 – Using Cash Flow Information and Present Value in Accounting Measurements

5

SFAC No. 1 Basic Objectives – The “Why” Users of financial statements –Investors and creditors –Other users Provide information that is –Useful in making decisions –Helpful in assessing future cash flows –Useful in determining what is owned and owed and their changes over time

6

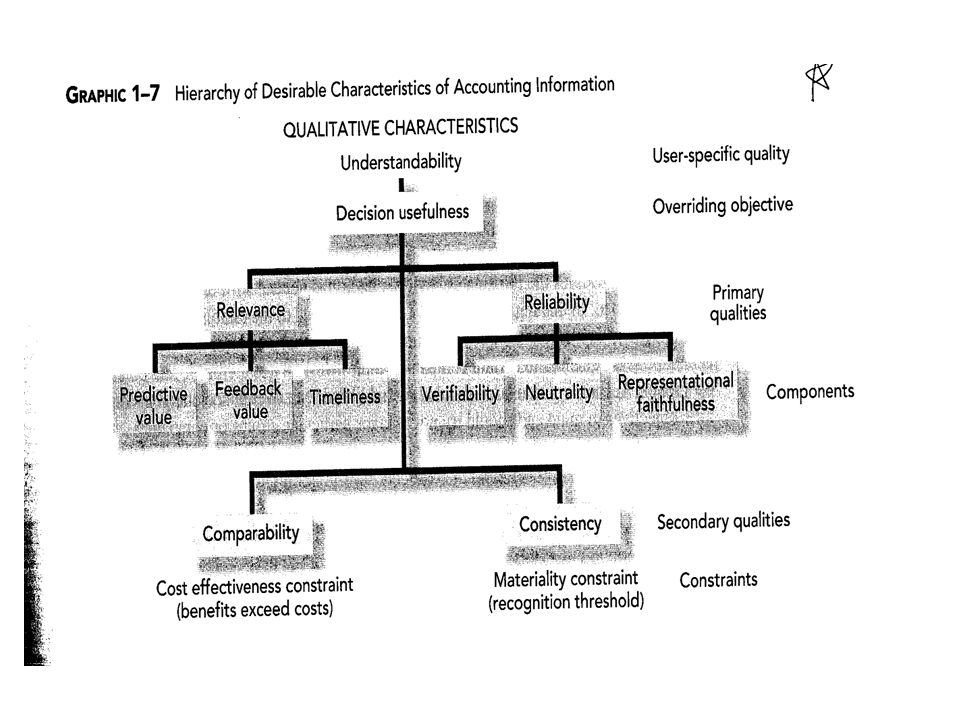

SFAC No. 2 Qualitative Characteristics Decision Usefulness and Understandability is overriding objective Primary Qualities –Relevance (can make a difference) Predictive value, Feedback value,Timeliness –Reliability (dependable) Representational faithfulness,Verifiability, Neutrality Often a trade-off occurs between relevance and reliability

Predictive value, Feedback value,Timeliness –Reliability (dependable) Representational faithfulness,Verifiability, Neutrality Often a trade-off occurs between relevance and reliability.")

7

SFAC No. 2 (Continued) Secondary Qualities –Comparability –Consistency Cost effectiveness Materiality

Secondary Qualities –Comparability –Consistency Cost effectiveness Materiality.")

8

SFAC No. 6 – Basic Elements Emphasis shifted to balance sheet Assets - probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events Liabilities- Probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events

9

SFAC 6 (continued) Equity: Assets - liabilities (residual interest); represents the ownership interest. Investments by Owners – Increases in net assets of a particular enterprise resulting from transfers to it from other entities of something of value to obtain or increase ownership interests (or equity) in it.

in it..")

10

SFAC 6 (continued) Distributions to owners – Decreases in net assets of a particular enterprise resulting from transferring assets, rendering services, or incurring liabilities by the enterprise to owners. Distributions to owners decrease ownership interests (or equity) in an enterprise.

in an enterprise..")

11

SFAC No. 6 (continued) Comprehensive Income - Includes traditional net income plus all other changes in equity except investments by owners or distributions to owners Revenues - Inflows of assets or settlements of liabilities, or both, during a period from delivering or producing goods, or rendering services, or other earnings activities that constitute the entity’s major or primary operations.

Comprehensive Income - Includes traditional net income plus all other changes in equity except investments by owners or distributions to owners Revenues - Inflows of assets or settlements of liabilities, or both, during a period from delivering or producing goods, or rendering services, or other earnings activities that constitute the entity’s major or primary operations..")

12

SFAC No. 6 (Continued) Expenses: Outflows or using up of assets or incurring of liabilities during a period as a result of the delivery or production of goods, the rendering of services, or other earnings activities that constitute an entity’s major or primary operations Gains and losses - increases and decreases in equity that arise from peripheral or incidental transactions other than those with owners.

Expenses: Outflows or using up of assets or incurring of liabilities during a period as a result of the delivery or production of goods, the rendering of services, or other earnings activities that constitute an entity’s major or primary operations Gains and losses - increases and decreases in equity that arise from peripheral or incidental transactions other than those with owners..")

13

SFAC No. 5 Recognition and Measurement The “how” implementation Basic Assumptions –Economic Entity Assumption –Going Concern Assumption –Monetary Unit Assumption –Periodicity Assumption

14

SFAC No. 5 (Continued) Basic Principles –Historical Cost –Revenue Recognition –Matching –Full Disclosure

Basic Principles –Historical Cost –Revenue Recognition –Matching –Full Disclosure.")

15

SFAC No. 5 (Continued) Constraints –Cost-Benefit relationship –Materiality –Industry practices –Conservatism

Constraints –Cost-Benefit relationship –Materiality –Industry practices –Conservatism.")

16

IASB Conceptual Framework International Accounting Standards Board Framework is similar to the FASB Framework with a few language differences Prudence (conservatism) IASB, Canadian Accounting Standards Board and FASB are working on a NEW CONCEPTUAL FRAMEWORK

IASB, Canadian Accounting Standards Board and FASB are working on a NEW CONCEPTUAL FRAMEWORK")

Similar presentations