Download presentation

Presentation is loading. Please wait.

1

Principals of Managerial Finance 9th Edition Chapter 3 Financial Statements, Taxes, Depreciation, and Cash Flow

2

Learning Objectives Describe the basic purpose and components of the stockholder’s report. Review the format and key components of the income statement, the balance sheet, the statement of retained earnings, the statement of cash flows, and the procedures for consolidating international financial statements. Understand the effect of depreciation and other non- cash charges on the firm’s cash flows.

3

Learning Objectives Determine the depreciable value of an asset, its depreciable life, and the amount of depreciation allowed each year for tax purposes using the modified accelerated cost recovery system (MACRS). Analyze the firm’s cash flows and develop and interpret the statement of cash flows. Discuss the fundamentals of business taxation of ordinary income and capital gains, and he treatment of tax losses.

4

The guidelines used to prepare and maintain financial records and reports are known as generally accepted accounting principles (GAAP). GAAP is authorized by the Financial Accounting Standards Board (FASB). Public corporations with more than $5 million in assets and more than 500 stockholders are required by the SEC to provide heir stockholders with an annual stockholders report. The Stockholders’ Report

. Public corporations with more than $5 million in assets and more than 500 stockholders are required by the SEC to provide heir stockholders with an annual stockholders report. The Stockholders’ Report.")

5

The income statement provides a financial summary of a company’s operating results during a specified period. Although they are prepared annually for reporting purposes, they are generally computed monthly by management and quarterly for tax purposes. Financial Statements The Income Statement

6

Financial Statements

7

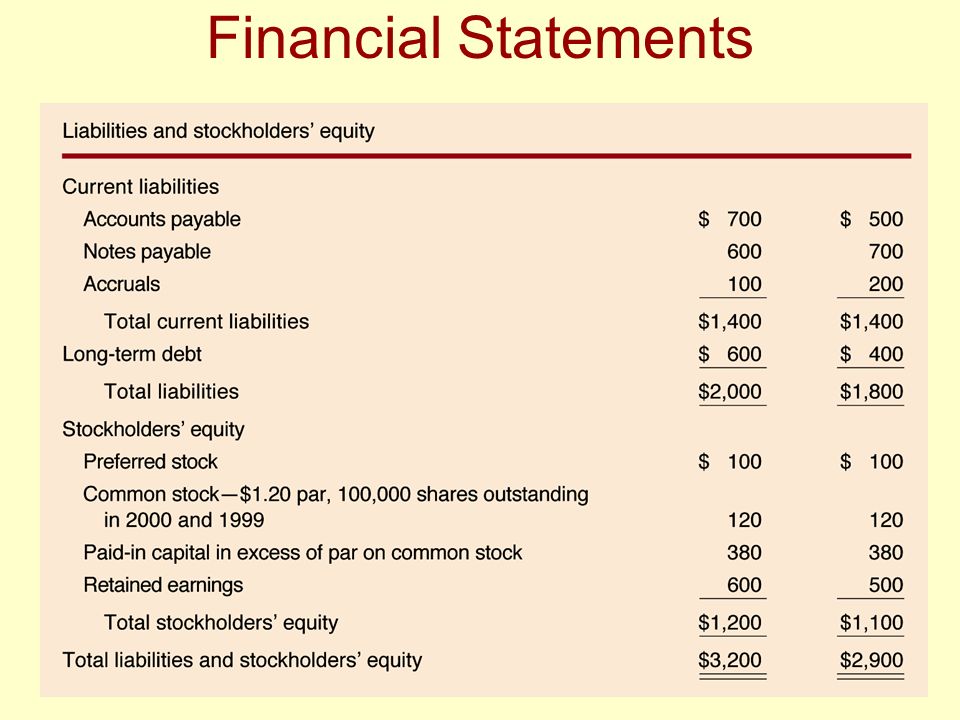

The balance sheet presents a summary of a firm’s financial position at a given point in time. Assets indicate what the firm owns, equity represents the owners’ investment, and liabilities indicate what the firm has borrowed. Financial Statements The Balance Sheet

8

Financial Statements

10

The statement of retained earnings reconciles the net income earned and dividends paid during the year, with the change in retained earnings. Financial Statements Statement of Retained Earnings

11

Financial Statements

12

The statement of cash flows provides a summary of the cash flows over the period of concern, typically the year just ended. This statement not only provides insight into a company’s investment, financing and operating activities, but also ties together the income statement and previous and current balance sheets. Financial Statements Statement of Cash Flows

13

Financial Statements

14

FASB 52 mandated that U.S. based companies translate their foreign-currency denominated assets and liabilities into dollars using the current rate (translation) method. Under the translation method, companies translate foreign-currency-denominated assets and liabilities into dollars for consolidation with the parent company’s financial statements. Income statement items are usually treated similarly, although they can also be translated at the average exchange rate during the period (year). Consolidating International Financial Statements

method. Under the translation method, companies translate foreign-currency-denominated assets and liabilities into dollars for consolidation with the parent company’s financial statements. Income statement items are usually treated similarly, although they can also be translated at the average exchange rate during the period (year). Consolidating International Financial Statements.")

15

Equity accounts, on the other hand, are translated into dollars by using the exchange rate that prevailed when the parent’s equity investment was made (the historical rate). Retained earnings are adjusted to reflect each year’s operating profits (or losses), but does not consider any profits or losses resulting from currency changes. Instead, translation gains and losses are accumulated in an equity reserve account called the cumulative translation adjustment. Consolidating International Financial Statements

, but does not consider any profits or losses resulting from currency changes. Instead, translation gains and losses are accumulated in an equity reserve account called the cumulative translation adjustment. Consolidating International Financial Statements.")

16

Translation gains (losses) increase (decrease) this account balance. However, the gains and losses are not “realized” until the parent company sells or shuts down the subsidiary. Consolidating International Financial Statements

17

Both individuals and businesses must pay taxes on income. The income of sole proprietorships and partnerships is taxed as the income of the individual owners, whereas corporate income is subject to corporate taxes. Both individuals and businesses can earn two types of income -- ordinary and capital gains. Under current law, tax treatment of ordinary income and capital gains change frequently due frequently changing tax laws. Business Taxation

18

Ordinary income is earned through the sale of a firms goods or services and is taxed at the rates depicted in Table 3.4 on the following slide. Business Taxation Ordinary Income Example Calculate federal income taxes due if taxable income is $80,000. Tax =.15 ($50,000) +.25 ($25,000) +.34 ($80,000 - $75,000) Tax = $15,450

+.25 ($25,000) +.34 ($80,000 - $75,000) Tax = $15,450.")

19

Business Taxation Ordinary Income

20

Business Taxation Average & Marginal Tax Rates Example What is the marginal and average tax rate for the previous example? Marginal Tax Rate = 34% Average Tax Rate = $15,450/$80,000 = 19.31% A firm’s marginal tax rate represents the rate at which additional income is taxed. The average tax rate is the firm’s taxes divided by taxable income. Table 3.5 illustrates average tax rates at various levels of taxable income.

21

Business Taxation

22

Tax on Interest & Dividend Income For corporations only, 70% of all dividend income received from an investment in the stock of another corporation in which the firm has less than 20% ownership is excluded from taxation. This exclusion is provided to avoid triple taxation for corporations. Unlike dividend income, all interest income received is fully taxed.

23

Business Taxation Debt versus Equity Financing Example A firm with 100,000 shares outstanding needs to raise an additional 500,000 in capital. They can do so by selling bonds that pay 6% interest or by issuing 10,000 additional shares at $50/share. The firm pays $3.00 in dividends for each share outstanding. In calculating taxes, corporations may deduct operating expenses and interest expense but not dividends paid. This creates a built-in tax advantage for using debt financing as the following example will demonstrate.

24

Business Taxation Debt versus Equity Financing

25

Business Taxation Debt versus Equity Financing As the example shows, the use of debt financing can increase cash flow and EPS, and decrease taxes paid. The tax deductibility of interest and other certain expenses reduces their actual (after-tax) cost to the profitable firm. It is the non-deductibility of dividends paid that results in double taxation under the corporate form of organization.

cost to the profitable firm. It is the non-deductibility of dividends paid that results in double taxation under the corporate form of organization..")

26

Business Taxation Capital Gains A capital gain results when a firm sells an asset such as a stock held as an investment for more than its initial purchase price. The difference between the sales price and the purchase price is called a capital gain. For corporations, capital gains are added to ordinary income and taxed like ordinary income at the firm’s marginal tax rate.

27

Business Taxation Tax Loss Carrybacks and Carryforwards Corporations experiencing losses can obtain tax relief by using tax loss carrybacks/carryforwards. A tax loss carryback/carryforward allows corporations experiencing operating losses to carry tax losses back (in time) up to 3 years and forward (in time) for as many as 15 years. The law required that losses first be carried back, applying them to the earliest year allowable, and progressively moving forward until the loss has been fully recovered or the carryforward period has passed.

up to 3 years and forward (in time) for as many as 15 years. The law required that losses first be carried back, applying them to the earliest year allowable, and progressively moving forward until the loss has been fully recovered or the carryforward period has passed..")

28

Depreciation Depreciation is the systematic charging of a portion of the costs of fixed assets against annual revenues over time. Depreciation for tax purposes is determined by using the modified accelerated cost recovery system (MACRS). On the other hand, a variety of other depreciation methods are often used for reporting purposes.

. On the other hand, a variety of other depreciation methods are often used for reporting purposes..")

29

Depreciation Financial managers are much more concerned with cash flows rather than profits. To adjust the income statement to show cash flows from operations, all non-cash charges should be added back to net profit after taxes. By lowering taxable income, depreciation and other non-cash expenses create a tax shield and enhance cash flow. Depreciation & Cash Flow

30

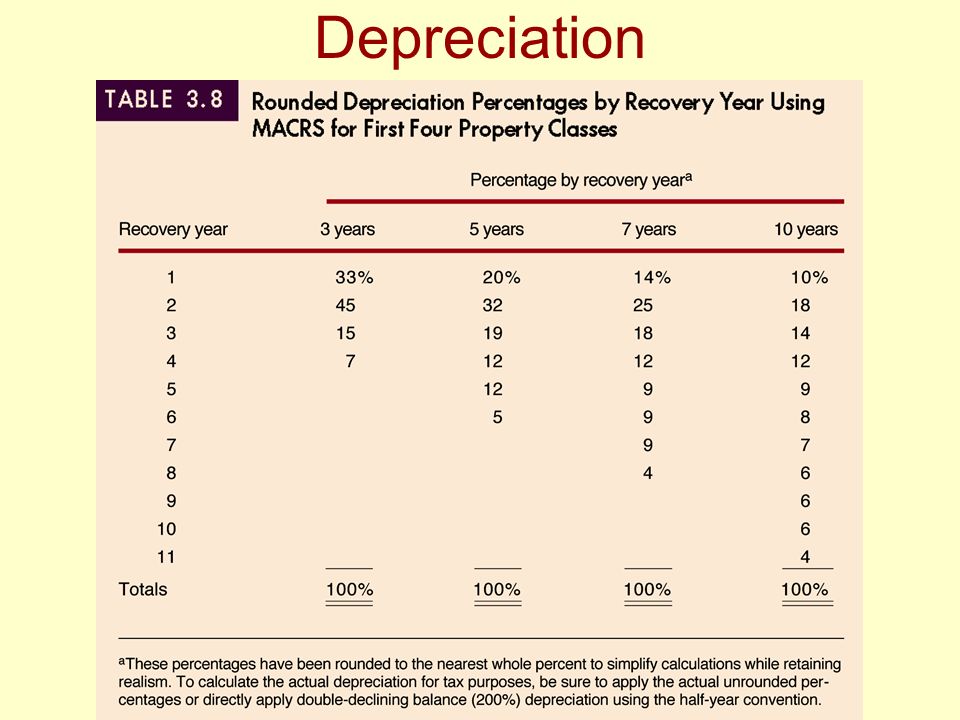

Depreciation Under the basic MACRS procedures, the depreciable value of an asset is its full cost, including outlays for installation. No adjustment is required for expected salvage value. For tax purposes, the depreciable life of an asset is determined by its MACRS recovery predetermined period. MACRS property classes and rates are shown in Table 3.7 and Table 3.8 on the following slides. Depreciable Value & Depreciable Life

31

Depreciation

33

An Example Elton Corporation acquired, for an installed cost of $40,000, a machine having a recovery period of 5 years. Using the applicable MACRS rates, the depreciation expense each year is as follows:

34

Question? If as a business owner you could design a design a depreciation schedule to look the way you wanted it to, what would it look like? Exactly! As long as you have positive taxable income, you would always prefer to expense it (100% depreciation). Remember, a dollar saved today is worth more than a dollar saved tomorrow! Depreciation

. Remember, a dollar saved today is worth more than a dollar saved tomorrow. Depreciation.")

35

Analyzing the Firm’s Cash Flows The statement of cash flows summarizes the firm’s cash flow over a given period of time. The statement of cash flows is divided into three sections: –operating flows –investment flows –financing flows The nature of these flows is shown in Figure 3.2 on the following slide.

36

Analyzing the Firm’s Cash Flows

37

Classifying Sources & Uses of Cash The statement of cash flows essentially summarizes the sources and uses of cash during a given period.

38

Analyzing the Firm’s Cash Flows Classifying Sources & Uses of Cash

39

Analyzing the Firm’s Cash Flows Classifying Sources & Uses of Cash

40

The Statement of Cash Flows

41

Analyzing the Firm’s Cash Flows Interpreting the Statement of Cash Flows The statement of cash flows ties the balance sheet at the beginning of the period with the balance sheet at the end of the period after considering the performance of the firm during the period through the income statement. “Net Increase (decrease) in cash and marketable securities should be equivalent to the difference between the cash and marketable securities on the balance sheet at the beginning of the year and the end of the year.

in cash and marketable securities should be equivalent to the difference between the cash and marketable securities on the balance sheet at the beginning of the year and the end of the year..")

Similar presentations

and what a firm owes (liabilities) Asset = Liability.>")