Download presentation

Presentation is loading. Please wait.

1

Stock Presentation Consumer Discretionary Sector November 17 th, 2009 Tiffany Arnett, Pinjalim Bora, Sam Brickell

2

Sector Recommendation Recap Short Term Hold on to the underweight position of the sector in the SIM portfolio. However, reshuffle the underlying composition. Long Term Depending on the positive organic sales growth in the 3 rd and the 4 th quarter, decide on increasing the weight to that of S&P 500

3

Currently, Consumer discretionary is underweight by 1.60% Current Sector weights & Composition

4

Current Sector Composition

5

Stock Recommendation Sell CoachMCD Buy DRI, 124 bps GME, 128 bps

6

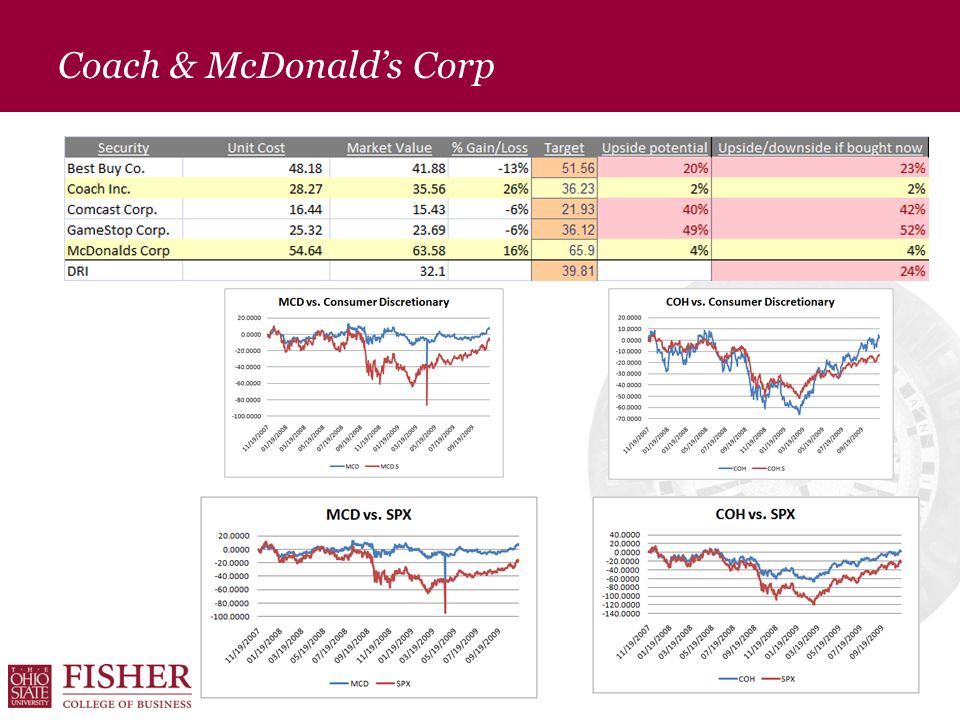

Business: McDonald’s: World’s largest fast-food restaurant chain Coach: High-end accessories retailer Key Drivers: MCD: Global expansion, increasing menu variety and value to the customer COH: New designers to drive brand creativity Risks: Both are in mature companies in competitive industries Coach & McDonald’s Corp

8

COH AbsoluteHighLowMedianCurrent P/Trailing E37.96.825.618.5 P/Forward E30.07.921.616.8 P/B14.13.19.35.8 P/S8.21.56.33.5 P/CF36.55.822.915.4 MCD Absolute HighLowMedianCurrent P/Trailing E21.614.217.217.6 P/Forward E19.513.616.116.0 P/B5.32.53.75.2 P/S3.81.82.63.8 P/CF15.89.612.613.5 MCD Relative to S&P 500 HighLowMedianCurrent P/Trailing E1.5.821.10.97 P/Forward E1.40.811.10.93 P/B3.10.81.22.3 P/S3.71.21.83.4 P/CF1.80.91.3 COH Relative to S&P 500 HighLowMedianCurrent P/Trailing E2.10.591.61.0 P/Forward E1.80.681.40.98 P/B4.82.03.22.6 P/S5.32.04.23.1 P/CF3.40.72.11.4 Coach & McDonald’s Corp – Valuation Analysis

9

COHMCD Relative to Industry MedianCurrentMedianCurrent P/Trailing E1.41.10.871.0 P/Forward E1.21.00.871.0 P/B3.01.60.80.9 P/S4.12.71.21.8 P/CF1.61.11.01.1 Coach & McDonald’s Corp – Valuation Analysis

10

Both are fairly valued Very little upside Can use past profits from these to invest in better opportunities Why Sell Coach & McDonald’s Corp

12

Darden Restaurants – Business Analysis Business Owns restaurants in North America. Red Lobster (690 restaurants) Olive Garden (691 restaurants) Longhorn Steakhouse (321 restaurants) The Capital Grille (37 restaurants) Bahama Breeze (24 restaurants) Seasons 52 (8 restaurants) A small amount of franchising activity in other countries.

Olive Garden (691 restaurants) Longhorn Steakhouse (321 restaurants) The Capital Grille (37 restaurants) Bahama Breeze (24 restaurants) Seasons 52 (8 restaurants) A small amount of franchising activity in other countries..")

13

Darden Restaurants – Business Analysis Key Drivers Same store sales (decreased 1.4%, compared to 5.6% for benchmark) New store openings (71 in 2009, 50-55 projected for 2010) Relative Success of expansion of newer concepts - Bahama Breeze - The Capital Grille - Seasons 52

New store openings (71 in 2009, projected for 2010) Relative Success of expansion of newer concepts - Bahama Breeze - The Capital Grille - Seasons 52")

14

Darden Restaurants – Business Analysis Risks Poor Sales (although not as dependent upon the state of the economy as you might think) - Poor sales could evolve out of many things though. Increased food costs (hedged somewhat by commodity contracts) Problems related to high level of indebtedness - Ratio of Consolidated Earnings from Continuing Operations to Fixed Charges is 4.2. - If problems arise the solution is simply to slow down building of new restaurants for a while.

Problems related to high level of indebtedness - Ratio of Consolidated Earnings from Continuing Operations to Fixed Charges is If problems arise the solution is simply to slow down building of new restaurants for a while..")

15

Darden Restaurants – Financial Analysis ROE is currently 25.4%, which is above median of 19.9%. Operating Margin is currently 9.0%. Net Profit Margin is 5.5%. Current Ratio is 0.5. Percentage LT debt to total capital reached a high immediately after the merger and has been decreasing at a steady rate ever since so they are being effective at working off their debt from the merger.

16

Darden Restaurants – Valuation Analysis o Price to Trailing Earnings is 11.4. o Price to Forward Earning is 11.5. o Price to Book is 2.7. o Price to Cash Flow is 6.6. All of these are below the historical medians.

17

Darden Restaurants – Valuation Analysis Currently P/E is 11.4. Median for past 5 years is 17.0, and Median for past 15 years is 16.8. Currently below it’s historical median point relative to industry, sector, and market. So ratios likely to expand going forward to return to usual levels. Target Price $39.81, stock currently trades at about $32.10 - (24% discount)

.")

18

Darden Restaurants – Valuation Analysis

19

Darden Restaurants – Recommendation Buy 124 Basis Points of DRI. Primary Catalysts Current P/E of 11.4 Increase in sales likely to come from an improving economy and improving consumer confidence. Less investor concern about their debt as they work to decrease it. Possible price floor from dividend yield (3.1% currently). Primary Risks Possible liquidity problem due to the debt load. Change in consumer’s tastes.

. Primary Risks Possible liquidity problem due to the debt load. Change in consumer’s tastes..")

21

GameStop Corporation (Ticker: GME) Business “World’s largest retailer of video game products and PC entertainment software” Sell new and used video game hardware, software and accessories + PC entertainment software and other merchandise. As of August 1 2009, 6333 stores operating in US, Australia, Canada and Europe Also, operate www.gamestop.com as the ecommerce platform and publish Game Informer - “industry’s largest multi-platform video game magazine in the United States based on circulation”.

22

Key Drivers Unique used game trading platform. Change in sales mix towards used video game products; higher margins. Aggressive growth through acquisitions - Electronics Boutique(2005), Micromania(2008) GameStop Corporation (Ticker: GME)

, Micromania(2008) GameStop Corporation (Ticker: GME).")

23

Risks Increasing gamer engagement by video game publishers. Business model not sustainable in the long run. High Correlation with economic indicators Consumer spending (R=0.92) Retail Sales (R=0.95) GDP ( R=0.72) GameStop Corporation (Ticker: GME)

Retail Sales (R=0.95) GDP ( R=0.72) GameStop Corporation (Ticker: GME).")

27

Forecast slow but steady growth in profitability driven by growth in margins over a 5 year period Also growth in Australia and Canada “In a Q3 business update, GameStop (NYSE: GME) said it still sees Q3 EPSGME of $0.27-$0.33…”. – www.streetInsider.com GameStop Corporation (Ticker: GME)

.")

29

Currently, Consumer discretionary is underweight by 1.60% Final Sector weights & Composition

30

Consumer Discretionary Sector Presentation Questions & Discussion

31

McDonalds Corporation (Ticker: MCD)

")

32

GameStop Corporation (Ticker: GME)

")

Similar presentations

$47.46 Wednesday, April 11, 2007.>")

- Extremely high barriers.>")

Fall 2009.>")