Download presentation

Presentation is loading. Please wait.

1

International Risk Sharing Across the Twentieth Century David S. Jacks Simon Fraser University and NBER Christopher M. Meissner University of California, Davis & NBER

2

► How much risk sharing has there been over the last 100 years? ► We use an asset pricing model to find out (cf. Brandt, Cochrane and Santa Clara, 2006) ► We find that risk sharing has been high despite other research to the contrary.

► We find that risk sharing has been high despite other research to the contrary..")

3

International Risk Sharing to Date ► Key idea is that consumers can rely on foreign asset markets to cover risks. ► If so then consumption should be highly correlated across countries and exchange rates should not move (much).

..")

4

International Risk Sharing to Date ► But many studies (too many to mention) document that consumption correlations are very low. ► Co-movement of C with real exchange rate is opposite to what theory would expect.

5

Risk sharing in the long run ► Consumption data is too poor prior to WWII to make much sense. ► Historical evidence of U-shaped integration. ► Price-based evidence is a prospect

6

The BCSC Measure ► BCSC use an asset pricing model to measure how much exchange rate movement impedes international risk sharing. ► The key is to note that real exchange rates move positively with the difference in the growth of marginal utility.

7

The Risk Sharing Measure ► Which relies on the idea that:

8

The Risk Sharing Measure ► M asks how much of the total volatility of the growth of marginal utility (h,a) is accounted for by exchange rate volatility?

is accounted for by exchange rate volatility")

9

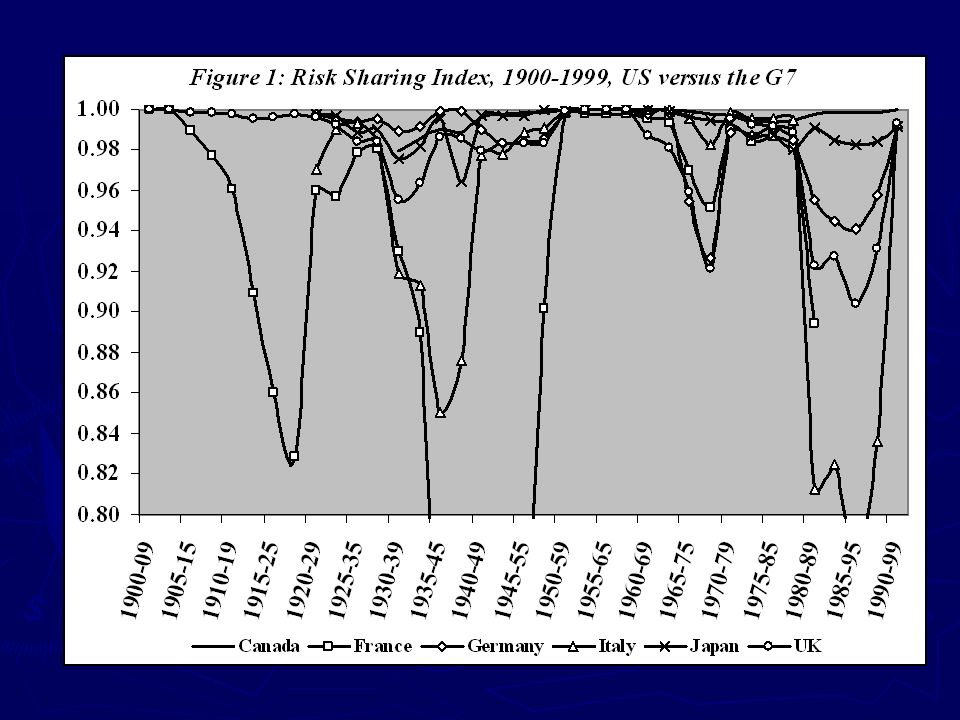

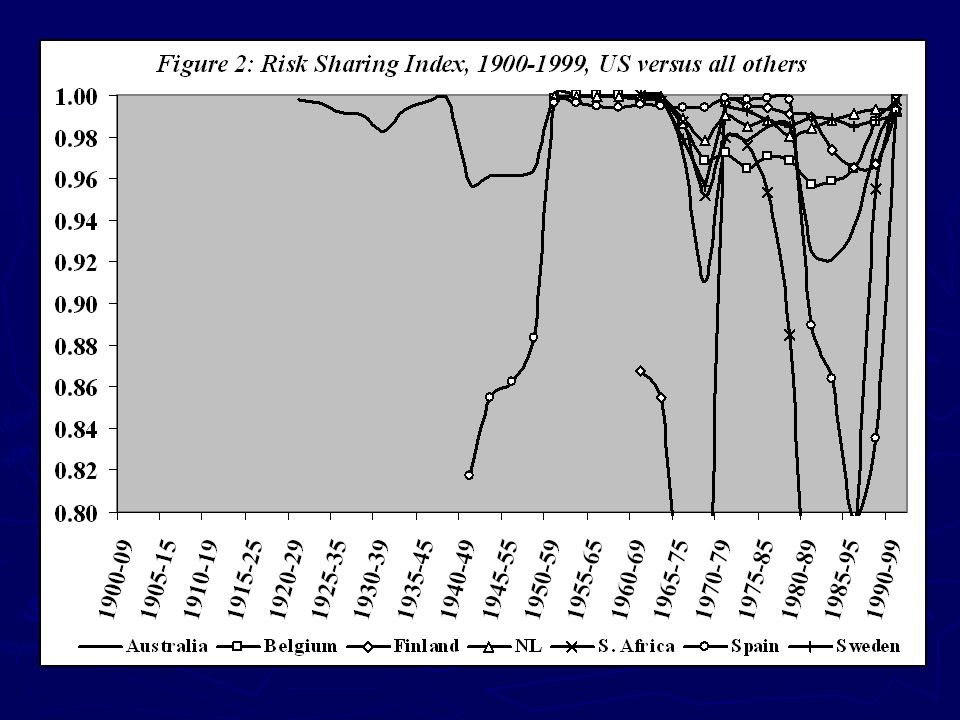

Data ► We calculate “excess” stock market returns (US and foreign) and exchange rate volatility. Use ex post real returns. ► Australia (1920-1999), Belgium (1950-1999), Canada (1935-1999), Finland (1960-1999), France (1900-1989), Germany (1925-1999), Italy (1925-1999), Japan (1920- 1999), Netherlands (1950-1999), South Africa (1960- 1999), Spain (1940-1999), Sweden (1960-1999), and the UK (1900-1999). ► We calculate the index with overlapping ten year periods 1900-1909, 1905-1914, 1910-1919,…, 1990-1999,

, Belgium ( ), Canada ( ), Finland ( ), France ( ), Germany ( ), Italy ( ), Japan ( ), Netherlands ( ), South Africa ( ), Spain ( ), Sweden ( ), and the UK ( ). ► We calculate the index with overlapping ten year periods , , ,…, ,.")

11

Results ► For US and the G7 countries in our sample: the measure never dips below 0.80 with one exception (Italy in 1985-1995). The average value for the six series is 0.97 92% of observations being above 0.90 in value. Interestingly, there are times when risk sharing uniformly declines. These periods are 1930-1939, 1965- 1975, and 1980-1995. M for US and UK is at its maximum 1900-1915

13

Robustness ► A consumption based measure can be calculated directly. It is much lower…0.36. This may measure overall risk sharing. M only captures risk shared via incomplete asset markets. ► What additional (uncovered risks) would be necessary to lower overall risk sharing? High volatility (50%) and a negative correlation of -0.4 would get us 0.36. ► Also, exchange rate volatility would have to be very high (>50%) to drop risk sharing downwards. ► A “true” equity premium of 1% could lower the measure to 0.3. ► Cross-border holdings are low but this is not necessarily an explanation. Income shocks may be correlated or risk can be shared by other means.

would be necessary to lower overall risk sharing. High volatility (50%) and a negative correlation of -0.4 would get us ► Also, exchange rate volatility would have to be very high (>50%) to drop risk sharing downwards. ► A true equity premium of 1% could lower the measure to 0.3. ► Cross-border holdings are low but this is not necessarily an explanation. Income shocks may be correlated or risk can be shared by other means..")

14

Further Thoughts ► This is a price based measure. Similar structures can give rise to seemingly high integration. ► Still, this means that there is little risk to be shared. Risk sharing is not that bad.

15

Further Thoughts & Conclusions ► The BCSC measure of risk sharing displays high risk sharing over the twentieth century with some (important) dips. ► Previous research on capital market integration pre-1950 looks at finance in the development process. ► More work could be done to think about the risk sharing benefits of such integration.

Similar presentations

2013 summary report Model developed by the Economist Intelligence Unit (EIU)>")

IBUS 302: International Finance Topic 16–Portfolio Analysis Lawrence Schrenk, Instructor.>")

>")