Download presentation

Presentation is loading. Please wait.

1

Ch. 9: The Exchange Rate and the Balance of Payments.

Exchange rates Definition Determinants Short run Long run Purchasing power parity Interest rate parity Balance of payments accounts Causes of an international deficit Alternative exchange rate policies and their long-run effects

2

Currencies and Exchange Rates

Supply of $ Created when U.S. Citizens sell dollars in the foreign exchange market in order to purchase foreign currency to purchase imports purchase foreign assets (stocks, bonds, real estate, etc.) Demand for $ Created when Foreign citizens buy dollars in the foreign exchange market with foreign currency to purchase U.S. exports purchase U.S. assets.

Demand for $ Created when Foreign citizens buy dollars in the foreign exchange market with foreign currency to. purchase U.S. exports. purchase U.S. assets.")

3

Currencies and Exchange Rates

Foreign Exchange Rates The price at which one currency exchanges for another. Currency depreciation A fall in the value of one currency in terms of another currency Makes imports more expensive Makes exports more affordable Currency appreciation A rise in value of one currency in terms of another currency.

4

1/EXUSEU = Euros/$ Current exchange rates at

5

The trade-weighted index is the average exchange rate of the U. S

The trade-weighted index is the average exchange rate of the U.S. dollar against other currencies, with individual currencies weighted by their importance in U.S. international trade. (Higher value implies stronger $)

")

6

What determines exchange rates? The Foreign Exchange Market

The Demand for One Currency Is the Supply of Another Currency Foreign citizens demanding U.S. dollars supply their own country’s money. Factors that influence the demand for U.S. dollars also influence the supply of foreign currencies. Factors that influence the demand for another country’s currency also influence the supply of U.S. dollars.

7

The Law of Demand for Foreign Exchange

Ceteris paribus, as the P of $ drops, quantity of $ demanded rises Exports effect As P of $ drops foreign citizens wish to purchase more U.S. exports quantity of $ demanded rises. Expected profit effect As P of $ drops, the larger the expected profit from buying U.S. assets quantity of $ demanded rises

9

The Law of Supply of Foreign Exchange

Ceteris paribus, as P of $ rises, the greater is the quantity of $ supplied in the foreign exchange market. Imports effect As P of $ rises, U.S. citizens increase imports and sell more $ to purchase more imports. Expected profit effect As P of $ rises, U.S. citizens see greater potential for profits in foreign assets and sell more $ to purchase more foreign assets.

11

The Foreign Exchange Market

Market Equilibrium If $ is “too strong”, surplus of $ If $ is “too weak”, shortage of $

12

Exchange Rate Fluctuations

Changes in exchange rate cause movement along the demand curve, NOT a change in demand. Changes in Demand for $ caused by: World demand for U.S. exports U.S. interest rate relative to the foreign interest rate Expected profits on U.S. assets relative to profits on foreign assets The expected future exchange rate

13

Exchange Rate Fluctuations

Changes in the exchange rate cause a movement along the supply curve, NOT a change in supply Changes in the supply of dollar are caused by: U.S. demand for imports U.S. interest rates relative to the foreign interest rate Expected profits on U.S. assets relative to profits on foreign assets The expected future exchange rate

14

Exchange Rate Fluctuations

Exchange Rate Expectations The exchange rate changes when it is expected to change. Expectations about the exchange rate are driven by deeper forces. Two such forces are Interest rate parity Purchasing power parity

15

Interest Rate Parity Expected $ return on investment in foreign currency = interest rate on foreign currency + expected change in value of foreign currency Interest rate parity exists when interest rates are such that expected returns on currencies are equal across countries. Market forces achieve interest rate parity very quickly. Example: U.S. interest rate=5%; German interest rate=8% What’s required for interest rate parity?

16

Interest Rate Parity Example: U.S. pays 5% interest; Japan pays 4% interest; Value of $ expected to appreciate by 3% over next year. Where will U.S. citizens buy bonds? Japanese buy bonds? Effect on interest rates in U.S. and Japan

17

Purchasing Power Parity

Exists when the exchange rate is such that a currency has the same “purchasing power” in all countries. If PPP did not exist, one could take advantage of “arbitrage” opportunities: buy item at low price and sell at high price drives up price in low price country and drives down price in high price country.

18

Purchasing Power Parity

Suppose $1 = 2 francs, price of gold=$500 in U.S. and 800 francs in France. What’s the arbitrage opportunity? What will happen to price of gold in U.S. France What will happen to price of $?

19

Purchasing Power Parity

In the long run, because of PPP: Exchange rate between foreign currency and dollar = price in foreign country / price in U.S. % ch in price of $ (exchange rate)= % ch in foreign price - % ch in U.S. prices

= % ch in foreign price - % ch in U.S. prices")

20

Financing International Trade

Balance of Payments Accounts Record a country’s international trading, borrowing, and lending. Transactions leading to an inflow of currency into the U.S. create a + (credit) in a balance of payments account Transactions leading to an outflow of currency from the U.S. create a – (debit) in a balance of payments account.

in a balance of payments account. Transactions leading to an outflow of currency from the U.S. create a – (debit) in a balance of payments account.")

21

Financing International Trade

Three balance of payments accounts Current account = NX + Net interest income + Net transfers Capital account =Foreign invest. in the U.S. - U.S. invest. abroad. Official settlements account records the change in U.S. official reserves. U.S. official reserves are the government’s holdings of foreign currency If U.S. official reserves increase, the official settlements account is negative. The sum of the three account balances is zero.

22

Financing International Trade

Borrowers and Lenders A net borrower has a current account deficit A net lender has a current account surplus The U.S. is currently a net borrower but during the 1960s and 1970s, the U.S. was a net lender.

24

Financing International Trade

Debtors and Creditors A debtor nation country that owes more than other countries owe to it. A creditor nation a country that owes less than other coutnries owe to it. Since 1986, the United States has been a debtor nation. Borrower/lender status based upon one year Debtor/creditor status based upon entire history of borrowing/lending.

25

Financing International Trade

Is being a net borrower “bad”? does not reduce long term economic growth if funds are used to finance capital accumulation can reduce economic growth if the borrowed funds are used to finance consumption. difficult to determine whether U.S. is borrowing for consumption or capital accumulation. Low savings rates in U.S. may be a concern.

26

Financing International Trade

Determinants of U.S. borrowing/lending from rest of world C+S+T=C+I+G+NX (T=net taxes) NX=(S-I) + (T-G) (S-I) = private sector balance (T-G) = public sector balance if balance>0, surplus if balance<0, deficit Ceteris paribus, U.S. borrowing from rest of world rises as public or private sector balance decreases

NX=(S-I) + (T-G) (S-I) = private sector balance. (T-G) = public sector balance. if balance>0, surplus. if balance<0, deficit. Ceteris paribus, U.S. borrowing from rest of world rises as public or private sector balance decreases.")

27

Financing International Trade

For the United States in 2010, Net exports were -$536 billion. Government sector balance was -$1,295 billion Private sector balance was $759 billion

28

Financing International Trade

The Three Sector Balances The private sector balance and the government sector balance tend to move in opposite directions. Net exports is the sum of the private sector and government sector balances.

29

Exchange Rate Policy Three possible exchange rate policies are

Flexible exchange rate Fixed exchange rate Crawling peg Flexible Exchange Rate A flexible exchange rate policy is one that permits the exchange rate to be determined by demand and supply with no direct intervention in the foreign exchange market by the central bank.

30

Exchange Rate Policy Fixed Exchange Rate pegs the exchange rate at a value decided by the government or central bank and that blocks the unregulated forces of demand and supply by direct intervention in the foreign exchange market. A fixed exchange rate requires active intervention in the foreign exchange market.

31

Exchange Rate Policy Suppose that the target is 100 yen per U.S. dollar. If demand increases, the central bank sells U.S. dollars to increase supply. Effect of “undervalued dollar” and subsequent intervention on 1. U.S. money supply? 2. U.S. Inflation?

32

Exchange Rate Policy If demand decreases, the central bank buys U.S. dollars (with foreign reserves) to decrease supply. Effect of “over-valued” dollar and subsequent intervention on: U.S. money supply and reserves of foreign currency U.S. inflation

33

Exchange Rate Policy Crawling Peg

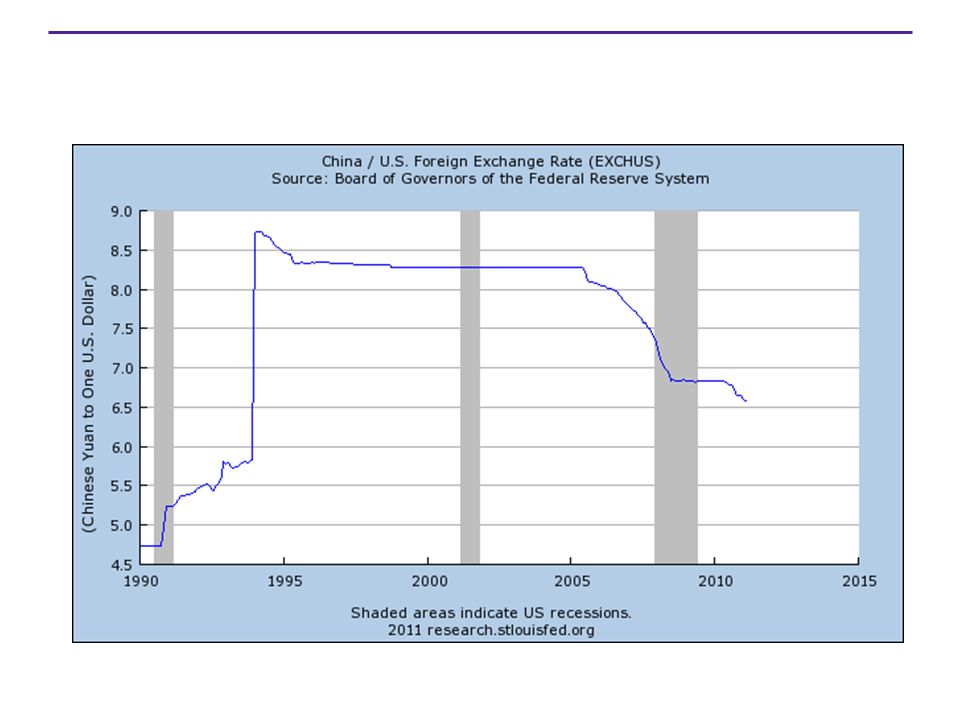

selects a target path for the exchange rate with intervention in the foreign exchange market to achieve that path. China is a country that operates a crawling peg. Crawling peg works like a fixed exchange rate except that the target value changes. Avoids wild swings in the exchange rate

35

Exchange Rate Policy The People’s bank buys U.S. dollars to maintain the target exchange rate. China’s official foreign reserves increase. Based on diagram, is $ over- or under-valued relative to Chinese Yuan?

36

Exchange Rate Policy People’s Bank of China in the Foreign exchange Market China’s official foreign currency reserves were rising until Stable and falling since. China will buy $ to drive up price of $; sell $ to drive down price of $.

37

Maintaining fixed exchange rates

If China wishes to maintain its exchange rate relative to the dollar, how will each of the following affect Chinese build-up of dollar reserves? An increase in inflation in China relative to U.S. inflation An increase in U.S. interest rates relative to China An increase in U.S. demand for Chinese exports. An increase in Chinese demand for U.S. exports

Similar presentations

S = I + (G-T) (Asset Market) There is only.>")