Download presentation

Presentation is loading. Please wait.

1

MONEY, BANKS, AND THE FEDERAL RESERVE

2

Objectives After studying this chapter, you will able to Explain why fiat money exists and why it is important Explain the economic functions of banks and other depository institutions and describe how they are regulated Explain how banks create money Describe the structure of the Federal Reserve System (the Fed), and the tools used by the Fed to conduct monetary policy Explain what an open market operation is, how it works, and how it changes the quantity of money and the interest rate

, and the tools used by the Fed to conduct monetary policy Explain what an open market operation is, how it works, and how it changes the quantity of money and the interest rate")

3

Why fiat money exists and why it is important? Double coincidence of wants problem Money is an implicit record of previous transactions If our capabilities of recording/recalling were unlimited, and if enforcement was free we would not need money Given limited recall and enforcement, money solves the problem of double coincidence of wants. As a result specialization becomes possible

4

How much money is out there? The two main official measures of money in the United States are M1 and M2. M1 consists of currency outside banks, traveler’s checks, and checking deposits owned by individuals and businesses. M2 consists of M1 plus time deposits, savings deposits, and money market mutual funds and other deposits.

5

Depository Institutions A depository institution is a firm that accepts deposits from households and firms and uses the deposits to make loans to other households and firms. A bank makes risky loans at an interest rate higher than that paid on deposits.

6

Financial Regulation, Deregulation, and Innovation Deposits are insured by the Federal Deposit Insurance Corporation (FDIC). This insurance guarantees deposits in amounts of up to $100,000 per depositor. This guarantee gives depository institutions the incentive to make risky loans because the depositors believe their funds to be perfectly safe; because of this incentive balance sheet regulations have been established.

7

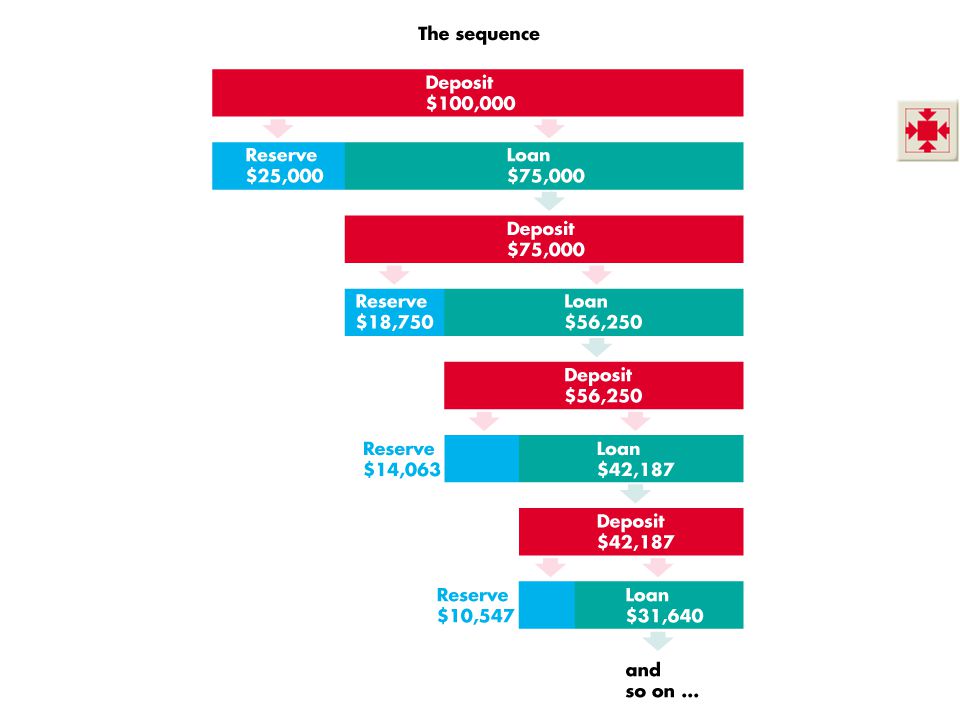

How Banks Create Money Reserves: Actual and Required The fraction of a bank’s total deposits held as reserves is the reserve ratio. The required reserve ratio is the fraction that banks are required, by regulation, to keep as reserves. Required reserves are the total amount of reserves that banks are required to keep. Excess reserves equal actual reserves minus required reserves.

8

How Banks Create Money Creating Deposits by Making Loans To see how banks create deposits by making loans, suppose the required reserve ratio is 25 percent. A new deposit of $100,000 is made. The bank keeps $25,000 in reserve and lends $75,000. This loan is credited to someone’s bank deposit. The person spends the deposit and another bank now has $75,000 of extra deposits. This bank keeps $18,750 on reserve and lends $56,250.

9

How Banks Create Money The process continues and keeps repeating with smaller and smaller loans at each “round.” Money creation = sum of all deposits

11

The Federal Reserve System The Federal Reserve System, or the Fed, is the central bank of the United States. A central bank is the public authority that regulates a nation’s depository institutions and controls the quantity of money.

12

The Federal Reserve System The Fed’s Goals and Targets The Fed conducts the nation’s monetary policy, which means that it adjusts the quantity of money in circulation. The Fed’s goals are to keep inflation in check, maintain full employment, moderate the business cycle, and contribute toward achieving long-term growth. In pursuit of its goals, the Fed pays close attention to interest rates and sets a target that is consistent with its goals for the federal funds rate, which is the interest rate that the banks charge each other on overnight loans of reserves.

13

The Federal Reserve System The Federal Open Market Committee (FOMC) is the main policy-making group in the Federal Reserve System. It consists of the members of the Board of Governors, the president of the Federal Reserve Bank of New York, and the 11 presidents of other regional Federal Reserve banks of whom, on a rotating basis, 4 are voting members. The FOMC meets every six weeks to formulate monetary policy.

14

The Federal Reserve System The Fed’s Policy Tools The Fed uses three monetary policy tools Required reserve ratios The discount rate Open market operations

15

The Federal Reserve System The Fed sets required reserve ratios, which are the minimum percentages of deposits that depository institutions must hold as reserves. The Fed does not change these ratios very often. The discount rate is the interest rate at which the Fed stands ready to lend reserves to depository institutions. An open market operation is the purchase or sale of government securities—U.S. Treasury bills and bonds—by the Federal Reserve System in the open market.

16

The Federal Reserve System The Fed’s Balance Sheet On the Fed’s balance sheet, the largest and most important asset is U.S. government securities. The most important liabilities are Federal Reserve notes in circulation and banks’ deposits.

17

Controlling the Quantity of Money How Required Reserve Ratios Work An increase in the required reserve ratio boosts the reserves that banks must hold, decreases their lending. As funds become scarce interest rates have a tendency to increase. (a lowering of the required reserve has a symmetric impact whereby interest rates end up going down) How the Discount Rate Works An increase in the discount rate raises the cost of borrowing reserves from the Fed. Thus, the costs of lending go up and interest rates have a tendency to go up.

How the Discount Rate Works An increase in the discount rate raises the cost of borrowing reserves from the Fed. Thus, the costs of lending go up and interest rates have a tendency to go up..")

18

Controlling the Quantity of Money How an Open Market Operation Works When the Fed conducts an open market operation by buying a government security, it increases banks’ reserves. Banks loan the excess reserves. By making loans, they create money. The reverse occurs when the Fed sells a government security.

19

Controlling the Quantity of Money Bank Reserves and the Money Multiplier The money multiplier total increase (per dollar) in the money supply that results of a one dollar change in the available stock of money.

in the money supply that results of a one dollar change in the available stock of money.")

20

Controlling the Quantity of Money The Multiplier Effect of an Open Market Operation When the Fed conducts an open market operation, the ultimate change in the money supply is larger than the initiating open market operation. Banks use excess reserves from the open market operation to make loans so that the banks where the loans are deposited acquire excess reserves which they, in turn, then loan.

21

Controlling the Quantity of Money Multiplier effect of an open market operation.

23

Controlling the Quantity of Money The Size of the Multiplier The multiplier effects on the money supply are negatively related to: 1)The required reserve ratio 2)The fraction of currency that does not go back to the banking system

The required reserve ratio 2)The fraction of currency that does not go back to the banking system")

24

Discussion on Monetary policy and the nominal interest rate The Fed trades T-bills and in doing so it affects their price The price of a bond is inversely related to the implicit interest rate it pays Implicit interest of a bond = Face value of the T-Bill/Price paid for the T-bill Hence, open market operations affect the interest rate paid by bonds

Similar presentations