Download presentation

Presentation is loading. Please wait.

1

INVESTMENT BANKING LESSON 13 DOING A DISCOUNTED FREE CASH FLOW ANALYSIS Investment Banking (2 nd edition) Beijing Language and Culture University Press, 2013 Investment Banking for Dummies, Matthew Krantz, Robert R. Johnson,Wiley & Sons, 2014

2

WHAT’S IN THE NEWS OR WHAT’S THERE TO LEARN? SHANGHAI OPENS FIRST PRIVATE BANK! THE TOP 10 HIGHEST PAID WHITE- COLLAR JOBS IN CHINA

3

VOCABULARY REVIEW – WHAT DO THESE WORDS MEAN? Bond indenture Fixed income securities Types of bonds: convertiblecallableputtable floating ratezero-coupon Seniority

4

VOCABULARY REVIEW – WHAT DO THESE WORDS MEAN? Bond trustee Yield to Maturity Premium Discount Default risk

5

VOCABULARY PREVIEW – This lesson Present value and discount rate Discounted free cash flow Free cash flows (FCF) Weighted average cost of capital (WACC) Capital expenditures

Weighted average cost of capital (WACC) Capital expenditures")

6

A. INTRODUCTION B. DISCOUNTED FREE CASH FLOW 1. Computing Free Cash Flow (FCF) 2. Forecasting (predicting free cash flow) C. CALCULATING THE WIGHTED AVERAGE COST OF CAPITAL (WACC)

C. CALCULATING THE WIGHTED AVERAGE COST OF CAPITAL (WACC).")

7

D. MEASURING THE COST OF DEBT AND EQUITY 1. Cost of Debt 2. Cost of Equity a. Build-up method b. Capital Asset Pricing Model (CAPM) – just mentioned but not examined E. THE VALUE OF A COMPANY USING DISCOUNTED FREE CASH FLOW ANALYSIS

– just mentioned but not examined E. THE VALUE OF A COMPANY USING DISCOUNTED FREE CASH FLOW ANALYSIS.")

8

Financial models are the foundation of IB. IB make big pay by showing companies (CEO’s, management) that by issuing or buying back securities, going public or going private, buying companies or make changes in the way the way the company operates, the value of the company can be increased.

that by issuing or buying back securities, going public or going private, buying companies or make changes in the way the way the company operates, the value of the company can be increased..")

9

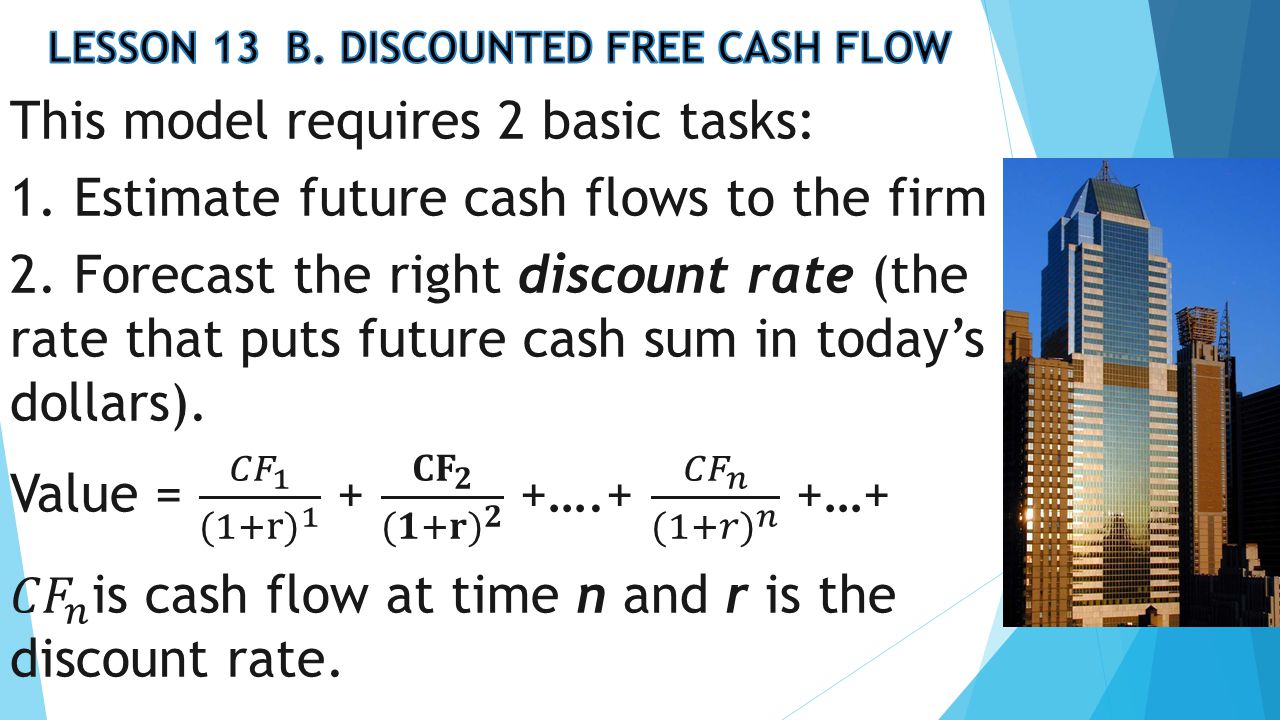

The financial value of any company is based on its ability to generate positive cash flow. Financial models are built on the idea that the value of any firm is present value of all future cash flows. This lesson presents the financial model that IB use: the discounted free cash flow model.

11

The formula is the math way of saying, the value of any asset is the present value of all future cash flows. The value of a company is made by a model that estimates free cash flows and discounts them back to the present with a discount rate called the weighted average cost of capital (WACC).

..")

12

What is Free Cash Flow (FCF)? The amount of cash flow from operations (CFO) remaining after paying for capital expenditures. CFO is cash flow from business operations that doesn’t include one time items such as a sale of a building or part of a company.

remaining after paying for capital expenditures. CFO is cash flow from business operations that doesn’t include one time items such as a sale of a building or part of a company..")

13

Capital expenditures are investments a company must make to replace assets that are worn out or need replacing. Interest expense is added back (net of taxes). Net of taxes means that interest on debt payments tax deductible. FCF=CFO+interest expense (1-tax rate) – capital expenditures Free cash flow (FCF) = Cash flow from operations (CFO)

. Net of taxes means that interest on debt payments tax deductible. FCF=CFO+interest expense (1-tax rate) – capital expenditures Free cash flow (FCF) = Cash flow from operations (CFO).")

15

Sample: Free Cash Flow from the most recent year for IBM. IBM for the year ended December 31, 2012 Income statement itemAmount (in millions of $) Cash flow from operations$19,586 Payments for property, plant and equipment (capital expenditures)($4,082) Amount from sale of property, plant and equipment $410 Investments and acquisitions($3,123) From EDGAR we see IBM paid $1,022 million of interest to debt holders in 2012 and a tax rate of 24%

Cash flow from operations$19,586 Payments for property, plant and equipment (capital expenditures)($4,082) Amount from sale of property, plant and equipment $410 Investments and acquisitions($3,123) From EDGAR we see IBM paid $1,022 million of interest to debt holders in 2012 and a tax rate of 24%.")

16

Let’s compute the free cash flow: 1. Add cash flow from operations to after tax interest $19,586. After-tax interest is $1,022 x (1-.24) = $777. $19,586 + $777 = $20,363 2. Subtract payments for capital expenditures $20,363-$4,082 = $16,281 3. Add amount from sale of capital expenditures $16,281 + $410 = $16,691 4. Subtract investments and acquisitions $16,691-$3,123 = $13,568 Current Cash Flow for IBM is $13,568 million (13.6 billion)

= $777. $19,586 + $777 = $20, Subtract payments for capital expenditures $20,363-$4,082 = $16, Add amount from sale of capital expenditures $16,281 + $410 = $16, Subtract investments and acquisitions $16,691-$3,123 = $13,568 Current Cash Flow for IBM is $13,568 million (13.6 billion).")

17

It’s easy to get the past, not so with the future. Valuation models aren’t based on the past but on expected future cash flows. To forecast free cash flow (FCF) means forecasting cash flow from operations. Forecasting FCF: (with help from IS) Cash flow from operations = Earnings before Interest & Taxes + depreciation – taxes

means forecasting cash flow from operations. Forecasting FCF: (with help from IS) Cash flow from operations = Earnings before Interest & Taxes + depreciation – taxes.")

18

To get earnings before interest and taxes, analysts must predict sales and cost of goods. In essence, this means forecasting the entire income statement: Sales Less: cost of sales Gross profit Less: General expenses Earnings before Interest/taxes Less: interest Earnings before taxes Less:taxes Net Income

19

The Weighted Average Cost of Capital (WACC) is the average rate of return of a company’s suppliers of capital and the rate at which the future cash flows are discounted bask to present value for valuing a company. The higher the WACC the lower the value of the firm cause the cost of capital is too high.

21

Why is the WACC so important? WACC is an estimate of the cost of funding for a firm. This is critical for internal operations and planning of the firm. If the managers – with help from IB – can look for opportunities to invest in projects that return more than the cost of capital, the value of the firm will increase. This is how wealth is created.

22

From what you know about IB now what other projects or ideas can you think that will help a company create more wealth and grow? Think like an IB. Brainstorm with a partner for a few minutes.

23

1. Start a new product line 2. Expand a current product line 3. Buy a product line from a competitor 4. Or just buy another competitor If a firm can get funds at a cost of 8% & earn 12% on those funds, the value of the firm will increase and stockholders will be happy. Are you beginning to see the critical role that IB play in helping companies expand and grow? What is so good about that?

24

To get the WACC an IB must first estimate ALL the costs of capital – the cost of debt & cost of equity. The cost of debt is easy, equity not so. 1. COST OF DEBT CAPITAL Bond values are easy to find through the bond market. So analysts will have to calculate an average among all the firm’s bonds.

25

But, in America, because debt can be deducted on taxes that must be considered. After-tax cost of debt=before-tax cost of debt x(1-tax rate) If average yield to maturity is 8% and the firm’s tax rate is 30%, the after-tax-cost of debt is: After-tax cost of debt = 8% x (1 - 0.3) = 5.6%

If average yield to maturity is 8% and the firm’s tax rate is 30%, the after-tax-cost of debt is: After-tax cost of debt = 8% x ( ) = 5.6%.")

26

2. COST OF EQUITY CAPITAL – Determining the right rate of return on equity is the most difficult part of completing a discounted cash flow analysis. Because there is so much risk in investing there is an old saying about investment: “You can eat well or you can sleep well!”

27

2. COST OF EQUITY CAPITAL – There are 2 ways to calculate the cost of equity capital: a. BUILD-UP METHOD – used for smaller, private firms b. CAPITAL ASSET PRICING MODEL – for large publicly-traded firms but we will not look at this as for many analysts it is just a starting point in measuring equity.

28

2. COST OF EQUITY CAPITAL - a. BUILD-UP METHOD: Starts with risk-free capital (yield on long-term US Treasury securities) and then adding risk premiums, of which there are three. Current yields on long-term government bonds are 3.2%. i. Market risk - see table of past returns from last 85 years (11.77-6.14) = 5.63% ii. Size premium-(16.51-11.77) = 4.74% iii. Other premium – This is one the analyst uses their own judgment. Assume 2%

and then adding risk premiums, of which there are three. Current yields on long-term government bonds are 3.2%. i. Market risk - see table of past returns from last 85 years ( ) = 5.63% ii. Size premium-( ) = 4.74% iii. Other premium – This is one the analyst uses their own judgment. Assume 2%.")

29

Annual returns for assets (1926-2011) Asset classReturnStandard deviation Large stocks11.77%20.30% Small stocks16.51%32.51% Long-term Corp bonds 6.36% 8.35% Long-term Govt bonds 6.14% 9.78% Medium-term Govt bonds 5.54% 5.67% Treasury bills 3.62% 3.10%

Asset classReturnStandard deviation Large stocks11.77%20.30% Small stocks16.51%32.51% Long-term Corp bonds 6.36% 8.35% Long-term Govt bonds 6.14% 9.78% Medium-term Govt bonds 5.54% 5.67% Treasury bills 3.62% 3.10%")

30

Now, let’s apply the following formula: Cost of equity = risk-free rate + market risk premium + size premium + other premium Cost of Equity = 3.2% + 5.63% + 4.74% + 2% = 15.57% Unlike the cost of debt, there is no tax break for equity.

31

We’ve seen how to calculate free cash flows (FCF) & the weighted average cost of capital (WACC) so now let’s put the formula to use and determine how IB get the value of a company. We’ll take a complicate formula and make it simple. How so?

Similar presentations