Download presentation

Presentation is loading. Please wait.

1

Chapter 5

2

The Time Value of Money

3

Simple Interest n Interest is earned on principal n $100 invested at 6% per year n 1 st yearinterest is $6.00 n 2 nd yearinterest is $6.00 n 3 rd year interest is $6.00 n Total interest earned:$18

4

Compound Interest n Interest is earned on previously earned interest n $100 invested at 6% with annual compounding n 1 st yearinterest is $6.00Principal is $106 n 2 nd yearinterest is $6.36Principal is $112.36 n 3 rd yearinterest is $6.74Principal is $119.11 n Total interest earned: $19.10

5

We know that receiving $1 today is worth more than $1 in the future. This is due to opportunity costs. The opportunity cost of receiving $1 in the future is the interest we could have earned if we had received the $1 sooner. Today Future

6

If we can measure this opportunity cost, we can: n Translate $1 today into its equivalent in the future (compounding). n Translate $1 in the future into its equivalent today (discounting). ? Today Future Today ? Future

. Today Future Today . Future.")

7

Future Value

8

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 1 year? 0 1 PV = FV =

9

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 1 year? Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 1 PV = -100 N = 1 PV = -100 FV = $106 FV = $106 0 1 0 1 PV = -100 FV =

10

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 1 year? Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 1 PV = -100 N = 1 PV = -100 FV = $106 FV = $106 0 1 0 1 PV = -100 FV = 106

11

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 1 year? Mathematical Solution: FV = PV (1 + i) n FV = 100 (1.06) 1 = $106 0 1 0 1 PV = -100 FV = 106

n FV = 100 (1.06) 1 = $ PV = -100 FV = 106.")

12

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 5 years? Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 5 PV = -100 N = 5 PV = -100 FV = $133.82 FV = $133.82 0 5 0 5 PV = -100 FV =

13

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 5 years? Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 5 PV = -100 N = 5 PV = -100 FV = $133.82 FV = $133.82 0 5 0 5 PV = -100 FV = 133. 82

14

Future Value - single sums If you deposit $100 in an account earning 6%, how much would you have in the account after 5 years? Mathematical Solution: FV = PV (1 + i) n FV = 100 (1.06) 5 = $ 133.82 0 5 0 5 PV = -100 FV = 133. 82

n FV = 100 (1.06) 5 = $ PV = -100 FV =")

15

Future Value - single sums If you deposit $100 in an account earning 6% with quarterly compounding, how much would you have in the account after 5 years?

16

0 ? PV = FV =

17

Calculator Solution: Calculator Solution: P/Y = 4I = 6 P/Y = 4I = 6 N = 20 PV = -100 N = 20 PV = -100 FV = $134.68 FV = $134.68 0 20 0 20 PV = -100 FV = Future Value - single sums If you deposit $100 in an account earning 6% with quarterly compounding, how much would you have in the account after 5 years?

18

Calculator Solution: Calculator Solution: P/Y = 4I = 6 P/Y = 4I = 6 N = 20 PV = -100 N = 20 PV = -100 FV = $134.68 FV = $134.68 0 20 0 20 PV = -100 FV = 134. 68 Future Value - single sums If you deposit $100 in an account earning 6% with quarterly compounding, how much would you have in the account after 5 years?

19

Mathematical Solution: FV = PV (1 + i/m) m x n FV = 100 (1.015) 20 = $134.68 0 20 0 20 PV = -100 FV = 134. 68 Future Value - single sums If you deposit $100 in an account earning 6% with quarterly compounding, how much would you have in the account after 5 years?

20

Future Value - single sums If you deposit $100 in an account earning 6% with monthly compounding, how much would you have in the account after 5 years?

21

0 ? PV = FV =

22

Calculator Solution: Calculator Solution: P/Y = 12I = 6 P/Y = 12I = 6 N = 60 PV = -100 N = 60 PV = -100 FV = $134.89 FV = $134.89 0 60 0 60 PV = -100 FV = Future Value - single sums If you deposit $100 in an account earning 6% with monthly compounding, how much would you have in the account after 5 years?

23

Calculator Solution: Calculator Solution: P/Y = 12I = 6 P/Y = 12I = 6 N = 60 PV = -100 N = 60 PV = -100 FV = $134.89 FV = $134.89 0 60 0 60 PV = -100 FV = 134. 89 Future Value - single sums If you deposit $100 in an account earning 6% with monthly compounding, how much would you have in the account after 5 years?

24

Mathematical Solution: FV = PV (1 + i/m) m x n FV = 100 (1.005) 60 = $134.89 0 60 0 60 PV = -100 FV = 134. 89 Future Value - single sums If you deposit $100 in an account earning 6% with monthly compounding, how much would you have in the account after 5 years?

25

Future Value - continuous compounding What is the FV of $1,000 earning 8% with continuous compounding, after 100 years?

26

0 ? PV = FV =

27

Mathematical Solution: Mathematical Solution: FV = PV (e in ) FV = PV (e in ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = $2,980,957.87 FV = $2,980,957.87 0 100 0 100 PV = -1000 FV = Future Value - continuous compounding What is the FV of $1,000 earning 8% with continuous compounding, after 100 years?

FV = PV (e in ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = $2,980, FV = $2,980, PV = FV = Future Value - continuous compounding What is the FV of $1,000 earning 8% with continuous compounding, after 100 years")

28

0 100 0 100 PV = -1000 FV = $2.98m Future Value - continuous compounding What is the FV of $1,000 earning 8% with continuous compounding, after 100 years? Mathematical Solution: Mathematical Solution: FV = PV (e in ) FV = PV (e in ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = $2,980,957.87 FV = $2,980,957.87

FV = PV (e in ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = 1000 (e.08x100 ) = 1000 (e 8 ) FV = $2,980, FV = $2,980,")

29

Continuous Compounding Calculator Keystrokes n 8 n 2 nd n e x =2,980.96 x 1,000 = 2,980,957.87 x 1,000 = 2,980,957.87

30

Present Value

31

Present Value - single sums If you receive $100 one year from now, what is the PV of that $100 if your opportunity cost is 6%?

32

0 ? PV = FV =

33

Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 1 FV = 100 N = 1 FV = 100 PV = -94.34 PV = -94.34 0 1 0 1 PV = FV = 100 Present Value - single sums If you receive $100 one year from now, what is the PV of that $100 if your opportunity cost is 6%?

34

Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 1 FV = 100 N = 1 FV = 100 PV = -94.34 PV = -94.34 Present Value - single sums If you receive $100 one year from now, what is the PV of that $100 if your opportunity cost is 6%? PV = -94. 34 FV = 100 0 1 0 1

35

Mathematical Solution: PV = FV / (1 + i) n PV = 100 / (1.06) 1 = $94.34 Present Value - single sums If you receive $100 one year from now, what is the PV of that $100 if your opportunity cost is 6%? PV = -94. 34 FV = 100 0 1 0 1

36

Present Value - single sums If you receive $100 five years from now, what is the PV of that $100 if your opportunity cost is 6%?

37

0 ? PV = FV =

38

Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 5 FV = 100 N = 5 FV = 100 PV = -74.73 PV = -74.73 0 5 0 5 PV = FV = 100 Present Value - single sums If you receive $100 five years from now, what is the PV of that $100 if your opportunity cost is 6%?

39

Calculator Solution: Calculator Solution: P/Y = 1I = 6 P/Y = 1I = 6 N = 5 FV = 100 N = 5 FV = 100 PV = -74.73 PV = -74.73 Present Value - single sums If you receive $100 five years from now, what is the PV of that $100 if your opportunity cost is 6%? 0 5 0 5 PV = -74. 73 FV = 100

40

Mathematical Solution: PV = FV / (1 + i) n PV = 100 / (1.06) 5 = $74.73 Present Value - single sums If you receive $100 five years from now, what is the PV of that $100 if your opportunity cost is 6%? 0 5 0 5 PV = -74. 73 FV = 100

41

Present Value - single sums What is the PV of $1,000 to be received 15 years from now if your opportunity cost is 7%?

42

0 15 0 15 PV = FV =

43

Calculator Solution: Calculator Solution: P/Y = 1I = 7 P/Y = 1I = 7 N = 15 FV = 1,000 N = 15 FV = 1,000 PV = -362.45 PV = -362.45 Present Value - single sums What is the PV of $1,000 to be received 15 years from now if your opportunity cost is 7%? 0 15 0 15 PV = FV = 1000

44

Calculator Solution: Calculator Solution: P/Y = 1I = 7 P/Y = 1I = 7 N = 15 FV = 1,000 N = 15 FV = 1,000 PV = -362.45 PV = -362.45 Present Value - single sums What is the PV of $1,000 to be received 15 years from now if your opportunity cost is 7%? 0 15 0 15 PV = -362. 45 FV = 1000

45

Mathematical Solution: PV = FV / (1 + i) n PV = 1000/ (1.07) 15 = $362.45 Present Value - single sums What is the PV of $1,000 to be received 15 years from now if your opportunity cost is 7%? 0 15 0 15 PV = -362. 45 FV = 1000

46

Present Value - single sums If you sold land for $11,933 that you bought 5 years ago for $5,000, what is your annual rate of return?

47

0 5 0 5 PV = FV =

48

Calculator Solution: Calculator Solution: P/Y = 1N = 5 P/Y = 1N = 5 PV = -5,000 FV = 11,933 PV = -5,000 FV = 11,933 I = 19% I = 19% 0 5 0 5 PV = -5000 FV = 11,933 Present Value - single sums If you sold land for $11,933 that you bought 5 years ago for $5,000, what is your annual rate of return?

49

Mathematical Solution: PV = FV / (1 + i) n PV = FV / (1 + i) n 5,000 = 11,933 / (1+ i) 5 5,000 = 11,933 / (1+ i) 5.419 = ((1/ (1+i) 5 ).419 = ((1/ (1+i) 5 ) 2.3866 = (1+i) 5 2.3866 = (1+i) 5 (2.3866) 1/5 = (1+i) i =.19 (2.3866) 1/5 = (1+i) i =.19 Present Value - single sums If you sold land for $11,933 that you bought 5 years ago for $5,000, what is your annual rate of return?

n PV = FV / (1 + i) n 5,000 = 11,933 / (1+ i) 5 5,000 = 11,933 / (1+ i) = ((1/ (1+i) 5 ).419 = ((1/ (1+i) 5 ) = (1+i) = (1+i) 5 (2.3866) 1/5 = (1+i) i =.19 (2.3866) 1/5 = (1+i) i =.19 Present Value - single sums If you sold land for $11,933 that you bought 5 years ago for $5,000, what is your annual rate of return")

50

Hint for single sum problems: n In every single sum future value and present value problem, there are 4 variables: n FV, PV, i, and n n When doing problems, you will be given 3 of these variables and asked to solve for the 4th variable. n Keeping this in mind makes “time value” problems much easier!

51

The Time Value of Money Compounding and Discounting Cash Flow Streams 01 234

52

Annuities n Annuity: a sequence of equal cash flows, occurring at the end of each period.

53

01 234 Annuities

54

Examples of Annuities: n If you buy a bond, you will receive equal semi-annual coupon interest payments over the life of the bond. n If you borrow money to buy a house or a car, you will pay a stream of equal payments.

55

n If you buy a bond, you will receive equal semi-annual coupon interest payments over the life of the bond. n If you borrow money to buy a house or a car, you will pay a stream of equal payments. Examples of Annuities:

56

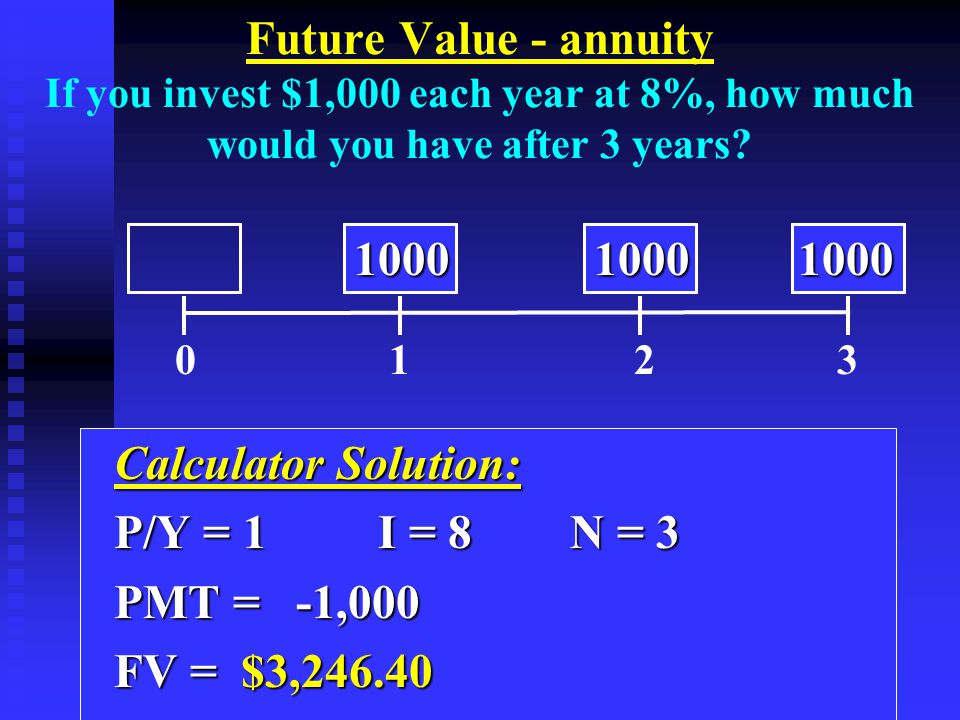

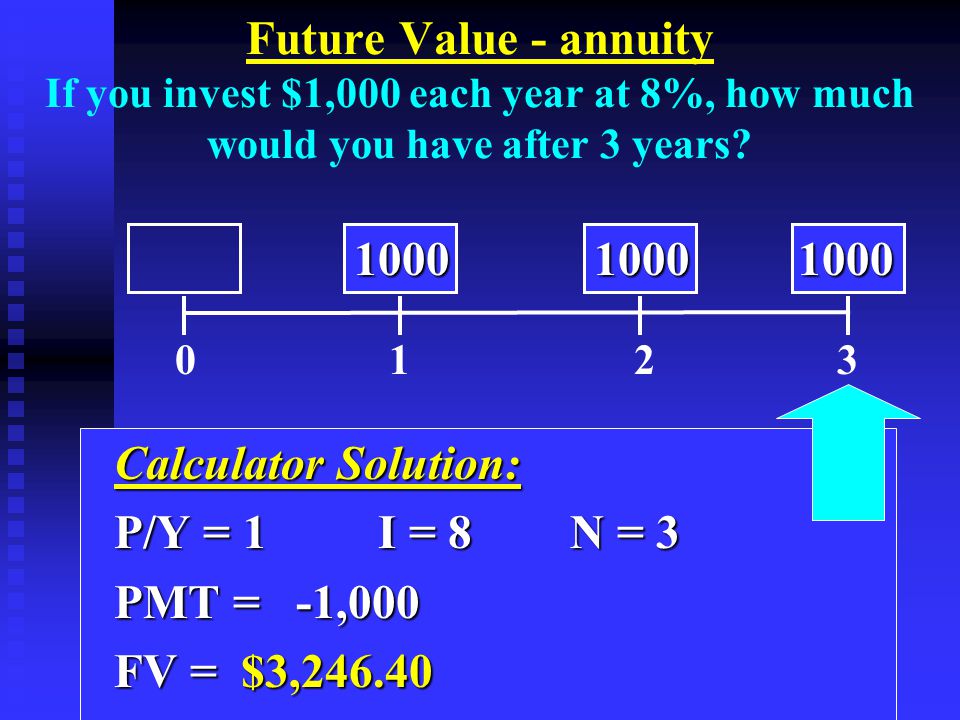

Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years?

57

0 1 2 3

58

Calculator Solution: Calculator Solution: P/Y = 1I = 8N = 3 P/Y = 1I = 8N = 3 PMT = -1,000 PMT = -1,000 FV = $3,246.40 FV = $3,246.40 Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years? 0 1 2 3 10001000 1000 10001000 1000

59

Calculator Solution: Calculator Solution: P/Y = 1I = 8N = 3 P/Y = 1I = 8N = 3 PMT = -1,000 PMT = -1,000 FV = $3,246.40 FV = $3,246.40 Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years? 0 1 2 3 10001000 1000 10001000 1000

60

Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years?

61

Mathematical Solution: FV = PMT (1 + i) n - 1 i FV = 1,000 (1.08) 3 - 1 = $3246.40.08.08 Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years?

n - 1 i FV = 1,000 (1.08) = $ Future Value - annuity If you invest $1,000 each year at 8%, how much would you have after 3 years")

62

Present Value - annuity What is the PV of $1,000 at the end of each of the next 3 years, if the opportunity cost is 8%?

63

0 1 2 3

64

Calculator Solution: Calculator Solution: P/Y = 1I = 8N = 3 P/Y = 1I = 8N = 3 PMT = -1,000 PMT = -1,000 PV = $2,577.10 PV = $2,577.10 0 1 2 3 10001000 1000 10001000 1000 Present Value - annuity What is the PV of $1,000 at the end of each of the next 3 years, if the opportunity cost is 8%?

65

Calculator Solution: Calculator Solution: P/Y = 1I = 8N = 3 P/Y = 1I = 8N = 3 PMT = -1,000 PMT = -1,000 PV = $2,577.10 PV = $2,577.10 0 1 2 3 10001000 1000 10001000 1000 Present Value - annuity What is the PV of $1,000 at the end of each of the next 3 years, if the opportunity cost is 8%?

66

Mathematical Solution: 1 1 PV = PMT 1 - (1 + i) n i 1 PV = 1000 1 - (1.08 ) 3 = $2,577.10.08.08 Present Value - annuity What is the PV of $1,000 at the end of each of the next 3 years, if the opportunity cost is 8%?

n i 1 PV = (1.08 ) 3 = $2, Present Value - annuity What is the PV of $1,000 at the end of each of the next 3 years, if the opportunity cost is 8%")

67

Other Cash Flow Patterns 0123 The Time Value of Money

68

Perpetuities n Suppose you will receive a fixed payment every period (month, year, etc.) forever. This is an example of a perpetuity. n You can think of a perpetuity as an annuity that goes on forever.

69

PMT i PV = n The PV of a perpetuity is very simple to find: Present Value of a Perpetuity

70

What should you be willing to pay in order to receive $10,000 annually forever, if you require 8% per year on the investment?

71

PMT $10,000 PMT $10,000 i.08 i.08 PV = =

72

What should you be willing to pay in order to receive $10,000 annually forever, if you require 8% per year on the investment? PMT $10,000 PMT $10,000 i.08 i.08 = $125,000 PV = =

73

Ordinary Annuity vs. Annuity Due $1000 $1000 $1000 4 5 6 7 8

74

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8

75

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 5 6 7

76

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 5 6 7 PVinENDMode

77

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 5 6 7 PVinENDModeFVinENDMode

78

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 6 7 8

79

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 6 7 8 PVinBEGINMode

80

Begin Mode vs. End Mode 1000 1000 1000 4 5 6 7 8 year year year 6 7 8 PVinBEGINModeFVinBEGINMode

81

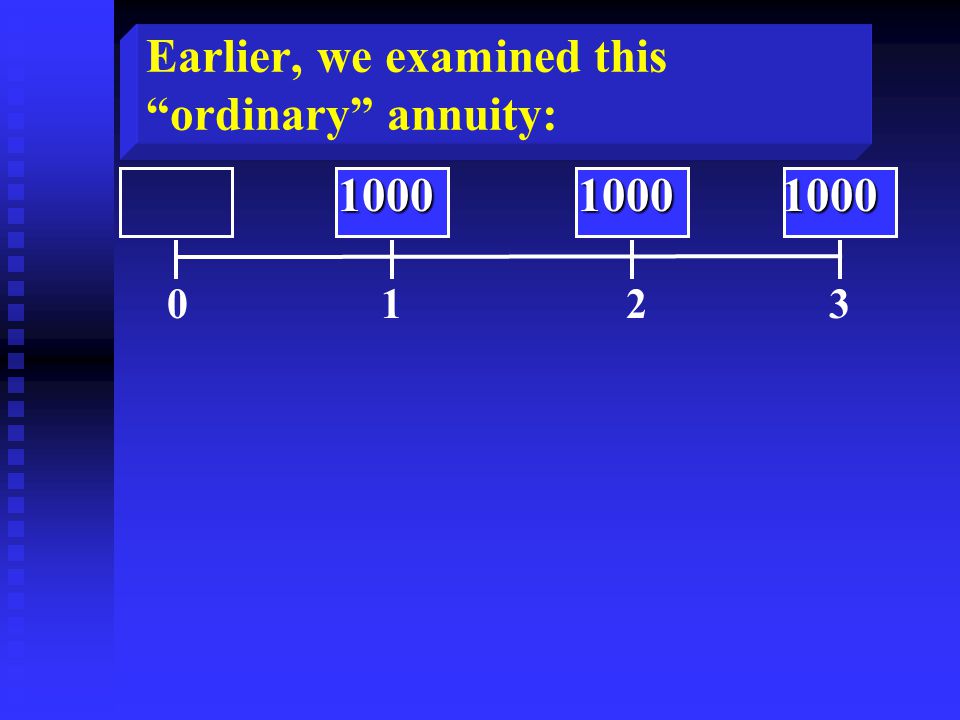

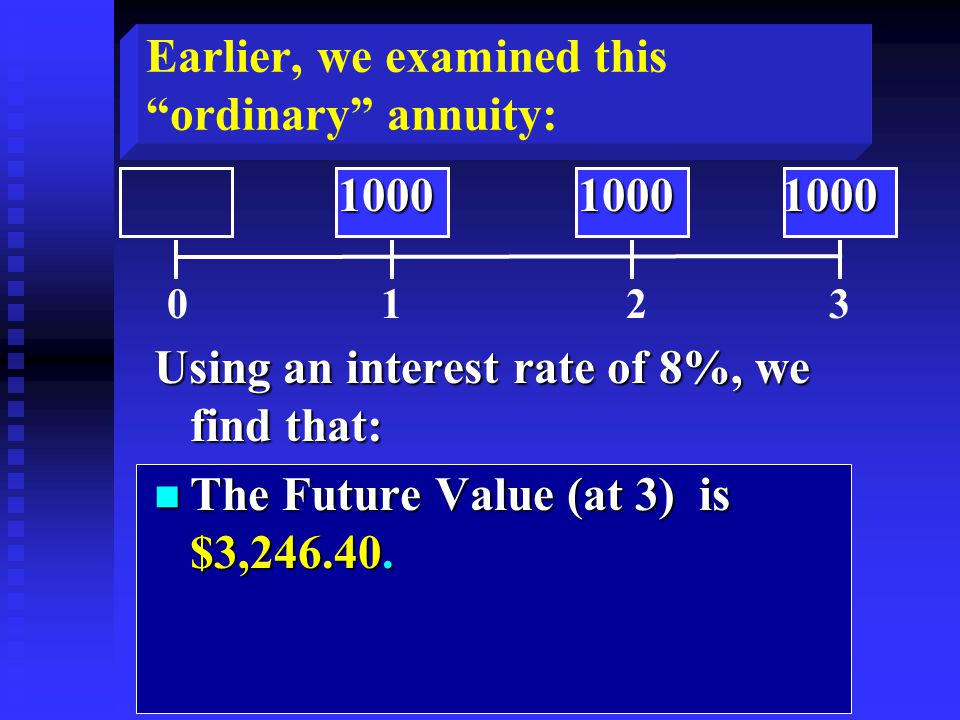

Earlier, we examined this “ordinary” annuity:

82

0 1 2 3 10001000 1000 10001000 1000

83

Earlier, we examined this “ordinary” annuity: Using an interest rate of 8%, we find that: 0 1 2 3 10001000 1000 10001000 1000

84

Earlier, we examined this “ordinary” annuity: Using an interest rate of 8%, we find that: n The Future Value (at 3) is $3,246.40. 0 1 2 3 10001000 1000 10001000 1000

85

Earlier, we examined this “ordinary” annuity: Using an interest rate of 8%, we find that: n The Future Value (at 3) is $3,246.40. n The Present Value (at 0) is $2,577.10. 0 1 2 3 10001000 1000 10001000 1000

is $2,")

86

n Is this an annuity? n How do we find the PV of a cash flow stream when all of the cash flows are different? (Use a 10% discount rate). Uneven Cash Flows 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000

. Uneven Cash Flows ,000 2,000 4,000 6,000 7,000.")

87

n Sorry! There’s no quickie for this one. We have to discount each cash flow back separately. 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000 Uneven Cash Flows

88

n Sorry! There’s no quickie for this one. We have to discount each cash flow back separately. 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000 Uneven Cash Flows

89

n Sorry! There’s no quickie for this one. We have to discount each cash flow back separately. 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000 Uneven Cash Flows

90

n Sorry! There’s no quickie for this one. We have to discount each cash flow back separately. 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000 Uneven Cash Flows

91

n Sorry! There’s no quickie for this one. We have to discount each cash flow back separately. 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000 Uneven Cash Flows

92

period CF PV (CF) period CF PV (CF) 0-10,000 -10,000.00 0-10,000 -10,000.00 1 2,000 1,818.18 1 2,000 1,818.18 2 4,000 3,305.79 2 4,000 3,305.79 3 6,000 4,507.89 3 6,000 4,507.89 4 7,000 4,781.09 4 7,000 4,781.09 PV of Cash Flow Stream: $ 4,412.95 0 1 2 3 4 -10,000 2,000 4,000 6,000 7,000

period CF PV (CF) 0-10, , , , ,000 1, ,000 1, ,000 3, ,000 3, ,000 4, ,000 4, ,000 4, ,000 4, PV of Cash Flow Stream: $ 4, ,000 2,000 4,000 6,000 7,000")

93

Example n Cash flows from an investment are expected to be $40,000 per year at the end of years 4, 5, 6, 7, and 8. If you require a 20% rate of return, what is the PV of these cash flows?

94

Example 012345678012345678012345678012345678 $0 0 0 04040404040 n Cash flows from an investment are expected to be $40,000 per year at the end of years 4, 5, 6, 7, and 8. If you require a 20% rate of return, what is the PV of these cash flows?

95

n This type of cash flow sequence is often called a “deferred annuity.” 012345678012345678012345678012345678 $0 0 0 04040404040

96

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

97

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

98

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

99

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

100

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

101

How to solve: 1) Discount each cash flow back to time 0 separately. 012345678012345678012345678012345678 $0 0 0 04040404040

102

How to solve: 1) Discount each cash flow back to time 0 separately. Or, 012345678012345678012345678012345678 $0 0 0 04040404040

103

2) Find the PV of the annuity: PV : End mode; P/YR = 1; I = 20; PMT = 40,000; N = 5 PV = $119,624 012345678012345678012345678012345678 $0 0 0 04040404040

Find the PV of the annuity: PV : End mode; P/YR = 1; I = 20; PMT = 40,000; N = 5 PV = $119, $")

104

2) Find the PV of the annuity: PV 3: End mode; P/YR = 1; I = 20; PMT = 40,000; N = 5 PV 3 = $119,624 012345678012345678012345678012345678 $0 0 0 04040404040

Find the PV of the annuity: PV 3: End mode; P/YR = 1; I = 20; PMT = 40,000; N = 5 PV 3 = $119, $")

105

119,624 012345678012345678012345678012345678

106

Then discount this single sum back to time 0. PV: End mode; P/YR = 1; I = 20; N = 3; FV = 119,624; Solve: PV = $69,226 119,624 012345678012345678012345678012345678 $0 0 0 04040404040

107

69,226 012345678012345678012345678012345678 119,624

108

n The PV of the cash flow stream is $69,226. 69,226 012345678012345678012345678012345678 $0 0 0 04040404040 119,624

109

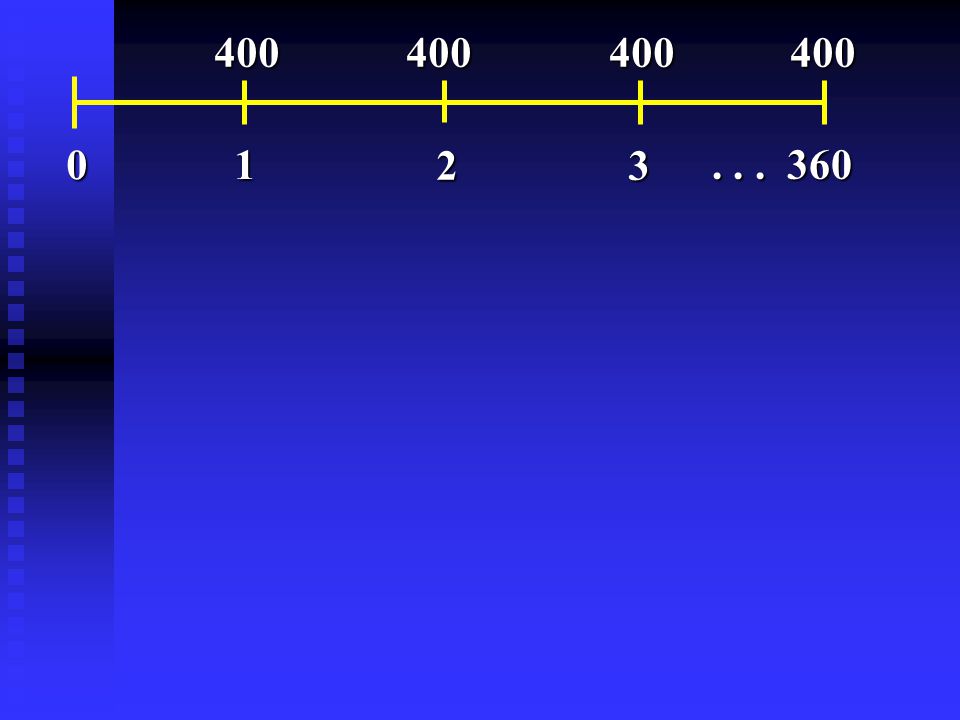

Retirement Example n After graduation, you plan to invest $400 per month in the stock market. If you earn 12% per year on your stocks, how much will you have accumulated when you retire in 30 years?

110

Retirement Example n After graduation, you plan to invest $400 per month in the stock market. If you earn 12% per year on your stocks, how much will you have accumulated when you retire in 30 years? 01 23... 360 400 400 400 400

111

01 23... 360 400 400 400 400

112

n Using your calculator, P/YR = 12 P/YR = 12 N = 360 PMT = -400 I%YR = 12 FV = $1,397,985.65 01 23... 360 400 400 400 400

113

Retirement Example If you invest $400 at the end of each month for the next 30 years at 12%, how much would you have at the end of year 30? Mathematical Solution: FV = PMT (1 + i) n - 1 FV = PMT (1 + i) n - 1 i FV = 400 (1.01) 360 - 1 = $1,397,985.65 FV = 400 (1.01) 360 - 1 = $1,397,985.65.01.01

n - 1 FV = PMT (1 + i) n - 1 i FV = 400 (1.01) = $1,397, FV = 400 (1.01) = $1,397,")

114

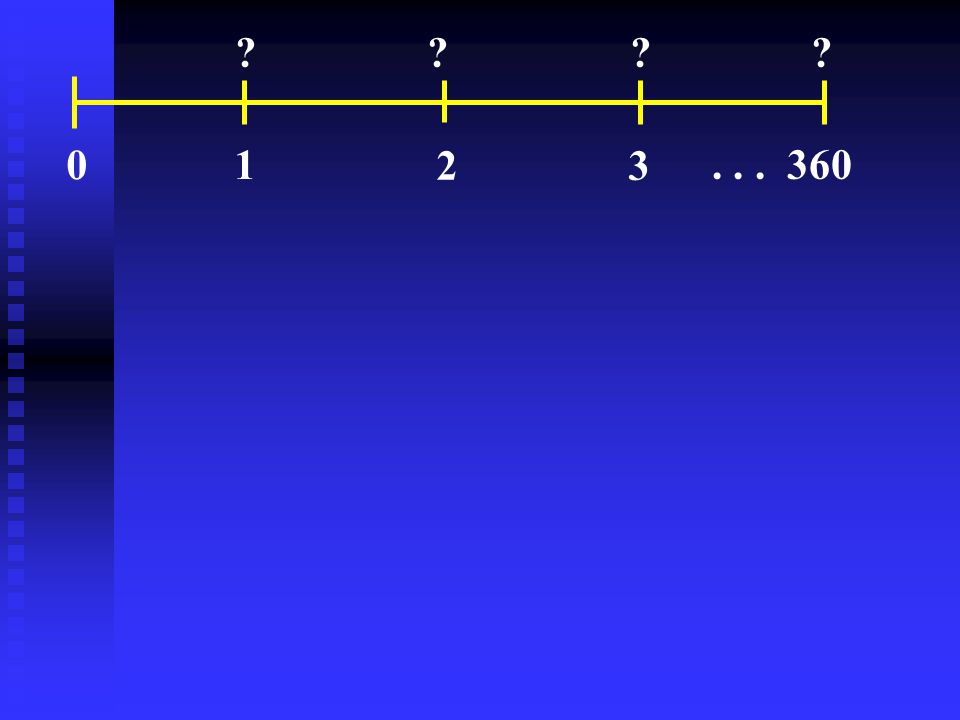

If you borrow $100,000 at 7% fixed interest for 30 years in order to buy a house, what will be your monthly house payment? House Payment Example

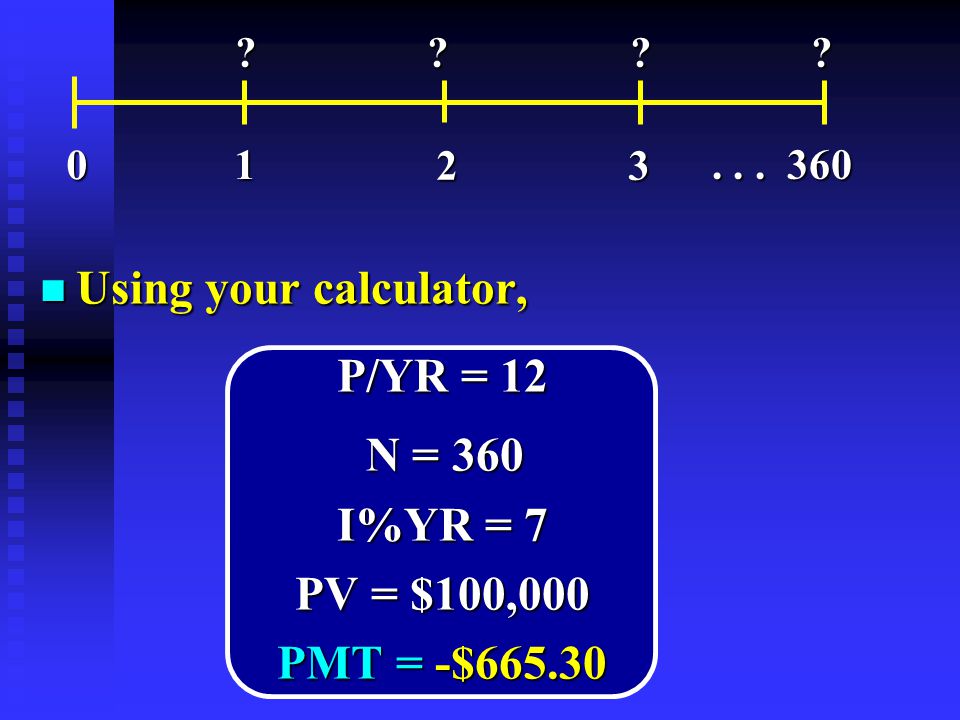

115

If you borrow $100,000 at 7% fixed interest for 30 years in order to buy a house, what will be your monthly house payment?

116

01 23... 360 ? ? ? ?

117

n Using your calculator, P/YR = 12 N = 360 N = 360 I%YR = 7 PV = $100,000 PMT = -$665.30 01 23... 360 ? ? ? ? ? ? ? ?

118

House Payment Example Mathematical Solution: 1 1 PV = PMT 1 - (1 + i) n i 1 100,000 = PMT 1 - (1.005833 ) 360 PMT=$665.30.005833.005833

n i 1 100,000 = PMT 1 - ( ) 360 PMT=$")

119

Team Assignment Upon retirement, your goal is to spend 5 years traveling around the world. To travel in style will require $250,000 per year at the beginning of each year. If you plan to retire in 30 years, what are the equal monthly payments necessary to achieve this goal? The funds in your retirement account will compound at 10% annually.

120

n How much do we need to have by the end of year 30 to finance the trip? n PV 30 = PMT (PVIFA.10, 5 ) (1.10) = = 250,000 (3.7908) (1.10) = = 250,000 (3.7908) (1.10) = = $1,042,470 = $1,042,470 272829303132333435 250 250 250 250 250 250 250 250 250 250

(1.10) = = 250,000 (3.7908) (1.10) = = 250,000 (3.7908) (1.10) = = $1,042,470 = $1,042,")

121

Using your calculator, Mode = BEGIN PMT = -$250,000 PMT = -$250,000 N = 5 I%YR = 10 P/YR = 1 PV = $1,042,466 272829303132333435 250 250 250 250 250 250 250 250 250 250

122

n Now, assuming 10% annual compounding, what monthly payments will be required for you to have $1,042,466 at the end of year 30? 272829303132333435 250 250 250 250 250 250 250 250 250 2501,042,466

123

Using your calculator, Mode = END N = 360 N = 360 I%YR = 10 P/YR = 12 FV = $1,042,466 PMT = -$461.17 272829303132333435 250 250 250 250 250 250 250 250 250 2501,042,466

124

n So, you would have to place $461.17 in your retirement account, which earns 10% annually, at the end of each of the next 360 months to finance the 5-year world tour.

Similar presentations